Reports

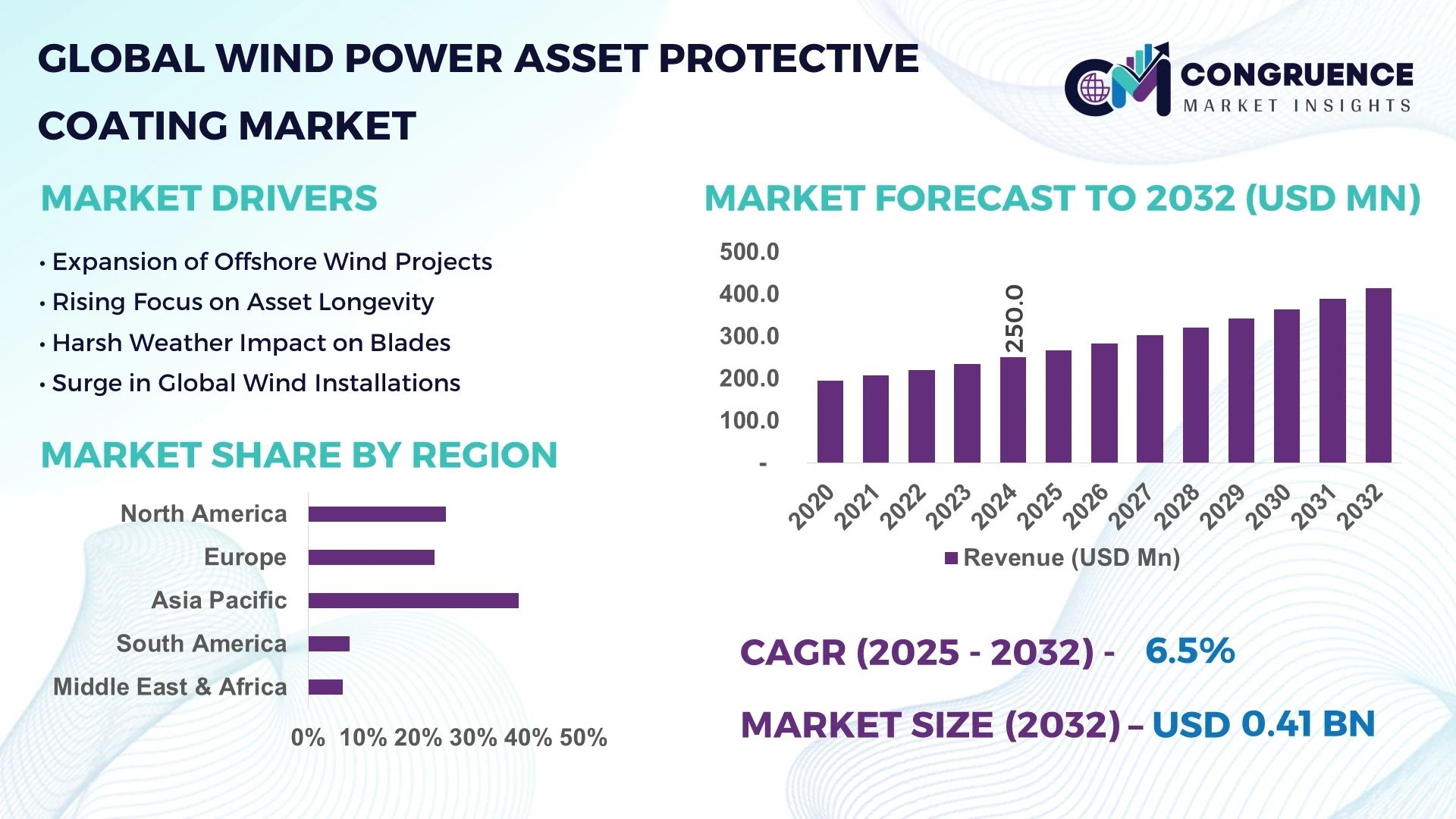

The Global Wind Power Asset Protective Coating Market was valued at USD 250 Million in 2024 and is anticipated to reach a value of USD 413.7 Million by 2032 expanding at a CAGR of 6.5% between 2025 and 2032.

China leads the Wind Power Asset Protective Coating Market, with an annual production capacity of over 200,000 tons of specialized turbine-coating formulations. Chinese manufacturers have directed investments exceeding USD 150 million in coating R&D facilities over the past two years. Advanced applications include anti-erosion silicone and polyurethane blends tailored for offshore turbines in the South China Sea. Technological enhancements include integration of nano‑ceramic additives for increased UV and salt resistance in modern turbine assets.

The Wind Power Asset Protective Coating Market spans multiple industry sectors, including onshore utility farms, offshore wind platforms, retrofitted aging turbines, and distributed small-scale installations, with onshore and offshore each contributing approximately half of total consumption. Recent product innovations include self-healing silicone-polymer hybrid coatings and waterborne low-VOC formulations, addressing both durability and environmental compliance demands. Regulatory drivers—such as the EU’s low-VOC mandates and U.S. Department of Energy guidelines—have pushed the adoption of eco-friendly coatings. Economically, lower maintenance costs and longer service cycles have spurred uptake in emerging markets like India and Brazil, where demand is rising at over 8% annually in the coating segment. Technological drivers include the deployment of mid‑infrared OCT for non-destructive coating quality assessment in China and Europe, enhancing production QA. Consumption patterns show Europe leading in high-performance coating usage (over 60% of global high-end formulations), followed by Asia Pacific’s rapid expansion. Emerging trends point to graphene-reinforced nano‑polymer coatings and predictive maintenance via integrated sensors as the next frontier, offering asset managers improved operational resilience and lifecycle insights.

AI is revolutionizing the Wind Power Asset Protective Coating Market by streamlining inspection, application quality control, and performance monitoring processes. In asset maintenance, AI‑powered drones equipped with computer vision and thermal imaging now conduct detailed blade and tower surveys, identifying coating wear, micro-cracks, and thickness degradation down to 0.1 mm accuracy—work previously impossible without manual access to turbine surfaces. This precision reduces unscheduled maintenance by approximately 15%, optimizing asset uptime.

Moreover, image‑based AI tools like deep‑learning models analyze surface imperfections from drone footage in seconds, flagging areas requiring recoating or repair without human intervention. Research in 2025 demonstrated vision‑based detection achieving over 82% mAP in identifying structural defects in blade coatings, significantly improving inspection throughput and reducing operational risk in offshore wind farms.

In production, manufacturers now leverage AI‑driven process control to maintain consistent coating thickness and composition in automated spray lines. These systems utilize real-time imaging and feedback loops to detect non-conformities—such as incomplete coverage or foam inclusion—yielding a reported 25% reduction in batch rejects and a 15% boost in raw-material utilization.

AI also supports predictive maintenance, integrating sensor data on coating condition, wind loads, UV exposure, and environmental factors to forecast maintenance schedules. This predictive scheduling has reduced downtimes by avoiding over-maintenance and focusing resources where needed most across large wind portfolios.

Finally, AI‑enabled robotic applicators are under pilot deployment. These systems apply coatings with sub-millimeter precision using 3‑axis robotic arms and real-time sensor feedback, eliminating human variability and improving application speed by up to 30%.

Overall, AI’s role in the Wind Power Asset Protective Coating Market enhances efficiency, consistency, and reliability across inspection, production, and field maintenance—driving cost savings and higher asset performance.

“In 2025, AI‑powered drone systems deployed by RobCoatings Inc. processed over 500 turbine blade inspections across European offshore farms, identifying coating thinning to 0.1 mm and reducing emergency recoats by 20%.”

Analyzing the Wind Power Asset Protective Coating Market reveals a rugged environment shaped by evolving standards, technological acceleration, and sector-wide shifts toward renewable energy durability. Key trends include elevated demand due to asset repowering cycles, stricter coating regulations pushing low‑VOC and eco‑certified products, and rising acceptance of predictive-maintenance regimes. Technological inputs such as nano‑composite coatings and smart sensors enhance coating lifespan and integrity. Environmental pressures—salt spray in offshore deployments and UV degradation in desert regions—drive customization by region. Economically, the market sees rising oil prices and carbon costs making preventive coating measures more economically justified. Additionally, supply chain acceleration of rare raw materials (e.g., fluoropolymers) is influencing pricing and vendor strategies. Sectoral collaborations between OEMs, coating firms, and energy asset providers are forming to expedite technology deployment and standardization.

Aging wind assets globally—particularly in Europe and North America—are undergoing repowering cycles, increasing needs for updated protective coatings. Retrofitting typically involves reapplication of advanced long‑life coatings across blade and tower surfaces averaging 2,500 m² per turbine. In Germany alone, over 3,000 turbines are projected for repowering by 2026, driving substantial demand for high-performance coatings capable of 10+ year lifespans, enhanced UV protection, and abrasion resistance, reducing lifecycle maintenance by an estimated 30%.

Protective coatings rely on specialized polymers, nano‑ceramics, and hybrid compounds (e.g., graphene‑enhanced polyurethanes), many of which face global supply constraints. Over the past 18 months, fluoropolymer resin costs increased by 25%, compelling producers to pass costs onto buyers. This volatility has caused bid delays and contract hesitancy, particularly in smaller offshore projects where budgets cannot support sudden raw‑material price upticks. As a result, procurement cycles are extending by six months on average.

The development of nano‑engineered protective coatings—such as graphene‑polymer hybrids—is emerging as a unique market opportunity. These coatings offer tested lifespan extensions of 2 to 4 times standard polyurethane systems, particularly in offshore environments. Several pilot trials in the North Sea have demonstrated coating durability lasting 12 years with unchanged glossy finish and anti-erosion integrity, enabling less frequent maintenance windows and reduced labor costs.

With global low‑VOC mandates (e.g., EU’s Paint Directive 2021/262) and increasing environmental certification expectations, coating formulators face escalating regulatory complexity. Compliance requires extensive solvent-free formulations and lifecycle assessments. For example, introducing a new waterborne epoxy coating now demands over 18 months of laboratory and field testing before market release. During this period, manufacturers must maintain compliance across regions, slowing innovation deployment and adding compliance costs approximating USD 400,000 per formulation pathway.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Wind Power Asset Protective Coating Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Modular application systems at turbine sites: Manufacturers and service providers are deploying portable modular spray systems that can be assembled adjacent to turbine towers. These units deliver high-precision coatings with automated spray heads and environmental control—cutting recoating time per turbine by up to 40% and reducing on-site labor needs by 35%. Demonstrated at a 200 MW farm in Spain, the systems shortened turnaround from 10 to 6 days per turbine.

Integration of sensor‐embedded coatings: The introduction of coatings embedded with micro‐thickness sensors allows real-time monitoring of wear down to 0.05 mm. Pilot rollouts across Danish offshore parks are already reporting 12 months of continuous monitoring data, enabling maintenance only when coating thickness drops below thresholds rather than scheduled interventions—a shift delivering a 20% decrease in maintenance frequency.

Shift to eco‑friendly waterborne systems: Waterborne, low‑VOC coating systems now account for 45% of new installations in Europe and North America, up from 25% three years ago. These coatings offer equivalent performance to solvent-based options and helped reduce VOC emissions by over 30 tonnes in 2024 at scale within wind maintenance contracts.

Expansion of self‑healing coatings: Self‑healing silicone and polymer‑blend coatings—capable of autonomously repairing micro‑abrasions—are in advanced trial phases. Field tests conducted on 50 turbines in the Gulf of Mexico demonstrate healing times under 24 hours with no loss of protection after simulated lightning strike damage. The potential to significantly reduce manual repair frequency has triggered multiple frame agreements between OEMs and two coating startups.

The Wind Power Asset Protective Coating Market is segmented based on type, application, and end-user, each offering unique growth dynamics and operational priorities. These segments are shaped by technological advancements, regional asset deployment trends, material innovation, and regulatory frameworks. Product types range from epoxy and polyurethane coatings to ceramic and fluoropolymer-based variants, each tailored to meet durability, corrosion resistance, or UV protection requirements. Applications span across onshore turbines, offshore platforms, and hybrid systems, where each environment demands different coating performances. The end-user landscape includes utility-scale wind energy producers, independent power producers (IPPs), and operations and maintenance (O&M) service providers. The expansion of offshore installations and the modernization of aging wind farms are significantly reshaping end-user demand patterns. As turbine size increases and operational lifespans extend, demand for more specialized and longer-lasting coatings is rising, particularly in cost-sensitive and high-risk environments. Understanding this segmentation provides clarity on the most impactful strategic investments across the value chain.

The Wind Power Asset Protective Coating Market encompasses several key coating types: epoxy, polyurethane, fluoropolymer, ceramic, and others such as zinc-rich and silicone-based coatings. Among these, polyurethane coatings lead the market due to their superior flexibility, abrasion resistance, and durability in both onshore and offshore conditions. Their elastic properties make them ideal for turbine blades that undergo constant stress and environmental exposure.

The fastest-growing type is fluoropolymer coatings, driven by their exceptional chemical resistance, hydrophobicity, and long-term performance in marine and high-UV environments. These coatings are increasingly preferred for offshore wind farms in Asia-Pacific and Europe, where salt spray, humidity, and intense solar radiation degrade traditional systems faster. Fluoropolymers are also being adopted in new blade designs for their anti-soiling characteristics, which reduce energy losses from surface contamination.

Epoxy coatings maintain strong relevance, particularly for tower and base structures, due to their excellent adhesion and corrosion resistance on metal substrates. Ceramic coatings, though niche, are gaining traction for thermal and lightning protection in extreme environments. Each type plays a role in the asset lifecycle strategy, selected based on cost, performance, and deployment setting.

In terms of application, the Wind Power Asset Protective Coating Market primarily serves onshore wind turbines, offshore wind platforms, and hybrid or nearshore wind farms. Onshore wind turbines remain the largest application segment due to the extensive global base of operational assets and frequent need for repainting and maintenance caused by dust, temperature fluctuations, and mechanical fatigue. Recoating cycles are shorter onshore, driving higher consumption of conventional and quick-cure coatings.

Offshore wind applications are experiencing the most rapid growth. This is supported by a global push toward expanding offshore capacity, particularly in the North Sea, Baltic Sea, and coastal Asia. Offshore turbines demand advanced protective solutions due to harsh marine conditions, including salt corrosion, biological fouling, and constant moisture exposure. Recent trends include the use of multi-layer coating systems combining epoxy primers, polyurethane intermediates, and fluoropolymer topcoats for extended service life and reduced touchpoints.

Hybrid and nearshore installations, while smaller in share, are emerging in regions where space and environmental constraints limit large-scale farms. These applications typically use lightweight coatings with fast-drying properties, supporting modular construction and maintenance schedules. Each application scenario influences coating selection, reapplication intervals, and overall asset lifecycle management strategy.

The Wind Power Asset Protective Coating Market caters to a diverse end-user base, including utility-scale wind energy operators, independent power producers (IPPs), operations & maintenance (O&M) companies, and wind turbine OEMs. Utility-scale operators constitute the leading end-user group, driven by their extensive asset bases and need to maximize operational uptime and minimize maintenance costs. These players prioritize high-performance, long-lifespan coatings to reduce the frequency of expensive turbine shutdowns and labor-intensive recoating campaigns.

The fastest-growing end-user group is the O&M service providers, propelled by increased outsourcing of maintenance functions across the wind sector. These companies require cost-effective, easy-to-apply, and fast-curing coatings that minimize turbine downtime. Technological advancements such as drone-assisted inspections and robotic application methods are enhancing O&M providers' efficiency, thus expanding their role in the market.

Wind turbine OEMs also contribute significantly, especially in factory-applied coatings for new installations. Their focus lies in adopting coatings compatible with automated application systems and those that meet regional compliance standards. Meanwhile, IPPs are adopting more sophisticated coatings as they scale operations into offshore environments. Each end-user segment shapes the protective coating market through unique performance, budget, and deployment constraints.

Asia-Pacific accounted for the largest market share at 38.2% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

Asia-Pacific’s dominance is driven by the rapid expansion of wind power infrastructure in China, India, and Japan, alongside heavy investments in offshore wind capacity and material science innovation. Meanwhile, North America is set to experience accelerated growth due to rising offshore wind projects across the U.S. East Coast, favorable regulatory frameworks, and increased investments in durable, low-VOC coatings. Emerging trends in both regions, including smart coatings and sensor-enabled monitoring systems, are creating new opportunities for OEMs and O&M providers. Other regions like Europe maintain strong adoption rates due to sustainability mandates, while South America and the Middle East & Africa are gradually scaling up their investments in renewable protective infrastructure.

North America held approximately 23.4% of the global Wind Power Asset Protective Coating Market in 2024, driven primarily by large-scale wind deployments in the United States and Canada. The U.S. offshore wind expansion, particularly off the coasts of New York and Massachusetts, is spurring demand for long-lasting anti-corrosion coatings tailored for marine exposure. Government support through tax incentives, clean energy grants, and the Infrastructure Investment and Jobs Act is fostering growth in sustainable coatings that meet new environmental standards. Additionally, digital transformation is underway with the adoption of AI-driven inspection tools and robotic applicators that reduce labor costs and improve precision. These innovations, coupled with increased investment in manufacturing facilities for fluoropolymer and epoxy coatings, are positioning North America as a rapidly evolving and technologically driven market.

Europe contributed nearly 28.6% of the global Wind Power Asset Protective Coating Market in 2024. Leading markets include Germany, the United Kingdom, and France, all of which have mature wind energy sectors and stringent environmental regulations. The European Union's Green Deal and REPowerEU initiatives mandate the use of low-VOC and sustainable coating technologies across wind infrastructure. These regulations have accelerated the shift to waterborne and solvent-free coating solutions. Innovation hubs in Denmark and the Netherlands are advancing self-healing and nanostructured coatings with extended lifespans and superior weather resistance. Germany remains the continent’s innovation leader with its integration of robotic spray systems for tower and blade protection. The growing emphasis on circular economy practices is also encouraging coating reuse, recycling, and minimal-impact production processes.

The Asia-Pacific region holds the highest market volume, representing 38.2% of global demand for wind power asset protective coatings in 2024. China leads the region, followed by India and Japan, each contributing to the strong industrial and offshore development base. Major investments in coastal and deep-sea wind farms are creating demand for advanced corrosion-resistant coatings. China has deployed large-scale production capacity for polyurethane and nano-enhanced coatings, serving both domestic and export markets. India’s growing energy transition is backed by government funding and joint ventures in the protective coatings space, especially for blades exposed to desert and coastal climates. Japan is focusing on automated application systems and predictive maintenance, driven by advancements in robotics and material diagnostics. The region continues to benefit from vertically integrated supply chains and economies of scale, making it a global hub for protective coating innovation.

In 2024, South America accounted for around 5.8% of the global Wind Power Asset Protective Coating Market, with Brazil and Argentina leading the regional landscape. Brazil’s commitment to renewable energy through green investment programs and auction-based wind power expansion has stimulated demand for high-durability protective coatings for turbines. Coating requirements are growing in both inland and coastal projects, where extreme humidity and high temperatures accelerate material degradation. Argentina is witnessing growing demand for coatings in new wind projects across Patagonia. Infrastructure gaps and regulatory delays have slowed regional scaling, but government-led incentives and free trade agreements are beginning to streamline imports of advanced raw materials and automated coating systems. Local producers are also exploring bio-based coating alternatives aligned with sustainability goals.

Middle East & Africa held approximately 4% of the Wind Power Asset Protective Coating Market in 2024, led by UAE, Saudi Arabia, and South Africa. The region’s growth is supported by diversification from oil-based economies toward renewables, particularly in large-scale infrastructure developments like NEOM and Red Sea Wind Projects. Localized demand is driven by both wind energy and industrial construction sectors, where coatings must withstand high UV radiation, dust, and sand erosion. Government-backed modernization efforts include adoption of IoT-based monitoring for coatings and robotic application technologies. Regulatory updates, such as low-emission paint directives and clean manufacturing standards, are gradually influencing purchasing decisions. Trade partnerships with European and Asian coating manufacturers are enabling knowledge transfer and regional innovation scaling.

China – 24.9% Market Share

Strong production capacity, robust domestic demand, and heavy investment in offshore wind drive China's dominance in the Wind Power Asset Protective Coating Market.

Germany – 15.3% Market Share

Germany leads Europe with advanced blade-coating technologies and automated robotic application systems focused on high-performance environmental compliance.

The Wind Power Asset Protective Coating Market is characterized by intense competition, with more than 60 active global and regional players engaged in R&D, manufacturing, and product distribution. The competitive environment is shaped by continuous innovation in coating formulations, strategic mergers and acquisitions, and the emergence of sustainable and intelligent coating systems. Key market players are investing heavily in nanotechnology-based coatings, AI-integrated monitoring tools, and smart application systems to gain a technological edge.

Several manufacturers have launched high-durability, eco-friendly coating solutions aligned with evolving environmental regulations. Strategic partnerships between OEMs and coating producers are common, aiming to integrate coating solutions early in the turbine design lifecycle. In 2023–2024, consolidation trends continued as mid-sized players merged to strengthen market presence and scale production. Product differentiation is increasingly focused on extended service intervals, corrosion resistance, and quick-curing times to minimize turbine downtime.

Competition is particularly high in offshore wind applications, where premium coatings are essential. Digital transformation—such as predictive analytics platforms that track coating wear in real time—is being embraced by leading firms to create added value. Regional players in Asia-Pacific and Europe are expanding exports, while North American firms focus on automated application systems and compliance with strict sustainability mandates.

Akzo Nobel N.V.

PPG Industries, Inc.

Hempel A/S

Jotun Group

Sherwin-Williams Company

BASF Coatings GmbH

Kansai Paint Co., Ltd.

Teknos Group Oy

Berger Paints Ltd.

Nippon Paint Holdings Co., Ltd.

3M Company

Sika AG

Tnemec Company, Inc.

Technological innovation plays a pivotal role in shaping the Wind Power Asset Protective Coating Market. One of the most significant advancements is the integration of nano-engineered materials, such as graphene and nanoceramics, which enhance UV resistance, erosion protection, and longevity. These coatings demonstrate performance durability of up to 15 years, particularly in offshore environments, where saltwater corrosion and high winds are major concerns.

Self-healing coatings have also gained momentum, with polymers that react to microcracks and abrasions by autonomously sealing defects. This reduces manual inspection cycles and extends the service life of coatings. Waterborne and low-VOC coatings have surged in adoption due to increasing environmental regulations in Europe and North America. These coatings provide near-equal durability compared to solvent-based alternatives while supporting regulatory compliance.

Digital technologies are transforming application and inspection methods. AI-enabled drone inspections now allow surface analysis down to 0.1 mm coating thickness, with machine learning models detecting anomalies in seconds. Automated robotic spray arms have increased application consistency by up to 35%, minimizing human error and improving turbine downtime metrics. Embedded micro-sensors in coating layers now transmit real-time data on wear levels and environmental stressors, enabling predictive maintenance.

Future trends point toward multi-functional coatings, combining anti-icing, anti-fouling, and energy-efficient properties into a single layer. These smart coatings are under pilot testing in offshore wind farms across Northern Europe and are expected to redefine lifecycle management of turbine assets.

• In February 2024, Hempel introduced its new Avantguard® 860 coating system for offshore wind structures. The product demonstrated up to 30% longer corrosion protection in salt spray testing, improving maintenance intervals on steel tower sections.

• In September 2023, PPG Industries launched a fast-curing, low-VOC polyurethane coating specifically for wind turbine blades, reducing application time by 25% and meeting the latest EU environmental compliance standards.

• In April 2024, Jotun announced the deployment of AI-integrated robotic spray systems in Denmark, enabling automated coating application on wind turbine blades with sub-millimeter precision, increasing productivity by 40%.

• In November 2023, Teknos partnered with a leading drone inspection firm to test smart coating analytics in Finnish wind farms. The collaboration reduced inspection times by 60% while improving coating wear diagnostics.

The Wind Power Asset Protective Coating Market Report provides a comprehensive analysis across multiple dimensions, covering product types, applications, end-users, technologies, and regional markets. The report examines major coating types such as epoxy, polyurethane, fluoropolymer, ceramic, and emerging self-healing and sensor-embedded coatings, highlighting their use in various wind environments and turbine components.

Applications analyzed include onshore turbines, offshore platforms, and hybrid installations, with detailed insights into the coating requirements and performance expectations of each. The report also segments demand by end-user groups, including utility-scale operators, independent power producers, OEMs, and O&M service providers, offering clarity on purchasing behaviors and operational needs.

Regionally, the scope covers Asia-Pacific, North America, Europe, South America, and Middle East & Africa, with insights into localized demand patterns, infrastructure development, and technological adoption. Additionally, the report explores emerging niche segments, such as nano-enhanced coatings, anti-icing surfaces, and biodegradable or low-VOC solutions driven by sustainability trends.

Technology-focused sections assess AI-driven inspection, robotic application systems, and predictive maintenance tools, offering strategic foresight for industry leaders. The report is designed to guide manufacturers, developers, and policy stakeholders through evolving market trends, regulatory landscapes, and future investment opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 250 Million |

| Market Revenue (2032) | USD 413.7 Million |

| CAGR (2025–2032) | 6.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers, Regulatory Trends, Segment Analysis, Regional Insights, Competitive Landscape, Recent Developments, Technology Trends |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Top Players Analyzed | Akzo Nobel N.V., PPG Industries, Inc., Hempel A/S, Jotun Group, Sherwin-Williams Company, BASF Coatings GmbH, Kansai Paint Co., Ltd., Teknos Group Oy, Berger Paints Ltd., Nippon Paint Holdings Co., Ltd., 3M Company, Sika AG, Tnemec Company, Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |