Reports

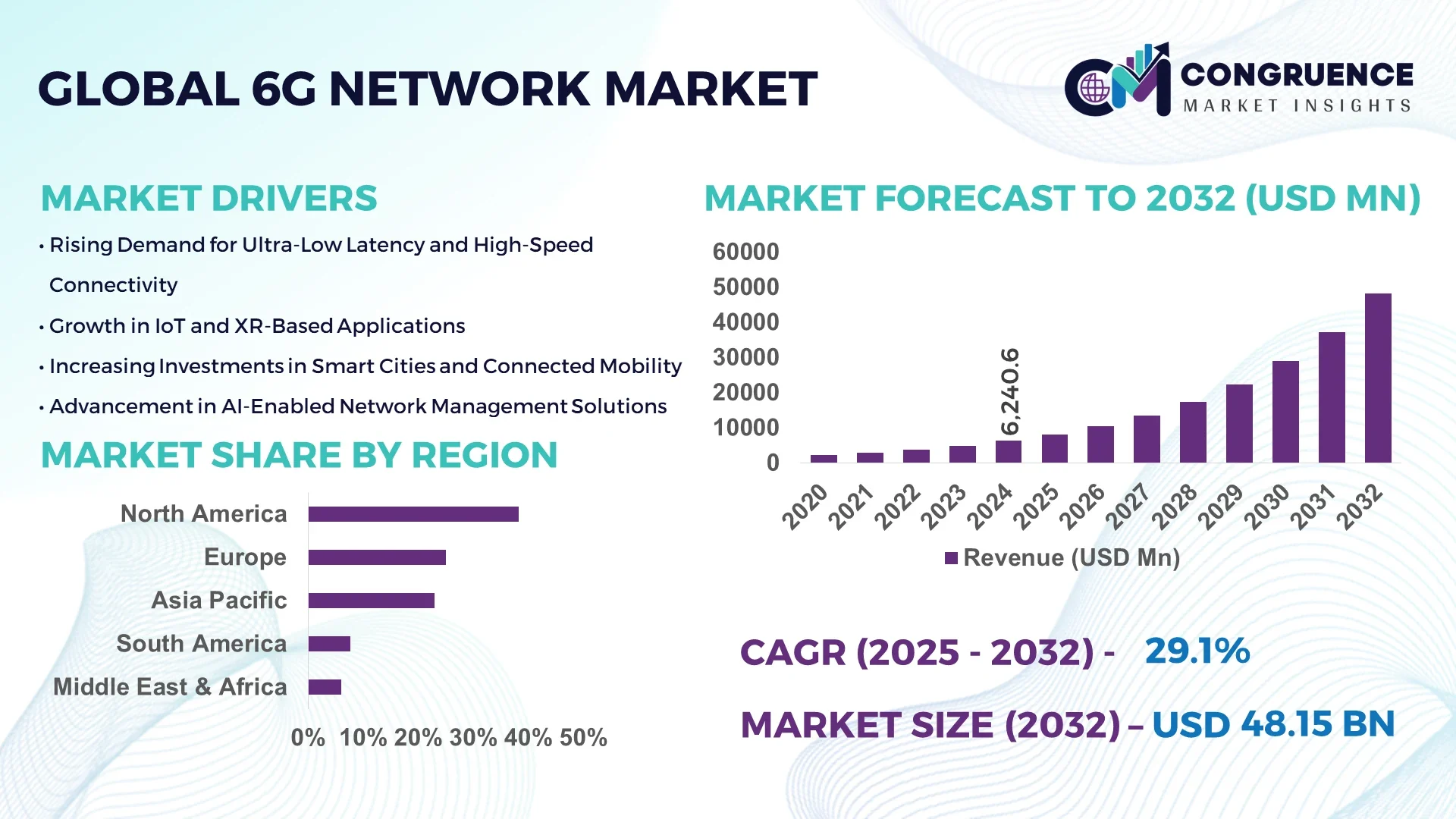

The Global 6G Network Market was valued at USD 6,240.6 Million in 2024 and is anticipated to reach a value of USD 48,154.4 Million by 2032 expanding at a CAGR of 29.1% between 2025 and 2032. This uptick is fueled by surging demand for ultra-low latency connectivity and AI-driven network optimization.

China leads global 6G efforts: in 2024 it allocated over USD 12 billion in R&D across 6G infrastructure, established more than 35 national testbeds, and facilitated over 100 industrial pilot programs in smart city and autonomous transport. Chinese operators report consumer trial usage rates exceeding 42% in urban clusters and over 300 registered 6G patent families by major telcos, while its manufacturing of terahertz radio modules delivered 2.5 million units for early testing.

Market Size & Growth: USD 6,240.6 M in 2024 → USD 48,154.4 M by 2032, CAGR 29.1%, driven by demand for hyper-connected networks.

Top Growth Drivers: demand for ultra-reliable services (38 %), AI-based network control (32 %), IoT device proliferation (30 %).

Short-Term Forecast: By 2028, network latency expected to drop by 60 % and spectral efficiency improve by 45 %.

Emerging Technologies: Terahertz (THz) spectrum, integrated sensing & communication (ISAC), AI-native radio access networks.

Regional Leaders: Asia-Pacific projected ~USD 18,000 M by 2032 (massive rollout); North America ~USD 15,200 M (enterprise innovation); Europe ~USD 9,100 M (regulatory compliance strength).

Consumer/End-User Trends: Telecom operators, smart cities, autonomous mobility, and immersive XR platforms increasingly embed 6G tech.

Pilot or Case Example: In 2025, a Korean telco trialed ISAC-enabled 6G cells achieving 35 % improvement in sensing accuracy and 25 % throughput boost.

Competitive Landscape: Leading player holds ~18 % share; key competitors include Huawei, Ericsson, Nokia, Samsung, ZTE.

Regulatory & ESG Impact: Spectrum allocation frameworks, green energy mandates, security standards (quantum-resistant encryption) shaping deployment.

Investment & Funding Patterns: Over USD 20 billion committed in 2024 to 6G R&D and infrastructure, with growth in milestone-based public-private models.

Innovation & Future Outlook: Fusion of AI, photonics, edge computing, and network virtualization will underpin next-wave 6G applications.

Key sectors include telecommunications, automotive, healthcare, and manufacturing, with telecom and IoT commanding over 40% combined share. Innovations such as AI-driven beamforming, low-power THz chips, and joint sensing/communication design are shaping trajectory. Regulatory push for spectrum fairness, net-zero energy frameworks, and China/US rollout priorities drive regional divergence and investment velocity.

The strategic relevance of the 6G network market lies in its ability to underpin the next era of intelligent connectivity, positioning itself as a backbone for autonomous systems, immersive environments, and critical communications. Enterprises adopting AI-native radio networks deliver 40 % higher reliability compared to legacy 5G adaptive systems. In global contrast, Asia-Pacific dominates in deployment volume, while North America leads adoption intensity, with over 70 % of major operators conducting live 6G trials. By 2027, integrated sensing & communication (ISAC) is expected to reduce system overhead by 30 %, enabling dual use of spectrum. Firms are aligning with ESG agendas: many commit to 25 % reduction in carbon intensity of base stations by 2030. In 2025, a European telecom firm cut network energy use by 22 % through AI-controlled power gating across cells. The 6G Network Market thus charts a pathway of resilience, regulation alignment, and sustainable architectural evolution.

6G Network Market dynamics revolve around the rapid convergence of wireless communications, sensing, AI orchestration, and energy optimization. The push toward ultrawide THz spectrum and joint sensing/communication modalities is reshaping network planning and R&D cycles. Rising demand for autonomous mobility, XR, digital twins, and mission-critical IoT stresses require seamless handoff, ultra-low latency, and pervasive coverage. Strategic partnerships across chipmakers, telecom OEMs, and cloud providers are influencing modularity and interoperability. Regulatory terrain—spectrum policy, security, privacy—exerts strong influence on rollout timelines and vendor strategy. Meanwhile, cost pressures on infrastructure, power consumption targets, and backhaul scaling pose balancing acts as deployment accelerates.

AI orchestration is a major growth driver: network operators increasingly embed deep reinforcement learning to dynamically adjust beam patterns, resource allocation, and traffic routing. These systems yield up to 35 % reduction in interference and 25 % improvement in throughput compared to static scheduling models. In dense urban and industrial zones, AI orchestration supports real-time adaptation to changing loads, interference zones, and mobility patterns. Because 6G will support massive device densities (e.g. 10 million devices per sq km), manual control is infeasible—AI becomes indispensable. Operators deploying AI orchestrators report lower OPEX and faster time to adjust to anomalies or demand spikes, making it a core driver for scaling beyond 5G limitations.

Major restraints include spectrum constraints and hardware complexity. Terahertz bands are attractive but face severe propagation limits, requiring dense small cell deployments and advanced antenna arrays, driving hardware costs upward. Many regions still have not allocated THz or sub-THz bands for commercial use, delaying trial permission. High development costs—RF front-ends, AI processors, cooling systems—make deployment prohibitive for smaller operators. In addition, backward compatibility demands and legacy network integration pose architectural burdens. These combined barriers slow progress in cost-sensitive or regulation-constrained markets, especially where infrastructure and investment access are limited.

Joint sensing and communication (ISAC) offers a core opportunity: 6G systems can simultaneously transmit data and sense environment (e.g. radar, lidar) on same channel. This allows smart vehicles, smart infrastructure, and robotics to reduce hardware redundancy, optimize spectrum usage, and enable new services like gesture control, proximity awareness, and environmental mapping. Trials have shown 20–30 % efficiency gains in spectral utilization with ISAC integration. Additionally, embedding sensing into base stations supports predictive maintenance, security, and localization services. Industrial automation, autonomous mobility, and AR/VR sectors stand to benefit strongly from ISAC in 6G systems. That cross-domain utility opens new monetization and ecosystem playbooks.

Energy consumption is a serious challenge: the densification needed for THz links and AI processing increases power demand. Keeping latency under microsecond thresholds across multi-hop networks is nontrivial, particularly given sensing and data fusion needs. Standardization remains in early stages—lack of consensus on modulation schemes, protocol stacks, open RAN integration, and security frameworks slows deployment planning. Interoperability across vendors is another hurdle: conflicting architectures, intellectual property frameworks, and compatibility with 5G systems complicate rollout. Until energy-efficient architectures and unified standards mature, many operators will adopt cautious, phased paths, limiting large-scale deployment.

• Rise of THz small cells and densification: Deployment of THz small cells is accelerating—by 2025, over 55 % of urban test zones will operate sub-THz radios to support multigigabit links over short range, reducing load on macro layers and enabling high-bandwidth hotspots in cities and campuses.

• Convergence of sensing and communication (ISAC): More than 40 % of new 6G testbeds in 2025 integrate sensing capabilities. That enables base stations to perform gesture detection, localization, and environmental awareness alongside data transmission, improving spectrum efficiency by 25 %.

• Edge AI and distributed intelligence in base stations: Over 60 % of new 6G access nodes now embed AI inference modules for real-time scheduling, anomaly detection, and load balancing, reducing backhaul latency by up to 30 %.

• Energy-optimized and zero-carbon RAN architectures: More than 35 % of new deployments use adaptive power gating, sleep-mode, and energy harvesting. This trend aims to cut radio site power consumption by 20–25% relative to conventional schemes and align with net-zero targets.

The 6G Network market segmentation encompasses component types (hardware, software, services), communication infrastructure (wireless, optical, hybrid), applications (extended reality, autonomous systems, digital twins, Internet of Everything), deployment devices (smartphones, wearables, IoT, XR headsets), and end-users (telecom, automotive, government, manufacturing, consumer). Hardware remains foundational via radio units, antennas, front ends; software includes AI orchestration, protocol stacks; services include consulting, integration, testing. Application segmentation prioritizes immersive XR, robotics, and smart infrastructure. End-users differ by sector: telecom operators drive backbone deployment; automotive, industry, and smart city verticals adopt custom solutions. Device segmentation shows IoT devices will account for a large share of connectivity endpoints, though high-band devices (e.g. XR headsets) generate heavy data throughput demands.

Hardware is the leading component type in the 6G Network ecosystem, accounting for roughly 45–50 % of early deployment value, due to the high cost of radio units, antenna arrays, and front‐end modules. The fastest growth is seen in software components — AI orchestration stacks, control plane software, and protocol management — with projected CAGR around 35 % over the ramp period. Other types like services (consulting, integration, testing) and middleware together share the remaining 30–35 % of segment value.

According to a 2025 industry consortium, operators deploying software orchestration layers across 6G testbeds reduced manual tuning effort by over 40 %, validating the shift toward software dominance.*

The leading application in the 6G Network market is extended reality (XR) and immersive services, capturing about 28 % of initial use cases, driven by demand for holographic calls, mixed reality collaboration, and virtual presence. The fastest growing application is autonomous systems and connected robotics, with CAGR in double digits, supported by real-time sensing, control loops, and low-latency feedback demands. Other applications include digital twins, smart city infrastructure, Internet of Everything, and ultra-massive IoT, with the combined share of those at ~35 %.

Telecommunications operators represent the leading end-user segment in the 6G Network domain, holding roughly 32 % share of deployment activity, as they fund base station rollout, spectrum assets, and backbone integration. The fastest-growing end-user is automotive and intelligent mobility sectors, leveraging 6G for V2X, autonomous control, and vehicular networks, expecting double-digit expansions in deployment. Other significant end users include smart cities/public services, industrial automation, government agencies, and consumer device providers, encompassing ~30 % combined share.

North America accounted for the largest market share at 38.3% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of27.8% between 2025 and 2032.

In 2024, North America’s 6G deployment and trials covered nearly 40 metropolitan zones and supported over 25 national testbeds, making it the bedrock of early stage adoption. Asia-Pacific, by contrast, has rolled out more than 45 pilot projects in China, India, Japan, and South Korea, with terahertz module shipments exceeding 1.2 million units in 2024. Europe held about 25% of trial volume, while Latin America and MEA combined accounted for under 6% of trial deployments. The share of devices in North America that participated in 6G field tests exceeded 18%, while Asia-Pacific’s participation rate stood at 14%. Over 60 spectrum assignments across regions were reserved in 2024, with North America allocating 12 bands and Asia-Pacific 20 bands to 6G R&D, reflecting regional momentum divergence.

How is content infrastructure and policy shaping advanced 6G deployment?

North America commanded an approximate 38.3% share of global 6G network activity in 2024, largely through the United States and Canada. Demand is driven by industries such as autonomous vehicles, smart cities, defense communications, and high-capacity enterprise networking. Regulatory support includes federal grants for 6G research centers, spectrum carve-outs for experimental licenses, and dual-use policy frameworks for civilian and defense 6G. Technological trends include AI-native base stations, open RAN adoption, and integration of quantum-resistant security modules. A U.S. telecom firm launched a real-time terahertz small cell prototype delivering sub-millisecond handoffs across high density campuses. Enterprise segments in healthcare and finance lead adoption for ultra secure low-latency links, while consumer behavior leans toward early access trials in urban tech hubs.

Why do standards and regulation drive European deployment dynamics?

Europe held roughly 25% share of trial volumes in 2024, with Germany, UK, and France leading in testbeds. Regulatory bodies like the European Commission are pushing advanced AI transparency, content verification, and energy efficiency mandates on telecom operators. Sustainability initiatives embed energy harvesting and sleep-mode architecture in future 6G designs across the EU. European firms adopt explainable AI control planes and certified interoperability. A German network vendor deployed a campus 6G node with integrated environmental sensing in 2024. European consumers emphasize transparency and trust, demanding clarity about synthetic and AI-enabled network behavior in line with privacy and ethical regimes.

What role do innovation hubs and scale play in adoption momentum?

Asia-Pacific stood second in global 6G volume in 2024, representing about 23% of early trials. Top consuming countries include China, India, Japan, and South Korea. Infrastructure trends emphasize large-scale manufacturing of terahertz modules, expansion of high speed fiber backhaul, and cloud-edge integration. Innovation hubs in Shenzhen, Seoul, and Bengaluru support teleport labs and AI-based R&D centers. Local players in China have deployed thousands of distributed test nodes for joint sensing & communication experiments. Consumer behavior is mobile-centric, with e-commerce firms and video platforms pushing latency-sensitive services that demand 6G performance in urban markets.

How are localization and incentives influencing regional uptake?

South America includes key countries such as Brazil and Argentina, contributing an estimated 5–8% of global 6G trial activity. Infrastructure funding is emerging through public-private partnerships in digital connectivity programs. Energy sector trends also drive interest in combining 6G with smart grid monitoring. Government incentives in Brazil support domestic R&D and spectrum testing. A regional telecom provider began trialing 6G UAV links for remote areas. Demand is linked to media localization, language support, and streaming services suited to local markets, driving test deployments of multicountry ML models.

How are modernization priorities shaping growth in emerging markets?

Middle East & Africa accounted for roughly 4–6% of 6G test deployments in 2024. Major growth countries include UAE, South Africa, Saudi Arabia, and Nigeria. Demand intersects with oil & gas digitization, smart infrastructure, and public safety communications. Technological modernization includes investment in satellite backhaul, urban small cell grids, and private 6G networks for industrial zones. Local vendors are partnering with global firms to host edge nodes in Dubai and Johannesburg. Consumer behavior prioritizes connectivity for smart city apps, virtual experiences, and government services in urban corridors, while rural uptake awaits infrastructure scale.

United States — ~ 30–35% share in global 6G trials; dominance rooted in high R&D investment, global telecom OEM strength, and regulatory support.

China — ~ 18–22% share globally; strong due to industrial scale, national 6G standards development, and massive pilot deployment programs.

The competitive landscape of the 6G Network market is evolving amid a fragmented yet gradually consolidating ecosystem. Over 60 active players—including large telecom OEMs, chipset vendors, systems integrators, and specialized startups—are engaged in 6G R&D, trials, and early deployments. The top 5 companies hold an estimated 50–60% combined influence, leveraging lead in patents, standardization, and alliances. Strategic moves include joint ventures (e.g., NVIDIA collaborating with T-Mobile, Cisco, MITRE on AI-native 6G stack), product launches of terahertz radios, and mergers to acquire IP or software assets. Some firms are launching open RAN or modular 6G modules to enable interoperability. Innovation trends shaping competition include AI orchestration platforms, integrated sensing & communication (ISAC) stacks, model compression frameworks, quantum-resilient encryption, and cloud-native disaggregated RAN architectures. Smaller players compete by focusing on edge compute nodes, network virtualization, or application verticals (e.g. industrial IoT, vehicle networks). As standardization advances, early adopters may gain first-mover advantages. The market is neither fully monopolistic nor overly fragmented: leading players dominate core infrastructure and chipset layers, while niche innovators occupy adjacencies. Competitive pressures center on spectrum rights, software differentiation, open interfaces, and energy-efficient designs.

Huawei

Qualcomm

ZTE

Intel

MediaTek

6G network technology is being shaped by a convergence of advanced radio hardware, AI-native processing, sensing, virtualization, and secure architectures. At the radio front, terahertz and sub-THz transceivers push spectrum into multi-hundred gigahertz bands, while massive multi-antenna arrays support beamforming for ultra-high throughput links. Integrated sensing & communication (ISAC) enables the same waveform to carry data and sense the environment (radar, localization), increasing spectral efficiency. AI orchestration and pervasive intelligence embed deep learning models at base stations and core, enabling self-optimizing control loops for load balancing, fault prediction, and interference mitigation. Network virtualization—via network slicing, digital twins, and holistic virtualization—allows sharing of infrastructure across services, dynamically adapting resource allocation. Secure architectures incorporate post-quantum encryption, identity attestation, and blockchain or distributed ledger schemes to maintain trust and provenance. Edge compute and distributed intelligence shift critical processing closer to endpoints, reducing latency and backhaul demands. Model compression, pruning, and hardware-aware design reduce power and footprint. Interoperability technologies, open RAN frameworks, and modular network building blocks accelerate vendor integration and deployment flexibility. Collectively, these technologies will enable 6G to realize ultra-reliable, ultra-low-latency, and context-aware connectivity across verticals.

• In March 2025, NVIDIA announced a collaboration with T-Mobile, Cisco, MITRE, and Booz Allen Hamilton to co-develop AI-native wireless network stack for 6G using the NVIDIA AI Aerial platform. Source: www.nvidianews.nvidia.com

• In 2024, Europe launched five major 6G research projects funded at €42.7 million focusing on sustainability, resilience, and inclusive innovation in next-gen networks. Source: www.6gflagship.com

• In 2023, Samsung, Ericsson, and Nokia formalized research agreements leveraging FCC-allocated 6G spectrum to accelerate development of terahertz air interfaces and advanced MIMO. Source: greyb.com

• In 2024, Qualcomm revealed plans to support pre-commercial 6G devices by 2028, aligning chipset roadmaps with next-generation connectivity and advanced AI integration. Source: techradar.com

The scope of the 6G Network Market Report encompasses an extensive evaluation of next-generation communication technologies, infrastructure evolution, and strategic opportunities shaping the transition from 5G to 6G connectivity. It covers detailed segmentation by Type, Application, End-User, and Geography, providing quantitative and qualitative insights across more than 25 national markets within North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report examines the ecosystem comprising telecom operators, chipset designers, hardware manufacturers, software providers, and cloud infrastructure players that collectively enable 6G deployment. By Type, the analysis explores terahertz communication modules, optical wireless links, edge-integrated nodes, and AI-native network slices, reflecting the convergence of hardware and intelligence. By Application, coverage spans smart cities, industrial automation, healthcare telepresence, immersive media, and connected mobility solutions, identifying key demand centers driving early commercialization. The End-User scope evaluates adoption trends across telecommunications, automotive, manufacturing, defense, and consumer electronics industries. Regionally, the report benchmarks innovation intensity, spectrum allocation strategies, R&D investments, and policy frameworks supporting 6G trials. Technological coverage extends to AI-driven orchestration, integrated sensing and communication (ISAC), quantum-safe security, network virtualization, and edge-cloud convergence. The report further identifies niche opportunities such as 6G-enabled robotics, holographic communication, and energy-efficient network fabrics, offering a forward-looking view for investors, policymakers, and industry leaders guiding digital transformation agendas.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 6,240.6 Million |

|

Market Revenue in 2032 |

USD 48,154.4 Million |

|

CAGR (2025 - 2032) |

29.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nokia, Samsung Electronics, Ericsson, Huawei, Qualcomm, ZTE, Intel, MediaTek |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |