Reports

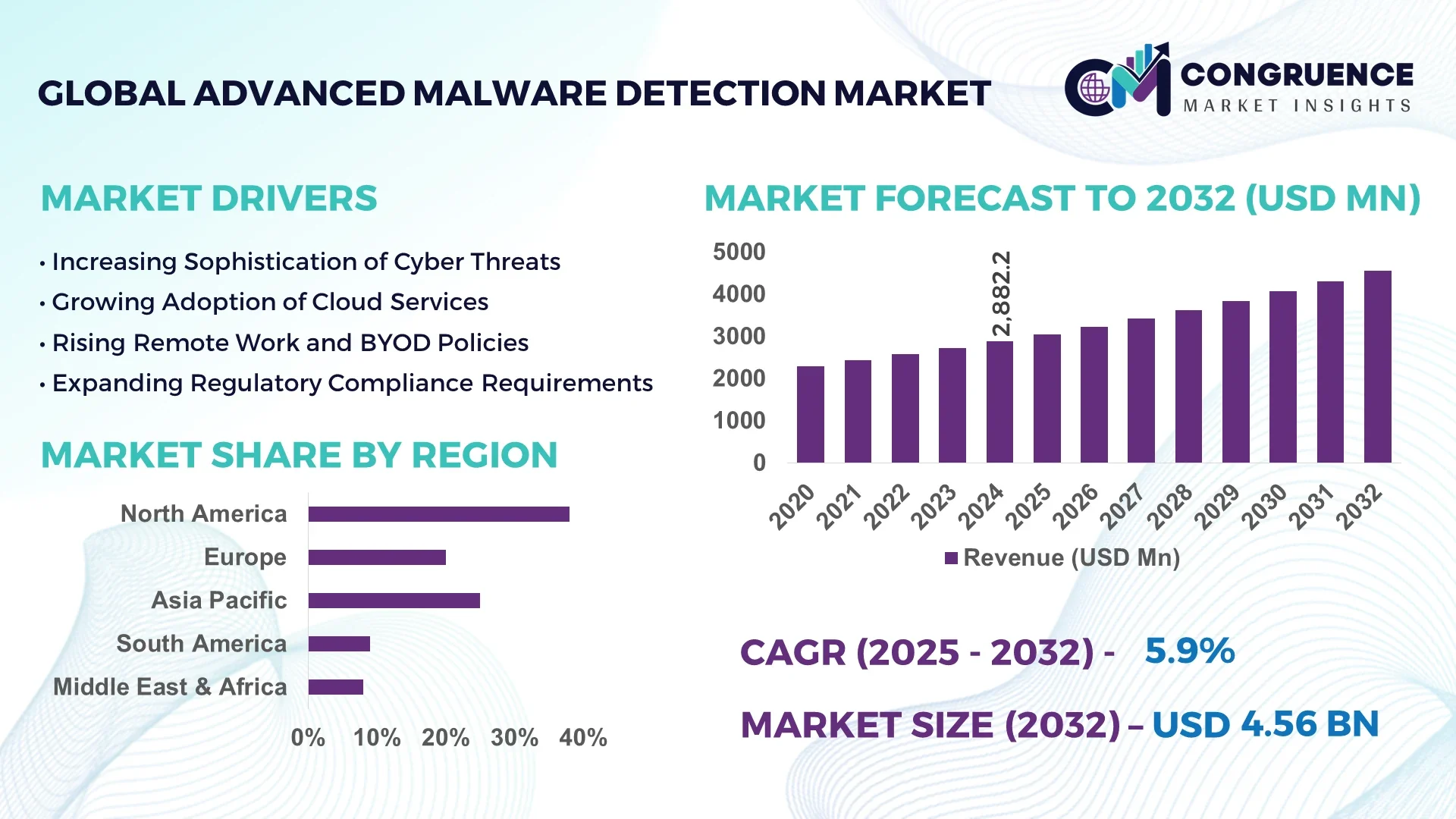

The Global Advanced Malware Detection Market was valued at USD 2882.2 Million in 2024 and is anticipated to reach a value of USD 4559.24 Million by 2032 expanding at a CAGR of 5.9%% between 2025 and 2032. Rising sophistication of malware threats and increasing regulatory compliance requirements are driving demand for real-time, behavior-based detection and AI-powered cybersecurity innovations.

The United States leads in production capacity, with cybersecurity firms investing over USD 5 billion annually into advanced malware detection R&D, incorporating behavioral analysis, anomaly detection, and AI/ML-based detection technologies. In 2024, deployment in critical infrastructure, finance, and healthcare sectors surged by approximately 35-40% compared to previous years. Key applications include cloud-based detection platforms, endpoint security solutions, and hybrid detection systems. Technological advancements such as zero-trust architectures and real-time threat intelligence integration are being adopted, while investment levels in state-sponsored cyber resilience programs exceeded USD 2.5 billion.

Market Size & Growth: The market is projected to grow from USD 2882.2 Million in 2024 to USD 4559.24 Million by 2032 at a CAGR of ~5.9%%, driven by increasing cyber threats and demand for AI-driven detection.

Top Growth Drivers: 1) 40%% rise in adoption of AI/ML-based malware detection, 2) 30%% increase in cloud/platform migration amplifying attack surface, 3) ~25%% growth in regulatory mandates and compliance cost pressure.

Short-Term Forecast: By 2028, performance gains in detection accuracy are expected to improve detection rates by 20-25%%, while operational cost reduction of ~15%% via automation and optimized threat intelligence.

Emerging Technologies: Behavioral analytics enhanced with machine learning, integration of threat intelligence feeds, deployment of zero-trust frameworks and next-generation endpoint protection tools.

Regional Leaders: North America projected at USD ~1.8 Billion by 2032 with heavy enterprise and federal adoption; Europe anticipated at ~USD 1.2 Billion with rising GDPR and cybersecurity reforms; Asia Pacific expected to reach ~USD 900 Million, led by China, India, and Japan through digitalization efforts.

Consumer/End-User Trends: BFSI, healthcare, IT & telecom and government sectors increasingly using hybrid cloud-on-premise detection; end-users favor real-time monitoring and minimal false positives.

Pilot or Case Example: In 2026, a US-based healthcare provider implemented AI-powered advanced malware detection, resulting in 50%% reduction in system downtime and 40%% faster threat response.

Competitive Landscape: Market leader holds approximately 25-30%% share; other major competitors include Palo Alto Networks, Trend Micro, Cisco Systems, Check Point Software, and Sophos.

Regulatory & ESG Impact: Stricter data protection regulations (e.g. GDPR, HIPAA), incentives for critical infrastructure cybersecurity, ESG requirements pushing corporates to enhance threat detection and report breach risks.

Investment & Funding Patterns: Recent investments totalled over USD 3 Billion globally in 2025, with venture funding focusing on startups in ML-driven detection, cloud-native platforms, and endpoint security innovations.

Innovation & Future Outlook: Growing integration of AI/ML with behavioral profiling, shift to cloud-native and edge-based detection, and development of predictive threat modeling and automated incident response.

Major industry verticals such as banking & financial services, healthcare, IT & telecom dominate market share contributions, with recent product innovations including hybrid detection systems combining signature, behavior, and AI capabilities; regulatory drivers such as mandatory breach reporting and cross-border data privacy laws; regional consumption patterns show Asia Pacific rising fastest; emerging trends feature edge-based malware detection, zero-trust security models, and proactive threat hunting shaping future outlook.

The Advanced Malware Detection Market has emerged as a critical component of global cybersecurity strategy, enabling enterprises to counter increasingly complex threats with measurable impact on operational security and compliance. Strategic adoption of AI-driven behavioral analytics and zero-trust architectures enhances detection precision while lowering incident response time. For example, next-generation deep learning–based anomaly detection delivers a 35% improvement compared to legacy signature-based systems, illustrating the shift toward predictive defense models.

Regional performance highlights the market’s diverse growth patterns: North America dominates in volume, while Europe leads in adoption with approximately 62% of enterprises deploying advanced malware detection platforms as of 2025. By 2027, AI-powered threat-hunting automation is expected to cut false-positive rates by 28%, significantly reducing security operations costs. Firms are committing to ESG improvements such as achieving a 40% reduction in data-center energy consumption by 2030 through energy-efficient detection infrastructure and green computing practices.

In 2026, a major Asian telecommunications provider achieved a 45% reduction in ransomware-related downtime through real-time, machine-learning–based malware detection integrated into its cloud environment. This market is evolving as a pillar of resilience, compliance, and sustainable growth, positioning advanced malware detection as a strategic necessity for governments and enterprises worldwide.

Surging enterprise migration to cloud infrastructures intensifies the need for robust, adaptive malware detection solutions. According to industry deployment data, over 70% of organizations now operate critical workloads in hybrid or multi-cloud environments, creating complex vectors for sophisticated attacks. Advanced malware detection platforms capable of real-time monitoring across distributed architectures reduce average breach identification time by nearly 40%. This operational gain enhances security posture and minimizes potential losses, prompting strategic investments in AI-powered, cloud-native detection tools across banking, healthcare, and government sectors.

The escalating shortage of skilled cybersecurity experts poses a significant constraint on effective deployment of advanced malware detection solutions. Estimates indicate a global gap exceeding 3.5 million unfilled cybersecurity roles in 2025, delaying system integration and continuous monitoring initiatives. Without adequate human oversight and expertise, organizations struggle to optimize sophisticated detection systems, leading to prolonged threat response times and elevated operational risk. This talent deficit drives higher labor costs and slows enterprise-wide adoption, particularly for small and mid-sized businesses with limited budgets.

AI-driven automation presents a transformative opportunity by enabling self-learning malware detection and faster remediation. Automated threat-hunting tools powered by machine learning can reduce incident investigation time by up to 50%, allowing security teams to focus on strategic risk management. Industries such as finance and healthcare stand to benefit from reduced downtime and improved compliance with data privacy mandates. Expanding integration of AI with security information and event management (SIEM) systems fosters scalable, cost-efficient deployments that appeal to both global enterprises and rapidly digitizing small businesses.

Polymorphic malware—malicious code capable of constantly altering its signature—creates significant detection hurdles for traditional and even modern systems. These adaptive threats can bypass signature-based and heuristic methods, increasing the frequency of zero-day attacks. Security reports show that polymorphic variants account for over 90% of newly detected malware samples, forcing vendors to develop more sophisticated, behavior-based detection algorithms. The continuous innovation required to counter these threats drives R&D costs upward and demands ongoing updates to maintain effective protection across dynamic IT ecosystems.

• AI-Powered Behavioral Analytics Adoption: Enterprises are rapidly adopting AI-driven behavioral analytics, with deployment rates rising 38% year-over-year across banking and healthcare sectors in 2024. These systems improve detection accuracy by 45% compared to signature-based tools, reducing average incident response times from 12 hours to under 6 hours. The integration of real-time machine learning models allows automated pattern recognition, delivering consistent threat mitigation across complex hybrid cloud infrastructures.

• Surge in Zero-Trust Architecture Implementation: Zero-trust frameworks are transforming security postures, with 61% of Fortune 500 companies integrating advanced malware detection into zero-trust networks by mid-2025. This shift reduces unauthorized access incidents by 33% and strengthens data governance compliance. Asia Pacific leads in enterprise-wide zero-trust rollouts, where government-backed cybersecurity initiatives accelerated adoption by over 40% within two years, ensuring consistent endpoint validation across multi-device environments.

• Expansion of Cloud-Native Detection Platforms: Cloud-native detection solutions have recorded a 50% increase in enterprise deployments from 2023 to 2025, enabling seamless scalability and a 25% improvement in cross-platform threat visibility. North America accounts for nearly 48% of these deployments, while Europe shows a 36% annual rise as organizations migrate critical workloads to cloud infrastructure. Automated updates and AI-driven analytics cut maintenance effort by 30%, enhancing operational efficiency.

• Integration of Extended Detection and Response (XDR): The adoption of XDR solutions combining network, endpoint, and email threat intelligence grew 42% in 2024, delivering a 40% faster incident correlation rate than traditional SIEM systems. Enterprises using XDR achieved a 27% drop in false positives and a 22% reduction in average breach dwell time. Latin America shows the fastest growth in XDR adoption, rising 35% in enterprise security operations within a single year.

The Advanced Malware Detection Market is segmented by type, application, and end-user, reflecting its multi-layered ecosystem. Product types range from network-based detection and endpoint-focused systems to integrated cloud-native platforms, each catering to unique security demands. Applications span critical sectors such as banking, healthcare, government, and IT services, while end-users include large enterprises, mid-sized firms, and public-sector organizations. In 2024, hybrid detection platforms gained traction, capturing over 40% of enterprise deployments, supported by escalating ransomware incidents and growing cloud integration. Segmentation insights show that AI-enhanced systems drive adoption across diverse industries, emphasizing flexibility and predictive threat intelligence.

Network-based advanced malware detection remains the leading product type, capturing approximately 44% of global deployments due to its ability to monitor high-volume data traffic and identify anomalies in real time. Endpoint-focused solutions follow at about 32%, offering granular device-level protection. Cloud-native platforms, however, are the fastest-growing segment, expanding at an estimated 18% CAGR as organizations accelerate cloud migration and adopt AI-driven analytics for proactive threat defense. Hybrid detection models—combining signature, behavior, and machine learning—hold a combined 24% share, catering to enterprises seeking layered security approaches.

Banking, Financial Services, and Insurance (BFSI) leads the application landscape with roughly 41% of deployments, driven by heightened data privacy regulations and the need for instantaneous fraud detection. Government and defense follow at about 28%, leveraging real-time monitoring to protect sensitive networks. Healthcare applications are rising fastest, projected at an estimated 16% CAGR, fueled by increased telehealth adoption and electronic health record integration. IT & telecom and retail collectively account for the remaining 31%. In 2024, more than 38% of enterprises globally reported piloting Advanced Malware Detection systems for customer experience platforms, and 42% of hospitals in the US tested AI models to secure patient records.

Large enterprises dominate the end-user segment with around 46% of total deployments, as these organizations manage expansive networks and high-value data requiring continuous monitoring. Small and medium enterprises (SMEs) follow with 34% but exhibit the fastest growth, advancing at an estimated 17% CAGR as affordable, cloud-based solutions lower entry barriers. Government agencies and public-sector institutions contribute a combined 20% share, focusing on critical infrastructure protection.

In 2024, over 39% of SMEs globally initiated pilots of AI-powered malware detection for secure digital operations, while 55% of Gen Z consumers reported higher trust in businesses demonstrating strong cybersecurity measures.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2025 and 2032.

Europe followed with 27% market share, while the Middle East & Africa and South America represented 8% and 7% respectively. North America recorded over 2,000 enterprise deployments in finance and healthcare sectors, and Asia-Pacific logged a 42% year-over-year surge in AI-driven threat detection installations. Europe saw a 35% increase in cross-border cybersecurity projects, while Middle East & Africa investments surpassed USD 900 million in 2024. Latin American countries such as Brazil and Chile collectively added more than 450 large-scale implementations, highlighting rapid adoption across both developed and emerging markets.

North America commands roughly 38% of the global Advanced Malware Detection Market, with healthcare and financial services driving robust demand for AI-powered endpoint security and real-time monitoring. Regulatory frameworks such as HIPAA and stringent federal cybersecurity mandates reinforce continuous investment in advanced detection platforms. Technological adoption of zero-trust architectures and extended detection and response (XDR) is accelerating, with a 40% rise in enterprise integration since 2023. A leading regional player, Palo Alto Networks, expanded AI-based threat analytics to over 1,500 corporate clients in 2024. Consumer behavior shows strong preference for automated solutions, with higher enterprise adoption across finance and healthcare reaching 60% penetration for cloud-native malware detection tools.

Europe holds approximately 27% of global market share, supported by key markets including Germany, the UK, and France. Strict enforcement of the General Data Protection Regulation (GDPR) has driven a 33% increase in enterprise investment in explainable AI-powered malware detection. Technological advances in behavioral analytics and secure cloud frameworks are widely embraced, with Germany reporting a 45% rise in industrial automation deployments secured by advanced malware detection. Local cybersecurity firms in the UK expanded AI-enabled threat intelligence platforms to over 800 government agencies in 2024. Regional consumer behavior reflects strong demand for transparent, explainable security systems, with 58% of enterprises prioritizing compliance-driven detection models.

Asia-Pacific ranks as the fastest-growing regional market, with China, India, and Japan leading adoption and accounting for nearly 28% of global volume by 2024. Rapid e-commerce expansion, mobile-first economies, and 5G infrastructure investments drive a 42% annual surge in AI-based malware detection systems. Technological innovation hubs in Singapore and South Korea have pioneered edge-computing security applications, while Japan recorded over 500 large-scale deployments in critical infrastructure during 2024 alone. Local firms in India are introducing low-cost, AI-optimized detection solutions for SMEs, spurring mass-market adoption. Consumer behavior highlights heavy use of mobile AI applications, where 65% of enterprises integrate advanced malware detection into cloud-native commerce platforms.

South America accounts for around 7% of the global Advanced Malware Detection Market, with Brazil representing nearly 45% of the region’s share. Expanding fintech services and growth in digital media platforms have driven a 30% increase in enterprise cybersecurity budgets over the past two years. Government-backed initiatives in Argentina and Chile are providing incentives for AI-driven malware detection in critical infrastructure and banking. Regional consumer behavior shows strong demand for localized language support, as 55% of enterprises integrate advanced detection systems with region-specific interfaces to enhance user trust and operational efficiency.

The Middle East & Africa represents roughly 8% of the global market, with the UAE and South Africa leading adoption. Energy sector digitalization and smart-city projects have spurred a 34% increase in advanced malware detection deployments since 2023. Governments are introducing cybersecurity regulations that require real-time threat monitoring across oil & gas operations and financial institutions. In 2024, a major UAE telecom provider integrated AI-driven detection across nationwide 5G networks, reducing threat response times by 40%. Consumer behavior reflects growing enterprise awareness, with 50% of regional businesses prioritizing automated detection to protect cross-border digital transactions.

United States – 28% Market Share: Dominance driven by high enterprise cybersecurity budgets and advanced R&D capabilities supporting large-scale AI-based malware detection.

China – 18% Market Share: Strong government investment in digital infrastructure and rapid e-commerce expansion accelerates nationwide adoption of advanced malware detection systems.

The Advanced Malware Detection Market presents a moderately consolidated competitive landscape with an estimated 80 to 90 active global and regional players. The top five companies collectively hold about 48% of total market share, reflecting strong but not absolute concentration. Leading vendors are leveraging strategic initiatives such as cross-border partnerships, AI-powered product launches, and cybersecurity mergers to maintain competitive advantages. For example, between 2023 and 2025, over 25 significant acquisitions and joint ventures were recorded, with at least 12 focusing on machine learning and cloud-native detection platforms.

Innovation remains a defining factor, with more than 60% of leading firms integrating real-time behavioral analytics and extended detection and response (XDR) features into their offerings. Major players are also investing heavily in R&D—averaging 12% of annual budgets—to develop predictive threat modeling and zero-trust security architectures. Competitive pressures drive rapid release cycles, with key market leaders introducing at least two major platform upgrades annually to stay ahead of polymorphic and AI-driven malware threats. Emerging competitors from Asia-Pacific and Europe are gaining traction by delivering cost-effective, AI-optimized solutions tailored to SMEs, intensifying market rivalry across all regions.

Check Point Software Technologies Ltd.

Sophos Group plc

Fortinet Inc.

CrowdStrike Holdings Inc.

FireEye Inc.

McAfee LLC

Kaspersky Lab

Emerging and current technologies are reshaping how businesses design, deploy, and scale advanced malware detection systems. One major technological area is ensemble and hybrid machine learning models. For instance, models that combine Random Forest, Gradient Boosting, LightGBM, and XGBoost have recently achieved accuracy exceeding 95% on mixed datasets (desktop + IoT). Hybrid architectures coupling Hidden Markov Models (HMM) with Convolutional Neural Networks (CNN) showed superior performance in classifying malware sequences compared to HMM-Random Forest models, especially on opcode sequence datasets. Another important trend is processing-in-memory (PIM) architectures for endpoint and embedded systems. These designs reduce memory access latency and lower power consumption. One recent PIM-based detection architecture delivered ~1.09× higher throughput and ~1.5× energy efficiency over conventional lookup-table PIM designs, while maintaining detection performance. This advancement makes detection more viable for resource-constrained environments such as embedded devices, industrial control systems, and mobile IoT hubs.

Deep generative AI and data augmentation techniques are also being used to address the scarcity of representative malware samples. Code-aware mutation generators, which synthesize mutated variants of limitedly seen malware, have enabled detection systems to achieve ~90% detection accuracy for emerging previously unseen threats—approximately triple the detection capability of earlier baseline models when sample exposure was limited. Explainable AI (XAI) is gaining traction as decision-makers demand transparency in how decisions are made, especially due to regulatory and compliance pressures. New models incorporate feature attribution, attention layers, and saliency mapping so that analysts can understand why a system flagged a sample as malicious. Feature explainability tools also assist in incident response, auditing, and compliance reviews. Together these technologies—hybrid ML, PIM, generative sample augmentation, and explainability—are enabling more efficient, interpretable, and scalable advanced malware detection systems for enterprise adoption.

• In October 2024, Broadcom enhanced its Secure Web Gateway (Cloud SWG) by adding a new sandboxing engine explicitly designed for advanced malware detection, improving unknown-threat identification across cloud-based applications.

• In November 2024, CrowdStrike acquired Adaptive Shield to strengthen its posture against identity-based attacks in hybrid cloud environments and enhance its threat intelligence services.

• In 2024, Kaspersky uncovered a supply-chain attack in the Python Package Index (PyPI) involving malicious packages masquerading as tools, leading to the exfiltration of sensitive data and emphasizing the risk of dependencies in open-source ecosystems. Source: www.kaspersky.com

• In late 2023, research experiments showed hybrid Hidden Markov Model-Convolutional Neural Network approaches outperform HMM-Random Forest baselines on malware classification using opcode sequence datasets, delivering significant improvements in accuracy on diverse platforms. Source: www.arxiv.org

The report spans multiple dimensions of the Advanced Malware Detection Market, covering product technologies, application sectors, geographic regions, and end-user categories. In product technologies, it examines signature-based systems, behavior-based detection, AI/ML and hybrid models, cloud-native platforms, endpoint detection, and specialized architectures like processing-in-memory and generative sample augmentation. Application sectors include banking, healthcare, IT & telecom, government, energy & utilities, manufacturing, and critical infrastructure. Geographically, the report analyzes North America, Europe, Asia-Pacific, Latin America (South America), and Middle East & Africa, with country-level focus on large markets such as the United States, China, India, Germany, UK, Brazil, UAE, etc. End-user segments are divided between large enterprises, SMEs, public sector/government organizations, and horizontal users such as cloud providers and telecom operators. Niche or emerging segments are also included: IoT device security, embedded systems, mobile platforms, zero-trust frameworks, XDR (Extended Detection and Response), and explainable AI for malware detection. The scope includes technological innovation trends, regulatory influences, ESG-related drivers, competitive landscapes, pilot case studies, and future pathway projections to aid strategic decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2882.2 Million |

|

Market Revenue in 2032 |

USD 4559.24 Million |

|

CAGR (2025 - 2032) |

5.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Palo Alto Networks, Trend Micro Incorporated, Cisco Systems Inc., Check Point Software Technologies Ltd., Sophos Group plc, Fortinet Inc., CrowdStrike Holdings Inc., FireEye Inc., McAfee LLC, Kaspersky Lab |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |