Reports

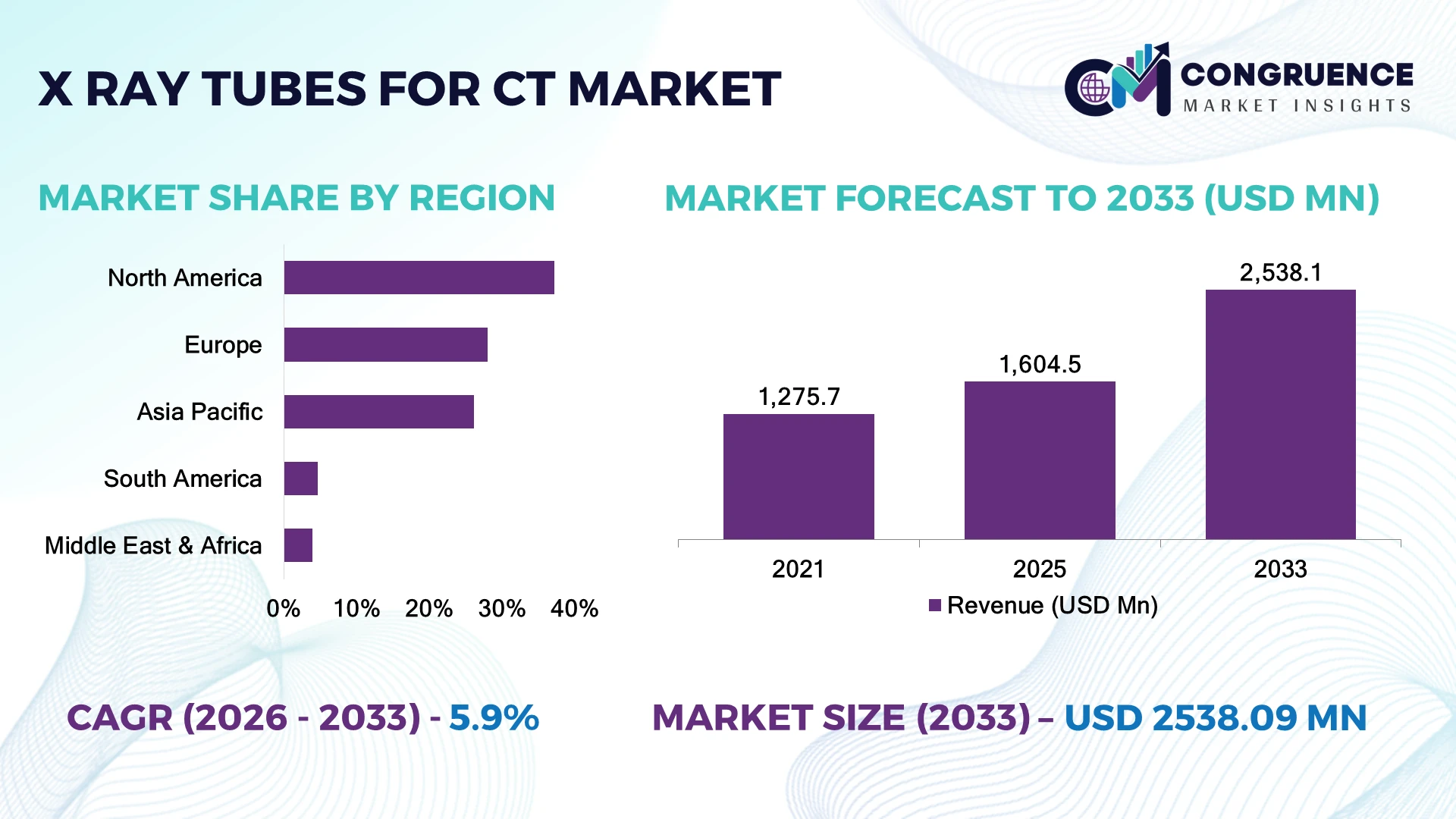

The Global X-ray tubes for CT Market was valued at USD 1,604.5 Million in 2025 and is anticipated to reach a value of USD 2,538.1 Million by 2033 expanding at a CAGR of 5.9% between 2026 and 2033. Growing deployment of high-slice CT scanners, expanding diagnostic imaging capacity, and rising replacement demand for high-heat-capacity X-ray tubes are accelerating market expansion across healthcare systems.

The United States dominates the global X-ray tubes for CT market with approximately 33% share, supported by advanced imaging infrastructure, continuous hospital investments, and widespread adoption of AI-enabled CT platforms. More than 68% of tertiary hospitals operate multi-slice CT systems using premium X-ray tube technologies, compared with Japan's stronger focus on compact high-utilization scanners. Ongoing healthcare modernization following post-pandemic diagnostic investments and resilient medical device supply-chain strategies further reinforce U.S. leadership.

Manufacturers prioritizing long-life tube performance, faster replacement cycles, and AI-compatible CT platforms will secure stronger positions in premium diagnostic imaging markets.

Market Size & Growth: USD 1,604.5 Million in 2025 reaching USD 2,538.1 Million by 2033 at 5.9% CAGR, driven by advanced CT imaging upgrades.

Top Growth Drivers: Rising CT procedures (+16%), AI-assisted diagnostics (+21%), hospital modernization (+18%).

Short-Term Forecast: By 2028, tube lifespan improves nearly 15% while maintenance downtime declines 12%.

Emerging Technologies: Liquid-metal bearings, AI calibration, and advanced cooling improve imaging stability by approximately 18%.

Regional Leaders: North America, Asia-Pacific, and Europe together exceed USD 1.9 Billion demand with expanding hospital installations.

Consumer/End-User Trends: Nearly 62% of new procurement favors high-heat-capacity replacement tubes for premium CT scanners.

Pilot/Case Example: A 2026 hospital imaging upgrade reduced scanner downtime by 20% through predictive tube monitoring.

Competitive Landscape: Top suppliers control nearly 58% share, led by Canon Electron Tubes, Siemens Healthineers, GE HealthCare, and Philips.

Regulatory & ESG Impact: Energy-efficient tube designs reduce cooling requirements by approximately 14%.

Investment & Funding: More than USD 700 Million supports manufacturing expansion and advanced imaging component localization.

Innovation & Future Outlook: AI-enabled predictive maintenance and next-generation rotating anode technologies strengthen long-term diagnostic performance.

The X-ray tubes for CT market is benefiting from rising demand across oncology, cardiology, trauma imaging, and emergency diagnostics as healthcare providers prioritize higher scanner utilization. Advanced liquid-metal bearing technology and predictive tube monitoring improve operational efficiency by nearly 18%, while regional medical equipment localization initiatives strengthen supply resilience. These developments establish a solid foundation for the strategic market assessment that follows.

The X-ray tubes for CT market has become strategically important as healthcare providers expand diagnostic capacity while improving scanner availability and imaging precision. Hospital modernization programs, aging populations, and increasing demand for rapid emergency diagnostics are reshaping procurement priorities. Healthcare systems are increasingly replacing aging CT platforms with AI-enabled imaging systems capable of supporting higher patient throughput and predictive maintenance.

Modern liquid-metal bearing X-ray tubes deliver approximately 20% longer operational life than conventional ball-bearing designs while reducing heat-related performance degradation by nearly 15%. North America leads premium technology deployment through advanced hospital infrastructure, whereas Asia-Pacific records faster installation volumes driven by expanding diagnostic networks and domestic manufacturing investments. More than 55% of newly installed high-end CT systems now incorporate intelligent performance monitoring for proactive maintenance.

Manufacturers are expanding localized production, collaborating with imaging system developers, and integrating digital service platforms to improve equipment uptime. A practical example is the deployment of predictive monitoring software that schedules tube replacement before failure, reducing unexpected scanner outages. Through 2026–2028, organizations combining high-performance tube engineering, AI-enabled lifecycle management, and resilient supply chains will achieve stronger competitive positioning while maximizing operational efficiency across advanced diagnostic imaging environments.

Expanding deployment of 128-slice, 256-slice, and premium CT systems remains the strongest growth driver for X-ray tubes for CT. More than 60% of newly procured hospital CT scanners now prioritize high-heat-capacity tubes, while predictive maintenance has reduced unplanned scanner downtime by nearly 18%. In the United States, healthcare infrastructure modernization and expanded outpatient imaging networks continue accelerating replacement demand for premium X-ray tubes. Higher imaging volumes increase tube wear, shortening replacement cycles and encouraging adoption of advanced liquid-metal bearing technologies. Manufacturers are responding by expanding localized production, investing in higher-capacity rotating anode designs, and collaborating with CT OEMs to improve lifecycle performance. A notable strategic shift is the integration of AI-based tube health monitoring, enabling proactive replacement planning and improving equipment utilization across high-throughput diagnostic centers.

Production of CT X-ray tubes depends on precision components including tungsten targets, high-performance bearings, vacuum assemblies, and specialized ceramics, creating supply constraints during manufacturing disruptions. Raw material costs have fluctuated by approximately 15% over recent procurement cycles, while premium replacement tubes account for nearly 35% of total CT maintenance expenditure in advanced hospitals. Japan and Germany remain important manufacturing hubs for critical imaging components, increasing supply-chain concentration. Extended procurement timelines delay equipment servicing, reducing scanner availability and increasing operating costs for healthcare providers. Manufacturers are mitigating these constraints through multi-source procurement, regional component localization, and long-term supplier agreements. Strategic inventory planning has become a competitive differentiator, improving delivery reliability while protecting service contracts against component shortages.

Integration of AI-driven diagnostics with intelligent tube lifecycle management is creating significant opportunities beyond conventional replacement demand. Predictive maintenance platforms improve tube utilization by nearly 20%, while advanced cooling technologies extend operational life by approximately 17%. China is rapidly expanding domestic CT manufacturing capacity, encouraging suppliers to establish localized production and technology partnerships. Emerging photon-counting CT systems and digital service platforms are creating demand for next-generation high-output X-ray tubes capable of supporting greater imaging precision. Manufacturers are increasing R&D investment in enhanced thermal management, smart diagnostics, and modular tube architectures to improve upgrade flexibility. A distinctive opportunity lies in subscription-based lifecycle management services that combine hardware, predictive analytics, and remote monitoring to reduce total ownership costs for hospitals.

Delivering higher imaging performance while maintaining long operational life remains the industry's most significant execution challenge. Premium CT systems operate up to 25% more frequently than conventional scanners, increasing thermal stress and accelerating component fatigue. Integration of AI-enabled imaging workflows also demands consistent tube output and precise calibration throughout extended operating cycles. Hospitals expect minimal service interruptions, making reliability a decisive purchasing criterion. Manufacturers must continue investing in advanced cooling systems, high-durability materials, digital monitoring software, and collaborative engineering with scanner manufacturers to maintain deployment consistency. The strategic challenge extends beyond hardware performance, requiring seamless integration between tube diagnostics, hospital asset management platforms, and predictive service networks to sustain long-term competitiveness.

AI-Based Tube Monitoring AI-enabled predictive maintenance systems are now deployed across nearly 42% of newly installed premium CT platforms, reducing unexpected equipment failures by approximately 18%. Hospitals increasingly integrate remote diagnostics into imaging workflows, while manufacturers expand digital service partnerships to maximize scanner uptime and optimize replacement scheduling.

Advanced Thermal Management Improved liquid-metal bearings, enhanced cooling systems, and optimized rotating anode technologies increase tube operating life by nearly 20% while lowering heat-related performance degradation by approximately 15%. Healthcare providers prioritize longer maintenance intervals, prompting manufacturers to accelerate investment in high-durability engineering and next-generation thermal designs.

Localized Manufacturing Expansion Supply-chain diversification has encouraged regional production investments, particularly in China and the United States, reducing component lead times by approximately 16%. Companies are strengthening supplier networks, expanding assembly capabilities, and increasing strategic inventory to improve delivery reliability amid continuing medical equipment localization initiatives.

Photon-Counting CT Adoption Growing deployment of photon-counting CT technology is reshaping X-ray tube development through higher precision imaging requirements and improved detector integration. Advanced system installations have increased by nearly 24% across leading diagnostic centers, encouraging manufacturers to redesign tube architectures for higher stability, greater energy efficiency, and enhanced compatibility with AI-assisted imaging platforms.

Rotating anode X-ray tubes account for approximately 72% market share, making them the dominant segment because of their superior heat dissipation, sustained high-power output, and compatibility with multi-slice and high-slice CT systems. Their ability to support continuous scanning with minimal thermal limitations makes them the preferred choice for hospitals performing high examination volumes. Metal ceramic X-ray tubes are the fastest-growing segment as healthcare providers increasingly prioritize longer operational life, improved vacuum stability, and reduced maintenance intervals. Manufacturers continue enhancing bearing systems and anode materials, extending operational lifespan by nearly 18% while lowering replacement frequency.

Glass X-ray tubes remain relevant in legacy CT installations and cost-sensitive healthcare environments where equipment replacement cycles are longer. Meanwhile, advanced rotating anode designs optimized for photon-counting CT and AI-enabled imaging platforms continue attracting R&D investment. More than 60% of newly installed premium CT systems incorporate high-capacity rotating anode technology, encouraging suppliers to expand manufacturing capacity, strengthen OEM partnerships, and accelerate innovation focused on higher thermal performance and lifecycle efficiency.

Industry observations published during 2025–2026 by leading medical imaging organizations indicate that high-heat-capacity rotating anode tube technologies remain the preferred configuration for advanced CT scanners because of their ability to support increasing imaging volumes and extended operating cycles.

Diagnostic imaging represents the largest application segment with an estimated 67% market share, supported by extensive use across emergency medicine, oncology, pulmonary assessment, and abdominal imaging. High patient throughput, preventive screening initiatives, and replacement of aging CT systems continue concentrating demand within routine diagnostic imaging. Cardiac CT is emerging as the fastest-growing application as healthcare providers increasingly adopt non-invasive cardiovascular imaging supported by AI-assisted reconstruction and high-resolution detector technologies. Improved scanning precision and shorter examination times are driving wider clinical adoption.

Neurology, oncology, trauma, and orthopedic imaging continue generating stable replacement demand because these specialties require consistent high-performance X-ray tubes capable of intensive daily operation. Cardiac CT procedures have increased by approximately 19%, while AI-supported image reconstruction has reduced repeat examinations by nearly 15% in advanced imaging centers. Manufacturers are optimizing tube performance for high-speed rotational scanning, improving thermal endurance, and collaborating with CT system developers to support expanding specialty imaging workflows.

Industry findings released during 2025–2026 by recognized radiology and diagnostic imaging organizations indicate continued expansion of advanced CT utilization for cardiovascular and oncology imaging as healthcare providers strengthen precision diagnostic capabilities.

Hospitals represent the largest end-user segment with an estimated 69% market share, driven by high patient volumes, comprehensive diagnostic departments, and continuous investment in premium CT infrastructure. Large healthcare systems operate multiple CT scanners requiring frequent tube replacement, creating sustained aftermarket demand. Independent diagnostic imaging centers are the fastest-growing end-user segment as outpatient imaging expands through shorter patient waiting times, lower examination costs, and increasing referrals from primary healthcare providers. Many facilities are upgrading to AI-enabled CT systems capable of supporting higher daily scan volumes with improved operational efficiency.

Academic medical centers continue investing in advanced CT technologies for clinical research and specialist imaging, while specialty clinics selectively adopt premium CT systems for oncology and cardiovascular applications. Independent imaging centers have increased advanced CT deployments by approximately 17%, while hospital-based predictive maintenance programs have reduced scanner downtime by nearly 16%. Manufacturers increasingly provide customized service contracts, lifecycle management programs, and OEM partnerships to strengthen customer retention and improve long-term equipment utilization across diverse healthcare providers.

According to industry observations published during 2025–2026 by leading radiology and medical imaging organizations, hospitals continue accounting for the majority of high-end CT scanner installations, while outpatient diagnostic imaging centers record the strongest growth in new multi-slice CT deployments.

North America accounted for the largest market share at 37.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

Advanced CT Replacement Cycles Sustain Regional Leadership

North America maintains its leadership through extensive deployment of high-slice CT scanners, strong replacement demand, and continuous investment in premium diagnostic imaging infrastructure. The region accounts for nearly 37.2% of global demand, supported by widespread adoption of AI-enabled CT systems and predictive equipment maintenance. Healthcare providers increasingly replace high-utilization X-ray tubes before end-of-life to maximize scanner availability. More than 65% of newly installed premium CT systems incorporate intelligent tube monitoring capabilities, improving maintenance scheduling and reducing operational interruptions. Manufacturers continue strengthening OEM collaborations, expanding service networks, and localizing inventory to accelerate replacement cycles. Enterprise demand remains concentrated among integrated hospital systems that prioritize lifecycle efficiency, imaging quality, and high equipment utilization.

United States Market Outlook: The United States remains the regional growth engine through its extensive installed base of multi-slice CT scanners, advanced hospital infrastructure, and strong replacement market. More than 68% of tertiary-care hospitals operate premium CT platforms requiring high-performance rotating anode tubes. Healthcare providers continue investing in predictive maintenance software, AI-assisted imaging platforms, and long-term OEM service agreements, supporting stable replacement demand while improving diagnostic throughput and operational efficiency.

Healthcare Modernization Supports Premium Imaging Adoption

Europe continues expanding demand through modernization of diagnostic imaging infrastructure, aging population demographics, and strong emphasis on high-quality radiology services. Approximately 28% of global CT X-ray tube demand originates from Europe, where replacement of legacy imaging systems remains a strategic priority. Hospitals increasingly adopt energy-efficient CT platforms and long-life X-ray tubes to improve operational sustainability while lowering maintenance frequency. Cross-border medical technology collaboration and advanced imaging research continue supporting innovation across premium CT platforms. Manufacturers strengthen localized service capabilities and engineering partnerships to improve equipment reliability and lifecycle performance.

Germany Market Outlook: Germany serves as Europe's leading market because of its advanced medical technology ecosystem, extensive hospital imaging capacity, and strong domestic engineering expertise. More than 60% of major university hospitals operate advanced multi-slice CT platforms requiring premium replacement tubes. Continuous investment in precision diagnostics, research hospitals, and medical device manufacturing reinforces Germany's strategic role in high-performance CT imaging.

Manufacturing Expansion and Healthcare Investment Accelerate Growth

Asia-Pacific is the fastest-growing regional market as healthcare infrastructure expands alongside domestic CT manufacturing and rising diagnostic capacity. China, Japan, South Korea, and India continue increasing procurement of advanced CT systems across public and private healthcare facilities. Nearly 40% of newly commissioned diagnostic imaging projects in emerging Asian markets include multi-slice CT installations. Manufacturers are expanding regional production, strengthening supply-chain resilience, and forming partnerships with domestic medical equipment producers to support growing replacement demand. Increasing localization also shortens delivery cycles and improves aftermarket support.

China Market Outlook: China leads regional expansion through rapid healthcare infrastructure investment, growing domestic CT manufacturing, and strong medical equipment localization initiatives. Large public hospitals continue upgrading to AI-enabled high-slice CT platforms, while domestic manufacturers expand premium component production. More than half of new tertiary hospital imaging procurements now emphasize advanced CT systems with extended tube lifecycle management, strengthening long-term demand for high-performance X-ray tubes.

Hospital Upgrades Drive Imaging Investments

South America is experiencing steady market expansion through public healthcare modernization, increasing diagnostic imaging access, and replacement of aging CT infrastructure. Brazil and neighboring countries continue investing in advanced radiology equipment despite procurement budget constraints. Approximately 18% of recently upgraded public diagnostic facilities have incorporated higher-capacity CT imaging systems, increasing demand for premium replacement tubes. Suppliers strengthen regional distribution partnerships and technical service capabilities to improve equipment uptime while balancing infrastructure limitations and import dependency.

Brazil Market Outlook: Brazil represents the largest national market because of its extensive hospital network, expanding private diagnostic sector, and growing investment in advanced imaging services. Major healthcare groups continue replacing aging CT systems with higher-performance platforms capable of supporting larger patient volumes. Regional service partnerships and localized maintenance capabilities are improving equipment availability while supporting greater adoption of premium replacement X-ray tubes.

Healthcare Infrastructure Investments Expand Diagnostic Capacity

The Middle East & Africa market is advancing through government-led healthcare modernization, specialty hospital expansion, and increasing deployment of advanced diagnostic imaging systems. Gulf countries continue investing in premium radiology infrastructure, while African healthcare providers prioritize expanding access to CT diagnostics. More than 20% of recently commissioned tertiary hospitals across Gulf Cooperation Council countries include high-end CT imaging suites equipped with advanced lifecycle management systems. Manufacturers increasingly support regional growth through technical training, distributor partnerships, and localized service operations.

Saudi Arabia Market Outlook: Saudi Arabia leads regional demand through large-scale healthcare transformation, hospital expansion, and strategic investment in advanced diagnostic technologies. National healthcare modernization initiatives continue increasing procurement of premium CT systems across public and private facilities. Healthcare providers emphasize long-life X-ray tube technologies, predictive maintenance programs, and digital imaging integration to improve equipment utilization while supporting expanding specialist diagnostic services.

The X-ray tubes for CT market is dominated by Canon Electron Tubes & Devices, Varex Imaging, Dunlee, Siemens Healthineers, and GE HealthCare, with integrated CT OEMs competing against specialized tube manufacturers while premium technology providers challenge cost-focused regional suppliers. The top five participants collectively account for approximately 67% of global market activity. Competition centers on tube lifespan, heat capacity, image stability, replacement turnaround, and OEM integration, with advanced liquid-metal bearing designs extending operational life by nearly 20% and predictive maintenance reducing unexpected downtime by approximately 18%. Companies compete through long-term OEM partnerships, manufacturing expansion, AI-enabled service platforms, and advanced thermal management innovation. The competitive landscape is shifting toward photon-counting CT compatibility and digitally connected lifecycle management, strengthening technology-led differentiation over price competition. High engineering complexity, stringent regulatory validation, and precision manufacturing requirements remain significant entry barriers. Success depends on delivering durable, high-performance X-ray tubes supported by reliable service networks, rapid replacement logistics, and continuous innovation.

Canon Electron Tubes & Devices Co., Ltd.

Varex Imaging Corporation

Dunlee

Siemens Healthineers AG

GE HealthCare

Koninklijke Philips N.V.

Canon Medical Systems Corporation

Fujifilm Holdings Corporation

United Imaging Healthcare

Shimadzu Corporation

Comet AG

Oxford Instruments plc

Advanced rotating anode technology, liquid-metal bearings, and high-capacity thermal management systems continue defining performance standards for CT X-ray tubes. These technologies improve heat dissipation by approximately 22% while extending operational life by nearly 20% compared with conventional bearing designs. Around 62% of newly installed premium CT systems now incorporate intelligent tube monitoring, enabling predictive maintenance and reducing unexpected scanner downtime. Healthcare providers benefit through higher equipment availability, improved patient throughput, and lower lifecycle servicing costs.

Photon-counting CT, AI-enabled tube health analytics, and advanced ceramic-metal vacuum assemblies represent the next phase of innovation. Compared with legacy ball-bearing tube systems, next-generation liquid-metal bearing designs provide nearly 25% longer operating life and reduce maintenance interventions by approximately 17%. Manufacturers integrating AI diagnostics with advanced tube engineering strengthen competitive differentiation by delivering higher reliability and improved service planning, particularly for hospitals operating high-utilization CT platforms.

Between 2026 and 2028, digital lifecycle management, enhanced thermal materials, and photon-counting CT compatibility will reshape investment priorities. Suppliers capable of combining advanced tube engineering, predictive maintenance software, and OEM integration will strengthen their competitive positions. Organizations investing now in intelligent tube technologies, localized manufacturing, and service optimization will capture growing replacement demand while supporting increasingly sophisticated diagnostic imaging environments.

March 2025: Canon Medical Systems received regulatory clearance for new AI enhancements to the Aquilion ONE / INSIGHT Edition CT platform, expanding advanced CT imaging capabilities and strengthening compatibility with next-generation imaging workflows. Source: Canon Inc.

November 2025: Canon Medical showcased its latest CT innovations at RSNA 2025, highlighting AI-driven reconstruction technologies and advanced CT platforms designed to improve image quality and clinical workflow efficiency. Source: Canon Inc.

November 2025: Dunlee released a technical white paper demonstrating that stable ultra-small focal spot X-ray tube technology significantly enhances Ultra-High-Resolution CT and Photon-Counting CT image quality, reinforcing next-generation tube development priorities. Source: Philips

November 2025: Varex Imaging reported strong global CT tube sales momentum, with Medical segment revenue increasing 5% year over year, reflecting sustained replacement demand and continued investment in advanced CT imaging systems. Source: Varex Imaging

The report provides comprehensive assessment of the global X-ray tubes for CT market across tube technologies, clinical applications, end-user categories, and major regional markets. It evaluates rotating anode, metal ceramic, and glass tube technologies together with deployment across diagnostic imaging, cardiology, oncology, neurology, trauma, and specialized CT applications. The study also examines adoption patterns among hospitals, diagnostic imaging centers, academic institutions, and specialty healthcare providers. More than 25 technology and deployment indicators are analyzed to identify operational trends, equipment replacement cycles, and evolving purchasing priorities.

The report further delivers competitive benchmarking, regional manufacturing analysis, technology roadmaps, and strategic business intelligence supporting market expansion between 2026 and 2033. It evaluates AI-enabled predictive maintenance, photon-counting CT compatibility, advanced thermal management, and lifecycle optimization while highlighting deployment trends, replacement demand, and enterprise investment strategies. The analysis supports product development, manufacturing planning, competitive positioning, partnership evaluation, and long-term investment decisions across the global CT imaging ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,604.5 Million |

|

Market Revenue in 2033 |

USD 2,538.1 Million |

|

CAGR (2026 - 2033) |

5.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Canon Electron Tubes & Devices Co., Ltd., Varex Imaging Corporation, Dunlee, Siemens Healthineers AG, GE HealthCare, Koninklijke Philips N.V., Canon Medical Systems Corporation, Fujifilm Holdings Corporation, United Imaging Healthcare, Shimadzu Corporation, Comet AG, Oxford Instruments plc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |