Reports

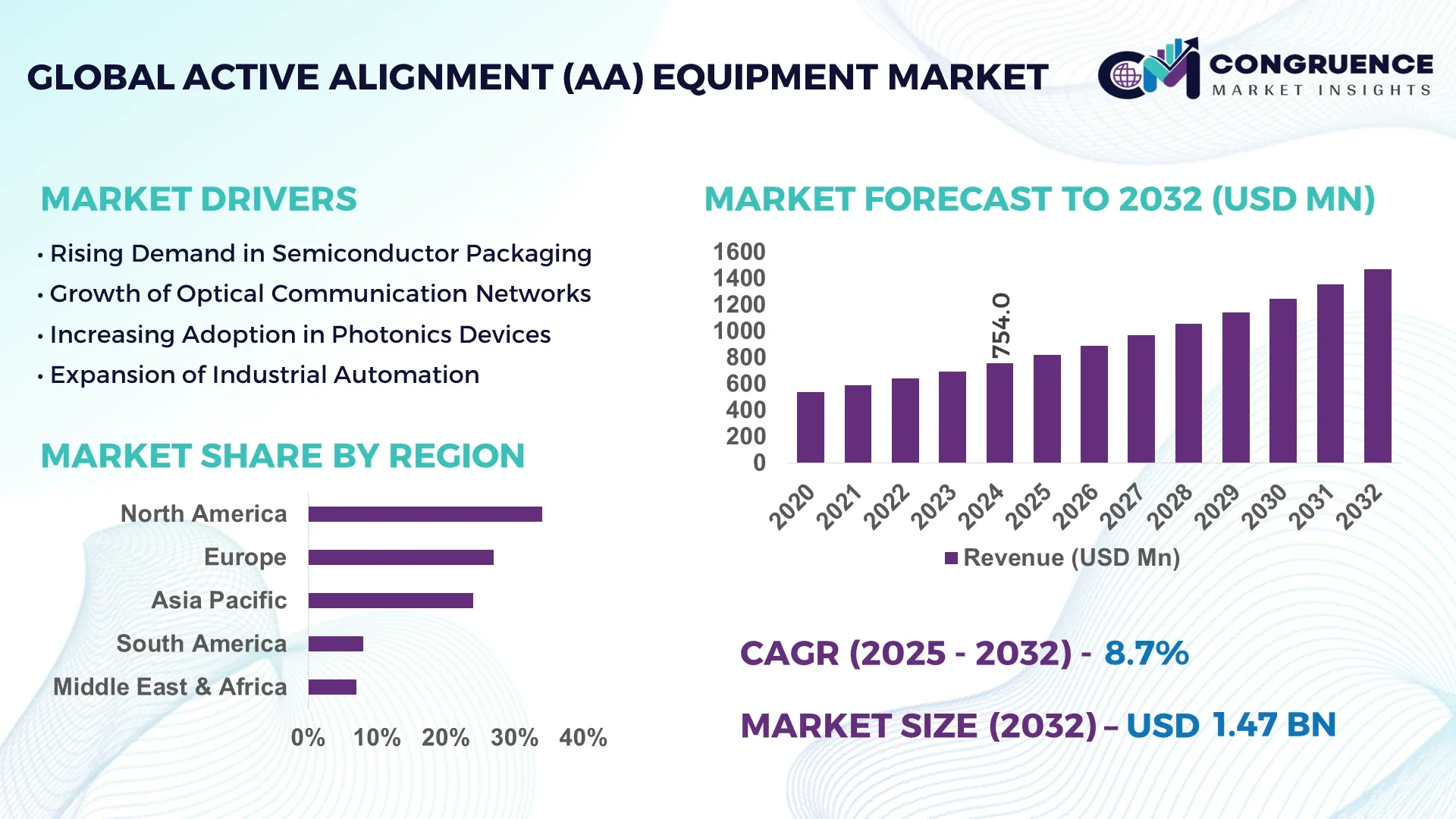

The Global Active Alignment (AA) Equipment Market was valued at USD 754 Million in 2024 and is anticipated to reach a value of USD 1,469.6 Million by 2032 expanding at a CAGR of 8.7% between 2025 and 2032.

The United States dominates the Active Alignment (AA) Equipment Market, leveraging high production capacity, substantial investment in precision optics and semiconductor manufacturing, and advanced research facilities. Key industry applications include optical communications, semiconductor packaging, and photonics, supported by continuous technological advancements in automation, machine vision systems, and high-speed alignment processes. Leading equipment manufacturers have focused on integrating AI-assisted calibration and robotic handling to enhance throughput and reduce defect rates.

The Active Alignment (AA) Equipment Market is witnessing significant adoption across semiconductor, telecommunication, and photonics sectors. The semiconductor industry accounts for the largest portion of demand due to the need for precise optical alignment in chip packaging and wafer-level testing. Technological innovations such as high-speed vision systems, automated robotic arms, and real-time feedback loops are enhancing equipment precision and reducing cycle times. Regulatory and environmental standards, including cleanroom and energy-efficiency requirements, are driving manufacturers to adopt eco-friendly production processes. Regional consumption patterns show high growth in North America and Asia-Pacific due to advanced manufacturing hubs, while emerging trends include miniaturization of devices and integration of AI and IoT technologies to optimize alignment accuracy and operational efficiency.

Artificial Intelligence (AI) is reshaping the Active Alignment (AA) Equipment Market by enhancing operational precision, optimizing workflow efficiency, and reducing human intervention in critical alignment processes. AI-driven vision systems allow real-time defect detection and adaptive calibration, ensuring higher throughput while minimizing alignment errors in semiconductor and photonics production lines. Machine learning algorithms are increasingly employed to analyze historical performance data, predict system drift, and automatically adjust alignment parameters, which significantly improves process stability and reduces equipment downtime.

AI also contributes to predictive maintenance within the Active Alignment (AA) Equipment Market, enabling manufacturers to schedule service intervals based on real-time machine condition monitoring. Robotics integrated with AI-powered control systems enhance the repeatability and accuracy of optical and microelectronic component positioning, essential for high-volume production. The adoption of AI further supports digital twin implementations, allowing simulation of alignment operations to identify potential bottlenecks and optimize equipment utilization. Collectively, AI integration improves production efficiency, reduces operational costs, and enables scalable high-precision manufacturing, positioning the Active Alignment (AA) Equipment Market for accelerated technological advancement.

"In March 2024, a leading semiconductor equipment manufacturer implemented an AI-based active alignment system capable of reducing optical fiber coupling errors by 35% while increasing throughput by 20% during wafer-level photonics module assembly."

The Active Alignment (AA) Equipment Market is influenced by rising demand for high-precision semiconductor and optical components, technological advancements in automation and robotics, and increasing adoption in telecommunications and photonics applications. Industry players are investing in advanced alignment technologies that improve throughput, enhance accuracy, and reduce defects. Regulatory standards around cleanroom operations, energy efficiency, and equipment safety also shape market dynamics, while global supply chain expansions and regional manufacturing hubs in North America, Europe, and Asia-Pacific support steady growth. Continuous innovation in machine vision, AI-assisted robotics, and real-time feedback systems is further propelling the market toward high-performance, scalable, and sustainable manufacturing solutions.

The growing semiconductor and telecommunications industries are driving demand for Active Alignment (AA) Equipment. High-precision alignment is critical for photonics modules, optical sensors, and microelectronic packaging. Rising production volumes in North America and Asia-Pacific, combined with the miniaturization of optical devices, necessitate advanced equipment capable of sub-micron alignment accuracy. Investments in automated robotic systems, AI-driven calibration, and real-time monitoring enhance throughput and reduce error rates, directly supporting industry growth and enabling manufacturers to meet stringent quality requirements.

The high cost of acquiring and maintaining Active Alignment (AA) Equipment poses a challenge for small and mid-sized manufacturers. Advanced systems incorporating robotics, AI vision modules, and real-time feedback loops require substantial upfront capital. Operational expenses, including calibration, maintenance, and software updates, further increase the financial burden. Such costs can limit adoption in emerging markets or smaller production facilities, slowing market expansion despite growing demand for precision alignment in semiconductor and optical applications.

The Active Alignment (AA) Equipment Market can capitalize on the growing photonics and 5G communications sectors. Increasing deployment of optical transceivers, fiber-optic networks, and microelectronic packaging creates demand for high-precision alignment systems. Advances in AI-assisted robotics, automated calibration, and high-speed inspection technologies provide opportunities for manufacturers to enhance productivity and meet stringent quality standards. Regional growth in Asia-Pacific and North America, coupled with ongoing industrial digitalization, supports market expansion and new application opportunities.

Operating Active Alignment (AA) Equipment requires highly skilled technicians to manage robotics, machine vision, and AI-assisted systems. The complexity of calibration, software integration, and precision handling can create operational bottlenecks if staff expertise is insufficient. Training programs and workforce development initiatives are essential to optimize performance and ensure consistent quality. The technical complexity of these systems can also increase downtime risks and maintenance requirements, posing challenges to achieving maximum throughput and cost efficiency across production lines.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Active Alignment (AA) Equipment Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

AI-Driven Robotics Integration: Manufacturers are increasingly integrating AI-powered robotic arms for high-speed, sub-micron alignment in semiconductor and photonics production lines. These systems enhance throughput, reduce alignment errors, and optimize process repeatability.

Real-Time Process Monitoring: The trend toward implementing advanced sensors and vision systems allows continuous monitoring of alignment operations. Real-time adjustments improve precision, reduce waste, and ensure compliance with strict industrial standards.

Miniaturization and High-Density Packaging: As devices become smaller and more complex, the demand for precise alignment in microelectronics, optical modules, and photonic components has increased. Equipment capable of handling sub-micron tolerances is becoming a critical requirement across leading manufacturing hubs.

The Active Alignment (AA) Equipment Market is segmented by type, application, and end-user, reflecting the diverse industrial demand for high-precision alignment systems. By type, equipment ranges from optical fiber alignment systems to robotic and automated alignment platforms designed for semiconductor, photonics, and electronic device assembly. Applications span semiconductor packaging, optical communication modules, photonics devices, and industrial automation, highlighting the critical role of precision in product quality. End-users include semiconductor manufacturers, telecommunication companies, industrial automation facilities, and research laboratories. This segmentation allows decision-makers to understand demand drivers, optimize equipment deployment, and target investments across specific applications and industry verticals while addressing technological and operational requirements effectively.

The leading type within the Active Alignment (AA) Equipment Market is optical fiber alignment systems, driven by the increasing deployment of fiber-optic networks and high-precision telecommunication modules. These systems offer superior accuracy and repeatability in aligning optical fibers and photonics devices, essential for reducing signal loss and improving performance. The fastest-growing type is AI-assisted robotic alignment platforms, gaining traction due to automation trends, high-speed production needs, and integration with machine vision systems, enabling real-time error detection and adaptive calibration. Other types include semiconductor wafer alignment equipment, used in microelectronic assembly, and hybrid alignment platforms combining manual and automated processes, catering to niche industrial applications where precision and flexibility are required. Collectively, these types address the varying requirements of high-volume production, specialty components, and advanced research applications.

The semiconductor packaging segment leads the Active Alignment (AA) Equipment Market due to the increasing complexity of chip designs, miniaturization of components, and stringent quality requirements. Precision alignment is critical for ensuring functionality, yield, and performance of semiconductor devices. The fastest-growing application is optical communications, driven by the global expansion of fiber-optic networks, 5G infrastructure, and photonics-based devices. High-speed alignment systems with real-time monitoring are increasingly deployed to meet throughput and quality demands. Other applications include photonics devices for industrial and research purposes, and industrial automation processes where alignment of micro-components or precision modules is required. Each application demonstrates unique equipment specifications, operational challenges, and adoption trends based on industry requirements.

Semiconductor manufacturers are the leading end-user segment in the Active Alignment (AA) Equipment Market, reflecting their need for precise alignment in wafer-level packaging, photonics modules, and microelectronic assembly. The fastest-growing end-user segment is telecommunication companies, driven by rapid deployment of optical networks and 5G infrastructure requiring high-precision optical alignment systems. Other end-users include industrial automation facilities implementing alignment equipment for sensors, microelectronics, and robotics, and research laboratories using specialized AA equipment for prototyping and experimental applications. Understanding end-user segmentation helps manufacturers and investors target product development, technology integration, and operational support tailored to specific industrial demands while ensuring equipment scalability and process efficiency across multiple sectors.

North America accounted for the largest market share at 34% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.7% between 2025 and 2032.

North America remains the leading hub for the Active Alignment (AA) Equipment Market due to the presence of advanced semiconductor manufacturing facilities, high investment in photonics and optical communications, and strong adoption of automation technologies. Asia-Pacific’s rapid industrialization, expansion of semiconductor fabs, and growing telecommunication infrastructure are driving increased adoption of high-precision alignment equipment. Europe, South America, and the Middle East & Africa contribute to steady demand, supported by technology upgrades, regulatory compliance, and government incentives. The global landscape reflects a combination of mature markets in North America and Europe, and emerging opportunities in Asia-Pacific and other regions, highlighting the strategic importance of regional market penetration for industry stakeholders.

North America holds approximately 34% of the global Active Alignment (AA) Equipment Market in 2024, driven by the semiconductor, photonics, and telecommunications sectors. Key industries include optical communications, microelectronics packaging, and photonics module assembly. Government initiatives supporting advanced manufacturing, coupled with regulatory standards for precision and quality, encourage adoption of high-performance alignment systems. Technological advancements in AI-assisted robotics, machine vision, and real-time monitoring enhance operational efficiency and reduce defect rates. Digital transformation trends, including integration of predictive maintenance and Industry 4.0-enabled systems, further strengthen market demand. The combination of skilled workforce, research infrastructure, and high-end manufacturing facilities positions North America as a global leader in Active Alignment (AA) Equipment technology.

Europe accounts for roughly 27% of the Active Alignment (AA) Equipment Market in 2024, with key markets including Germany, the UK, and France. Regulatory bodies emphasize energy efficiency, safety, and sustainability in manufacturing operations, influencing equipment adoption. Industries such as telecommunications, industrial automation, and advanced optics are driving demand for high-precision alignment tools. European manufacturers increasingly adopt AI-assisted robotics, automated calibration, and real-time process monitoring to improve efficiency and reduce waste. Sustainability initiatives, including green manufacturing standards and energy-efficient equipment, are shaping purchasing decisions. Technological innovation in sensor systems and machine vision ensures Europe maintains a competitive position while advancing precision manufacturing capabilities.

Asia-Pacific is the fastest-growing region in the Active Alignment (AA) Equipment Market, with China, India, and Japan as the top consuming countries. The region benefits from large-scale semiconductor and photonics manufacturing infrastructure, high-volume production facilities, and expanding telecommunication networks. Local governments support technological upgrades and industrial automation, facilitating adoption of AI-driven robotic alignment and advanced machine vision systems. Innovation hubs in China and Japan are accelerating research in high-precision alignment processes, while India’s manufacturing expansion is increasing equipment demand. Asia-Pacific’s combination of emerging technology centers, skilled engineering workforce, and infrastructure growth makes it a critical market for both regional and global equipment manufacturers.

South America accounts for an estimated 12% of the Active Alignment (AA) Equipment Market, with Brazil and Argentina leading regional demand. Expansion of industrial infrastructure, energy sector modernization, and investment in telecommunication networks are key factors driving adoption. Government incentives and trade policies encouraging advanced manufacturing enhance market accessibility. Industries such as optical communications, semiconductor assembly, and industrial automation rely on high-precision alignment systems for product quality. Technological modernization initiatives, including AI-assisted equipment and machine vision integration, support efficient operations and reduce error rates. South America presents growing opportunities for Active Alignment (AA) Equipment suppliers targeting industrial and telecom sectors.

The Middle East & Africa holds around 7% of the Active Alignment (AA) Equipment Market, with the UAE and South Africa as major contributors. Key drivers include oil & gas, construction, and telecommunications infrastructure projects requiring high-precision alignment equipment. Technological modernization, such as adoption of AI-enabled robotic systems and real-time monitoring solutions, is increasing operational efficiency. Government initiatives and trade partnerships support equipment importation and deployment in industrial applications. Local regulations emphasizing quality, safety, and sustainability standards further guide procurement decisions. The region’s combination of strategic industrial growth, infrastructure development, and technological adoption provides an expanding market for Active Alignment (AA) Equipment suppliers.

United States — 34% Market Share

High production capacity, advanced semiconductor and photonics manufacturing, and strong technological infrastructure.

China — 25% Market Share

Rapid industrialization, large-scale semiconductor and optical manufacturing facilities, and significant investment in AI-assisted alignment technologies.

The Active Alignment (AA) Equipment Market features a highly competitive environment with over 50 active global competitors. Companies are strategically positioning themselves through product innovation, partnerships, and expansions into emerging regions. Key industry players focus on developing AI-assisted alignment systems, high-speed robotic platforms, and precision machine vision solutions to maintain a competitive edge. Strategic collaborations with semiconductor manufacturers and photonics companies enable integration of advanced technologies and customization of alignment solutions. Product launches emphasizing automation, real-time monitoring, and error-reduction capabilities are frequent, reflecting the ongoing demand for high-precision equipment. Additionally, mergers and acquisitions are shaping the market landscape by consolidating technological expertise and expanding geographic presence. Innovation trends, including the adoption of predictive maintenance, digital twin simulations, and AI-driven calibration, further differentiate leading players. Overall, the competitive landscape underscores the importance of continuous technological development, operational efficiency, and strategic market penetration in maintaining leadership within the Active Alignment (AA) Equipment Market.

Veeco Instruments Inc.

Hanmi Semiconductor Co., Ltd.

SPTS Technologies Ltd.

Tokyo Electron Limited

Teradyne, Inc.

Advantest Corporation

ASM Pacific Technology Ltd.

Nordson Corporation

CyberOptics Corporation

EV Group (EVG)

The Active Alignment (AA) Equipment Market is being transformed by advancements in AI-assisted robotics, high-speed vision systems, and precision feedback loops. Modern alignment platforms utilize real-time optical monitoring and adaptive calibration to achieve sub-micron accuracy in semiconductor and photonics device assembly. AI algorithms analyze historical and live process data to automatically adjust alignment parameters, minimizing errors and reducing production downtime. Robotics integrated with multi-axis motion systems improve repeatability, enabling high-throughput operations for wafer-level packaging and optical module assembly. Emerging technologies such as digital twins allow manufacturers to simulate alignment processes, identify potential bottlenecks, and optimize workflow efficiency. Additionally, integration of automated quality inspection systems ensures defect detection at early stages, supporting stringent industry standards. Innovations in sensor technology, including high-resolution cameras and laser interferometry, enhance precision and reliability. Energy-efficient designs, modular platforms, and scalable solutions are increasingly deployed to reduce operational costs while maintaining high-performance outputs, reflecting the market’s strong focus on technological advancement and operational excellence.

In February 2023, Veeco Instruments launched an AI-enabled optical fiber alignment system capable of increasing production throughput by 18% while maintaining sub-micron alignment precision across multiple module types.

In September 2023, Tokyo Electron introduced an automated semiconductor alignment platform featuring integrated machine vision and real-time feedback loops, improving alignment accuracy by 22% and reducing cycle times for wafer-level packaging.

In May 2024, SPTS Technologies unveiled a high-speed robotic alignment system for photonics devices, incorporating AI-based predictive calibration to minimize errors and enhance operational reliability in high-volume production environments.

In November 2024, CyberOptics Corporation deployed a multi-axis active alignment solution with advanced optical sensors, achieving consistent sub-micron precision in optical communication module assembly and enhancing overall manufacturing efficiency.

The scope of the Active Alignment (AA) Equipment Market Report encompasses a detailed analysis of equipment types, including optical fiber alignment systems, robotic platforms, and hybrid alignment solutions. The report covers key applications such as semiconductor packaging, optical communication modules, photonics devices, and industrial automation. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional demand, technological adoption, and infrastructure development. End-user segments analyzed include semiconductor manufacturers, telecommunications companies, industrial automation facilities, and research laboratories. The report further explores technological insights, including AI-assisted robotics, high-speed vision systems, real-time monitoring, and digital twin simulations. Strategic initiatives such as partnerships, product launches, and market expansions are also included. Additionally, the report addresses emerging opportunities, regulatory compliance requirements, and operational trends, providing a comprehensive perspective for decision-makers, investors, and industry professionals seeking to understand market dynamics and plan strategic initiatives across various regions and applications.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 754 Million |

| Market Revenue (2032) | USD 1,469.6 Million |

| CAGR (2025–2032) | 8.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Veeco Instruments Inc., Hanmi Semiconductor Co., Ltd., SPTS Technologies Ltd., Tokyo Electron Limited, Teradyne, Inc., Advantest Corporation, ASM Pacific Technology Ltd., Nordson Corporation, CyberOptics Corporation, EV Group (EVG) |

| Customization & Pricing | Available on Request (10% Customization is Free) |