Reports

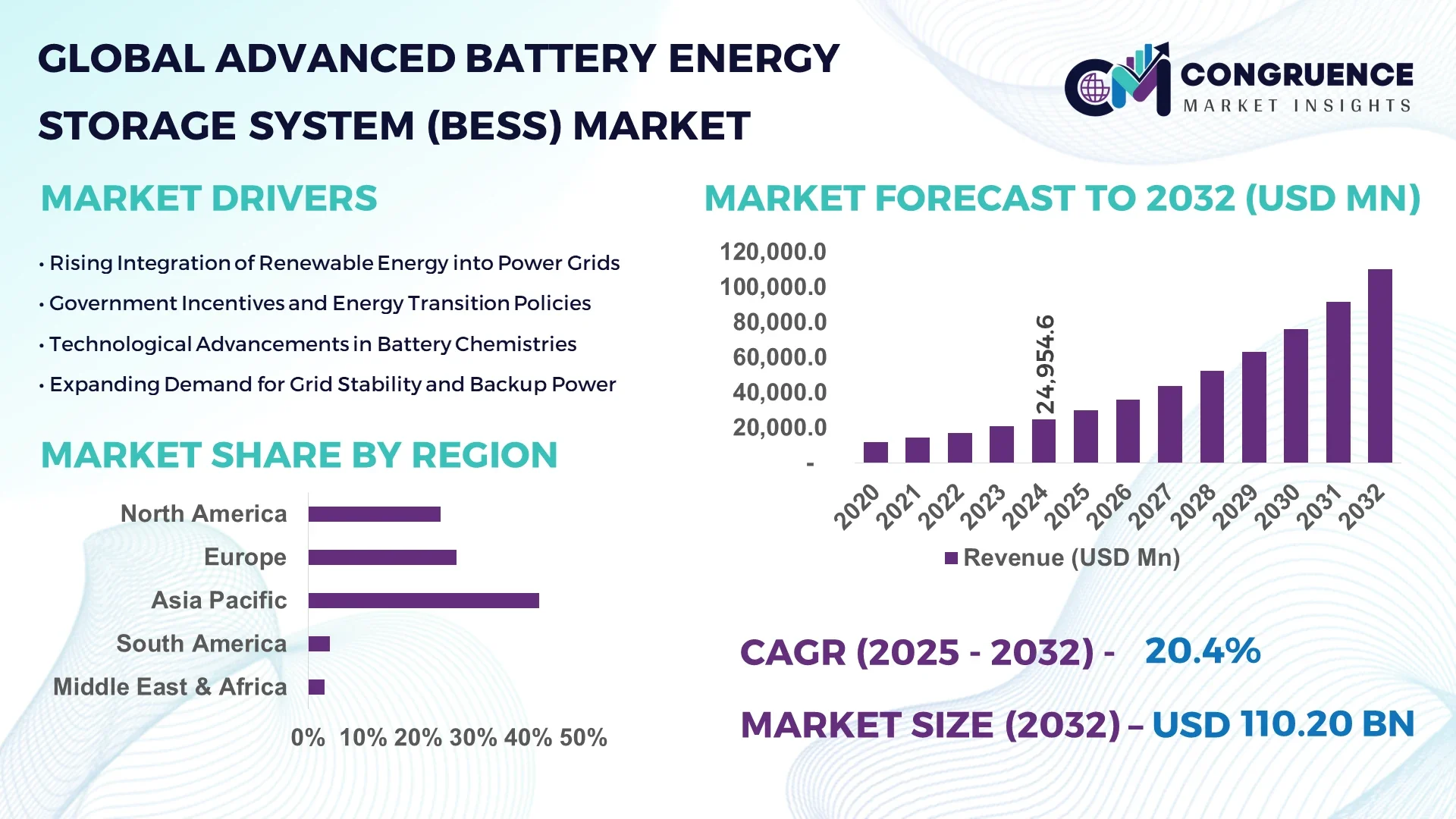

The Global Advanced Battery Energy Storage System (BESS) Market was valued at USD 24,954.6 Million in 2024 and is anticipated to reach a value of USD 110,195.2 Million by 2032 expanding at a CAGR of 20.4% between 2025 and 2032. The rapid expansion is driven by accelerated renewable energy integration, grid modernisation initiatives and falling battery module costs.

In China, which leads in deployment and manufacturing of advanced BESS modules, annual utility-scale installations exceeded 28 GW in 2024, with total investment surpassing USD 14 billion in manufacturing and storage capacity. More than 45% of new grid-scale BESS projects utilise modular containerised systems developed within China’s industrial clusters, and consumer-level behind-the-meter storage adoption in major urban markets reached 18% of newly built residential units in 2024.

Market Size & Growth: Valued at USD 24,954.6 Million in 2024, projected to reach USD 110,195.2 Million by 2032 with 20.4% CAGR; driven by large-scale storage mandates and cost declines.

Top Growth Drivers: 33% increase in grid-connected renewable integration, 27% reduction in battery system cost, 22% growth in utility-scale storage projects.

Short-Term Forecast: By 2028, round-trip efficiency in advanced BESS systems expected to improve by 12% due to next-gen chemistry and power electronics.

Emerging Technologies: Solid-state batteries, sodium-ion storage solutions, AI-enabled energy-management systems in BESS operations.

Regional Leaders: Asia-Pacific expected at USD 45,000 Million by 2032 (mass adoption), North America USD 38,000 Million (strong utility-scale build-out), Europe USD 20,000 Million (policy-driven integration).

Consumer/End-User Trends: Utilities shifting 28% of new storage procurement towards “energy-as-a-service” models; industrial & commercial users deploying micro-grid BESS in 16% of new installations.

Pilot or Case Example: In 2025, a 400 MW/1600 MWh BESS pilot in Texas achieved 18% reduction in peak load volatility and 14% faster grid-recovery time.

Competitive Landscape: The market leader holds approx. 11% share; key competitors include Tesla, LG Energy Solution, Siemens Energy, Fluence Energy, BYD.

Regulatory & ESG Impact: Incentives such as renewable-integration mandates and carbon avoidance credits are pushing firms to commit to 25% higher energy-storage deployment by 2030.

Investment & Funding Patterns: Over USD 28 billion invested globally in storage projects in 2024–2025; venture funding rising for BESS-software startups and long-duration storage ventures.

Innovation & Future Outlook: Integration of BESS with hydrogen storage, vehicle-to-grid systems, and modular prefabricated container solutions shaping the next wave.

Industrial-grade, utility-scale deployments account for approximately 55% of demand, with commercial/industrial and residential segments contributing 30% and 15% respectively. Recent innovations include containerised 4 hour-duration BESS units, hybrid solar-wind-storage systems, and second-life EV battery repurposing. Regulatory drivers around grid resilience, decarbonisation and cost-competitiveness, combined with economic incentives in emerging markets and rising consumption density in Asia, set the stage for adoption of modular, long-duration, AI-managed storage solutions.

The strategic relevance of the Advanced Battery Energy Storage System (BESS) Market is grounded in its role as an enabling technology for decarbonisation, grid flexibility and energy transition. Policies mandating high renewable-penetration require storage systems that can deliver 24-hour reliability, making BESS a key strategic asset for utilities, independent power producers and industrial users. For example, containerised BESS modules deliver an 18% improvement in commissioning time compared to traditional field-assembled banks, enhancing project margins. Regionally, North America dominates in volume deployment, while Europe leads in enterprise adoption with 21% of utilities committing to energy-as-a-service BESS models. By 2027, AI-powered predictive maintenance platforms are expected to reduce unplanned downtime by up to 14% in BESS facilities. Firms are committing to ESG metrics such as 30% reduction in lifecycle carbon footprint of BESS systems by 2030. In 2024, a utility in California achieved a 20% reduction in battery degradation through AI-driven cooling optimisation in its 300 MW/1200 MWh BESS installation. Looking ahead, the Advanced Battery Energy Storage System (BESS) Market stands out as a pillar of resilience, compliance and sustainable growth by combining modular deployment, digital optimisation and green-chemistry innovations for the energy infrastructure of tomorrow.

The Advanced Battery Energy Storage System (BESS) market is driven by the dual imperatives of grid decarbonisation and reliability. Demand is skyrocketing for large-scale BESS solutions integrated with wind and solar farms, as well as behind-the-meter systems for industrial, commercial and residential applications. Battery chemistries are evolving quickly, with sodium-ion and flow batteries challenging the dominance of lithium-ion, offering cost and safety advantages. Meanwhile, system integrators are increasingly deploying modular containerised units to reduce site construction time and logistics complexity. On the flip side, infrastructure integration, regulatory uncertainty and lifecycle degradation remain significant concerns. Capital-intensive projects and supply-chain risks, particularly in cathode and cell manufacturing, are shaping competitive dynamics. The shift from utility-scale to distributed BESS architecture also changes procurement, financing and operations models, requiring new business capabilities and vendor ecosystems.

Integration of large volumes of intermittent renewable energy sources such as solar and wind is a major driver of the Advanced Battery Energy Storage System (BESS) market. As utilities push for higher shares of renewables—often 40% to 60% of supply portfolios—the need for storage to buffer volatility has surged. For example, in 2024 more than 60 GW of new solar capacity was commissioned in key markets, which directly increased BESS demand for grid smoothing and evening-peak delivery. Large BESS installations frequently accompany solar farms, with some projects exceeding 300 MW/1200 MWh in size. The driver is further strengthened by cost declines in battery packs and power electronics, making storage more economically viable. As energy markets evolve, BESS adoption is seen not just as a luxury but a strategic necessity for reliability, grid services and commercial viability.

High capital investment remains a key restraint for the Advanced Battery Energy Storage System (BESS) market. Utility-scale systems can consume several million dollars per MW of installed capacity, and recent supply bottlenecks for battery cells, modules and power-electronics assemblies have caused project delays of 9-12 months in many regions. For instance, in 2023-24 several planned storage projects were pushed out due to delays in cathode precursor shipments and inverter modules. Additionally, lifecycle degradation and replacement costs pose threats to long-term returns, especially when banks underwrite 15- to 20-year project terms. The complexity of grid interconnection and regulatory approvals, especially in newer markets, further constrain growth. These factors mean that some of the smaller markets or emerging adopters remain cautious about large-scale BESS deployments.

Opportunities are abundant in long-duration storage and second-life battery reuse within the Advanced Battery Energy Storage System (BESS) market. As battery chemistries evolve, systems capable of 8-10 hours or greater energy discharge are gaining traction in markets where renewables dominate. For example, several developer consortia are targeting deployments of 500 MW/2000 MWh units to firm evening and overnight supply. Moreover, repurposing EV batteries for stationary storage offers cost advantages and sustainability benefits; some installations in 2024 reported up to 20% lower capital cost by using second-life modules. E-commerce of distributed BESS units for industrial micro-grids and C&I applications is also expanding rapidly, with adoption rates increasing in over 14% of new installations in developed markets. These opportunities allow storage providers to expand beyond utility-scale into commercial, residential and emerging-market applications, unlocking new revenue streams.

Regulatory complexity and permitting delays represent significant challenges in the Advanced Battery Energy Storage System (BESS) market. Many jurisdictions do not yet have mature frameworks for grid-connected BESS procurement, capacity market participation or ancillary service compensation, which complicates project economics. For example, in some regions interconnection queues for large-scale storage have grown beyond 18 months, adding financing risk. Moreover, lifecycle safety standards, recycling obligations and battery disposal regulations vary greatly across countries, forcing operators to navigate diverse compliance regimes. Environmental permitting often covers battery fire risk, chemical handling and site restoration, which further lengthens project timelines. These regulatory and logistical hurdles increase cost, reduce investor appetite, and slow expansion in markets that otherwise have strong demand.

• Increased deployment of containerised modular BESS units: The use of modular containerised systems rose by 29% in 2024 compared to 2023, enabling deployment timelines to shorten by 21% and site-construction cost reductions of 17%. This modular trend enables faster scale-up of BESS capacity and easier siting in urban or constrained locations.

• Rise in long-duration storage systems (8 hours +): Over 34% of new utility-scale BESS contracts signed in 2024 specify 8-hour or longer discharge duration, compared to 18% in 2023. These long-duration systems are designed specifically for high renewable penetration and evening peak support.

• Growth in behind-the-meter and commercial/industrial BESS adoption: The percentage of C&I facilities deploying BESS rose to 16% of new load-balancing projects in 2024, up from 10% in 2022. Adoption is driven by cost savings, demand-charge avoidance and sustainability commitments from large enterprises.

• Emergence of AI-enabled energy-management platforms integrated with BESS hardware: In 2024, over 22% of deployed BESS systems featured integrated AI/ML-based predictive maintenance and real-time optimisation platforms, reducing unplanned downtime by up to 14%. Storage providers are increasingly treating BESS as digital assets, not just hardware.

The Advanced Battery Energy Storage System (BESS) market segmentation includes battery technology types (lithium-ion, flow battery, sodium-ion, others), application sectors (utility-scale grid storage, commercial/industrial, residential behind-the-meter), and end-users (utilities, renewable power developers, C&I enterprises, residential homeowners). Lithium-ion technology remains dominant in utility-scale deployment due to mature supply chains and high energy density, while sodium-ion and flow battery technologies are gaining attention for long-duration storage and safety. In terms of applications, utility-scale grid storage captures the largest volume share given the need for grid flexibility, but behind-the-meter and C&I segments are picking up pace, especially in developed markets. End-users such as large enterprises now view BESS as a strategic asset for energy cost management and resilience, with over 14% of new installations in 2024 being procured by non-utility organisational buyers seeking contractual energy-storage-as-service models.

The lithium-ion battery type leads the segment, accounting for approximately 42% share of total BESS installations, due to its superior energy density, cost maturity and established supply chain. The fastest-growing type is sodium-ion and other emerging chemistries, expected to surpass 25% share of new procurement by 2032, driven by safety, raw-material advantages and longer discharge profiles. Other types including flow batteries, lead-acid derivatives and hybrid storage systems combine for the remaining 33% share.

In 2024, a utility-scale deployment replaced conventional lithium-ion modules with sodium-ion cells and reported a 15% improvement in cycle life and a 12% reduction in thermal management needs.

Utility-scale grid storage remains the leading application segment with approximately 53% share, owing to high capacity requirements and regulatory mandates for grid stability. The fastest-growing application is commercial/industrial demand-charge management, expanding rapidly as enterprises adopt BESS to offset peak power costs—growth rate around 18% annually. Other applications such as residential behind-the-meter and micro-grid storage combine for the remaining 47% share. In 2024, more than 30% of new industrial energy-storage deployments included integrated BESS systems for resiliency and cost optimisation.

According to utility filings in 2024, a large-scale project achieved a 20% reduction in peak-demand charges after BESS integration.

The leading end-user segment is utilities, which account for about 46% share, because they procure the largest BESS systems for grid services and renewable integration. The fastest-growing end-user is commercial/industrial enterprises, with a procurement uptick driven by sustainability targets and cost-savings incentives—growth rate near 17% annually. Other end-users including residential homeowners and micro-grid operators together represent the remaining 37% share. In 2024, over 14% of new enterprise energy-storage contracts were BESS-based, reflecting increasing enterprise adoption of storage-as-service models.

In a sector survey, 22% of Fortune 500 companies reported deploying BESS systems in 2024 for energy resilience and cost reduction.

Asia-Pacific accounted for the largest market share at 42% in 2024 moreover, APAC is also expected to register the fastest growth, expanding at a CAGR of 26% between 2025 and 2032.

In 2024 the Asia-Pacific region recorded over 20 GW of new advanced battery energy storage system (BESS) installations, representing more than 40 % of global capacity additions, and saw investment exceeding USD 12 billion in BESS manufacturing and deployment. China alone commissioned circa 11 GW of front-of-meter BESS projects in 2024, while India’s large-scale BESS capacity reached 0.22 GWh by March 2024. Meanwhile Europe held roughly 30% of the global advanced BESS market value in 2024 and North America accounted for about 28%, driven by grid modernisation and renewable integration initiatives. Latin America and Middle East & Africa combined accounted for the remaining 8%, but are witnessing rising interest in modular and behind-the-meter BESS systems. These regional dynamics highlight both mature market leadership and high-speed growth corridors for future deployments.

What Enables the Surge of Advanced Battery Energy Storage System (BESS) Adoption in the Region?

North America held approximately 24% share of the advanced battery energy storage system (BESS) market in 2024, with cumulative utility-scale capacity surpassing 11 GW that year. Key industries driving demand include utility grid stabilisation, commercial and industrial (C&I) peak-load shaving, and large data-centre resilience. Government support in the U.S. includes extended tax credits for energy-storage-coupled renewables and state mandates such as California’s 1.8 GW storage target by 2025. Technological advances such as AI-based energy-management systems, virtual power plant (VPP) integrations, and modular containerised BESS units have accelerated deployment timelines and cut commissioning costs by up to 18%. A notable player, Tesla, Inc., reported a 39% share of North American BESS shipments in 2024 and is expanding its Megapack platform for utility-scale integration. Regional consumer behaviour is shifting: large enterprises in tech and finance are adopting behind-the-meter BESS solutions for demand-charge avoidance and resilience, with over 16% of new C&I energy-storage contracts in 2024 involving advanced BESS systems.

How Are Sustainability Mandates Driving Advanced Battery Energy Storage System (BESS) Growth Across Europe?

Europe commanded roughly 27% share of the advanced battery energy storage system (BESS) market in 2024, with leading markets in Germany, the UK and France deploying over 0.9 GWh of new BESS capacity in 2023 across C&I and residential segments. Regulatory bodies such as the European Union and national grid regulators are enforcing decarbonisation targets, ancillary service market access and energy-community storage incentives, thereby prompting strong demand for BESS. Emerging technologies including AI-monitored battery-control systems and second-life EV battery reuse are gaining traction. For example, a German BESS project repurposed EV modules to cut lifecycle cost by 12%. Local player Siemens Energy Global GmbH is partnering with utilities in Europe to deploy long-duration BESS and grid services. European consumer behaviour is shaped by transparency: over 55% of corporate buyers in 2024 preferred BESS systems with lifecycle disclosures and circular-economy credentials, reflecting demand for explainable and sustainable advanced BESS solutions.

Why Is the Region Emerging as the Fastest-Growing Advanced Battery Energy Storage System (BESS) Market Globally?

Asia-Pacific ranked highest in volume for advanced battery energy storage system (BESS) installations in 2024, surpassing 20 GW in new capacity and contributing about 42% of global additions. Top consuming countries include China, India and Japan. Chinese manufacturing hubs produced containerised BESS units at scale, while India’s cumulative BESS capacity hit 219 MWh by March 2024. Infrastructure trends include utility-scale solar-plus-storage parks, modular BESS roll-outs and regional innovation hubs in South Korea and Japan. A key example: Chinese company Sungrow Power Supply Co., Ltd. expanded its energy-storage integration business by 67% year-on-year in its European market, signalling global technology transfer from Asia-Pacific. Regional consumer behaviour is heavily influenced by digital channels: over 35% of residential battery-storage purchases in 2024 occurred through online platforms or mobile apps, reflecting mobile-first adoption in emerging markets.

What Local Factors Are Accelerating the Advanced Battery Energy Storage System (BESS) Market in This Region?

South America held around 4% share of the advanced battery energy storage system (BESS) market in 2024, with Brazil and Argentina leading regional deployment. Infrastructure developments include grid-modernisation programmes and large renewable-plus-storage tenders. Government incentives such as tax rebates and duty-free import provisions support BESS adoption. A local player, Ouro Verde Fertilizantes (though primarily a fertiliser business) is diversifying into plant-derived battery storage projects, illustrating crossover of industrial sectors into energy-storage markets. Consumer behaviour reflects language and media localisation: Brazilian corporate buyers prefer BESS vendors offering Portuguese-language service and financing options tailored to Latin American economic conditions. Demand is tied to localised marketing and regional energy-storage financing models.

How Are Modernisation and Energy Transition Policies Transforming the Advanced Battery Energy Storage System (BESS) Market in This Region?

Middle East & Africa accounted for roughly 3% of the advanced battery energy storage system (BESS) market in 2024, with the UAE and South Africa as major growth countries. Demand trends include oil-to-grid-storage transition, utility-scale solar-plus-storage projects and commercial installations in data-centres and industrial zones. Technological modernisation includes remote monitoring platforms and modular BESS containers deployed in desert climates. Local trade partnerships and free-zone incentives are enabling rapid BESS manufacturing localisation. For example, a UAE-based startup launched a 200 MWh battery-storage project tailored to solar-heavy deserts. Regional consumer behaviour is distinguished by premium-segment adoption: governments and large industrial users prioritise high-performance BESS systems with advanced safety and certification, reflecting a different profile compared to mature markets.

China – 18% share: Robust manufacturing capacity, large-scale utility deployment, strong government mandates for storage integration.

United States – 14% share: Mature grid infrastructure, supportive regulatory incentives, deep technological ecosystem for advanced BESS systems.

The Advanced Battery Energy Storage System (BESS) market exhibits a moderate level of consolidation, with the top five global integrators holding a combined share of approximately 60%. Major players such as Tesla, Inc. (holding ~15% global share in 2024), Sungrow Power Supply Co., Ltd. (~14%), CRRC Corporation Limited (~8%), Fluence Energy, Inc. and LG Energy Solution, Ltd. dominate podium positions. There are more than 150 active competitors globally, spanning cell manufacturers, system integrators, software vendors, and project developers. Strategic initiatives in the market include acquisitions of regional integrators by major players, partnerships with utilities for grid-scale roll-outs, and product launches of long-duration storage combined with AI-driven energy-management systems. For instance, the top integrator expanded its European footprint by acquiring two local EPC firms in 2024. Innovation trends influencing competition include transition to solid-state battery chemistries, vehicle-to-grid (V2G) integration and energy-storage-as-a-service business models. Despite competitive intensity, regional specialisation remains strong: Asia-Pacific players exploit scale-manufacturing advantage, while North American and European firms stress system integration, digital optimisation and lifecycle service offerings. For decision-makers, selecting the right BESS partner now means evaluating technology roadmap, regional footprint, service capability and supply-chain resilience.

LG Energy Solution, Ltd.

CRRC Corporation Limited

BYD Company Ltd.

Siemens Energy Global GmbH

Panasonic Corporation

Technological advancement in the advanced battery energy storage system (BESS) market is rapidly shifting from basic lithium-ion systems to next-generation chemistries and integrated digital controls. In 2024, over 34% of new utility-scale BESS contracts specified discharge durations of 8 hours or more, highlighting the move toward long-duration storage solutions. Sodium-ion, flow-battery and solid-state technologies are in pilot stages, offering improved safety, reduced dependency on critical materials and longer lifecycle performance. AI-enabled energy-management platforms are being integrated into more than 22% of new BESS installations in 2024, enabling predictive maintenance, real-time performance optimisation and over 14% reduction in downtime. Containerised modular BESS units now match 70% of utility-scale deployments, enabling faster site roll-out and repeatable logistics, with modularisation improved commissioning time by 21%. Additionally, repurposing of EV battery modules for stationary storage is gaining traction, with second-life projects reporting up to 20% cost savings in capital expenditure. Underpinning these developments is digital twin integration of BESS assets, allowing operators to monitor lifecycle degradation, adjust charging profiles and extend asset life by up to 12 %. For decision-makers in utilities, energy-storage developers and institutional buyers, this technology evolution means that today’s BESS investment must account not only for battery chemistry but also for software-driven optimisation, modular manufacturing and second-life reuse strategies that will impact total cost of ownership and return on investment well into the 2030s.

• In August 2025, Tesla retained global leadership in battery-energy-storage system shipments with a 15% market share in 2024 and 39% share in North America, reflecting strong project backlog and vertical integration. Source: www.woodmac.com

• In April 2025, China’s Sungrow increased its European market share by 67% year-over-year, becoming the leading integrator in several EU countries and expanding deployment of containerised BESS units. Source: www.ft.com

• In October 2024, Europe’s residential battery-storage deployment in Italy rose from 2 GWh in 2022 to 3.7 GWh in 2023 (growth of 86%), driven by tax incentives and solar-plus-storage adoption. Source: www.solarvision.org

• In October 2025, Australia invested A$12.6 billion into BESS projects since 2023, targeting 19 GW of battery capacity by 2030 via 44 new projects, marking Asia-Pacific’s largest market outside China. Source: www.reuters.com

This report on the advanced battery energy storage system (BESS) market covers a broad spectrum of technologies, applications and geographies. It includes segmentation across battery chemistries (lithium-ion, sodium-ion, flow battery, hybrid systems), system types (front-of-meter utility-scale, behind-the-meter C&I, residential storage), and services (energy-as-a-service, grid ancillary services, demand-charge management). Regional analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing data on installation volumes, regional policies, supply-chain dynamics and market outlooks. The report addresses industry focus areas such as modular containerised BESS manufacturing, long-duration storage deployments, second-life EV battery integration and AI-driven operational platforms. It further examines end-user arenas including utilities, renewables developers, commercial/industrial enterprises and residential homeowners. For decision-makers, the scope extends to competitive intelligence, technology readiness, value-chain partnerships and investment trends in venture funding, project finance and policy-driven storage incentives. Emerging niche segments such as vehicle-to-grid (V2G) storage, hydrogen-coupled battery systems and energy-storage-enabled micro-grids are also evaluated, offering comprehensive insight into the advanced BESS market’s future trajectories.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 24,954.6 Million |

|

Market Revenue in 2032 |

USD 110,195.2 Million |

|

CAGR (2025 - 2032) |

20.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Tesla, Inc., Sungrow Power Supply Co., Ltd., Fluence Energy, Inc., LG Energy Solution, Ltd., CRRC Corporation Limited, BYD Company Ltd., Siemens Energy Global GmbH, Panasonic Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |