Reports

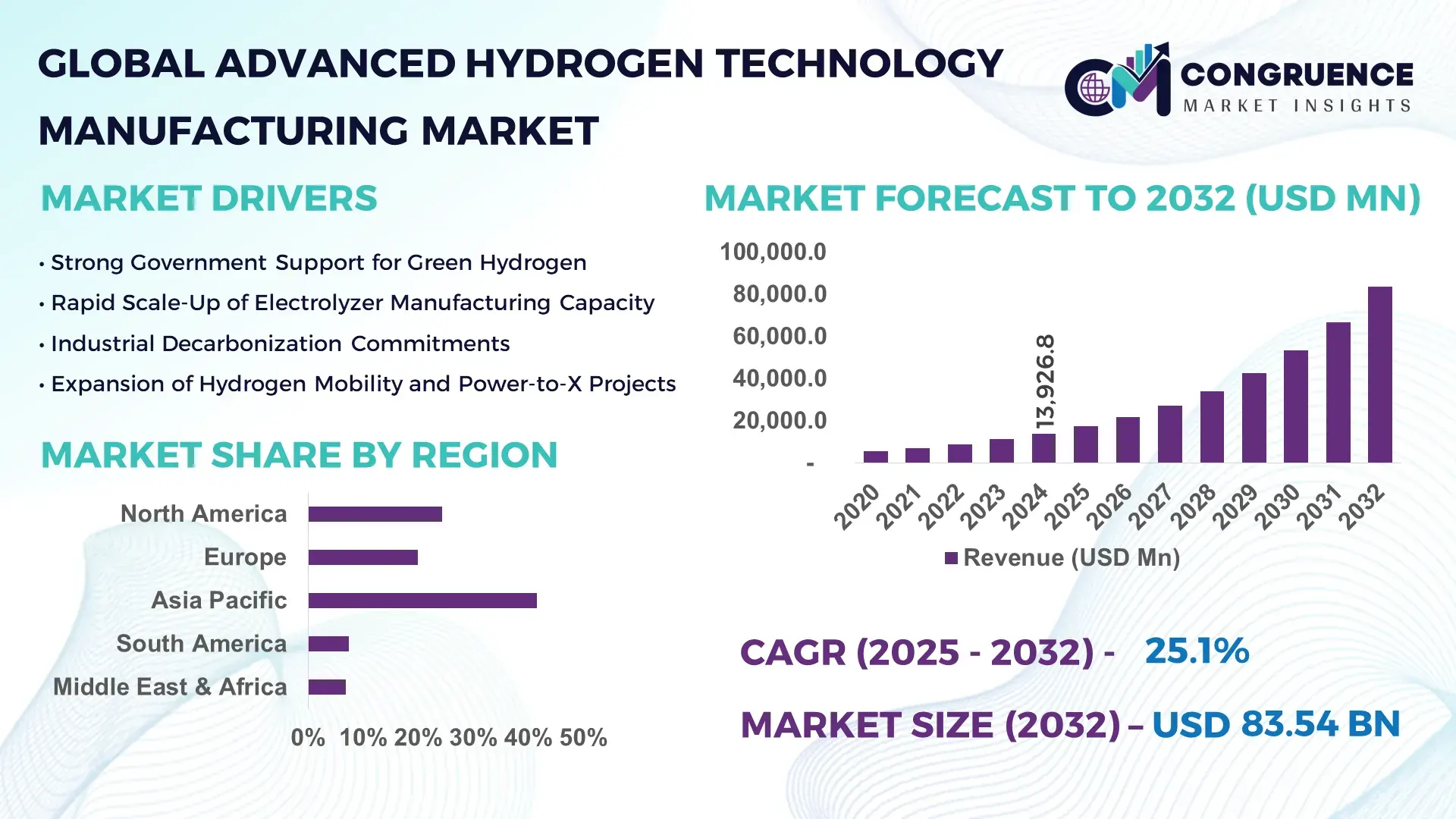

The Global Advanced Hydrogen Technology Manufacturing Market was valued at USD 13,926.8 Million in 2024 and is anticipated to reach a value of USD 83,543.0 Million by 2032 expanding at a CAGR of 25.1% between 2025 and 2032, according to an analysis by Congruence Market Insights. This rapid expansion is primarily driven by accelerated decarbonization mandates, large-scale electrolyzer deployments, and rising industrial demand for low-emission hydrogen across energy-intensive sectors.

China represents the most dominant country in the Advanced Hydrogen Technology Manufacturing Market, supported by large-scale electrolyzer manufacturing capacity exceeding 12 GW annually and cumulative hydrogen infrastructure investments crossing USD 18 billion. The country operates more than 300 hydrogen refueling stations and has deployed over 9,000 hydrogen-powered commercial vehicles. Industrial hydrogen adoption spans steelmaking, ammonia synthesis, and refinery desulfurization, with green hydrogen pilots accounting for nearly 35% of newly approved hydrogen projects. Technological advancements include domestically produced PEM and alkaline electrolyzers achieving efficiency levels above 75%, alongside automated stack manufacturing lines producing over 5,000 units annually.

Market Size & Growth: Valued at USD 13.9 billion in 2024, projected to reach USD 83.5 billion by 2032, expanding at a CAGR of 25.1% driven by industrial decarbonization and energy transition targets.

Top Growth Drivers: Electrolyzer adoption up 42%, industrial hydrogen substitution improving emissions efficiency by 38%, and government-backed hydrogen hubs accelerating deployment by 46%.

Short-Term Forecast: By 2028, advanced manufacturing automation is expected to reduce electrolyzer production costs by 28%.

Emerging Technologies: Solid oxide electrolyzers, AI-enabled process control, and high-pressure hydrogen storage composites.

Regional Leaders: Asia Pacific projected at USD 31.2 billion by 2032 with scale manufacturing; Europe at USD 26.4 billion driven by green mandates; North America at USD 18.7 billion led by industrial retrofits.

Consumer/End-User Trends: Heavy industries account for 54% of demand, while transport and power-to-gas applications show rising pilot adoption.

Pilot or Case Example: In 2024, a steel decarbonization pilot achieved 32% CO₂ reduction using hydrogen-based direct reduction.

Competitive Landscape: A leading manufacturer holds ~18% share, followed by four global players each ranging between 6–9%.

Regulatory & ESG Impact: Over 45 countries offer hydrogen tax credits, carbon pricing offsets, or production-linked incentives.

Investment & Funding Patterns: Recent global investments exceeded USD 52 billion, dominated by project finance and public–private partnerships.

Innovation & Future Outlook: Integrated electrolyzer–storage systems and modular gigafactories are shaping next-phase scalability.

Advanced Hydrogen Technology Manufacturing serves energy, chemicals, refining, and mobility sectors, with industrial applications contributing nearly 48% of demand. Innovations in membrane durability, stack miniaturization, and automated assembly lines are reducing unit costs. Policy-backed hydrogen corridors, rising renewable penetration, and cross-border supply agreements are reshaping regional consumption, while power-to-X and export-oriented hydrogen projects define the forward outlook.

The Advanced Hydrogen Technology Manufacturing Market has emerged as a strategic cornerstone for global energy transition strategies, industrial decarbonization, and long-term energy security planning. Manufacturing advancements across electrolyzers, hydrogen storage systems, and compression technologies are enabling scalable, low-emission hydrogen production for steel, chemicals, mobility, and grid-balancing applications. Proton exchange membrane electrolyzers deliver 22% higher load flexibility compared to conventional alkaline systems, improving compatibility with intermittent renewable energy inputs.

Asia Pacific dominates in production volume, while Europe leads in adoption, with over 61% of large industrial enterprises integrating hydrogen-based processes into decarbonization roadmaps. By 2027, AI-enabled electrolyzer optimization is expected to improve energy efficiency by 19% through predictive maintenance and real-time load balancing. Firms are committing to ESG performance metrics such as 40% lifecycle emission reductions and 30% water-use optimization by 2030 through closed-loop electrolysis systems.

In 2024, Germany achieved a 27% reduction in industrial hydrogen carbon intensity through national-scale green hydrogen hubs integrating offshore wind and advanced electrolyzer manufacturing. Strategic pathways increasingly emphasize modular gigafactories, localized supply chains, and digital twins for production optimization. Collectively, these developments position the Advanced Hydrogen Technology Manufacturing Market as a pillar of resilience, compliance, and sustainable industrial growth.

The Advanced Hydrogen Technology Manufacturing Market is shaped by accelerating clean energy mandates, industrial electrification limits, and the need for scalable zero-carbon fuels. Manufacturing capacity expansion, particularly for electrolyzers and storage systems, is influenced by declining renewable energy costs and national hydrogen strategies. Demand is further supported by infrastructure buildouts such as hydrogen pipelines, refueling stations, and export terminals. However, variability in regulatory clarity and infrastructure readiness across regions continues to influence investment pacing. Technological convergence between automation, materials science, and digital manufacturing platforms is enhancing production yields, while localization policies are reshaping global supply chains.

Industrial sectors account for over 30% of global CO₂ emissions, prompting accelerated adoption of hydrogen-based alternatives. In steel production, hydrogen direct reduction processes reduce emissions by up to 90% compared to coal-based methods. More than 120 industrial hydrogen projects reached final investment decisions in 2024, with electrolyzer manufacturing capacity expanding by over 60% year-on-year. Refineries and chemical plants increasingly substitute grey hydrogen with low-carbon variants, driving sustained demand for advanced manufacturing systems capable of large-scale, continuous operation.

Electrolyzer manufacturing facilities require capital investments exceeding USD 150 million per GW of annual capacity, creating entry barriers for smaller manufacturers. Additionally, hydrogen storage and transport infrastructure remains underdeveloped, with pipeline coverage below 5% of natural gas networks globally. Limited availability of critical materials such as iridium and platinum further constrains production scalability, while permitting delays extend project timelines by 12–18 months in several regions.

Power-to-X applications enable hydrogen conversion into ammonia, methanol, and synthetic fuels, opening export markets for renewable-rich regions. Over 45 large-scale hydrogen export projects are under development globally, with combined output potential exceeding 20 million tons annually. Manufacturing opportunities extend to specialized electrolyzers, liquefaction systems, and port-integrated hydrogen hubs. Countries targeting hydrogen exports are offering long-term offtake contracts, improving demand certainty for equipment manufacturers.

Lack of harmonized standards for electrolyzer safety, efficiency testing, and interoperability increases customization costs by up to 18%. Skilled labor shortages in electrochemistry, automation, and hydrogen safety slow factory ramp-ups, with training gaps affecting nearly 25% of planned manufacturing expansions. Additionally, rapid technology evolution creates asset obsolescence risks, complicating long-term capital planning.

• Modular Electrolyzer Gigafactories: Over 48% of new manufacturing facilities adopt modular layouts, reducing setup time by 34% and enabling phased capacity expansion beyond 1 GW per site.

• Automation and Digital Twins: Automated stack assembly improves output consistency by 29%, while digital twins cut commissioning errors by 21% across large-scale plants.

• Advanced Materials Innovation: Catalyst loading reductions of 35% are achieved through nanostructured membranes, extending electrolyzer lifespan beyond 90,000 operating hours.

• Integration with Renewables: Co-located hydrogen manufacturing with solar and wind assets improves utilization rates by 26% and stabilizes production economics.

The Advanced Hydrogen Technology Manufacturing Market is segmented by type, application, and end-user, reflecting diverse deployment requirements. Product segmentation highlights electrolyzer technologies and storage systems, while application segmentation spans industrial processing, energy storage, and mobility. End-user insights reveal strong demand from heavy industry and utilities, with emerging adoption among transport operators and synthetic fuel producers. Segmentation trends indicate increasing preference for flexible, modular manufacturing systems aligned with regional energy strategies.

Alkaline electrolyzers lead with approximately 44% adoption due to mature supply chains and cost efficiency, while PEM electrolyzers account for 32% driven by rapid response capability. Solid oxide electrolyzers represent the fastest-growing segment with a projected CAGR of 28.6%, supported by high-temperature efficiency gains exceeding 20%. Other technologies, including anion exchange membranes and hybrid systems, collectively contribute around 24% and serve niche industrial applications.

Industrial feedstock applications dominate with a 46% share, driven by steel, ammonia, and refining demand. Energy storage and grid balancing applications hold 29%, while mobility-related uses are the fastest-growing segment with a CAGR of 31.2%, supported by hydrogen trucking and rail pilots. Remaining applications contribute 25%. In 2024, over 41% of industrial enterprises piloted hydrogen systems for process heat substitution, and 37% of logistics operators tested hydrogen-powered fleets.

Heavy industry leads end-user adoption with a 52% share, followed by utilities at 21%. Transport operators represent the fastest-growing end-user group with a CAGR of 33.4%, driven by fuel cell vehicle infrastructure expansion. Other end-users, including power-to-X producers and export terminals, contribute 27%. In 2024, 39% of large enterprises reported active hydrogen manufacturing pilots, while 44% of utilities integrated hydrogen for grid flexibility.

Asia Pacific accounted for the largest market share at 41.6% in 2024 however, Europe is expected to register the fastest growth, expanding at a CAGR of 27.9% between 2025 and 2032.

Asia Pacific benefits from over 65 GW of announced electrolyzer manufacturing capacity, with China, Japan, and South Korea collectively contributing more than 58% of global hydrogen equipment output. Europe, driven by large-scale green hydrogen corridors and cross-border infrastructure projects, has committed over 120 industrial hydrogen manufacturing projects exceeding 18 million tons of planned annual output. North America follows with 24.3% share, supported by hydrogen hub funding and industrial retrofitting programs. The Middle East & Africa region is emerging with over 9 million tons of planned export-oriented hydrogen capacity, while South America contributes 6.8%, led by renewable-rich hydrogen production zones and ammonia export initiatives.

How is large-scale industrial decarbonization accelerating equipment demand?

This region accounts for approximately 24.3% of the Advanced Hydrogen Technology Manufacturing Market, driven by demand from refining, chemicals, steel, and heavy transportation. More than 60% of regional hydrogen projects are tied to industrial fuel switching and grid-scale energy storage. Federal incentives supporting clean hydrogen production have unlocked over USD 8 billion in manufacturing-linked funding, accelerating electrolyzer factory expansions. Digital manufacturing, AI-enabled quality control, and robotic stack assembly have improved output consistency by nearly 26%. Local players are expanding gigawatt-scale electrolyzer plants to support hydrogen hubs. Regional adoption patterns show higher enterprise uptake across energy utilities and logistics operators, with over 44% of large industrial firms actively piloting hydrogen-based systems.

Can regulatory alignment transform hydrogen manufacturing into an industrial backbone?

Europe holds nearly 27.1% of global market demand, with Germany, the UK, and France accounting for over 62% of regional deployments. EU-wide hydrogen strategies and carbon pricing frameworks have increased industrial hydrogen adoption by 39% since 2022. Advanced technologies such as solid oxide electrolyzers and digital twins are increasingly adopted, with over 48% of new manufacturing projects integrating predictive analytics for lifecycle optimization. Regional players are investing in vertically integrated electrolyzer-to-storage production lines. Consumer and enterprise behavior reflects strong regulatory influence, with over 57% of industrial buyers prioritizing traceable, certifiable low-carbon hydrogen equipment.

Why is manufacturing scale becoming the region’s defining advantage?

Asia-Pacific ranks first globally in production volume, supplying more than 52% of total hydrogen manufacturing equipment output. China, Japan, and India lead consumption, with China alone operating over 300 hydrogen industrial clusters. Manufacturing trends emphasize cost-optimized alkaline electrolyzers and automated assembly lines producing over 5,000 stacks annually per facility. Innovation hubs in Shanghai, Osaka, and Bengaluru focus on membrane efficiency and catalyst reduction. Local manufacturers are scaling modular electrolyzer platforms for export markets. Regional behavior is driven by infrastructure-led demand, with over 46% of deployments linked to industrial parks and logistics corridors.

How are renewable resources reshaping regional production priorities?

South America accounts for approximately 6.8% of global demand, led by Brazil, Chile, and Argentina. Over 70% of hydrogen manufacturing projects are integrated with solar and wind assets exceeding 25 GW in capacity. Government-backed incentives and export-oriented trade policies are accelerating ammonia and synthetic fuel manufacturing. Regional players are focusing on cost-efficient electrolyzer assembly and port-based hydrogen hubs. Adoption patterns show demand closely tied to export logistics and industrial localization, with more than 38% of projects targeting cross-border hydrogen supply agreements.

Is export-led hydrogen manufacturing redefining industrial strategy?

This region represents around 7.4% of global demand, with the UAE, Saudi Arabia, and South Africa leading deployments. Hydrogen manufacturing is closely linked to oil & gas diversification and large-scale export infrastructure. Over 60% of regional projects exceed 500 MW capacity, emphasizing advanced compression and liquefaction technologies. Modernization efforts include automated electrolyzer assembly and digital asset monitoring. Local players are forming trade partnerships to secure long-term offtake contracts. Consumer behavior is driven by industrial-scale procurement, with centralized buyers accounting for nearly 72% of equipment demand.

China: 28.9% share — supported by gigawatt-scale electrolyzer production capacity and integrated industrial hydrogen adoption.

Germany: 15.7% share — driven by strong regulatory frameworks and high deployment of green hydrogen manufacturing systems.

The Advanced Hydrogen Technology Manufacturing Market is moderately consolidated, with over 90 active global manufacturers spanning electrolyzers, storage systems, and integrated hydrogen solutions. The top five companies collectively account for approximately 46% of total market activity, reflecting strong technological differentiation and capital intensity. Competitive strategies emphasize capacity expansion, vertical integration, and partnerships with renewable developers. More than 35 strategic collaborations were announced between 2023 and 2024 to accelerate hydrogen hub deployments. Innovation is focused on reducing catalyst dependency, improving system durability beyond 90,000 operating hours, and standardizing modular designs. Smaller players compete through niche technologies such as solid oxide systems and portable hydrogen units, while large manufacturers dominate industrial-scale installations.

ITM Power

Plug Power

Thyssenkrupp Nucera

Cummins Inc.

McPhy Energy

Bloom Energy

Toshiba Energy Systems

Linde plc

John Cockerill Hydrogen

Sunfire GmbH

Ballard Power Systems

Advanced Hydrogen Technology Manufacturing is being transformed by innovations across electrolyzer design, materials science, and digital production systems. Solid oxide electrolyzers operate at temperatures above 700°C, enabling electrical efficiency improvements of up to 20% compared to low-temperature systems. PEM electrolyzers increasingly integrate advanced membranes that reduce precious metal usage by nearly 35%. Automation and robotics now handle over 55% of stack assembly processes, reducing defect rates by 22%. Digital twins and AI-based predictive maintenance systems are deployed across 48% of new manufacturing facilities, improving uptime and asset utilization. High-pressure composite storage vessels capable of 700 bar operation are extending transport efficiency by 18%. Integrated manufacturing lines combining electrolyzers, compressors, and power electronics are shortening commissioning timelines by over 30%. These technological shifts are enabling scalable, export-ready hydrogen manufacturing ecosystems.

• In July 2024, Siemens Energy expanded its electrolyzer manufacturing facility in Berlin, increasing annual production capacity to 3 GW to support large-scale industrial hydrogen projects. Source: www.siemens-energy.com

• In May 2024, NEL ASA commissioned a fully automated electrolyzer production line capable of producing one 500 MW system every 90 days, improving throughput efficiency by 25%. Source: www.nelhydrogen.com

• In October 2023, ITM Power launched a next-generation PEM electrolyzer platform with 20% higher current density, enabling more compact industrial installations. Source: www.itm-power.com

• In August 2023, Plug Power deployed an integrated hydrogen liquefaction system at a U.S. manufacturing hub, increasing on-site hydrogen availability by 40%. Source: www.plugpower.com

The Advanced Hydrogen Technology Manufacturing Market Report comprehensively evaluates the global landscape of hydrogen equipment production, covering electrolyzers, storage systems, compression technologies, and integrated hydrogen solutions. The scope includes detailed segmentation by technology type, application areas such as industrial feedstock, energy storage, mobility, and export-oriented production, as well as end-user industries including steel, chemicals, utilities, and transportation. Geographic coverage spans North America, Europe, Asia Pacific, South America, and the Middle East & Africa, capturing regional manufacturing capacities, deployment patterns, and infrastructure readiness. The report examines technological advancements such as solid oxide systems, AI-enabled manufacturing, modular gigafactories, and advanced materials. It also addresses policy frameworks, industrial adoption metrics, and emerging niches like power-to-X and hydrogen exports. Designed for strategic planners and decision-makers, the report provides a structured understanding of market breadth, competitive positioning, and future-ready manufacturing pathways without redundancy.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 13,926.8 Million |

|

Market Revenue in 2032 |

USD 83,542.9 Million |

|

CAGR (2025 - 2032) |

25.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens Energy, NEL ASA, Air Liquide, ITM Power, Plug Power, Thyssenkrupp Nucera, Cummins Inc., McPhy Energy, Bloom Energy, Toshiba Energy Systems, Linde plc, John Cockerill Hydrogen, Sunfire GmbH, Ballard Power Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |