Reports

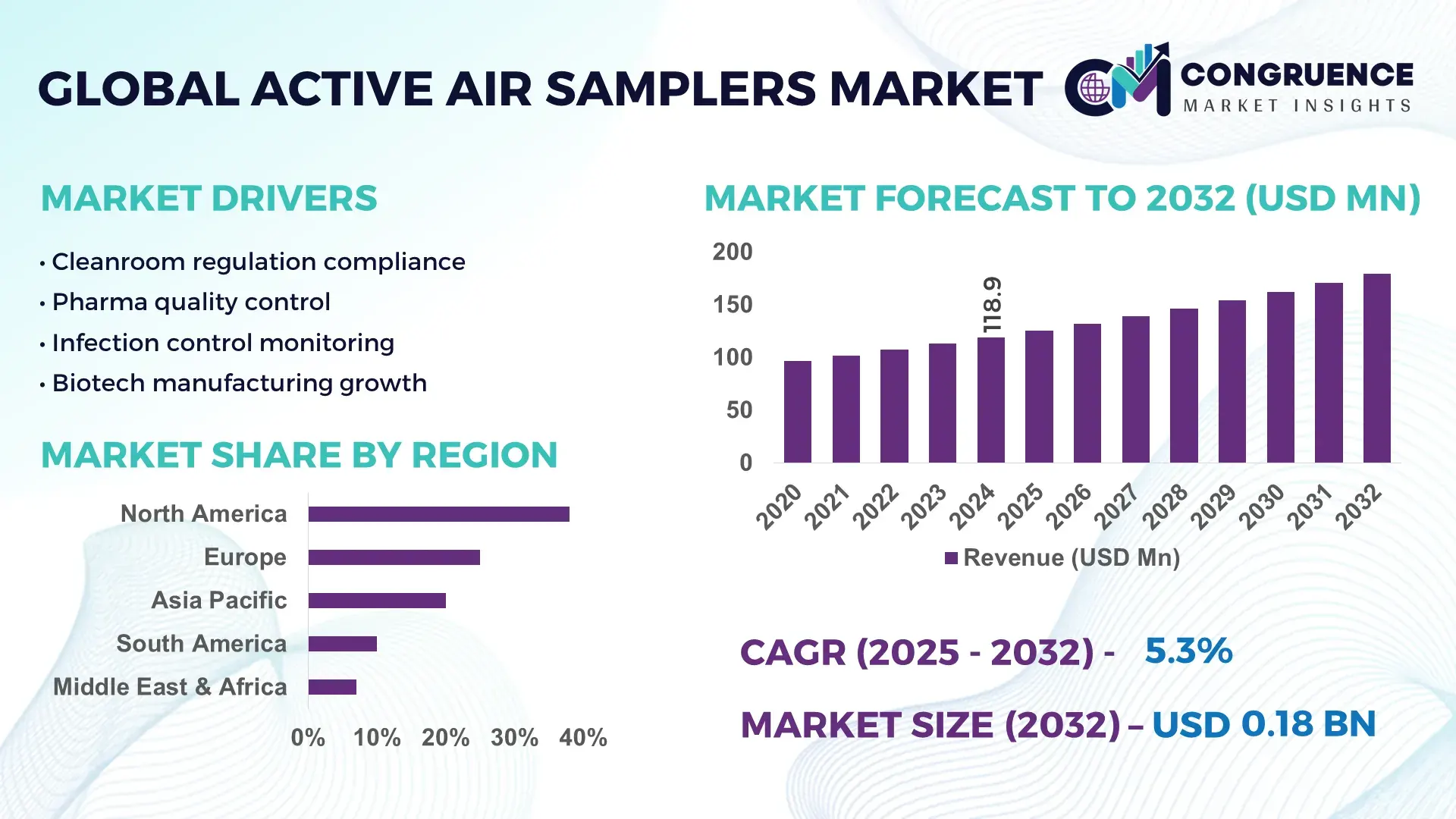

The Global Active Air Samplers Market was valued at USD 118.88 Million in 2024 and is anticipated to reach a value of USD 179.7 Million by 2032 expanding at a CAGR of 5.3% between 2025 and 2032. This growth is driven by rising regulatory emphasis on airborne contamination monitoring across pharmaceutical manufacturing, healthcare facilities, and cleanroom-dependent industries.

The United States dominates the Active Air Samplers marketplace, supported by strong domestic manufacturing capacity and sustained institutional investment. More than 35% of global active air sampler manufacturing facilities are located in the U.S., with annual production exceeding 22,000 units. Public and private investments in environmental monitoring technologies surpassed USD 420 million in 2023. Active air samplers are widely deployed across pharmaceutical cleanrooms, biotechnology labs, food processing plants, and hospital infection control units. Technological advancements such as IoT-enabled real-time microbial detection, HEPA-integrated sampling systems, and automated volumetric airflow calibration have seen adoption rates above 48% among large U.S.-based life science manufacturers. North America accounts for approximately 38% of global installations, with pharmaceutical and biotech users representing nearly 52% of end-user demand.

Market Size & Growth: Valued at USD 118.88 Million in 2024, projected to reach USD 179.7 Million by 2032 at a CAGR of 5.3%, supported by stricter cleanroom compliance and airborne contamination control mandates.

Top Growth Drivers: Pharmaceutical cleanroom adoption +41%, hospital infection surveillance deployment +34%, food safety monitoring integration +29%.

Short-Term Forecast: By 2028, automated active air samplers are expected to deliver 22% reduction in sampling time and 18% improvement in microbial detection accuracy.

Emerging Technologies: IoT-connected samplers, real-time microbial analytics, low-noise high-flow volumetric sampling systems.

Regional Leaders: North America USD 68.4 Million by 2032 with pharma-led adoption; Europe USD 52.1 Million driven by GMP enforcement; Asia-Pacific USD 46.8 Million supported by biotech facility expansion.

Consumer/End-User Trends: Pharmaceutical manufacturers and hospitals account for over 60% of installations, with increased preference for portable, automated, and data-integrated systems.

Pilot or Case Example: A 2024 hospital infection-control pilot in Germany achieved a 27% reduction in airborne contamination incidents using continuous active air sampling.

Competitive Landscape: Market leader Merck KGaA holds ~18% share, followed by Sartorius AG, bioMérieux, Particle Measuring Systems, and Thermo Fisher Scientific.

Regulatory & ESG Impact: Compliance with ISO 14644, EU GMP Annex 1, and FDA aseptic processing guidelines is accelerating adoption of validated active air samplers.

Investment & Funding Patterns: Over USD 310 Million invested globally since 2022, with strong growth in smart monitoring and cleanroom automation funding.

Innovation & Future Outlook: Integration of AI-driven microbial trend analysis and cloud-based compliance reporting is expected to reshape monitoring workflows.

The Active Air Samplers Market serves critical industry sectors including pharmaceuticals (approximately 45% of demand), healthcare and hospitals (17%), biotechnology research (15%), food and beverage processing (13%), and electronics cleanrooms (10%). Recent innovations include battery-operated portable samplers, automated colony counting integration, and continuous air monitoring platforms compatible with digital quality management systems. Regulatory frameworks such as EU GMP Annex 1 revisions, ISO cleanroom standards, and hospital-acquired infection prevention policies are key market drivers. Regionally, North America leads consumption due to high pharmaceutical output, while Asia-Pacific shows the fastest growth fueled by expanding biologics manufacturing and hospital infrastructure. Emerging trends include continuous monitoring adoption, smart data analytics, and integration of active air samplers into broader environmental monitoring ecosystems, positioning the market for steady long-term expansion.

The strategic relevance of the Active Air Samplers Market is closely tied to its role in contamination control, regulatory compliance, and operational risk mitigation across highly regulated industries. Pharmaceutical and biotechnology manufacturing facilities rely on active air samplers as a core component of environmental monitoring programs, with over 65% of GMP-certified cleanrooms globally deploying continuous or periodic active air sampling systems. Strategy is increasingly centered on automation, data integrity, and integration with digital quality management systems. IoT-enabled active air samplers deliver nearly 32% improvement in data accuracy compared to traditional manual impactor-based sampling standards.

Asia-Pacific dominates in production volume due to expanding pharmaceutical manufacturing hubs, while Europe leads in adoption with approximately 58% of regulated life science enterprises using automated active air monitoring solutions. By 2027, AI-driven microbial trend analytics integrated into active air samplers is expected to improve contamination detection lead time by 25%, enabling faster corrective action. From a compliance and ESG standpoint, firms are committing to sustainability metrics such as 30% reduction in consumable waste and recyclable sampling media by 2030. In 2024, a U.S.-based pharmaceutical manufacturer achieved a 21% reduction in cleanroom deviation incidents through deployment of real-time active air sampling combined with predictive analytics. Looking ahead, the Active Air Samplers Market is positioned as a critical pillar supporting operational resilience, regulatory assurance, and sustainable growth across global life science and healthcare ecosystems.

Pharmaceutical and biotechnology facilities represent the largest driver for the Active Air Samplers Market, accounting for more than 45% of total installations globally. The number of GMP-compliant cleanrooms increased by over 18% between 2021 and 2024, directly increasing demand for validated air monitoring equipment. Each Grade A and B cleanroom typically requires multiple active air samplers to meet routine and continuous monitoring protocols. Additionally, vaccine manufacturing, biologics, and cell therapy facilities demand higher sampling frequencies, often exceeding 20 sampling cycles per shift. This structural expansion of contamination-sensitive production environments continues to generate sustained demand for reliable, high-precision active air sampling systems.

Despite strong demand fundamentals, the Active Air Samplers Market faces restraints related to high upfront validation, calibration, and maintenance requirements. Installation and qualification of active air samplers can increase environmental monitoring program costs by 15–20%, particularly in multi-room cleanroom facilities. Regular airflow calibration, microbial efficiency validation, and consumable replacement add to lifecycle costs. Smaller laboratories and contract manufacturers often delay upgrades due to budget constraints, opting for periodic manual sampling instead. Additionally, skilled personnel are required to interpret data and maintain compliance documentation, limiting adoption in cost-sensitive regions and smaller healthcare facilities.

Automation and digital integration present a major growth opportunity for the Active Air Samplers Market. Over 40% of pharmaceutical manufacturers plan to transition to automated environmental monitoring systems within the next five years. Active air samplers integrated with cloud-based dashboards, electronic batch records, and alarm systems reduce manual intervention and audit preparation time by up to 30%. Emerging markets in Asia-Pacific and Latin America are also investing in new GMP facilities, creating greenfield opportunities for modern air sampling solutions. Portable and battery-operated samplers tailored for modular cleanrooms and hospital isolation units further expand addressable use cases.

Regulatory fragmentation remains a key challenge for the Active Air Samplers Market. While standards such as ISO 14644 and EU GMP Annex 1 define general requirements, regional interpretation and enforcement vary significantly. Manufacturers must customize validation protocols for different geographies, increasing compliance complexity and documentation burden. Frequent regulatory updates require equipment upgrades or software modifications, raising operational uncertainty for end users. Additionally, audits increasingly demand real-time traceability and data integrity controls, placing pressure on legacy air samplers that lack digital capabilities. These challenges require continuous innovation and close alignment between manufacturers and regulatory bodies.

• Accelerated Adoption of Modular and Prefabricated Cleanroom Infrastructure: The expansion of modular and prefabricated cleanroom construction is reshaping demand patterns in the Active Air Samplers market. Approximately 55% of newly commissioned pharmaceutical and biotechnology facilities now incorporate modular cleanroom designs to reduce construction timelines by 30–40%. These facilities require flexible, portable, and rapidly deployable active air samplers compatible with prefabricated wall and ceiling systems. In Europe and North America, over 48% of modular cleanroom projects specify compact active air samplers with quick-mount airflow interfaces, driving higher demand for precision-engineered, lightweight systems capable of fast validation.

• Shift Toward Continuous and Automated Air Monitoring Systems: Active air samplers are increasingly deployed in continuous monitoring configurations rather than periodic sampling models. Nearly 42% of regulated manufacturing sites upgraded to automated sampling systems between 2022 and 2024, reducing manual intervention by 35%. Automated volumetric control improves sampling consistency by up to 28% compared to manually adjusted units. This trend is particularly strong in aseptic fill-finish lines, where continuous monitoring has lowered environmental deviation incidents by approximately 22% within the first year of implementation.

• Integration of Digital Data Management and Connectivity Features: Digitalization is transforming active air samplers into connected compliance tools. Over 46% of newly installed systems now feature direct integration with electronic quality management systems and cloud-based dashboards. These connected samplers improve audit readiness by 31% and reduce environmental monitoring documentation time by nearly 25%. Facilities adopting digitally enabled samplers report up to 18% faster root-cause analysis during contamination investigations, reinforcing demand for software-enabled hardware platforms across pharmaceutical and hospital environments.

• Rising Demand from Hospital Infection Control and Isolation Units: Hospitals and healthcare facilities are emerging as high-growth adopters of active air samplers, particularly for infection surveillance in operating rooms and isolation wards. Active air monitoring deployments in hospitals increased by approximately 27% between 2021 and 2024. Portable samplers capable of handling airflow volumes above 100 liters per minute are preferred, supporting real-time detection of airborne pathogens. Facilities using routine active air sampling have reported up to 20% reductions in post-surgical airborne contamination incidents, strengthening long-term adoption trends in healthcare settings.

The Active Air Samplers market is segmented by type, application, and end-user, reflecting varied operational requirements across contamination-sensitive environments. Product differentiation is primarily driven by portability, automation level, and airflow precision. Application segmentation highlights strong demand from regulated manufacturing and healthcare settings where airborne microbial control is mandatory. End-user insights show adoption patterns closely aligned with regulatory exposure, scale of operations, and quality assurance maturity. Across segments, decision-makers increasingly prioritize accuracy, validation speed, digital traceability, and compatibility with cleanroom standards, shaping procurement and upgrade strategies globally.

Active Air Samplers are categorized into portable active air samplers, fixed/remote active air samplers, and automated continuous monitoring air samplers. Portable active air samplers currently account for approximately 46% of adoption, driven by their flexibility, ease of validation, and suitability for routine monitoring across multiple cleanroom zones. Fixed and remote systems represent about 28% of adoption, primarily used in high-grade cleanrooms requiring constant location-based sampling. However, automated continuous monitoring air samplers are the fastest-growing type, expanding at an estimated 9.4% CAGR, supported by rising demand for real-time contamination alerts and reduced manual intervention. The remaining niche systems, including hybrid and specialty samplers for isolators and biosafety cabinets, together contribute roughly 26% of total installations.

Applications of Active Air Samplers span pharmaceutical manufacturing, hospitals and healthcare facilities, biotechnology research laboratories, food and beverage processing, and electronics cleanrooms. Pharmaceutical manufacturing leads application usage with nearly 44% adoption, as aseptic processing, sterile filling, and biologics production require frequent and validated air monitoring. Hospitals and healthcare settings account for around 21%, focusing on operating theaters and isolation wards. Biotechnology research is the fastest-growing application, advancing at an estimated 8.7% CAGR due to the expansion of cell and gene therapy labs requiring stringent environmental controls. Food, beverage, and electronics applications collectively contribute approximately 35%, supporting hygiene validation and particulate control.

Pharmaceutical and biotechnology companies represent the leading end-user group, accounting for about 48% of total Active Air Samplers adoption due to strict regulatory oversight and continuous monitoring mandates. Hospitals follow with roughly 22%, while contract research and manufacturing organizations account for nearly 15%. However, research institutes and academic laboratories are the fastest-growing end-user segment, expanding at an estimated 7.9% CAGR, driven by increased funding for infectious disease research and biosafety infrastructure. Food processors, electronics manufacturers, and environmental monitoring agencies together contribute the remaining 15%, with adoption rates exceeding 30% in large-scale facilities.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

North America leads due to high penetration of GMP-compliant pharmaceutical facilities, with over 65% of biologics and sterile drug manufacturing sites actively using validated active air samplers. Europe followed with approximately 29% share in 2024, supported by stringent EU GMP Annex 1 enforcement across more than 12,000 regulated cleanrooms. Asia-Pacific held nearly 23% share, driven by rapid expansion of pharmaceutical and hospital infrastructure, with China and India together accounting for over 45% of new cleanroom additions since 2021. South America and the Middle East & Africa collectively represented about 10%, with adoption concentrated in urban healthcare hubs and export-oriented pharmaceutical clusters. Regional disparities are shaped by regulatory maturity, healthcare spending intensity, cleanroom density per capita, and pace of digital monitoring adoption.

How is advanced regulatory enforcement shaping demand for precision monitoring systems?

North America accounted for approximately 38% of the Active Air Samplers market in 2024, supported by strong demand from pharmaceutical manufacturing, biotechnology research, and hospital infection control programs. More than 70% of large pharmaceutical plants in the U.S. deploy automated or semi-automated air sampling systems to meet FDA aseptic processing requirements. Recent regulatory updates emphasizing data integrity and continuous monitoring have accelerated replacement of legacy samplers. Digital transformation trends include integration with electronic batch records and centralized dashboards, now adopted by nearly 44% of facilities. Local manufacturers are focusing on IoT-enabled samplers with real-time alerts to reduce deviation investigations. Regional consumer behavior shows higher enterprise-level adoption in healthcare systems, where multi-site hospital networks standardize air sampling protocols across facilities.

Why is compliance-driven innovation accelerating system upgrades?

Europe held close to 29% of the Active Air Samplers market in 2024, with Germany, the UK, and France collectively contributing over 60% of regional installations. Regulatory bodies enforcing updated EU GMP Annex 1 guidelines have increased demand for continuous and automated air monitoring, particularly in sterile manufacturing. Sustainability initiatives encouraging reduced consumable waste have driven adoption of reusable and low-impact sampling heads. Approximately 36% of new installations now include digital traceability features. Regional manufacturers are investing in low-noise, energy-efficient samplers tailored for hospital and laboratory use. Consumer behavior reflects strong preference for explainable, audit-ready systems capable of supporting regulatory inspections with minimal manual documentation.

How is industrial expansion transforming environmental monitoring demand?

Asia-Pacific ranked as the fastest-expanding region, holding about 23% of the Active Air Samplers market in 2024. China, India, and Japan are the largest consuming countries, together accounting for nearly 68% of regional demand. Rapid growth in pharmaceutical exports, hospital construction, and contract manufacturing has driven installation of over 9,000 new cleanrooms since 2020. Regional innovation hubs are focusing on compact, cost-efficient samplers compatible with modular facilities. Local manufacturers are scaling production to meet domestic demand while improving calibration accuracy. Consumer behavior varies widely, with large enterprises adopting automated systems while smaller laboratories prioritize portable, entry-level samplers for compliance.

What role does healthcare modernization play in adoption patterns?

South America represented approximately 6% of the global Active Air Samplers market in 2024, with Brazil and Argentina accounting for over 70% of regional usage. Growth is supported by investments in pharmaceutical manufacturing, vaccine production, and hospital infrastructure upgrades. Government incentives targeting local drug production have increased cleanroom installations by nearly 22% since 2021. Trade policies encouraging medical equipment imports have improved access to advanced air samplers. Regional suppliers focus on rugged, easy-to-maintain systems suited for variable operating environments. Consumer behavior shows demand closely tied to public healthcare expansion and regulatory alignment with international standards.

How are healthcare investments and industrial diversification influencing demand?

The Middle East & Africa accounted for roughly 4% of the Active Air Samplers market in 2024, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Healthcare infrastructure projects and pharmaceutical localization initiatives are primary growth drivers. More than 120 new hospitals and life science facilities were commissioned across the region between 2021 and 2024, increasing demand for validated air monitoring systems. Technological modernization includes adoption of portable samplers for flexible deployment. Regional regulations increasingly reference international GMP standards, boosting compliance-driven purchases. Consumer behavior reflects preference for durable, low-maintenance systems due to climatic and operational conditions.

United States Active Air Samplers Market – 26% share: Dominance driven by high concentration of GMP-certified pharmaceutical facilities and advanced regulatory enforcement.

Germany Active Air Samplers Market – 12% share: Leadership supported by strong pharmaceutical manufacturing base and strict compliance with EU cleanroom standards.

The Active Air Samplers market is moderately fragmented, characterized by the presence of approximately 25–30 active global and regional manufacturers competing across regulated and non-regulated end-use sectors. The top five companies collectively account for an estimated 55–60% of total installations, indicating a semi-consolidated structure driven by technological differentiation and regulatory credibility rather than price competition alone. Market leaders are positioned strongly in pharmaceutical and biotechnology applications, where validated performance, audit readiness, and digital traceability are key purchasing criteria.

Competitive strategies increasingly focus on product innovation, with over 40% of leading players introducing upgraded models featuring automated airflow control, real-time microbial alerts, and software integration between 2022 and 2024. Strategic partnerships between equipment manufacturers and digital quality management providers have increased by nearly 30%, enabling end-to-end environmental monitoring solutions. Select players are expanding geographically through distribution agreements in Asia-Pacific and the Middle East to capture infrastructure-led demand. Mergers and technology acquisitions remain selective, accounting for fewer than 10% of competitive actions, as firms prioritize organic innovation and regulatory approvals. Overall, competition is intensifying around automation, portability, and compliance-driven performance metrics.

Sartorius AG

Merck KGaA

bioMérieux

Thermo Fisher Scientific

Particle Measuring Systems

Lighthouse Worldwide Solutions

MBV AG

Orum International

VWR International

The Active Air Samplers market is undergoing significant technological evolution, with innovations centered on automation, connectivity, and analytical precision. Traditional impaction-based samplers, which historically accounted for over 60% of installed units due to their simplicity, are increasingly being supplemented or replaced by advanced volumetric and real-time detection systems. Automated volumetric control technology now featured in approximately 48% of newly installed samplers ensures precise airflow regulation at set flow rates (e.g., 100–400 L/min) without manual calibration, reducing operator variability and improving consistency across sampling cycles.

Digital integration is a defining trend: more than 42% of modern active air samplers are equipped with embedded connectivity features that stream data directly to electronic quality systems and centralized dashboards. This shift enables audit-ready reporting, remote monitoring, and enhanced trend analysis, which has accelerated deployment in multi-site pharmaceutical and biotechnology operations. Wi-Fi and Ethernet enabled units support secure data transfer and timestamped logging, which improves compliance documentation efficiency by an estimated 28–32% in operational evaluations.

Emerging technologies include IoT-enabled sensors, predictive analytics modules, and AI-assisted contamination pattern recognition. IoT connectivity allows real-time alerts based on predefined thresholds, improving response times to airborne contamination events by more than 20% compared with standalone samplers. Predictive algorithms analyze historical sampling data to identify anomalies before excursions occur, benefiting cleanroom environments where proactive mitigation protects sensitive production processes.

In terms of hardware innovation, battery-operated and lightweight portable samplers now make up close to 35% of new deployments in hospitals and field labs due to demands for flexibility and rapid redeployment. Additionally, high-efficiency HEPA-integrated sampling heads improve capture efficiency for micron and sub-micron particulates, addressing stringent requirements in advanced laboratories and electronics cleanrooms. As digital transformation and advanced sampling technologies converge, the Active Air Samplers market is increasingly defined by systems that deliver higher data integrity, operational agility, and compliance support for complex quality management ecosystems.

• In early 2023, Sartorius expanded its MD8 series to include models offering automated flow rate validation and auto-recorded audit trails compliant with updated cleanroom standards, designed to reduce operator error in sterile manufacturing environments.

• In mid-2024, Merck MilliporeSigma introduced a new MAS-100 NT software suite enabling centralized monitoring of multiple active air samplers across cleanroom zones, improving oversight for facilities operating parallel manufacturing lines.

• In late 2023, Lighthouse Worldwide Solutions upgraded its cloud-enabled ecosystem, integrating viable air data with particle counts and environmental parameters like temperature and humidity into a unified contamination dashboard. (

• In 2024, Particle Measuring Systems launched a mobile calibration verification unit for active air samplers, allowing contract manufacturing organizations to revalidate equipment in-house without disrupting production schedules.

The Active Air Samplers Market Report provides a comprehensive analysis of the global landscape, offering an in-depth view across product, application, technology, and regional dimensions. It covers key product segments such as portable microbial air samplers, desktop units, fixed/remote monitoring systems, and continuous air sampling platforms, detailing configuration options, efficiency characteristics, and suitability for different environmental monitoring needs. The report also examines application domains including pharmaceutical production, biotechnology research, hospitals and clinical laboratories, food processing facilities, and electronics cleanrooms, providing insights into adoption drivers, usage patterns, and compliance requirements unique to each sector.

On the technology front, the report highlights current and emerging innovations such as automated volumetric control, embedded connectivity, IoT-enabled data integration, and enhanced microbial capture mechanisms, illustrating how digital transformation is influencing procurement decisions and operational practices. Geographic scope includes detailed breakdowns for North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with specific country-level insights on regulatory pressure, infrastructure expansion, and regional adoption behavior. End-user focus areas extend to contract development and manufacturing organizations (CDMOs), academic laboratories, and environmental monitoring agencies. Emerging and niche segments such as battery-operated portable units, hybrid fixed-portable configurations, and AI-assisted air quality analysis solutions are also examined, offering decision-makers clarity on opportunity areas, competitive positioning, and technological differentiation within the active air samplers ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 118.88 Million |

|

Market Revenue in 2032 |

USD 179.7 Million |

|

CAGR (2025 - 2032) |

5.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sartorius AG, Merck KGaA, bioMérieux, Thermo Fisher Scientific, Particle Measuring Systems, Lighthouse Worldwide Solutions, MBV AG, Orum International, VWR International, Sartorius AG, Thermo Fisher Scientific, Particle Measuring Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |