Reports

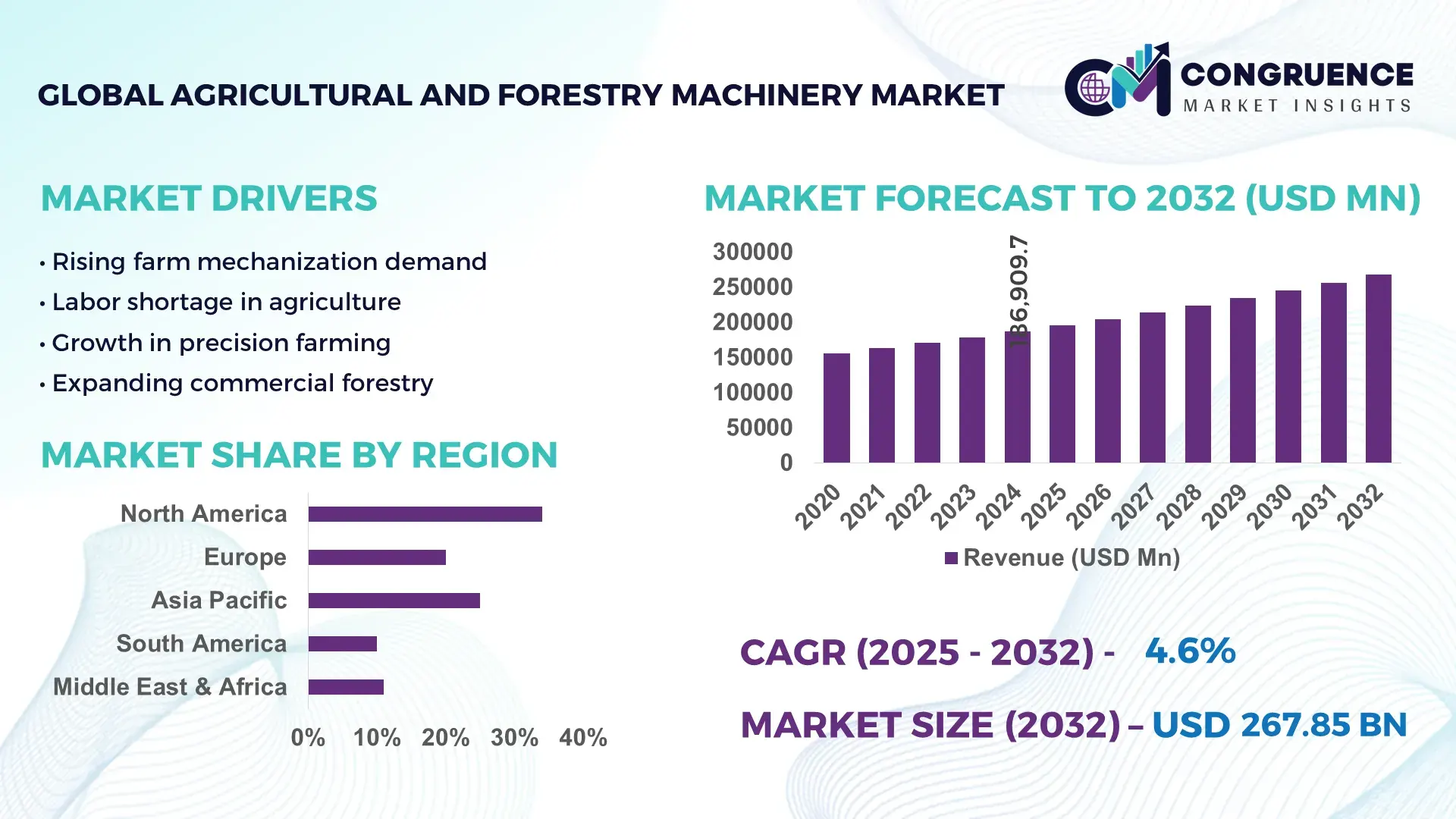

The Global Agricultural and Forestry Machinery Market was valued at USD 186,909.74 Million in 2024 and is anticipated to reach a value of USD 267,846.15 Million by 2032 expanding at a CAGR of 4.6% between 2025 and 2032. Growth is supported by rising farm mechanization, labor shortages, and increasing adoption of precision and automation-enabled equipment across large-scale agricultural operations.

The United States dominates the Agricultural and Forestry Machinery marketplace through large-scale production capacity, high capital investment, and advanced technology deployment. The country hosts over 1,200 agricultural equipment manufacturing facilities, producing more than 45% of North America’s total farm machinery output annually. Capital investment in agricultural machinery exceeded USD 38 billion in 2023, with strong deployment across row crop farming, forestry harvesting, and land management. Precision agriculture adoption exceeds 65% among large farms, driven by GPS-guided tractors, autonomous harvesters, and telematics-enabled forestry equipment. Tractor penetration exceeds 90 units per 1,000 hectares, and over 70% of new equipment sales integrate digital monitoring or automation features.

Market Size & Growth: Valued at USD 186.9 billion in 2024 and projected to reach USD 267.8 billion by 2032, growing at a CAGR of 4.6%, driven by mechanization intensity and productivity-focused equipment upgrades.

Top Growth Drivers: Farm mechanization adoption (+42%), operational efficiency improvement (+28%), labor dependency reduction (+35%).

Short-Term Forecast: By 2028, average operational cost reduction of 18% is expected through automation and precision-guided machinery.

Emerging Technologies: Autonomous tractors, AI-based yield optimization systems, and IoT-enabled forestry harvesters.

Regional Leaders: North America projected at USD 89.5 billion by 2032 with high precision adoption; Europe at USD 71.2 billion driven by sustainability-focused machinery; Asia-Pacific at USD 82.6 billion supported by rapid mechanization in emerging economies.

Consumer/End-User Trends: Large commercial farms and forestry operators increasingly prefer integrated machinery platforms with predictive maintenance and real-time analytics.

Pilot or Case Example: A 2024 autonomous tractor pilot in North America achieved a 22% reduction in fuel usage and 19% productivity gain.

Competitive Landscape: Deere & Company (~28% share) followed by CNH Industrial, AGCO Corporation, Kubota Corporation, and CLAAS Group.

Regulatory & ESG Impact: Emission compliance standards, precision-farming incentives, and carbon reduction mandates accelerating adoption of efficient machinery.

Investment & Funding Patterns: Over USD 52 billion invested globally since 2022, with strong project finance and OEM-led technology partnerships.

Innovation & Future Outlook: Expansion of fully autonomous fleets, digital farm ecosystems, and electrified machinery platforms shaping long-term industry transformation.

The Agricultural and Forestry Machinery Market spans key sectors including tractors (approximately 38% of equipment demand), harvesting machinery (26%), forestry equipment (18%), and planting and cultivation machinery (remaining share). Recent innovations such as hybrid-electric tractors, autonomous logging systems, and AI-driven equipment diagnostics are reshaping operational efficiency. Regulatory emphasis on emission reduction and sustainable land use continues to influence equipment design and procurement. Regionally, North America and Europe emphasize technology-intensive machinery, while Asia-Pacific shows strong volume growth driven by rising mechanization rates. Future outlook remains positive, supported by digital integration, automation, and increasing capital expenditure in modern agricultural infrastructure.

The Agricultural and Forestry Machinery Market holds strategic relevance as a critical enabler of global food security, sustainable land management, and productivity optimization amid labor shortages and climate variability. Enterprises are increasingly aligning capital allocation toward smart machinery that integrates automation, connectivity, and data analytics to stabilize yields and reduce operational volatility. Autonomous tractor platforms deliver approximately 25% improvement in fuel efficiency and field productivity compared to conventional manually operated tractors, establishing a clear benchmark for technology-led competitiveness. Asia-Pacific dominates in volume due to high equipment deployment across small and mid-sized farms, while North America leads in adoption with over 68% of large agricultural enterprises using precision or semi-autonomous machinery.

By 2027, AI-driven precision farming systems are expected to improve input utilization efficiency by nearly 30%, particularly in fertilizer and water application, supporting short-term profitability and long-term resource conservation. From a compliance and ESG perspective, firms are committing to sustainability metrics such as 20–25% reduction in equipment-related emissions and 40% recyclability of machine components by 2030 through electrification and lightweight material adoption. In a measurable micro-scenario, in 2024, a U.S.-based agricultural equipment manufacturer achieved a 21% reduction in machine downtime by deploying predictive maintenance powered by IoT and machine-learning algorithms. Looking ahead, the Agricultural and Forestry Machinery Market is positioned as a pillar of operational resilience, regulatory compliance, and sustainable growth, supporting both industrial-scale producers and evolving environmental mandates.

Rising mechanization intensity is a primary driver of the Agricultural and Forestry Machinery Market as farms and forestry operators seek productivity gains amid shrinking labor availability. In developed economies, over 70% of agricultural land is now cultivated using mechanized equipment, while emerging regions are rapidly increasing tractor density per hectare. Mechanized harvesting and planting systems can improve operational efficiency by 20–35% compared to manual or semi-mechanized practices. Forestry operations adopting advanced logging machinery report up to 40% reduction in cycle time and significant improvements in worker safety. Government-backed mechanization programs and equipment financing schemes further reinforce adoption, particularly among mid-sized farms transitioning toward commercial-scale operations.

High upfront equipment costs and ongoing maintenance complexity remain significant restraints within the Agricultural and Forestry Machinery Market. Advanced tractors, harvesters, and forestry machines often require substantial capital investment, placing pressure on small and marginal operators. Maintenance expenses can account for nearly 15–20% of total equipment lifecycle costs, particularly for technology-intensive machinery requiring skilled technicians and proprietary parts. Limited availability of service infrastructure in rural and remote regions exacerbates downtime risks. Additionally, fluctuations in raw material prices and component supply chains contribute to price volatility, delaying purchase decisions and encouraging extended use of aging equipment fleets.

Digitalization and autonomous systems present significant growth opportunities in the Agricultural and Forestry Machinery Market. Precision guidance, autonomous navigation, and real-time analytics enable farms to optimize input usage and improve yield predictability. Autonomous machinery can operate for extended hours, delivering up to 30% higher land coverage per day. Forestry operators benefit from remotely monitored equipment that enhances safety and operational transparency. Equipment-as-a-service models and data-driven service contracts are also emerging, lowering entry barriers and enabling recurring value creation. These developments open new revenue streams for manufacturers while improving return on investment for end-users.

Regulatory complexity and workforce skills gaps pose ongoing challenges for the Agricultural and Forestry Machinery Market. Compliance with evolving emission standards and safety regulations increases design complexity and certification timelines for new equipment. At the operational level, effective utilization of advanced machinery requires digital literacy and technical expertise that are often lacking in rural labor pools. Training programs and upskilling initiatives add indirect costs for operators. Moreover, cross-border differences in regulatory frameworks complicate global equipment standardization, increasing customization requirements and slowing international market expansion.

• Accelerated Adoption of Autonomous and Semi-Autonomous Machinery: Automation is rapidly reshaping the Agricultural and Forestry Machinery market, with over 48% of newly deployed tractors and harvesters now equipped with semi-autonomous steering or task automation features. Field trials show productivity improvements of 22–30% per operating hour, while fuel optimization systems deliver 18% lower consumption. Large-scale farms adopting autonomous fleets report up to 35% reduction in labor dependency, particularly during peak planting and harvesting seasons, improving operational continuity.

• Expansion of Precision and Data-Driven Equipment Platforms: Precision agriculture tools integrated into machinery are seeing widespread adoption, with more than 62% of commercial farms using GPS-guided equipment and sensor-based implements. Variable rate technology enables 25% fertilizer savings and 20% water-use reduction per hectare. Forestry machinery fitted with real-time terrain and load analytics has improved operational accuracy by 28%, reducing equipment wear and unplanned downtime by approximately 15% across intensive logging operations.

• Rising Demand for Electrified and Low-Emission Machinery: Electrification is gaining traction as sustainability targets tighten, with electric and hybrid agricultural machinery deployments growing by over 40% in pilot and early commercial programs. Battery-assisted tractors demonstrate 35–45% lower direct emissions compared to diesel-only models, while noise reduction of nearly 50% supports extended operating hours. Forestry operators using hybrid harvesters report 17% lower maintenance intervals due to simplified powertrain architectures.

• Growth of Modular and Prefabrication-Enabled Machinery Applications: Modular and prefabricated construction practices are influencing machinery demand, particularly for equipment supporting pre-fabricated agricultural infrastructure and controlled-environment facilities. Approximately 55% of new projects utilizing modular approaches achieved measurable cost benefits, while automated cutting and forming machinery reduced on-site labor requirements by 30%. Demand for high-precision, CNC-enabled agricultural machinery has increased by over 25% in Europe and North America, where efficiency and standardization are critical.

The Agricultural and Forestry Machinery market is segmented by type, application, and end-user, reflecting diverse operational needs across farming and forestry value chains. Equipment demand varies by mechanization intensity, land size, crop patterns, and forest management practices. Type-based segmentation highlights the dominance of tractors and harvesting machinery, while application-based segmentation shows strong concentration in agricultural production and commercial forestry operations. End-user segmentation underscores the growing role of large commercial farms alongside expanding adoption among contractors and government-backed land management agencies. Across all segments, technology integration, automation readiness, and equipment lifecycle efficiency are key differentiators shaping purchasing behavior and deployment strategies.

Tractors represent the leading product type in the Agricultural and Forestry Machinery market, accounting for approximately 41% of total equipment adoption due to their versatility across plowing, hauling, planting, and harvesting support functions. Harvesting machinery holds around 27%, driven by combine harvesters and forage harvesters supporting large-scale crop operations. Forestry-specific machinery, including feller bunchers, skidders, and forwarders, contributes nearly 18%, reflecting steady demand from commercial logging and land management activities.

Precision-enabled and autonomous machinery is the fastest-growing type, expanding at an estimated CAGR of 9.8%, supported by rising adoption of GPS guidance, AI-based navigation, and remote monitoring systems. These machines reduce fuel usage by 18–25% and improve task accuracy by over 30%, accelerating replacement cycles. Remaining types such as planting equipment, sprayers, and soil preparation machinery collectively account for about 14%, serving niche and seasonal applications.

Agricultural production is the dominant application segment, representing nearly 63% of total machinery utilization, supported by intensive use in crop cultivation, harvesting, and post-harvest handling. Forestry operations account for approximately 24%, driven by mechanized logging, land clearing, and biomass extraction. Agriculture-focused machinery adoption remains higher due to year-round equipment utilization and multi-crop applicability.

Forestry mechanization is the fastest-growing application, expanding at an estimated CAGR of 8.6%, supported by stricter safety norms and the need for efficient timber extraction. Advanced forestry machines have reduced manual labor exposure by over 45% and improved harvesting cycle times by nearly 35%. Other applications, including landscaping, land reclamation, and infrastructure-related land preparation, collectively contribute around 13%.

Large commercial farms are the leading end-user segment, accounting for approximately 46% of machinery demand due to high equipment utilization rates and strong capital investment capacity. Agricultural contractors follow with nearly 29%, providing mechanized services to small and mid-sized farms and supporting shared equipment models. Forestry enterprises contribute about 17%, driven by continuous investment in high-capacity and safety-focused machinery.

Agricultural contractors are the fastest-growing end-user group, expanding at an estimated CAGR of 10.2%, fueled by rising demand for outsourced mechanized services and reduced ownership costs for smallholders. Adoption rates among contractors exceed 60% for multi-functional tractors and harvesting systems. Remaining end-users, including government agencies, cooperatives, and land management authorities, collectively represent around 8%.

North America accounted for the largest market share at 34.2% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2025 and 2032.

North America’s leadership is supported by high mechanization density exceeding 90 tractors per 1,000 hectares, strong replacement demand, and advanced precision farming adoption above 65%. Europe followed with a 27.6% share, driven by sustainability-led equipment upgrades and emission-compliant machinery. Asia-Pacific contributed 29.1% of global demand, supported by rising mechanization across China, India, and Southeast Asia, where tractor penetration increased by over 18% in the last four years. South America held 6.1%, anchored by large-scale commercial farming in Brazil and Argentina, while the Middle East & Africa accounted for 3.0%, reflecting gradual modernization and government-backed mechanization initiatives. Regional demand patterns continue to diverge based on farm size, policy frameworks, technology readiness, and access to financing.

How is large-scale automation redefining purchasing behavior across mature farming ecosystems?

The region holds approximately 34.2% of global Agricultural and Forestry Machinery demand, supported by extensive use across row-crop farming, commercial forestry, and contract farming services. Agriculture, forestry management, and biofuel feedstock production are the primary demand-driving industries. Regulatory support includes equipment electrification incentives and emission compliance standards targeting over 20% reduction in machinery-related emissions by 2030. Digital transformation is advanced, with more than 68% of enterprises using GPS-guided or telematics-enabled equipment. Local manufacturers are expanding autonomous tractor and smart harvester portfolios, while end-users favor high-capacity machinery with predictive maintenance features. Consumer behavior shows preference for premium, technology-intensive equipment, with higher enterprise adoption across large farms and contract operators.

How are sustainability mandates accelerating equipment modernization across regulated landscapes?

Europe represents nearly 27.6% of the Agricultural and Forestry Machinery market, with Germany, France, and the UK collectively contributing over 55% of regional demand. Strong regulatory oversight and environmental compliance frameworks have increased adoption of low-emission and precision-enabled machinery. More than 60% of newly registered agricultural equipment meets advanced emission standards, while digital field management tools are used by approximately 52% of commercial farms. Regional manufacturers are investing in electrified tractors and smart implements to align with circular economy targets. Consumer behavior is shaped by regulatory pressure, leading to higher demand for transparent, efficiency-verified machinery and lifecycle-optimized equipment.

Why is scale-driven mechanization reshaping equipment demand across emerging economies?

Asia-Pacific ranks as the fastest-expanding region, contributing 29.1% of global machinery volume. China, India, and Japan dominate consumption, together accounting for over 70% of regional equipment deployment. Infrastructure development, localized manufacturing, and government-backed mechanization programs have increased tractor availability by more than 20% in rural areas over five years. Innovation hubs focusing on compact tractors, low-cost harvesters, and digital monitoring systems are expanding rapidly. Local manufacturers are scaling production of affordable, multi-purpose equipment. Consumer behavior reflects growth driven by mobile-enabled farm services, cooperative ownership models, and rapid adoption among small and mid-sized farms.

How are export-oriented farming models influencing equipment investment cycles?

South America accounts for approximately 6.1% of global demand, led by Brazil and Argentina, which together represent over 75% of regional machinery usage. Large-scale soybean, corn, and sugarcane farming drives high-capacity tractor and harvester demand. Infrastructure improvements and favorable trade policies support machinery imports and localized assembly. Government incentives for farm modernization have increased mechanized land coverage by nearly 15% since 2020. Regional players focus on durable, high-horsepower equipment suited for extensive acreage. Consumer behavior is closely tied to export crop cycles, with purchasing decisions aligned to commodity performance and seasonal financing availability.

How is gradual mechanization supporting food security and land optimization goals?

The Middle East & Africa region contributes about 3.0% of global Agricultural and Forestry Machinery demand. Growth is concentrated in countries such as the UAE, Saudi Arabia, and South Africa, where controlled-environment agriculture and commercial farming are expanding. Mechanization supports agriculture, land reclamation, and forestry management linked to construction and infrastructure projects. Technological modernization includes adoption of irrigation-integrated machinery and remote monitoring systems. Trade partnerships and import incentives are improving equipment accessibility. Consumer behavior reflects demand for robust, low-maintenance machinery adapted to arid conditions and variable terrain.

United States Agricultural and Forestry Machinery Market – 26.8% share: Dominance driven by high production capacity, advanced precision farming adoption, and strong commercial farm demand.

China Agricultural and Forestry Machinery Market – 18.9% share: Leadership supported by large-scale mechanization programs, expanding domestic manufacturing, and rapid deployment across small and mid-sized farms.

The Agricultural and Forestry Machinery market exhibits a moderately consolidated competitive structure, characterized by the presence of approximately 40–50 active global and regional manufacturers competing across tractors, harvesting machinery, and forestry equipment. The top five companies collectively account for nearly 62% of total equipment deployment worldwide, reflecting strong brand loyalty, established dealer networks, and scale-driven manufacturing advantages. Market leaders maintain dominant positioning through continuous product innovation, high R&D intensity averaging 4–6% of annual operating budgets, and accelerated rollout of autonomous, precision-guided, and low-emission machinery platforms.

Strategic initiatives increasingly define competitive differentiation. Over 65% of leading manufacturers launched digitally enabled equipment or software-integrated upgrades between 2023 and 2025, while partnership activity rose by 28%, particularly in AI navigation, battery systems, and telematics integration. Mergers and acquisitions remain selective, with consolidation focused on acquiring niche precision-technology providers rather than expanding traditional manufacturing capacity. The market also reflects competitive pressure from regional manufacturers, which account for nearly 30% of unit volumes in Asia-Pacific and South America by offering cost-optimized machinery. Innovation trends such as autonomous fleets, predictive maintenance, and equipment-as-a-service models continue to reshape competitive dynamics and long-term positioning.

Deere & Company

CNH Industrial N.V.

AGCO Corporation

Kubota Corporation

CLAAS Group

Mahindra & Mahindra Ltd.

Yanmar Holdings Co., Ltd.

SDF Group

Escorts Kubota Limited

J C Bamford Excavators Ltd.

Technology evolution is fundamentally reshaping the Agricultural and Forestry Machinery market, with a strong shift toward automation, connectivity, and sustainability-driven engineering. Precision agriculture technologies are now embedded in over 65% of newly manufactured tractors and harvesting machines, enabling GPS-guided steering accuracy within ±2.5 cm, which reduces overlap during field operations by nearly 20%. Advanced telematics platforms monitor fuel consumption, engine health, and implement performance in real time, helping operators achieve 15–25% improvements in equipment uptime through predictive maintenance.

Autonomous and semi-autonomous machinery represents one of the most impactful advancements. Self-guided tractors and harvesters equipped with AI-based vision systems can operate continuously for up to 20 hours per day, increasing land coverage by 30–35% compared to manually operated equipment. In forestry applications, automated load balancing and terrain-adaptive control systems have reduced equipment tip-over incidents by 40%, significantly improving operator safety. Machine learning algorithms also support yield prediction and task optimization, improving input efficiency by approximately 25% across large-scale farming operations.

Electrification and hybrid powertrains are gaining momentum as emission regulations tighten. Battery-assisted tractors and hybrid harvesters demonstrate 35–45% reductions in direct emissions and lower noise levels by nearly 50%, enabling extended operational windows. Materials innovation, including high-strength lightweight alloys and advanced composites, is improving durability while reducing overall machine weight by 10–15%. Together, these technologies are transforming the Agricultural and Forestry Machinery market into a digitally integrated, efficiency-driven ecosystem aligned with long-term sustainability and productivity objectives.

In 2024, Deere & Company expanded its autonomous machinery portfolio by commercializing second-generation autonomous tractors equipped with advanced computer vision and AI-based obstacle detection, enabling fully driverless tillage operations. The platform demonstrated productivity gains of over 30% in large-scale row crop farming deployments.

In 2024, AGCO Corporation advanced electrification by initiating series production of its Fendt e100 Vario electric tractor, designed for municipal, specialty crop, and livestock operations. The model supports zero-emission operation with up to five hours of runtime, addressing sustainability and noise-reduction requirements.

In 2023, CNH Industrial strengthened its precision and autonomy capabilities through deeper integration of autonomous guidance, sensing, and control technologies across its Case IH and New Holland equipment lines, enabling enhanced automated harvesting and planting workflows with reduced operator intervention.

In 2023, Kubota Corporation unveiled next-generation autonomous and smart agriculture machinery concepts, focusing on scalable automation, fleet coordination, and digital farm management, aimed at addressing labor shortages and improving operational efficiency across small and mid-sized farms.

The Agricultural and Forestry Machinery Market Report provides a comprehensive assessment of equipment used across agricultural production, forestry operations, and land management activities. The scope covers key machinery types including tractors, harvesting equipment, planting and cultivation machinery, and specialized forestry machines, addressing both conventional and technology-enabled variants. The report evaluates applications spanning commercial farming, contract-based agricultural services, mechanized forestry, biomass harvesting, and land development projects.

Geographically, the analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional variations in mechanization intensity, equipment penetration, and technology adoption. The report incorporates insights into precision agriculture systems, autonomous and semi-autonomous machinery, electrified powertrains, and digital fleet management platforms, highlighting their influence on operational efficiency and equipment lifecycle optimization.

End-user coverage includes large commercial farms, agricultural contractors, forestry enterprises, cooperatives, and government-backed land management agencies. The scope also considers emerging segments such as equipment-as-a-service models, shared machinery platforms, and hybrid-electric forestry equipment. Overall, the report is designed to support strategic planning, investment assessment, and competitive benchmarking by delivering structured insights into market structure, technology evolution, regional deployment patterns, and industry transformation dynamics.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 186909.74 Million |

|

Market Revenue in 2032 |

USD 267846.15 Million |

|

CAGR (2025 - 2032) |

4.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Deere & Company , CNH Industrial N.V., AGCO Corporation , Kubota Corporation , CLAAS Group, Mahindra & Mahindra Ltd., Yanmar Holdings Co., Ltd., SDF Group, Escorts Kubota Limited, J C Bamford Excavators Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |