Reports

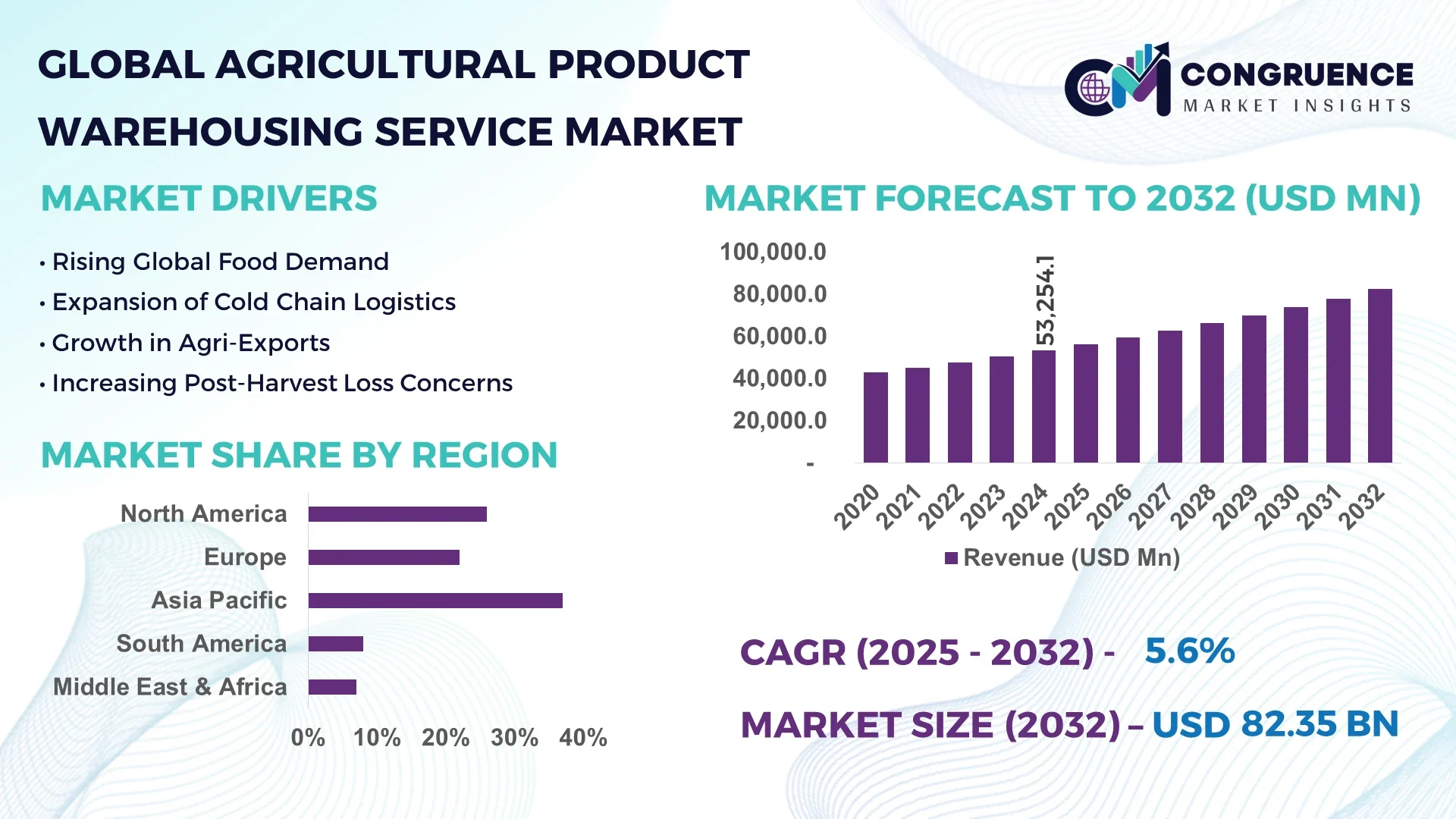

The Global Agricultural Product Warehousing Service Market was valued at USD 53254.08 Million in 2024 and is anticipated to reach a value of USD 82350.11 Million by 2032 expanding at a CAGR of 5.6% between 2025 and 2032.

China has developed an expansive agricultural warehousing infrastructure featuring advanced temperature-controlled storage, automated grain handling lines, and IoT-enabled monitoring systems for real-time condition tracking. Major investments in smart logistics hubs and energy-efficient cold-chain facilities support critical operations in grain preservation, perishable goods storage, and agricultural exports, with technological upgrades enhancing operational precision and throughput efficiency.

The Agricultural Product Warehousing Service Market is driven by strong demand from sectors including fresh produce, dairy, grains, and seafood, supported by large-scale temperature-controlled distribution networks and modern logistics frameworks. Technological advancements such as AI-powered inventory optimization, renewable energy-powered refrigeration, and automated pallet handling are transforming operational performance. Regulatory initiatives targeting food safety compliance, environmental sustainability, and reduction of post-harvest losses are accelerating the adoption of eco-efficient warehousing models. Growth in Asia-Pacific is propelled by expanding organized retail, rising urban consumption, and modernization of agricultural supply chains. Emerging trends include modular cold-storage units, blockchain-based traceability, and scalable on-farm warehousing solutions, ensuring resilience and adaptability across dynamic agricultural trade environments.

AI is revolutionizing the Agricultural Product Warehousing Service Market by delivering intelligent automation, predictive analytics, and optimized resource allocation. Machine learning algorithms are enabling dynamic storage slotting based on real-time demand forecasts, reducing spoilage risks and maximizing available capacity. AI-powered vision systems enhance accuracy in sorting, grading, and packaging, improving product quality consistency while minimizing human error. Predictive maintenance models monitor refrigeration systems and handling equipment, reducing downtime and safeguarding sensitive commodities.

In modern warehousing facilities, AI-integrated autonomous guided vehicles (AGVs) and robotic pickers streamline material handling, improving throughput and reducing operational bottlenecks. Intelligent routing algorithms coordinate warehouse-to-transport scheduling, aligning inventory readiness with shipment dispatch to enhance supply chain synchronization. AI also strengthens regulatory compliance by automating environmental monitoring, generating instant audit reports, and ensuring adherence to temperature and hygiene standards.

The result is a leaner, faster, and more resilient warehousing ecosystem capable of meeting fluctuating market demands while optimizing costs. By leveraging AI, the Agricultural Product Warehousing Service Market is achieving higher productivity, improved inventory visibility, and enhanced adaptability to seasonal and market-driven changes.

“In 2025, a leading global cold-chain operator deployed AI-driven pallet allocation and predictive truck scheduling systems in its agricultural warehouses, reducing retrieval times by 27% and improving overall cold-storage efficiency for perishable goods.”

The Agricultural Product Warehousing Service Market operates within a complex ecosystem shaped by global trade flows, supply chain modernization, and advancements in cold-chain logistics. Increasing consumer demand for fresh, high-quality produce has driven investment in temperature-controlled facilities, automated handling systems, and digital monitoring platforms. Seasonal production variability and the need for long-term storage stability have accelerated the integration of smart warehousing solutions capable of adjusting environmental conditions in real time. Government initiatives promoting food safety compliance and reductions in post-harvest losses continue to influence infrastructure development, while the growth of e-commerce in food retail channels has added pressure for faster and more flexible storage capabilities. Emerging trends include warehouse energy optimization through renewable sources, AI-driven inventory allocation, and blockchain-enabled traceability for enhanced transparency across supply chains.

The rapid expansion of cold-chain infrastructure is a key driver propelling growth in the Agricultural Product Warehousing Service Market. Rising consumption of fresh produce, dairy products, seafood, and processed frozen foods is increasing demand for specialized storage environments with precise temperature and humidity controls. Technological advancements, such as automated refrigeration systems and IoT-based monitoring devices, ensure the quality and shelf life of sensitive commodities, reducing spoilage rates. In developing economies, public-private investments are enhancing rural and peri-urban storage capacity, allowing producers to access broader markets. This expansion supports global agricultural trade by enabling long-distance transportation without compromising product integrity, thereby reinforcing market competitiveness and supply chain resilience.

One of the significant restraints in the Agricultural Product Warehousing Service Market is the substantial capital investment required to establish and maintain modern storage facilities. Building temperature-controlled warehouses equipped with automated handling systems, energy-efficient cooling units, and real-time monitoring technology demands considerable upfront expenditure. In addition to high installation costs, operational expenses such as energy consumption, skilled labor, and maintenance can be prohibitive, especially for small and mid-sized enterprises. Fluctuating energy prices and increasing regulatory compliance requirements further raise operating costs. These financial barriers can slow infrastructure upgrades in certain regions, limiting access to modern storage solutions and impacting the overall efficiency of agricultural supply chains.

The integration of renewable energy into warehousing operations presents a substantial growth opportunity for the Agricultural Product Warehousing Service Market. Solar-powered refrigeration systems, wind-assisted energy generation, and biomass-based heating are increasingly being adopted to reduce dependency on conventional power sources. These technologies lower long-term operational expenses while aligning with global sustainability objectives and environmental regulations. In regions with abundant sunlight, photovoltaic systems can power climate-controlled storage, significantly cutting energy costs and enhancing carbon footprint reduction. This transition also opens avenues for government incentives and green financing, encouraging warehouse operators to invest in sustainable infrastructure. As consumer demand for eco-friendly supply chains rises, renewable-powered facilities will gain a competitive advantage in attracting contracts from environmentally conscious retailers and exporters.

A major challenge facing the Agricultural Product Warehousing Service Market is the ability to maintain consistent product quality during supply chain disruptions. Factors such as extreme weather events, transportation delays, geopolitical tensions, and pandemics can hinder the timely movement of goods, increasing the burden on storage facilities. Extended storage periods require precise environmental control, particularly for perishable products, to prevent spoilage and meet stringent quality standards. Interruptions in power supply or equipment malfunctions during such disruptions can lead to significant product losses. Additionally, fluctuating import-export regulations and inspection delays can further complicate inventory turnover, forcing warehouse operators to invest in backup systems, redundant capacity, and advanced monitoring tools to safeguard stored commodities.

Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction is rapidly changing the infrastructure landscape of the Agricultural Product Warehousing Service Market. Precision-engineered elements are manufactured off-site using automated machinery, reducing reliance on skilled on-site labor and significantly shortening project timelines. In Europe and North America, where space utilization and speed-to-market are priorities, modular warehousing enables rapid deployment in both urban and rural areas. These solutions also allow for scalable expansion, enabling operators to adjust capacity in response to seasonal fluctuations and regional demand surges.

Integration of IoT-Enabled Monitoring Systems: IoT-based monitoring technologies are becoming a core feature of modern agricultural warehouses, delivering real-time tracking of temperature, humidity, and product condition. Advanced sensor arrays integrated into storage facilities enable immediate alerts for deviations, preventing spoilage of perishable commodities such as fruits, vegetables, and dairy products. In Asia-Pacific, adoption rates have accelerated as operators seek compliance with stringent food safety standards while improving traceability across global supply chains. These systems also generate valuable performance analytics to optimize energy use and inventory turnover.

Shift Toward Renewable Energy-Powered Warehousing: Sustainability goals and rising energy costs are driving investment in renewable-powered agricultural warehousing solutions. Solar-powered refrigeration units, wind-assisted energy systems, and hybrid storage facilities are being implemented to reduce operational expenses while meeting environmental regulations. In regions with high solar exposure, photovoltaic systems are powering entire cold-chain facilities, enabling operators to cut energy costs by double-digit percentages. This shift is also attracting partnerships with environmentally conscious retailers and export companies.

Automation and Robotics in Material Handling: Automation is transforming warehouse operations through the adoption of robotic pickers, automated guided vehicles (AGVs), and conveyor systems tailored for agricultural goods. These systems enhance throughput, reduce human error, and improve handling of fragile or perishable products. Large-scale facilities in North America and East Asia are integrating robotics with AI-based warehouse management platforms, enabling predictive inventory allocation and optimized product flow. Automation is also reducing operational strain during labor shortages, ensuring continuity in high-demand seasons.

The Agricultural Product Warehousing Service Market is segmented based on type, application, and end-user, each influencing operational priorities and investment trends. Types vary from traditional ambient storage to advanced climate-controlled and cold-chain facilities, each serving distinct commodity needs. Applications range from bulk grain preservation to perishable goods management, with specialized infrastructure supporting each category. End-users span from large-scale exporters and agro-processing industries to retail distribution hubs and farmer cooperatives, with differing requirements in terms of scale, storage duration, and compliance. Understanding these segments helps stakeholders align facility design, technological integration, and service offerings with evolving market demands and regional supply chain strategies.

The market includes ambient storage facilities, cold-chain warehouses, climate-controlled storage, and specialized modular units. Cold-chain warehouses lead the market due to their critical role in preserving perishable goods like fruits, vegetables, dairy, and meat products under optimal temperature and humidity conditions. Their dominance is reinforced by technological advances in refrigeration and energy efficiency. The fastest-growing type is modular storage units, driven by the need for flexible, rapidly deployable facilities in both rural and urban settings. These units can be scaled up or down to meet seasonal demand and are increasingly favored in emerging economies where infrastructure needs to adapt quickly to production cycles. Climate-controlled warehouses serve niche markets such as seed preservation and specialty crop storage, offering extended shelf life and quality retention. Ambient storage facilities remain essential for grains, pulses, and other commodities that do not require refrigeration but benefit from moisture and pest control systems.

Applications span grain storage, perishable goods preservation, seed storage, and processed agricultural product warehousing. Perishable goods preservation is the leading application, supported by the expansion of global cold-chain networks and growing demand for fresh produce in both domestic and export markets. This segment benefits from innovations such as automated climate regulation and real-time quality monitoring. The fastest-growing application is processed agricultural product storage, fueled by the rising demand for ready-to-cook and packaged food items, which require stable temperature and contamination-free environments. Grain storage remains a substantial segment, particularly in regions with high production volumes and government-supported food security reserves. Seed storage, although smaller in scale, is gaining relevance in precision agriculture, where maintaining genetic integrity and germination potential is critical. Each application segment requires tailored storage conditions and technological support to optimize quality and minimize losses.

End-users in the Agricultural Product Warehousing Service Market include exporters, agro-processing companies, retail distribution centers, farmer cooperatives, and government food security agencies. Exporters lead the segment due to the necessity for high-quality, compliant storage before international shipment, ensuring product freshness and adherence to import standards. Agro-processing companies are the fastest-growing end-user group, driven by their expanding role in value-added food production and the need for integrated storage solutions close to processing facilities. Retail distribution centers play a vital role in linking warehouses to consumer markets, especially in urban areas with high turnover rates. Farmer cooperatives increasingly utilize shared storage to consolidate supply and improve bargaining power in the market. Government agencies maintain significant warehousing capacity to support food security programs, particularly in regions prone to supply disruptions. Each end-user group influences storage design, capacity requirements, and the level of technological integration needed to meet their operational objectives.

Asia-Pacific accounted for the largest market share at 37% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

The Asia-Pacific region continues to benefit from large-scale agricultural production, advanced cold-chain infrastructure in key economies, and rapid integration of digital warehouse management solutions. Meanwhile, North America’s anticipated acceleration is supported by automation adoption, strong consumer demand for fresh produce, and expansion of sustainable warehousing practices. Regional dynamics are also shaped by regulatory frameworks, climate considerations, and the pace of investment in renewable-powered storage solutions. Emerging economies in South America, the Middle East, and Africa are investing in modern facilities to meet domestic consumption needs and expand export capacity, indicating a gradual shift in global warehousing capabilities toward energy-efficient and technologically integrated operations.

Innovative Storage Solutions Driving Agri-Warehousing Evolution

North America holds approximately 26% of the Agricultural Product Warehousing Service Market, driven by robust demand from industries such as fresh produce, dairy, meat processing, and packaged food manufacturing. Federal and state-level support for modernizing cold-chain logistics is fostering adoption of advanced warehouse automation and AI-driven inventory systems. Regulatory compliance with food safety standards like the FSMA has prompted significant investment in temperature-controlled storage and digital traceability solutions. Digital transformation is accelerating through IoT-enabled monitoring and predictive analytics for maintenance scheduling. The region’s warehousing operators are increasingly focusing on sustainability, with renewable-powered facilities and energy-efficient refrigeration systems gaining prominence.

Green Technology Integration Reshaping Agricultural Warehousing

Europe accounts for around 22% of the Agricultural Product Warehousing Service Market, with Germany, France, and the UK being key hubs for advanced storage infrastructure. The region benefits from strong regulatory oversight on food safety and environmental sustainability, guided by organizations such as the European Food Safety Authority. Investments in eco-friendly refrigeration technologies and solar-powered facilities are aligning warehousing operations with EU climate goals. Adoption of blockchain for supply chain transparency and AI-based stock rotation optimization is expanding. Cross-border trade within the EU continues to stimulate demand for standardized, compliant warehousing that ensures consistent product quality across member states.

Advanced Cold-Chain Networks Boosting Regional Storage Efficiency

Asia-Pacific dominates with a 37% market share, supported by high agricultural output from China, India, and Japan, and growing demand for fresh and processed food exports. The region’s infrastructure development includes mega cold-storage hubs, port-centric warehouses, and digitally integrated supply chains. Investment in smart warehousing platforms and automated material handling systems is increasing, particularly in China’s logistics clusters and India’s agri-export corridors. Japan’s focus on high-value produce and precision-controlled environments has driven innovation in compact cold-storage facilities. The region’s competitive advantage is reinforced by strong government initiatives to reduce post-harvest losses and boost export readiness.

Infrastructure Modernization Enhancing Storage Capacity

South America holds approximately 8% of the Agricultural Product Warehousing Service Market, with Brazil and Argentina leading in production and storage capacity. Government-backed infrastructure programs are expanding cold-chain coverage into rural production zones, enabling more efficient market access for perishable goods. Trade agreements with North America, Europe, and Asia are creating new demand for export-compliant storage solutions. Renewable energy integration in warehouse operations, particularly solar-powered refrigeration in agricultural belts, is gaining traction. Modernization efforts also include upgrading port-side warehousing to meet international quality standards for agricultural exports.

Technological Upgrades Supporting Agri-Storage Expansion

The Middle East & Africa account for nearly 7% of the Agricultural Product Warehousing Service Market, with demand driven by food security initiatives and the growing import of agricultural commodities. The UAE and South Africa are leading in warehouse modernization, implementing AI-based temperature monitoring and energy-efficient cold-chain systems. Regional governments are prioritizing investments in logistics infrastructure to support both domestic supply chains and re-export hubs. Partnerships with global logistics providers are accelerating the adoption of international best practices in storage, handling, and traceability, ensuring the region’s facilities meet global compliance standards.

China – 24% market share – Leadership is supported by extensive agricultural output, advanced cold-chain logistics, and rapid deployment of smart warehousing technology.

United States – 18% market share – Dominance is driven by large-scale retail distribution networks, strong technological integration, and strict regulatory compliance in food storage.

The Agricultural Product Warehousing Service market features a moderately consolidated competitive landscape, with over 120 active service providers operating globally. A few large-scale players dominate regional markets through extensive storage networks, automated facilities, and integrated cold chain solutions, while mid-sized firms compete by offering specialized services tailored to local agricultural products. Strategic collaborations between warehousing operators and agri-tech firms are on the rise, enabling the deployment of AI-driven inventory management systems and IoT-based monitoring for real-time quality control. In recent years, mergers and acquisitions have intensified, particularly in Asia-Pacific and North America, as companies seek to expand geographic coverage and enhance operational capacity. Sustainability initiatives, such as energy-efficient cooling systems and renewable-powered storage facilities, are also influencing market positioning. Competitive differentiation increasingly depends on technology adoption, infrastructure scalability, and the ability to handle diverse agricultural commodities under strict regulatory compliance.

Lineage Logistics Holdings, LLC

Americold Logistics, LLC

Agro Merchants Group, LLC

United States Cold Storage, Inc.

NewCold Advanced Cold Logistics

Nichirei Logistics Group Inc.

Kloosterboer Group B.V.

Congebec Inc.

VX Cold Chain Logistics Pvt. Ltd.

Frialsa Frigorificos S.A. de C.V.

The Agricultural Product Warehousing Service market is increasingly anchored in a wave of sophisticated technologies that enhance storage efficiency, traceability, and asset utilization. Advanced automation platforms are enabling real-time temperature and humidity control, ensuring perishable inventory remains within stringent preservation thresholds. Autonomous guided vehicles (AGVs) and robotic sorting systems are being deployed for flexible, high-precision pallet movement, significantly reducing manual handling errors and downtime. Digital twin technologies are emerging as critical tools, offering virtual replicas of warehousing environments that allow simulation of workflows and system optimization before physical implementation. Blockchain-enabled traceability systems are gaining traction, especially in markets where provenance and auditability of agricultural goods are high priorities; this ensures immutable tracking of each batch from production to dispatch.

Unmanned aerial vehicles (UAVs), paired with RFID scanning, are being piloted for rapid inventory audits—drastically cutting the time to reconcile large-scale stockpiles while improving accuracy in volume calculation. These systems also enhance security by identifying anomalies or unauthorized access in high-volume facilities. Predictive maintenance technologies, supported by IoT and machine learning, continually assess refrigeration and conveyor equipment, flagging wear or performance degradation before breakdown occurs. Integrating solar and renewable energy-powered refrigeration units into warehousing infrastructure is also transforming operating models: warehouses in high-sunlight geographies are now maintaining cold-chain conditions with minimal dependence on grid electricity while improving sustainability credentials. Together, these technological trends deliver a tangible shift—accelerating warehousing performance, reducing waste, and enabling scalable, intelligent operations tailored to evolving demands in agricultural supply chains.

• In early 2024, a pioneering UAV and blockchain-based system was tested in an industrial warehouse, enabling automated inventory scanning, fast item localization via RFID signal strength, and secure distributed ledger traceability of storage data in real-world operations.

• Mid-2023 saw Indian infrastructure plans reveal a storage capacity gap exceeding 50%, prompting accelerated construction of modern silos and cold storage hubs to fulfill growing domestic demand for agricultural warehousing.

• By late 2024, an Indian agricultural warehousing company introduced geo-tagging and cadastral mapping tools across its network of over 1,300 warehouses to enhance farmland monitoring and improve crop intake accuracy.

• In Q2 2024, a regional government initiated a dedicated warehousing policy targeting logistical cluster development in delta districts, aimed at boosting cold storage integration and linking warehousing clusters to upcoming dry ports and logistics parks.

The scope of the Agricultural Product Warehousing Service Market Report encompasses a comprehensive review of service offerings, technological segments, regional geographies, application categories, and emerging industry focus areas. It covers a broad typology of storage solutions—from ambient and temperature-controlled to modular and renewable-energy-powered facilities—while examining end-user applications such as grain storage, perishable preservation, seed conservation, and processed product warehousing. Geographically, the report analyzes core regions including North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, highlighting infrastructure status, regional demand drivers, and strategic growth corridors.

Technological domains explored include automation systems, IoT-based climate monitoring, robotics and AGVs, blockchain traceability, UAV-assisted inventory management, digital twins, and energy-efficient refrigeration tied to solar or renewable energy sources. The report also examines stakeholder segments ranging from exporters, agro-processors, retailers, farmer cooperatives, to governmental agencies—detailing their distinct warehousing requirements, preferred service features, and investment prioritizations. Special focus areas include modular construction trends, cold-chain optimization, green infrastructure integration, and supply chain transparency, offering a nuanced map of both mainstream and niche market avenues essential for robust strategic planning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 53254.08 Million |

|

Market Revenue in 2032 |

USD 82350.11 Million |

|

CAGR (2025 - 2032) |

5.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Lineage Logistics Holdings, LLC, Americold Logistics, LLC, Agro Merchants Group, LLC, United States Cold Storage, Inc., NewCold Advanced Cold Logistics, Nichirei Logistics Group Inc., Kloosterboer Group B.V., Congebec Inc., VX Cold Chain Logistics Pvt. Ltd., Frialsa Frigorificos S.A. de C.V. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |