Reports

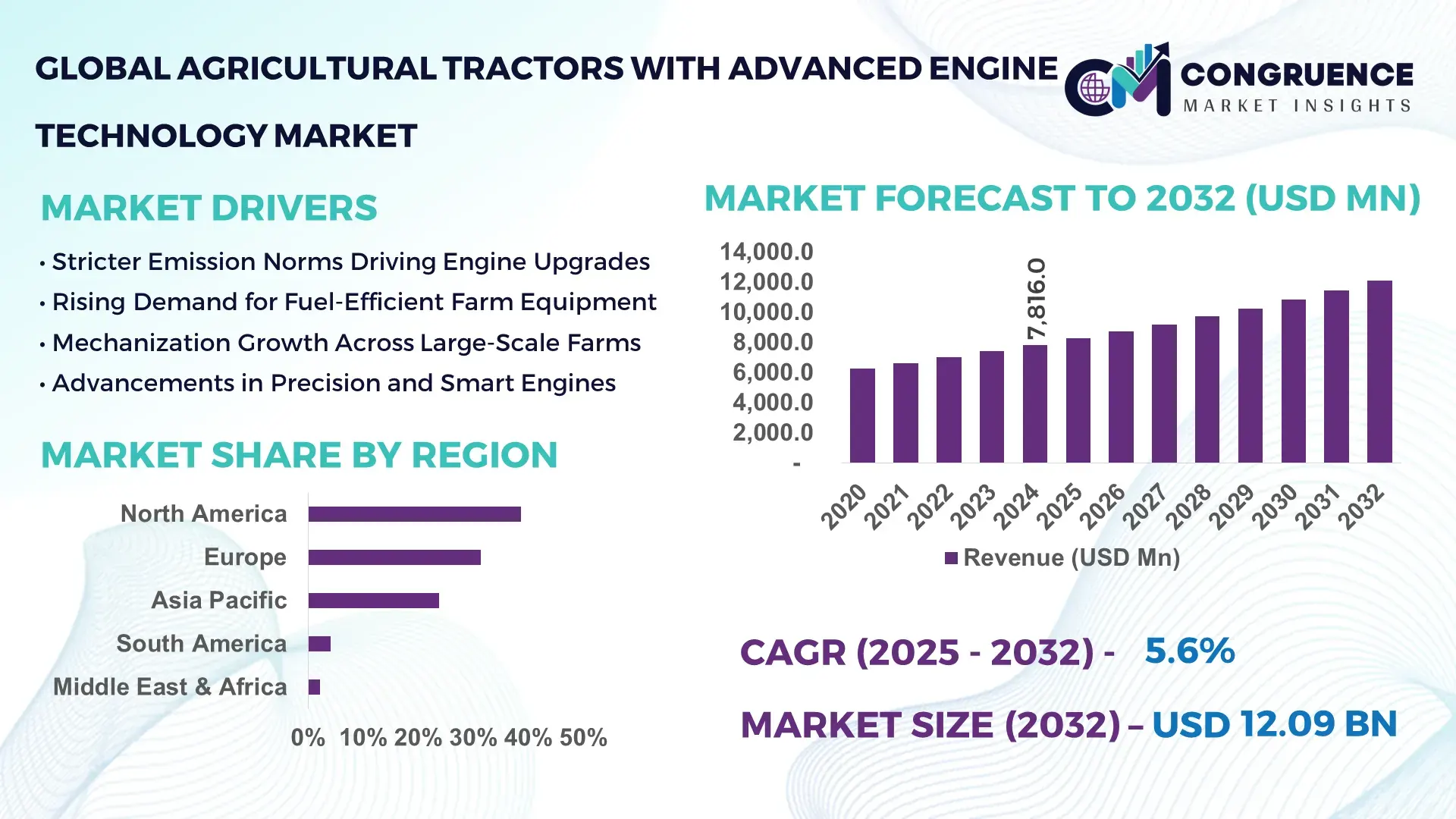

The Global Agricultural Tractors with Advanced Engine Technology Market was valued at USD 7,816.0 Million in 2024 and is anticipated to reach a value of USD 12,086.4 Million by 2032, expanding at a CAGR of 5.6% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is supported by increasing adoption of fuel-efficient, low-emission tractor engines aligned with evolving agricultural productivity and sustainability requirements.

The United States represents the dominant country in the Agricultural Tractors with Advanced Engine Technology Market, driven by strong domestic manufacturing capacity and rapid technology integration. The country produces over 300,000 agricultural tractors annually, supported by advanced engine R&D investments exceeding USD 2.1 billion per year across OEMs and component suppliers. Tier 4 Final–compliant engines are now deployed in more than 85% of newly sold mid-to-high horsepower tractors, reflecting widespread adoption of advanced combustion, exhaust after-treatment, and electronic fuel management systems. Precision agriculture applications account for nearly 62% of advanced-engine tractor usage, while autonomous and semi-autonomous tractor pilots have expanded across over 18 million acres of U.S. farmland.

Market Size & Growth: Valued at USD 7,816.0 million in 2024, projected to reach USD 12,086.4 million by 2032, growing at a CAGR of 5.6% due to rising demand for efficient, low-emission farm mechanization.

Top Growth Drivers: Emission-compliant engine adoption (68%), fuel efficiency improvement (22%), precision farming integration (41%).

Short-Term Forecast: By 2028, advanced engine tractors are expected to reduce fuel consumption per hectare by 14%.

Emerging Technologies: Hybrid diesel-electric drivetrains, AI-enabled engine control units, hydrogen-ready combustion systems.

Regional Leaders: North America (USD 3,960 million by 2032, high horsepower adoption), Europe (USD 3,120 million, emission-driven upgrades), Asia Pacific (USD 3,480 million, rapid mechanization).

Consumer/End-User Trends: Large commercial farms account for 58% of deployments, with rising uptake among contract farming operators.

Pilot or Case Example: In 2023, a U.S. Midwest pilot using AI-optimized engines achieved 11% productivity gains.

Competitive Landscape: Deere & Company (~32%), CNH Industrial, AGCO Corporation, Kubota, Mahindra & Mahindra.

Regulatory & ESG Impact: Stricter emission norms driving 25% faster engine replacement cycles.

Investment & Funding Patterns: Over USD 4.6 billion invested globally in advanced tractor engine innovation since 2021.

Innovation & Future Outlook: Integration of autonomous control, predictive maintenance, and alternative fuels shaping next-gen tractors.

Advanced engine tractors primarily serve row-crop farming (46%), horticulture (21%), and livestock operations (18%). Recent innovations include electronically controlled common-rail systems and real-time emission monitoring. Regulatory pressure, fuel price volatility, and mechanization incentives are reshaping regional consumption, while hybrid and hydrogen-compatible engines are emerging as long-term growth pathways.

The Agricultural Tractors with Advanced Engine Technology Market holds strong strategic relevance as global agriculture transitions toward higher productivity, regulatory compliance, and sustainability. Advanced engine platforms integrate precision fuel injection, electronic control units, and exhaust after-treatment systems that collectively improve operational efficiency and environmental performance. For instance, AI-enabled engine management delivers 12% efficiency improvement compared to conventional mechanical fuel systems, enabling farmers to optimize output under variable field conditions.

From a regional perspective, Asia Pacific dominates in volume, driven by mechanization programs, while Europe leads in adoption with nearly 64% of enterprises deploying emission-compliant advanced engine tractors. These variations highlight differing policy priorities and technology maturity levels across regions. In the short term, by 2027, predictive engine diagnostics powered by machine learning are expected to reduce unplanned tractor downtime by 18%, directly impacting farm profitability.

Compliance and ESG considerations are increasingly shaping procurement strategies. Manufacturers and large farming enterprises are committing to 20% lifecycle emission reductions and 30% recyclable component usage by 2030. A micro-scenario illustrates this shift: in 2024, a German OEM achieved a 15% fuel-efficiency gain by deploying hybrid diesel-electric engines across its premium tractor line.

Looking forward, the Agricultural Tractors with Advanced Engine Technology Market is positioned as a pillar of agricultural resilience, regulatory alignment, and sustainable growth, supporting long-term food security and operational scalability.

The Agricultural Tractors with Advanced Engine Technology Market Dynamics reflect a transition toward smarter, cleaner, and more efficient farm machinery. Adoption is shaped by emission regulations, rising fuel costs, and the need for precision agriculture. Advanced engines enable real-time monitoring, adaptive power output, and reduced maintenance intervals. Integration with GPS-based farming systems and telematics platforms enhances asset utilization and field productivity. OEMs are aligning product portfolios with regional compliance frameworks, while farmers increasingly evaluate total cost of ownership rather than upfront equipment cost. These dynamics collectively accelerate demand for technologically advanced tractors across developed and emerging agricultural economies.

Sustainability mandates and efficiency targets are key drivers. Advanced engines reduce particulate emissions by up to 90% compared to legacy designs and improve fuel utilization by 10–18%, directly lowering operating costs. Governments across North America and Europe incentivize adoption through tax credits and modernization grants, accelerating fleet upgrades. Precision farming compatibility further boosts yields per hectare, encouraging large-scale farms to invest in advanced engine tractors as core productivity assets.

Advanced engine tractors carry 25–35% higher upfront costs than conventional models due to complex electronics and after-treatment systems. Small and marginal farmers often face financing constraints, limiting adoption despite long-term savings. Maintenance requires skilled technicians and diagnostic tools, increasing service dependency. In price-sensitive regions, refurbished or lower-spec models remain prevalent, slowing penetration of advanced engine technologies.

The integration of hybrid, biofuel, and hydrogen-ready engines presents significant opportunities. Pilot programs indicate biofuel-compatible engines can cut lifecycle emissions by up to 40%, while hybrid systems deliver 15% power efficiency gains. Emerging markets are investing in localized fuel ecosystems, creating new demand for adaptable engine platforms and retrofitting solutions.

Divergent emission standards across regions complicate product standardization. OEMs must customize engines for multiple compliance regimes, increasing development cycles. Infrastructure gaps, such as limited access to ultra-low sulfur fuel or diagnostic service networks, constrain performance optimization in rural areas. These challenges increase operational risk for both manufacturers and end-users.

Electrification-Ready Powertrains: Over 38% of new tractor platforms launched in 2024 feature hybrid-ready architectures, enabling future electrification while delivering 12–16% fuel savings today. OEMs are standardizing modular engine bays to reduce redesign time by 20%.

AI-Driven Engine Optimization: Smart engine control systems using real-time sensor data are improving load efficiency by 14% and cutting maintenance costs by 17%, with adoption exceeding 45% among large farms in North America.

Emission-Focused Retrofitting: Nearly 29% of existing tractor fleets in Europe are undergoing engine upgrades or retrofits to meet stricter emission rules, extending equipment life by 6–8 years while reducing nitrogen oxide output by 70%.

Connected Telematics Integration: Advanced engine tractors with cloud-based telematics now account for 52% of premium segment sales, enabling predictive maintenance that lowers breakdown frequency by 19% and improves seasonal uptime across high-intensity farming operations.

The Agricultural Tractors with Advanced Engine Technology Market is segmented based on type, application, and end-user, reflecting differences in power requirements, operational intensity, and technology adoption across farming systems. By type, segmentation is largely influenced by horsepower class and engine architecture, as advanced combustion, hybridization, and electronic control systems are adopted unevenly across tractor categories. Application-based segmentation highlights how advanced engine tractors are deployed across row crop farming, horticulture, livestock operations, and specialty agriculture, each requiring different torque profiles, duty cycles, and emission performance. End-user segmentation further distinguishes demand patterns between large commercial farms, medium-scale agricultural enterprises, cooperatives, and government-supported farming initiatives. Across all segments, adoption is shaped by mechanization levels, regulatory compliance needs, fuel efficiency priorities, and the integration of precision agriculture technologies. This segmentation structure enables stakeholders to assess demand concentration, technology readiness, and upgrade cycles across distinct market clusters without relying on uniform adoption assumptions.

The market by type is primarily segmented into mid-horsepower tractors (40–100 HP), high-horsepower tractors (above 100 HP), compact tractors (below 40 HP), and specialty tractors equipped with advanced engine technologies. Mid-horsepower tractors lead the segment, accounting for approximately 46% of total adoption, as they balance fuel efficiency, versatility, and compatibility with advanced engine control units and emission after-treatment systems. These tractors are widely used across mixed farming operations and benefit from optimized combustion systems that reduce fuel consumption by up to 15% per operating hour. High-horsepower tractors represent the fastest-growing type, driven by large-scale mechanized farming and autonomous-ready platforms. This segment is expanding at an estimated 6.8% CAGR, supported by rising demand for AI-managed engines, higher torque efficiency, and reduced downtime in intensive farming operations. Compact tractors contribute steadily to the market, particularly in horticulture and smallholder farming, while specialty tractors serve niche applications such as vineyards and orchards. Collectively, compact and specialty tractors account for a combined 28% share, emphasizing targeted but consistent demand.

By application, the Agricultural Tractors with Advanced Engine Technology Market is segmented into row crop farming, horticulture and specialty crops, livestock and dairy farming, and contract farming services. Row crop farming dominates the application landscape with nearly 52% adoption, as large-scale cultivation requires high fuel efficiency, consistent power delivery, and compliance with emission norms during prolonged operating cycles. Advanced engine tractors in this application reduce fuel wastage by up to 14% per hectare and support precision seeding and harvesting systems. Contract farming services are the fastest-growing application, supported by shared equipment models and mechanization outsourcing. This segment is growing at an estimated 7.1% CAGR, driven by increasing reliance on high-performance tractors capable of operating across diverse farm types. Horticulture and specialty crops account for around 21% of adoption, benefiting from compact advanced engines that offer lower noise and emission levels. Livestock and dairy farming applications collectively contribute 19%, focusing on maneuverability and low-speed torque efficiency. In 2024, over 41% of large farming enterprises globally reported deploying advanced engine tractors for multi-crop operations, while 36% of mechanized farms integrated engine telematics for fuel monitoring and predictive maintenance.

End-user segmentation includes large commercial farms, medium-scale farms, agricultural cooperatives, and government or institutional farming bodies. Large commercial farms lead the market with approximately 48% adoption, supported by higher capital availability, focus on operational efficiency, and early adoption of advanced engine and telematics technologies. These users prioritize tractors with electronically managed engines that deliver consistent performance and reduced maintenance intervals. Agricultural cooperatives represent the fastest-growing end-user group, expanding at an estimated 6.9% CAGR, driven by pooled investment models and shared access to advanced machinery. Medium-scale farms account for a combined 32% share, gradually upgrading fleets to comply with emission standards and reduce fuel costs. Government and institutional users contribute the remaining 20%, particularly through subsidized mechanization and rural development programs. In 2024, over 39% of organized farming cooperatives adopted advanced engine tractors to support shared mechanization models, while 44% of large farms implemented engine diagnostics systems to optimize seasonal operations.

North America accounted for the largest market share at 38.6% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.9% between 2025 and 2032.

Region-wise performance in the Agricultural Tractors with Advanced Engine Technology Market reflects differences in mechanization intensity, regulatory maturity, and capital investment. North America leads due to high penetration of emission-compliant tractors, with over 72% of new tractor registrations incorporating advanced engine control and after-treatment systems. Europe follows with 31.4% share, driven by sustainability mandates and rapid replacement of legacy diesel engines. Asia-Pacific, holding 23.8% share in 2024, shows accelerating demand supported by rising tractor density, which increased from 18 units per 1,000 hectares in 2015 to 29 units in 2024. South America and the Middle East & Africa together account for 6.2%, reflecting gradual mechanization, expanding commercial farming, and government-backed modernization programs. Across regions, fuel efficiency gains of 10–18%, emission reductions exceeding 70%, and growing adoption of engine telematics are key measurable differentiators shaping regional demand patterns.

North America represents approximately 38.6% of the global market share, supported by high replacement rates of older tractor fleets and widespread adoption of advanced engines in mid- and high-horsepower segments. Row crop farming, dairy, and large commercial agriculture drive demand, accounting for nearly 64% of regional tractor utilization. Regulatory frameworks emphasizing low-emission equipment have resulted in over 80% of newly sold tractors meeting advanced emission and fuel-efficiency standards. Digital transformation is evident, with 47% of tractors equipped with engine telematics and predictive diagnostics. A leading regional OEM has expanded smart-engine production lines, enabling real-time fuel optimization and reducing maintenance downtime by 15%. Consumer behavior shows preference for premium, technology-rich equipment, with large farms prioritizing total lifecycle efficiency over upfront cost.

Europe holds close to 31.4% of the global market share, with Germany, France, and the UK collectively contributing over 58% of regional demand. Sustainability-focused regulations and carbon-reduction targets have accelerated adoption of advanced engine tractors, particularly in the 50–120 HP range, which accounts for 44% of deployments. Emerging technologies such as hybrid drivetrains and electronically managed exhaust systems are increasingly common, with 39% of new tractors integrating such features. A prominent regional manufacturer has introduced hydrogen-ready engines for pilot deployment across commercial farms. Consumer behavior in the region reflects regulatory-driven purchasing decisions, with buyers favoring compliant, low-emission tractors to meet environmental and reporting requirements.

Asia-Pacific ranks third by current share but first by growth momentum, accounting for 23.8% of global adoption. China, India, and Japan together represent over 70% of regional tractor demand. Tractor density and manufacturing capacity have expanded rapidly, with regional production exceeding 1.2 million units annually. Local innovation hubs focus on compact and mid-horsepower advanced engines tailored for small and medium farms. A major regional player has scaled production of electronically controlled diesel engines, improving fuel efficiency by 13%. Consumer behavior varies widely, with smallholders prioritizing affordability, while contract farming enterprises increasingly adopt advanced engine models for multi-crop operations.

South America accounts for approximately 4.1% of global market share, led by Brazil and Argentina, which together contribute over 65% of regional demand. Large-scale soybean, corn, and sugarcane farming drive the need for high-torque, fuel-efficient tractors. Infrastructure upgrades and trade-friendly policies have supported mechanization, resulting in 27% growth in advanced-engine tractor imports over the past four years. A regional manufacturer has localized production of emission-compliant engines to reduce operating costs for commercial farms. Consumer behavior reflects demand linked closely to export-oriented agriculture and productivity gains.

The Middle East & Africa region represents about 2.1% of the global market, with demand concentrated in South Africa, UAE, and parts of North Africa. Agricultural diversification programs and food security initiatives are driving gradual adoption, particularly in irrigation-intensive farming. Technological modernization focuses on rugged, fuel-efficient engines capable of operating in extreme climates. A local distributor has partnered with global OEMs to introduce advanced engine tractors suited for arid conditions. Consumer behavior emphasizes durability and low maintenance, with government-supported projects accounting for nearly 40% of regional purchases.

United States – 26.8% Market Share: High production capacity, strong adoption of precision agriculture, and rapid replacement of legacy tractor fleets.

Germany – 14.6% Market Share: Advanced manufacturing ecosystem, strict emission compliance requirements, and high penetration of technology-driven farming systems.

The Agricultural Tractors with Advanced Engine Technology Market is moderately consolidated with roughly 50+ active global competitors, including tractors and powertrain specialists. The top five companies—John Deere, AGCO Corporation, CNH Industrial, Kubota Corporation, and Mahindra & Mahindra—collectively command approximately 60–65% of the active advanced engine technology deployments worldwide. Competitive strategies focus on innovation in digital integration, autonomous functionalities, sustainable engine platforms, and expanded service ecosystems. Over the past two years, major participants launched enhanced connectivity features, telematics platforms, and precision farming solutions tailored to advanced engine tractors. Strategic initiatives include partnerships between tractor OEMs and tech firms to co-develop AI-driven guidance and predictive maintenance tools, along with product launches that emphasize low-emission engines and hybrid drive systems. Companies are increasingly investing in R&D hubs and expanding regional production footprints to meet diverse regulatory and environmental standards. Market fragmenters include smaller regional manufacturers targeting niche segments with specialized engine tuning and cost-effective advanced solutions. This competitive environment is shaped by the need to balance durability, digital capabilities, and regulatory compliance, making advanced engine tractor innovation a key competitive differentiator.

Kubota Corporation

Mahindra & Mahindra

Massey Ferguson

Fendt

CLAAS

Deutz-Fahr

Same DeutzFahr Group

Advanced technologies are substantially reshaping the Agricultural Tractors with Advanced Engine Technology Market. Modern tractors increasingly integrate precision guidance systems, which enhance field accuracy and operational efficiency by reducing overlaps and input waste. Advanced engine controls with electronic fuel injection, turbocharging, and adaptive emission systems are elevating engine responsiveness and fuel efficiency across varying loads. Telematics and IoT integrations enable remote diagnostics, predictive maintenance, and performance optimization, with many fleets reporting up to 20–25% reduction in unscheduled downtime through real-time sensor feedback. Autonomous navigation and AI-enabled guidance systems are being deployed, particularly in high-value cropping regions, enabling tractors to operate with minimal human input and higher consistency in repetitive tasks. Hybrid and electric drivetrains are emerging, especially in compact and orchard applications, offering quieter operation and lower lifecycle energy costs. Digital cockpit systems with touch interfaces provide operators with actionable data on engine health, soil conditions, and implement integration. Engine manufacturers are also developing biofuel-compatible platforms and alternative fuel engine variants to align with sustainability agendas and regulatory demands for lower emissions. Across the market, advanced engine management systems and connected ecosystems are pivotal in driving performance, reliability, and user experience in next-generation agricultural tractors.

In 2024, John Deere introduced its largest 9RX series tractor at the Commodity Classic in Houston, designed for improved field efficiency by enabling farmers to eliminate passes and reduce soil compaction, increasing productivity by up to 100 acres per day with its advanced engine and track technology. Source: www.agriculture.com

In 2023 and continuing into 2024, New Holland refreshed its T9 SmartTrax tractors, adding SmartTrax systems with boosted horsepower, upgraded cabs, and improved efficiency — offering operators flexibility between wheel and track units tailored for advanced engine performance. Source: www.agriculture.com

In 2025, AGCO spotlighted AI, autonomy, and mixed-fleet solutions at AGCO Tech Day, showcasing retrofit autonomous systems (e.g., PTx Trimble Outrun) on Fendt 900 Vario tractors and AI-based weed and fertilizer applications that reduce chemical use by up to 70%, reflecting advanced technology integration. Source: www.apache.org

In 2024, CNH Industrial progressed autonomous and intelligent farming tech through acquisitions and partnerships, including integrating machine vision automation capabilities from Augmenta to enhance real-time agronomic insights on New Holland tractors and other brands, strengthening precision operation capabilities.

The Agricultural Tractors with Advanced Engine Technology Market Report offers a comprehensive assessment of segment performance, covering product types, application use cases, engine platforms, power ranges, and end-user segments across global regions. The scope includes detailed analysis of internal combustion, hybrid, and electric engine technologies, along with digital feature integrations such as GPS guidance, telematics, and autonomous navigation systems. Geographic coverage extends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with in-depth regional consumption and adoption patterns, as well as infrastructure and regulatory landscape insights. The report also examines production capacities, manufacturing trends, and supply chain dynamics, exploring how localized facilities and investment flows affect global availability and technological rollout. End-user segments, including commercial farms, specialty crop growers, and large agri-business operators, are profiled with usage patterns, machinery preferences, and operational requirements. Emerging niche segments like precision autonomous tractors, orchard-specific vehicles, and biofuel compatible engine variants are evaluated for future relevance. Critical technology aspects such as integrated sensor arrays, IoT telematics, predictive maintenance systems, and hybrid powertrain developments are detailed to inform strategic decision-making. The report’s analytical framework supports executives, investors, and planners in understanding competitive positioning, innovation trends, and growth enablers shaping the advanced engine tractor landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 7,816.0 Million |

| Market Revenue (2032) | USD 12,086.4 Million |

| CAGR (2025–2032) | 5.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | John Deere, AGCO Corporation, CNH Industrial, Kubota Corporation, Mahindra & Mahindra, Massey Ferguson, Fendt,CLAAS, Deutz-Fahr, Same DeutzFahr Group |

| Customization & Pricing | Available on Request (10% Customization Free) |