Reports

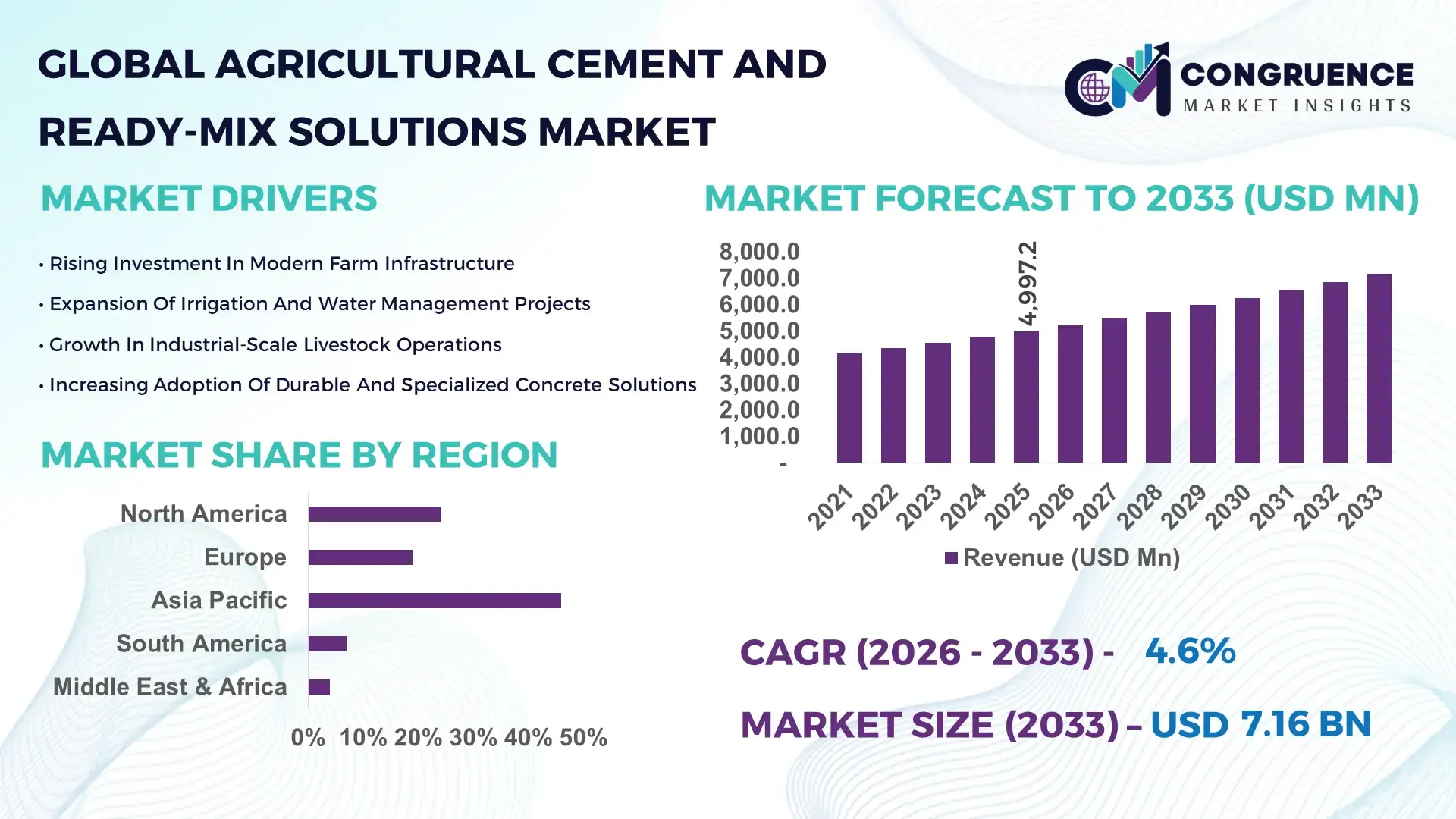

The Global Agricultural Cement and Ready-Mix Solutions Market was valued at USD 4,997.2 Million in 2025 and is anticipated to reach a value of USD 7,161.1 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by modernization of farm infrastructure, expansion of large-scale livestock operations, and rising investments in climate-resilient agricultural facilities.

China dominates the Agricultural Cement and Ready-Mix Solutions Market with annual cement production exceeding 2 billion metric tons, a significant portion allocated to rural infrastructure and agri-industrial projects. More than 35% of newly constructed livestock housing facilities in key agricultural provinces utilize specialized sulfate-resistant and moisture-controlled ready-mix formulations. Government-backed rural revitalization programs have directed over USD 100 billion toward irrigation channels, grain storage silos, and reinforced farm roads since 2020. Technological integration includes automated batching plants capable of producing 180 cubic meters per hour and the adoption of low-carbon clinker blends reducing CO₂ emissions by up to 15% per ton. Large-scale greenhouse clusters exceeding 20,000 hectares rely on high-durability concrete foundations to withstand humidity levels above 85%, reflecting advanced material engineering adoption across agricultural zones.

Market Size & Growth: USD 4,997.2 Million in 2025, projected to reach USD 7,161.1 Million by 2033 at 4.6% CAGR, driven by mechanized farming and livestock infrastructure upgrades.

Top Growth Drivers: 48% adoption in modern dairy farms; 35% efficiency gain from pre-engineered farm sheds; 22% reduction in maintenance costs using fiber-reinforced mixes.

Short-Term Forecast: By 2028, high-performance ready-mix solutions expected to reduce construction cycle time by 18% across large agricultural projects.

Emerging Technologies: Low-carbon cement blends, self-compacting concrete, IoT-enabled batching systems.

Regional Leaders: Asia-Pacific projected at USD 3,200 Million by 2033; North America at USD 1,950 Million; Europe at USD 1,420 Million, each reflecting rising precision agriculture investments.

Consumer/End-User Trends: Over 52% of commercial poultry farms prefer corrosion-resistant ready-mix for hygiene compliance.

Pilot Case: In 2024, a large dairy cooperative reduced structural maintenance costs by 20% using fiber-enhanced agricultural concrete.

Competitive Landscape: Top player holds ~16% share; leading competitors include multinational cement majors and regional ready-mix providers.

Regulatory & ESG Impact: 30% clinker substitution targets and water recycling mandates influencing production processes.

Investment Patterns: Over USD 2.5 billion invested globally in rural construction and automated batching plants in 2024–2025.

Innovation & Outlook: Integration of carbon-capture-ready kilns and modular precast farm structures shaping next-generation growth.

Livestock housing accounts for nearly 40% of Agricultural Cement and Ready-Mix Solutions demand, followed by irrigation infrastructure at 28% and grain storage facilities at 18%. Fiber-reinforced and sulfate-resistant formulations are gaining traction due to improved durability in high-moisture environments. Environmental compliance policies promoting low-carbon blends and regional consumption growth in Asia-Pacific and North America support steady infrastructure expansion across mechanized farming ecosystems.

The Agricultural Cement and Ready-Mix Solutions Market plays a critical strategic role in enabling resilient farm infrastructure, biosecure livestock housing, and climate-adaptive agricultural facilities. Precision-engineered concrete foundations reduce structural degradation by up to 25% compared to conventional site-mixed alternatives. Self-compacting concrete delivers 30% faster placement efficiency compared to traditional vibrated mixes, improving labor productivity and minimizing onsite errors.

Asia-Pacific dominates in volume due to expansive irrigation canal projects and rural modernization, while North America leads in adoption intensity with over 62% of commercial farms utilizing specialized ready-mix solutions for large barns and grain silos. By 2027, automated batching and AI-enabled mix optimization are expected to reduce material waste by 15% and improve compressive strength consistency by 12%.

Sustainability compliance is reshaping production pathways, with firms committing to 20% clinker reduction by 2030 through blended cement technologies and supplementary cementitious materials. In 2025, a major agribusiness developer in the United States achieved a 17% lifecycle emission reduction by integrating low-carbon ready-mix solutions in feed storage complexes.

Looking forward, the Agricultural Cement and Ready-Mix Solutions Market is positioned as a pillar of resilient agri-infrastructure, supporting food security, regulatory compliance, and sustainable rural development initiatives worldwide.

The Agricultural Cement and Ready-Mix Solutions Market is shaped by expanding mechanized agriculture, rising livestock density, and the need for durable farm infrastructure resistant to moisture, chemicals, and heavy machinery loads. Increasing demand for reinforced grain silos, manure management systems, and irrigation channels is influencing the adoption of specialized high-strength and sulfate-resistant concrete mixes.

Technological integration in batching plants, capable of producing more than 150 cubic meters per hour, enhances supply chain efficiency. Climate variability and frequent extreme weather events are accelerating investments in flood-resistant foundations and wind-resistant farm structures. Additionally, government rural infrastructure programs and food security initiatives are encouraging standardized construction materials to ensure long-term structural performance in agricultural environments.

Rising modernization of agricultural infrastructure significantly boosts demand for Agricultural Cement and Ready-Mix Solutions. Globally, over 45% of large-scale farms are upgrading storage facilities and livestock shelters to meet biosecurity and hygiene regulations. Reinforced concrete silos extend operational lifespan by 20–25 years compared to conventional steel alternatives in humid climates.

Mechanized harvesting equipment weighing above 15 tons requires heavy-duty concrete flooring with compressive strengths exceeding 40 MPa, encouraging adoption of high-performance ready-mix solutions. Additionally, government-backed irrigation projects covering more than 10 million hectares annually demand durable canal linings and water-retaining structures, further driving consistent material consumption across agricultural zones.

Volatility in limestone, clinker, and energy prices poses a significant restraint for the Agricultural Cement and Ready-Mix Solutions Market. Energy accounts for nearly 30% of cement production costs, and fuel price increases above 12% annually can compress manufacturer margins. Transportation expenses for ready-mix delivery within a 50–80 km radius also impact profitability, especially in rural regions with limited logistics infrastructure.

Environmental compliance costs linked to carbon emission regulations require kiln upgrades and emission control technologies, increasing capital expenditure by up to 10% for mid-sized producers. Such cost pressures can slow adoption among small-scale farmers with constrained investment budgets.

The transition toward climate-resilient agriculture presents strong opportunities for Agricultural Cement and Ready-Mix Solutions. Low-carbon blended cement formulations can reduce emissions by 15–25% while maintaining structural integrity above 35 MPa compressive strength. Rising investments in vertical farming and greenhouse complexes exceeding 25,000 square meters per unit demand high-durability flooring and foundation systems.

Precision batching technologies that improve mix accuracy by 10% reduce material waste and enhance sustainability performance. Furthermore, adoption of precast modular farm components is projected to grow steadily, enabling faster construction cycles and scalable deployment across expanding agri-industrial clusters.

Stringent carbon emission targets and environmental regulations challenge the Agricultural Cement and Ready-Mix Solutions Market by requiring significant technological adaptation. Cement manufacturing contributes approximately 7–8% of global CO₂ emissions, prompting regulatory mandates for emission reduction. Compliance often requires investment in alternative fuels and carbon capture systems, increasing operational complexity.

Additionally, water scarcity in agricultural regions limits onsite mixing operations, increasing reliance on centralized ready-mix plants. Balancing sustainability commitments with cost competitiveness remains a critical operational challenge for manufacturers serving rural and semi-urban agricultural markets.

• Expansion of Fiber-Reinforced Agricultural Concrete: Over 42% of newly constructed livestock facilities now integrate fiber-reinforced concrete, improving crack resistance by 30% and extending structural life beyond 25 years under high-moisture exposure. Adoption is particularly strong in dairy and poultry sectors where hygiene durability standards are rising.

• Growth in Low-Carbon Blended Cement Usage: Approximately 35% of agricultural ready-mix production now incorporates supplementary cementitious materials, reducing clinker content by up to 20%. This shift lowers embodied carbon while maintaining compressive strength levels above 40 MPa, aligning with sustainability-driven rural infrastructure projects.

• Automation in Rural Batching Plants: Automated batching systems with digital moisture sensors improve mix consistency by 12% and reduce material waste by 10%. More than 50% of new rural plants commissioned in 2025 include IoT-enabled quality monitoring tools for precision-controlled agricultural construction.

• Rise in Precast and Modular Farm Structures: Nearly 38% of large-scale farm construction projects utilize precast concrete components, shortening build time by 18% and reducing onsite labor requirements by 22%. This modular approach enhances scalability for expanding livestock and greenhouse operations globally.

The Agricultural Cement and Ready-Mix Solutions Market is segmented by type, application, and end-user to address diverse farm infrastructure requirements. By type, traditional Portland cement, blended cement, and specialized ready-mix formulations represent core product categories. By application, livestock housing, irrigation systems, grain storage facilities, and farm roads dominate material consumption.

End-user insights indicate large commercial farms and agribusiness developers account for the majority of structured concrete demand, while smallholder farms contribute through incremental rural infrastructure upgrades. Advanced material selection increasingly reflects climate resilience needs, heavy-load endurance, and sustainability compliance, supporting durable agricultural construction ecosystems.

Traditional Portland cement accounts for approximately 44% of Agricultural Cement and Ready-Mix Solutions demand due to its cost-effectiveness and compressive strength exceeding 35 MPa. Blended cement follows with nearly 32% share, offering improved sulfate resistance and 15% lower carbon intensity. However, specialized fiber-reinforced and self-compacting ready-mix solutions represent the fastest-growing type, expanding at 6.8% CAGR, driven by demand for enhanced durability and faster construction timelines.

These advanced mixes improve structural crack resistance by up to 30% and reduce placement time by 20% compared to conventional formulations. Remaining niche types, including rapid-setting and waterproof variants, collectively account for 24% of market consumption, serving irrigation canal linings and high-moisture livestock facilities.

Livestock housing leads with nearly 40% share of Agricultural Cement and Ready-Mix Solutions consumption, driven by large dairy complexes and poultry farms requiring corrosion-resistant flooring. Irrigation infrastructure accounts for 28%, while grain storage silos represent 18%. Modular greenhouse foundations and farm roads collectively contribute 14%.

The fastest-growing application is greenhouse and vertical farming structures, expanding at 7.1% CAGR due to rising investment in controlled-environment agriculture. In 2025, more than 41% of commercial greenhouse operators adopted reinforced ready-mix foundations to enhance humidity resilience. Additionally, 36% of agribusiness firms reported upgrading feed storage facilities with high-durability concrete flooring.

Large commercial agribusinesses account for approximately 52% of Agricultural Cement and Ready-Mix Solutions demand, reflecting structured investment capacity and regulatory compliance needs. Medium-sized farms represent 30%, while smallholder farms contribute 18% through incremental infrastructure development.

The fastest-growing end-user segment is industrial-scale livestock producers, expanding at 6.5% CAGR due to rising protein consumption and biosecure housing requirements. More than 48% of dairy cooperatives implemented reinforced concrete manure management systems in 2025 to comply with environmental standards. Additionally, 39% of integrated poultry farms reported transitioning to corrosion-resistant flooring solutions to reduce maintenance costs.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.4% between 2026 and 2033.

Asia-Pacific’s leadership is supported by more than 60% of global rural infrastructure expansion projects concentrated in China, India, and Southeast Asia. Over 18 million hectares of irrigated farmland across the region rely on reinforced canal linings and concrete-based water retention systems. China alone operates over 3,000 large-scale rural batching plants with average production capacities exceeding 150 cubic meters per hour, while India adds nearly 25,000 kilometers of rural roads annually, many utilizing ready-mix agricultural-grade concrete.

North America holds approximately 24% of global demand, driven by over 2 million commercial farms and high mechanization rates where equipment exceeding 20 tons requires heavy-duty flooring solutions. Europe accounts for nearly 19%, supported by modernization of more than 10,000 dairy farms annually. South America contributes around 7%, with Brazil representing over 55% of regional agricultural infrastructure spending. Meanwhile, Middle East & Africa, currently at 4%, is accelerating due to food security investments exceeding USD 15 billion in irrigation and greenhouse projects between 2024 and 2026, positioning it as the fastest-expanding regional cluster.

How Is Advanced Farm Modernization Transforming High-Performance Agricultural Construction Demand?

North America represents approximately 24% of the Agricultural Cement and Ready-Mix Solutions Market, supported by highly mechanized farming systems and more than 2 million operational farms. The United States and Canada collectively produce over 500 million tons of cement annually, with a significant share allocated to rural infrastructure and livestock housing upgrades. Dairy, poultry, and grain storage industries drive demand, particularly for fiber-reinforced and sulfate-resistant mixes designed to withstand ammonia exposure and freeze-thaw cycles exceeding 50 cycles per year.

Government programs supporting rural development and climate-resilient agriculture have directed billions toward irrigation rehabilitation and biosecure livestock facilities. Digital transformation trends include GPS-enabled batching trucks and moisture-sensor-controlled mixing systems improving quality consistency by 10–12%. A leading regional producer has introduced carbon-reduced agricultural concrete blends that lower embodied emissions by 18% per cubic meter. Consumer behavior reflects higher enterprise-level adoption, where over 65% of large agribusiness operators prioritize long-lifecycle infrastructure investments.

Why Are Sustainability Mandates Accelerating Durable Agricultural Infrastructure Adoption?

Europe accounts for nearly 19% of the Agricultural Cement and Ready-Mix Solutions Market, with Germany, France, and the UK leading infrastructure upgrades across more than 8 million agricultural holdings. Over 40% of new livestock housing projects incorporate low-carbon blended cement to meet regional sustainability frameworks. The European Green Deal and emissions trading mechanisms are encouraging clinker substitution rates above 25% in agricultural construction materials.

Adoption of self-compacting concrete has grown steadily, improving placement efficiency by 15% in confined barn environments. Digital monitoring of batching plants through automated control systems enhances material precision and reduces waste by nearly 8%. A major European cement producer has deployed carbon-capture-ready kilns capable of reducing CO₂ intensity per ton by 20%. Consumer behavior indicates regulatory-driven demand, with farm operators increasingly prioritizing compliant, traceable material sourcing aligned with environmental reporting standards.

What Drives High-Volume Agricultural Infrastructure Expansion Across Emerging Economies?

Asia-Pacific leads global volume consumption, accounting for 46% of Agricultural Cement and Ready-Mix Solutions demand. China, India, and Japan are the top consuming countries, collectively investing in more than 20 million hectares of irrigation modernization and greenhouse expansion. Over 3,000 automated batching facilities operate in rural China, while India adds approximately 12 million cubic meters of ready-mix annually for canal lining and grain storage projects.

Manufacturing trends emphasize large-scale clinker capacity and integrated logistics networks. Innovation hubs in Shanghai, Tokyo, and Bengaluru focus on high-durability and humidity-resistant formulations capable of maintaining structural integrity in environments exceeding 80% relative humidity. A leading regional supplier has launched precast modular farm components reducing construction time by 20%. Consumer behavior reflects rapid rural digitization, where mobile-based procurement platforms and e-commerce channels streamline ready-mix ordering for mid-sized farms.

How Are Agribusiness Expansion and Export Crops Supporting Infrastructure Growth?

South America represents approximately 7% of the Agricultural Cement and Ready-Mix Solutions Market, with Brazil and Argentina accounting for over 70% of regional consumption. Brazil alone cultivates more than 80 million hectares of farmland, necessitating durable farm roads and reinforced storage silos. Infrastructure trends show increasing deployment of corrosion-resistant concrete for soybean and corn export facilities.

Government incentives supporting irrigation efficiency and export competitiveness have accelerated rural infrastructure upgrades. Energy-intensive cement plants across the region produce over 60 million tons annually, supplying both agricultural and industrial projects. A major Brazilian producer has introduced high-strength agricultural-grade ready-mix formulations capable of achieving compressive strengths above 45 MPa. Regional consumer behavior indicates demand closely tied to agribusiness media campaigns and language-localized procurement systems, particularly in Brazil’s agritech clusters.

Why Is Food Security Investment Fueling Durable Agricultural Construction Across Arid Regions?

Middle East & Africa accounts for approximately 4% of global Agricultural Cement and Ready-Mix Solutions demand but is the fastest-growing regional segment. The UAE and Saudi Arabia are investing heavily in greenhouse complexes exceeding 5,000 hectares, requiring moisture-resistant and thermally stable concrete foundations. South Africa contributes significantly through irrigation canal rehabilitation covering over 300,000 hectares.

Technological modernization includes desalination-integrated agricultural projects utilizing reinforced concrete reservoirs. Trade partnerships across the Gulf Cooperation Council facilitate cement import-export flows exceeding 20 million tons annually. A regional producer has deployed solar-powered batching plants reducing operational energy consumption by 15%. Consumer behavior reflects food security priorities, where governments and private investors emphasize long-term durability and climate resilience in agricultural infrastructure development.

China – 34% share: Dominates the Agricultural Cement and Ready-Mix Solutions Market due to massive rural infrastructure programs and annual cement production exceeding 2 billion metric tons.

United States – 21% share: Leads through advanced mechanized farming, over 2 million farms, and strong investment in high-durability agricultural construction materials.

The Agricultural Cement and Ready-Mix Solutions Market is moderately consolidated, with the top five companies collectively accounting for approximately 48% of global market presence. Over 200 regional and local producers operate batching plants serving rural and semi-urban agricultural clusters. Multinational cement manufacturers maintain integrated supply chains with annual production capacities exceeding 100 million tons each, enabling cost efficiencies and broad distribution networks.

Strategic initiatives include mergers, sustainability-focused product launches, and digital batching innovations. More than 30% of leading players have introduced low-carbon agricultural concrete lines between 2024 and 2025. Partnerships with agribusiness developers and irrigation authorities are increasing, particularly in Asia-Pacific and North America. Investment in automated batching systems and precast agricultural components enhances differentiation. Competitive positioning increasingly depends on emission reduction capabilities, high-strength formulations above 40 MPa, and logistics reach within 100 km service radii. Regional players compete on pricing flexibility and localized supply, while global firms emphasize ESG compliance and technology-driven efficiency.

CRH plc

UltraTech Cement Ltd.

China National Building Material Company (CNBM)

Anhui Conch Cement Company

Buzzi Unicem

Votorantim Cimentos

Taiheiyo Cement Corporation

Dangote Cement

Siam Cement Group (SCG)

Vicat Group

Aditya Birla Group (Grasim Industries – Cement Division)

Technological advancements in the Agricultural Cement and Ready-Mix Solutions Market are centered on durability enhancement, emission reduction, and digital process optimization. Blended cement incorporating fly ash, slag, and calcined clay reduces clinker content by up to 25%, lowering carbon intensity while maintaining compressive strengths above 40 MPa. Fiber-reinforced concrete improves crack resistance by nearly 30%, extending livestock housing lifespan beyond 25 years.

Automation in batching plants equipped with IoT sensors ensures moisture accuracy within ±1%, enhancing mix consistency and reducing material waste by approximately 10%. Self-compacting concrete technology reduces placement time by 15–20%, especially in confined agricultural structures. Carbon-capture-ready kilns and alternative fuels such as biomass and refuse-derived fuels contribute to emission reduction targets of up to 20% per ton.

Precast modular components for farm sheds and silos shorten project timelines by 18% and improve structural standardization. AI-enabled quality monitoring platforms track temperature, curing cycles, and slump consistency in real time. Water recycling systems integrated into ready-mix plants reduce freshwater usage by 25%, addressing sustainability mandates. These innovations collectively support resilient, compliant, and cost-efficient agricultural infrastructure development.

• In March 2025, Holcim expanded its low-carbon ECOPlanet cement portfolio for infrastructure and agricultural applications, targeting a reduction of at least 30% CO₂ intensity compared to standard formulations. The expansion includes new production lines in Europe and North America. Source: www.holcim.com

• In September 2024, CEMEX announced investment in advanced admixture technologies to enhance durability and sulfate resistance in ready-mix solutions for agricultural and water infrastructure projects across Latin America. Source: www.cemex.com

• In February 2025, Heidelberg Materials inaugurated a carbon capture pilot facility designed to reduce up to 70% of process emissions at a European cement plant, supporting low-carbon construction materials for rural infrastructure. Source: www.heidelbergmaterials.com

• In July 2024, UltraTech Cement commissioned a new grinding unit in India adding 2.7 million tons annual capacity, supporting rural infrastructure and irrigation projects under national agricultural modernization initiatives. Source: www.ultratechcement.com

The Agricultural Cement and Ready-Mix Solutions Market Report provides a comprehensive evaluation of product types including traditional Portland cement, blended cement, fiber-reinforced mixes, and specialty agricultural formulations designed for high-moisture and chemical-resistant environments. The report covers applications such as livestock housing, irrigation canals, grain storage silos, greenhouse foundations, farm roads, and manure management systems.

Geographic analysis spans Asia-Pacific, North America, Europe, South America, and Middle East & Africa, highlighting infrastructure investments across more than 100 countries. The report evaluates technological advancements including automated batching systems, low-carbon clinker substitutes, carbon capture integration, and precast modular components.

Industry focus areas include large agribusiness developers, medium-scale commercial farms, and smallholder infrastructure projects. It also addresses regulatory frameworks promoting emission reduction, water recycling, and sustainable rural construction. Market dynamics, competitive positioning, innovation pipelines, and sustainability benchmarks are assessed to support strategic decision-making for manufacturers, infrastructure planners, and agricultural developers seeking durable and environmentally responsible construction solutions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 4,997.2 Million |

|

Market Revenue in 2033 |

USD 7,161.1 Million |

|

CAGR (2026 - 2033) |

4.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Holcim, CEMEX, Heidelberg Materials, CRH plc, UltraTech Cement Ltd., China National Building Material Company (CNBM), Anhui Conch Cement Company, Buzzi Unicem, Votorantim Cimentos, Taiheiyo Cement Corporation, Dangote Cement, Siam Cement Group (SCG), Vicat Group, Aditya Birla Group (Grasim Industries – Cement Division) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |