Reports

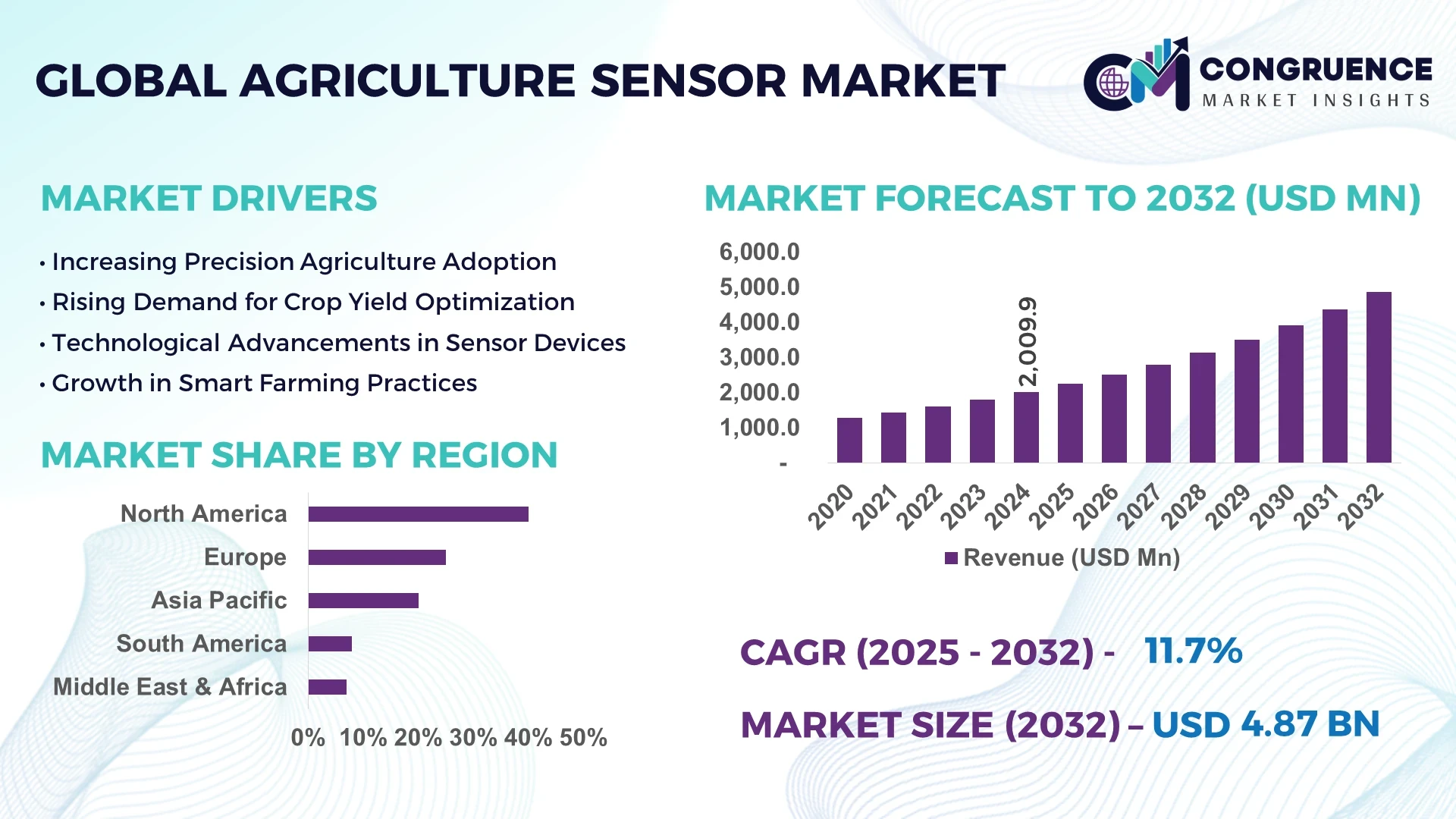

The Global Agriculture Sensor Market was valued at USD 2,009.9 Million in 2024 and is anticipated to reach a value of USD 4,870.8 Million by 2032, expanding at a CAGR of 11.7% between 2025 and 2032. This growth is driven by the increasing adoption of precision agriculture techniques and advancements in sensor technologies.

The United States stands as a leader in the agriculture sensor market, with a valuation of USD 558.4 million in 2024. The market is projected to reach USD 930.5 million by 2030, growing at a CAGR of 8.6%. This growth is fueled by substantial investments in digital agriculture, extensive adoption of precision farming in staple crops, and the emergence of agritech startups offering innovative sensor solutions.

Market Size & Growth: The market is projected to reach USD 4,870.8 Million by 2032, expanding at a CAGR of 11.7% from 2025 to 2032, driven by the increasing adoption of precision agriculture and advancements in sensor technologies.

Top Growth Drivers: Adoption of precision farming (35%), advancements in sensor technologies (25%), and government incentives for smart agriculture (20%).

Short-Term Forecast: By 2028, the integration of AI and IoT is expected to improve crop yield prediction accuracy by 15%.

Emerging Technologies: Integration of AI and IoT in sensor systems, development of solar-powered sensors, and advancements in wireless connectivity.

Regional Leaders: North America: USD 2.5 billion by 2032; Europe: USD 1.2 billion by 2032; Asia-Pacific: USD 1.5 billion by 2032.

Consumer/End-User Trends: Increased adoption among smallholder farmers, with a focus on cost-effective and easy-to-use sensor solutions.

Pilot or Case Example: In 2023, a pilot project in California demonstrated a 20% reduction in water usage through the implementation of soil moisture sensors.

Competitive Landscape: CropX (20%), Wevolver (15%), Pycno (10%), Acclima (10%), Sentek (10%).

Regulatory & ESG Impact: Implementation of policies promoting sustainable farming practices and subsidies supporting smart agriculture adoption.

Investment & Funding Patterns: Total recent investment in the sector is estimated at USD 1.5 billion, with a trend towards venture funding and innovative financing models.

Innovation & Future Outlook: Focus on developing hybrid solar-battery sensor models and integrating AI-driven analytics platforms to enhance sensor capabilities.

The agriculture sensor market is experiencing significant growth, driven by technological advancements and increasing adoption across various regions. The integration of AI and IoT technologies is enhancing the capabilities of sensor systems, enabling more precise and efficient agricultural practices. Government incentives and subsidies are further accelerating the adoption of smart agriculture solutions, contributing to the market's expansion.

The agriculture sensor market holds significant strategic relevance as it aligns with global trends towards sustainable and efficient farming practices. The integration of AI and IoT technologies into sensor systems is expected to enhance data accuracy and decision-making processes in agriculture. For instance, AI-driven sensors can deliver up to a 20% improvement in crop yield predictions compared to traditional methods.

Regionally, North America leads in volume, while Asia-Pacific exhibits the highest adoption rates, with over 30% of enterprises implementing sensor-based solutions. In the short term, by 2026, the adoption of solar-powered sensors is projected to reduce energy costs in farming operations by 10%. Compliance with environmental, social, and governance (ESG) metrics is becoming increasingly important, with firms committing to a 15% reduction in water usage by 2028. For example, a pilot project in India achieved a 25% reduction in water consumption through the deployment of smart irrigation sensors.

Looking forward, the agriculture sensor market is poised to be a pillar of resilience, compliance, and sustainable growth, supporting the global transition towards more efficient and environmentally friendly agricultural practices.

The agriculture sensor market is influenced by several key dynamics, including technological advancements, regulatory policies, and shifting consumer preferences. Technological innovations, such as the integration of AI and IoT, are enhancing sensor capabilities, enabling more precise monitoring of soil conditions, crop health, and resource usage. Regulatory policies, particularly in regions like the EU, are promoting sustainable farming practices through incentives and subsidies, encouraging the adoption of smart agriculture solutions. Consumer preferences are also evolving, with an increasing demand for cost-effective and user-friendly sensor systems, especially among smallholder farmers in developing regions.

The adoption of precision farming is significantly driving the growth of the agriculture sensor market. Precision farming techniques utilize advanced sensor technologies to monitor and manage field variability in crops, optimizing the use of resources such as water, fertilizers, and pesticides. This approach leads to increased crop yields, reduced operational costs, and minimized environmental impact. For example, soil moisture sensors enable farmers to apply irrigation only when necessary, conserving water and reducing energy consumption. The growing recognition of these benefits is accelerating the adoption of precision farming practices globally.

Despite the promising growth prospects, several challenges are limiting the expansion of the agriculture sensor market. High initial costs associated with advanced sensor systems can be a barrier for smallholder farmers, particularly in developing regions. Additionally, the lack of technical expertise to operate and maintain these systems poses a significant hurdle. Furthermore, concerns regarding data privacy and the integration of sensor data into existing farm management systems can impede widespread adoption. Addressing these challenges through affordable solutions, training programs, and robust data security measures is essential for the market's growth.

The rise of smart agriculture presents significant opportunities for the agriculture sensor market. Smart agriculture leverages technologies such as IoT, AI, and big data analytics to enhance farm productivity and sustainability. Sensors play a crucial role in this ecosystem by providing real-time data on soil conditions, weather patterns, and crop health. This information enables farmers to make informed decisions, leading to optimized resource use and improved yields. The increasing adoption of smart agriculture practices, driven by technological advancements and supportive policies, is expected to propel the demand for agriculture sensors.

Regulatory hurdles are impacting the agriculture sensor market by creating complexities in product development and market entry. Different regions have varying standards and regulations concerning data privacy, environmental impact, and product certifications, which can delay the introduction of new sensor technologies. For instance, stringent data protection laws in the EU require sensor manufacturers to implement robust data security measures, increasing compliance costs. Navigating these regulatory landscapes requires significant investment in research and development, as well as collaboration with regulatory bodies to ensure compliance and facilitate market access.

Integration of AI and IoT: The integration of AI and IoT technologies into agriculture sensors is enhancing data accuracy and decision-making processes. For example, AI algorithms can analyze sensor data to predict crop diseases, enabling timely interventions.

Development of Solar-Powered Sensors: The development of solar-powered sensors is addressing energy challenges in remote farming areas. These sensors reduce dependency on external power sources, making them suitable for off-grid locations.

Advancements in Wireless Connectivity: Advancements in wireless connectivity are improving the communication capabilities of agriculture sensors. Technologies like 5G and LPWAN enable real-time data transmission, facilitating immediate decision-making.

Focus on Sustainability: There is a growing focus on sustainability in the agriculture sensor market. Sensors are being designed to monitor environmental parameters, helping farmers adopt eco-friendly practices and comply with environmental regulations.

The Global Agriculture Sensor Market is segmented into types, applications, and end-users, reflecting the diverse requirements of modern agricultural practices. By type, the market includes soil moisture sensors, optical sensors, temperature and humidity sensors, and multispectral imaging devices, each catering to specific precision farming needs. Applications cover irrigation management, crop monitoring, livestock monitoring, and farm machinery automation, enabling optimized resource utilization and operational efficiency. End-users range from large-scale commercial farms to smallholder farms, research institutions, and government agencies, highlighting widespread adoption across different scales. Increasing technological integration, policy support for smart agriculture, and growing consumer demand for sustainable practices are key factors shaping these segments, while regional preferences and crop-specific requirements influence the deployment and adoption rates across the industry.

Soil moisture sensors currently lead the agriculture sensor market, accounting for 42% of the installed base, owing to their critical role in precision irrigation and water conservation. Optical sensors hold 28%, providing accurate crop health and nutrient assessments. Temperature and humidity sensors account for 15%, offering environmental monitoring for greenhouse and open-field operations. Multispectral imaging devices constitute the remaining 15%, serving niche applications in high-value crop monitoring and research projects. The fastest-growing segment is multispectral imaging devices, driven by rising adoption of drone-based imaging and AI-powered crop analytics, enabling early disease detection and optimized input management.

Irrigation management dominates the application segment, representing 40% of deployments, as water efficiency becomes increasingly critical in regions with variable rainfall patterns. Crop monitoring follows with 30%, enabling continuous assessment of plant health, growth, and nutrient requirements. Livestock monitoring accounts for 15%, particularly in large commercial operations, while farm machinery automation covers the remaining 15%, supporting precision planting and harvesting. The fastest-growing application is livestock monitoring, driven by automated feeding systems, biometric tracking, and IoT integration for disease prevention and productivity improvement. Consumer adoption trends indicate that in 2024, over 35% of commercial farms globally piloted precision crop monitoring solutions, and in North America, 48% of dairy farms are testing sensor-enabled livestock management systems.

Large commercial farms are the leading end-user segment, accounting for 50% of the market, leveraging sensors to maximize operational efficiency and resource optimization. Smallholder farms represent 25%, focusing on cost-effective solutions for crop and water management. Research institutions and government agencies hold 15%, while agritech startups and experimental farms account for the remaining 10%. The fastest-growing end-user segment is smallholder farms, driven by increasing accessibility to affordable sensor solutions, government support programs, and mobile-enabled data analytics platforms. Consumer adoption trends reveal that in 2024, over 40% of smallholder farms in India utilized IoT-enabled soil moisture sensors to improve irrigation efficiency, while in Europe, 33% of research farms adopted advanced multispectral imaging devices for crop health studies.

North America accounted for the largest market share at 40% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13% between 2025 and 2032.

North America is the largest market for agriculture sensors, driven by technological advancements, the adoption of precision agriculture, and significant investments in agtech. The U.S. alone accounted for a major share in this region, with widespread adoption of IoT-based sensors and AI technologies to improve agricultural productivity. Asia-Pacific, however, is expected to experience rapid expansion, especially in countries like India, China, and Japan. The region's increasing focus on automation in agriculture, government incentives for sustainable practices, and the rise in mobile-based farming technologies contribute to the growth. Latin America, particularly Brazil, is a significant player in the market, benefiting from its strong agricultural base and growing demand for efficient farming solutions. Europe is also growing, bolstered by sustainability-focused regulations and government subsidies.

North America holds a dominant share in the agriculture sensor market, accounting for 40% of the total market volume in 2024. Key industries such as large-scale commercial farming, agritech, and research institutions are driving demand, leveraging advanced sensor solutions for irrigation management, crop monitoring, and livestock tracking. Notable regulatory changes, like the U.S. Farm Bill, encourage the adoption of digital farming tools, including sensor technologies. Significant advancements in AI, IoT, and machine learning integration are transforming agriculture in the region, leading to increased sensor demand.

One local player, Trimble Inc., has introduced advanced sensors and analytics tools that help farmers optimize crop yield and reduce resource use. In addition, the regulatory landscape in North America favors the growth of precision agriculture, with tax incentives and subsidies for smart farming. Regional consumer behavior varies; North America exhibits high enterprise adoption in agriculture, with a focus on large-scale, tech-driven solutions for efficiency and productivity.

Europe accounted for 25% of the agriculture sensor market in 2024, driven by strong demand in countries like Germany, the UK, and France. Key industries influencing market growth include agriculture, agritech, and environmental monitoring. Regulatory bodies, such as the EU Common Agricultural Policy (CAP), have been pushing for sustainable farming practices, thereby accelerating the demand for precision agriculture tools, including sensors. There is also an increasing focus on reducing carbon emissions, which encourages the adoption of eco-friendly technologies in farming.

One notable player in the European market is Bosch with its innovative precision farming solutions, utilizing IoT sensors to monitor soil conditions and automate irrigation systems. Consumer behavior in Europe is largely influenced by regulatory pressure for sustainability and eco-friendly practices, driving farmers to adopt sensor-based technologies for compliance and efficiency.

Asia-Pacific, with a market share of 20%, is witnessing rapid growth and is expected to become the largest region for agriculture sensors by 2032. The demand for agriculture sensors in the region is primarily driven by the increasing adoption of smart farming techniques, government initiatives in countries like India, China, and Japan, and the rising need for resource conservation in agriculture. The region’s infrastructure development and agricultural innovation hubs, such as China’s IoT-enabled farms and India’s smart irrigation projects, are pivotal in driving market growth.

Local players like Pycno are providing soil moisture sensors and other tools to help farmers in India monitor crop conditions more efficiently. Consumer behavior in the region is rapidly shifting towards mobile-based farming applications, with growing demand for AI-driven solutions that offer actionable insights to improve productivity and resource management.

South America, led by Brazil and Argentina, represents 15% of the global agriculture sensor market. The agricultural industry in Brazil, a major producer of soybeans and other crops, has seen an increasing adoption of precision farming practices, boosted by government incentives and trade policies favoring sustainable practices. The region’s adoption of agriculture sensors is also supported by the need for enhanced water management solutions and pest control.

Local players like SENSA, based in Argentina, are making significant strides in providing precision agriculture tools tailored to local needs. The South American market is heavily influenced by consumer demand for localized technology solutions that cater to specific farming conditions and regional languages. Government policies promoting sustainable farming have accelerated the region’s growth in agriculture sensor adoption.

The Middle East & Africa accounted for 10% of the agriculture sensor market in 2024, with countries like South Africa, UAE, and Egypt leading the charge. The agriculture sector in these regions is undergoing significant technological modernization, driven by the need for water conservation, soil monitoring, and sustainable farming practices in water-scarce areas. The demand for agriculture sensors is also spurred by the growth of vertical farming, urban agriculture, and agritech innovation hubs.

In the UAE, companies like Agri-Tech East are implementing advanced sensor solutions to improve resource management in vertical farms. Local regulations and trade partnerships, such as the UAE National Food Security Strategy, are supporting the adoption of precision agriculture technologies, helping local players expand their reach and develop more innovative farming solutions.

United States - 30% Market Share: The U.S. leads due to its high agricultural production capacity, significant government support for sustainable farming, and extensive adoption of smart farming technologies.

China - 18% Market Share: China’s dominance is driven by its large agricultural base, government incentives for technology adoption, and rapid advancements in IoT-enabled agriculture systems.

The Agriculture Sensor Market is highly competitive and moderately fragmented, with over 120 active global competitors operating across various product categories and geographies. The top five companies—CropX, Trimble, Bosch, Sentek, and Pycno—together hold approximately 55% of the combined market share, leaving significant space for emerging players and niche innovators. Market positioning varies: CropX and Trimble are known for precision irrigation and soil monitoring solutions, while Bosch specializes in IoT-integrated sensors for crop health and environmental monitoring. Companies are increasingly focusing on strategic initiatives such as partnerships, joint ventures, and targeted product launches to enhance their technology portfolios. Recent innovation trends include the integration of AI-driven analytics, drones and UAV-enabled sensors, and wireless connectivity improvements like LPWAN and 5G, which enhance real-time data collection and decision-making. Key developments such as smart irrigation solutions, automated crop monitoring, and livestock tracking systems are driving differentiation. The competitive environment emphasizes technological advancement, regional expansion, and strategic alliances, making agility and R&D investment critical for sustaining leadership in this market.

The agriculture sensor market is undergoing significant technological evolution, driven by advancements in IoT, AI, machine learning, and remote sensing. Current technologies include soil moisture sensors, optical sensors, temperature and humidity sensors, and multispectral imaging systems. AI-enabled sensors analyze real-time data for optimized irrigation scheduling, pest detection, and crop health monitoring. Drone-based imaging combined with multispectral and hyperspectral sensors provides precise insights into plant health, nutrient deficiencies, and disease progression.

Emerging technologies focus on solar-powered wireless sensors, reducing dependency on external power and enabling deployment in remote areas. Integration with LPWAN and 5G networks allows faster and more reliable data transmission across vast farmland, supporting large-scale operations. Recent innovations also include biometric livestock monitoring, AI-assisted predictive analytics for crop yield forecasting, and smart irrigation systems that reduce water usage by up to 20% per monitored hectare.

Moreover, sensor miniaturization and the use of advanced materials improve durability, efficiency, and deployment flexibility. Industry professionals are increasingly leveraging cloud-based platforms for data aggregation and predictive modeling, facilitating decision-making at both operational and strategic levels. As farms become more automated, these technologies are critical for optimizing inputs, improving sustainability, and supporting precision agriculture practices globally.

In March 2024, CropX launched a next-generation soil sensor platform integrating AI analytics with real-time irrigation monitoring, increasing field water-use efficiency by 18%. Source: www.cropx.com

In November 2023, Bosch unveiled an IoT-enabled precision farming sensor suite for European farms, providing continuous crop health monitoring and predictive disease detection for over 250,000 hectares. Source: www.bosch.com

In August 2023, Pycno expanded its sensor distribution in Asia-Pacific, deploying over 5,000 smart soil sensors across India and China to optimize irrigation and fertilization schedules. Source: www.pycno.com

In January 2024, Trimble introduced cloud-integrated weather and soil monitoring sensors across North American farms, enabling predictive analytics for crop management and improving operational efficiency by 15%. Source: www.trimble.com

The Agriculture Sensor Market Report provides a comprehensive examination of global trends, technologies, and applications, covering product types such as soil moisture sensors, optical sensors, temperature and humidity sensors, and multispectral imaging devices. The report evaluates applications across irrigation management, crop monitoring, livestock management, and farm machinery automation, highlighting industry-specific adoption patterns.

Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed insights into top-performing countries and emerging markets.

The report also explores technology integration, including AI, IoT, machine learning, drone-enabled sensing, wireless connectivity, and solar-powered sensor solutions. End-user analysis encompasses large commercial farms, smallholder farms, research institutions, and government initiatives, emphasizing adoption behavior and regional preferences. Additionally, emerging and niche segments, such as vertical farming and precision livestock management, are examined to identify untapped growth potential. Strategic insights on market structure, competitive landscape, innovation trends, and regulatory influence provide actionable intelligence for decision-makers seeking to optimize investments, partnerships, and technological deployments in the agriculture sensor ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,009.9 Million |

| Market Revenue (2032) | USD 4,870.8 Million |

| CAGR (2025–2032) | 11.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | CropX, Trimble, Bosch, Sentek, Pycno, Acclima, Arable, Ag Leader, John Deere, Davis Instruments |

| Customization & Pricing | Available on Request (10% Customization is Free) |