Reports

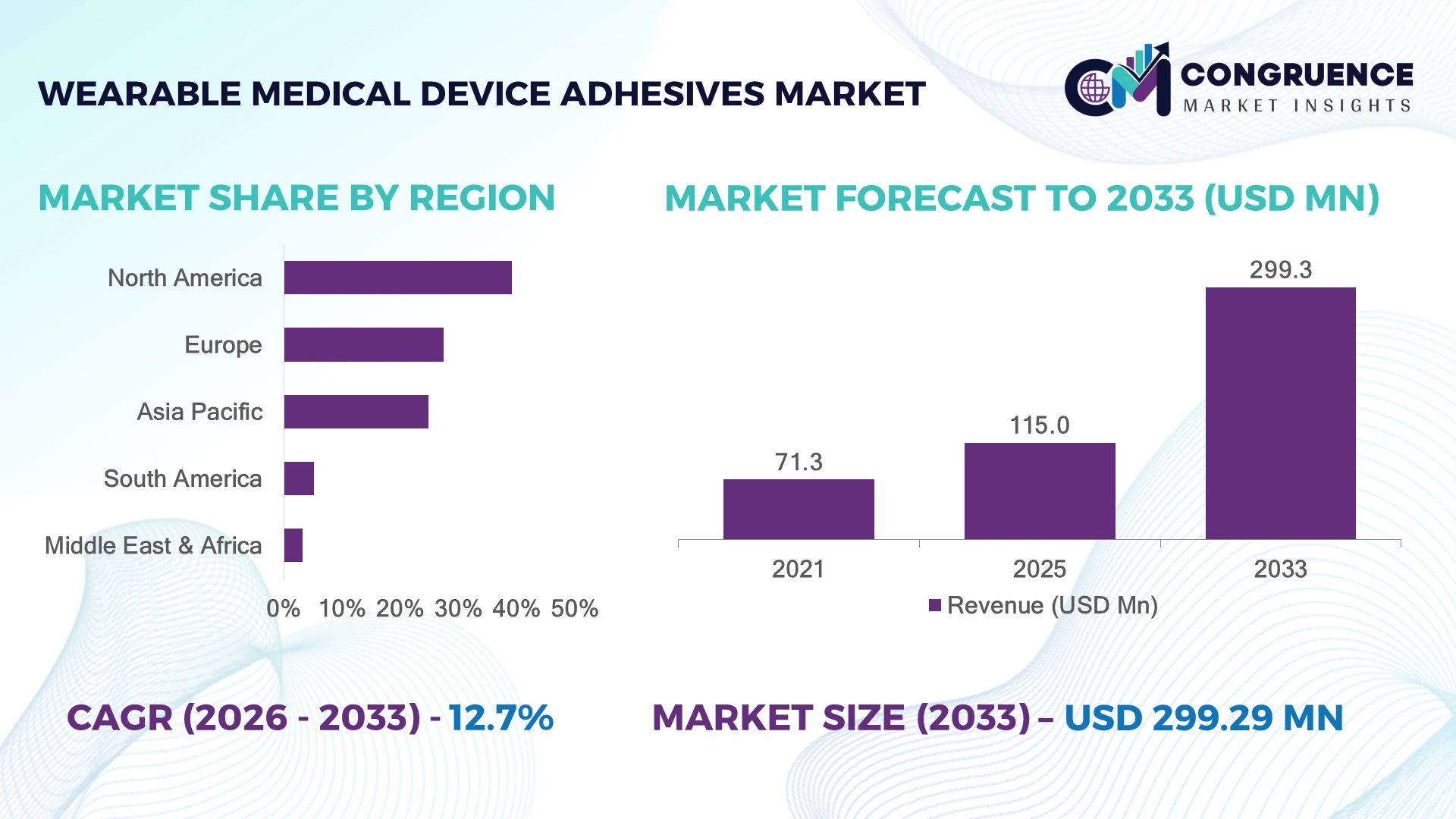

The Global Wearable Medical Device Adhesives Market was valued at USD 115.0 Million in 2025 and is anticipated to reach a value of USD 299.3 Million by 2033 expanding at a CAGR of 12.7% between 2026 and 2033. Continuous innovation in skin-friendly silicone and acrylic adhesive chemistries, coupled with expanding adoption of wearable glucose monitors, cardiac patches, and remote patient monitoring systems, is accelerating long-term market expansion.

The United States leads the global market with an estimated 38% share, supported by extensive deployment of continuous glucose monitoring devices, over 2,000 digital health companies, and strong FDA-backed wearable innovation programs, while Germany remains Europe's manufacturing hub with higher medical-grade adhesive production efficiency. The CHIPS and Science Act further strengthens domestic healthcare technology supply chains and advanced material development.

Manufacturers are prioritizing localized production, advanced adhesive formulations, and strategic healthcare partnerships to strengthen product differentiation and long-term competitive positioning.

Market Size & Growth: USD 115.0 Million (2025) to USD 299.3 Million (2033) at 12.7% CAGR, driven by rapid expansion of continuous health monitoring and advanced skin-safe adhesive technologies.

Top Growth Drivers: Remote patient monitoring adoption (+32%), wearable sensor integration (+28%), and silicone adhesive innovation (+24%) accelerate market momentum.

Short-Term Forecast: By 2028, skin adhesion durability improves by 20% while product replacement frequency declines by nearly 15%.

Emerging Technologies: AI-enabled health wearables, breathable silicone adhesives, antimicrobial coatings, and flexible printed electronics reshape next-generation devices.

Regional Leaders: North America (~USD 112 Million), Europe (~USD 78 Million), and Asia-Pacific (~USD 67 Million) benefit from digital healthcare expansion, localized production, and advanced manufacturing investments.

Consumer/End-User Trends: More than 58% of wearable medical device users prefer hypoallergenic, long-wear adhesives for multi-day monitoring applications.

Pilot/Case Example: In 2024, next-generation adhesive patches demonstrated approximately 25% stronger skin retention while reducing irritation by nearly 18% during extended wear.

Competitive Landscape: Henkel holds an estimated 15% market share alongside 3M, Avery Dennison, Dow, and Scapa as leading technology innovators.

Regulatory & ESG Impact: Solvent-free adhesive adoption exceeds 30%, supporting stricter environmental compliance and lower manufacturing emissions amid global supply-chain diversification.

Investment & Funding: More than USD 650 Million has supported manufacturing expansion, material innovation, and strategic partnerships across advanced wearable healthcare ecosystems.

Innovation & Future Outlook: Bio-based polymers, ultra-thin adhesive films, and smart skin-compatible materials strengthen product performance and long-term clinical reliability.

Wearable Medical Device Adhesives Market demand continues to strengthen across continuous glucose monitoring, cardiac monitoring, and remote patient care applications as manufacturers introduce breathable, hypoallergenic, and extended-wear adhesive technologies. More than 60% of new wearable healthcare platforms emphasize multi-day skin compatibility. Regional manufacturing expansion and stricter medical material compliance are also reshaping sourcing strategies, setting the foundation for broader strategic market development.

Wearable medical device adhesives have become strategically important as healthcare providers expand remote patient monitoring, home-based diagnostics, and connected care ecosystems. Competition increasingly depends on adhesive reliability, patient comfort, and compatibility with miniaturized wearable electronics. Supply-chain diversification across North America and Asia has encouraged manufacturers to localize specialty material production while reducing dependence on single-region sourcing for critical medical-grade polymers.

Modern silicone-based adhesive systems deliver nearly 30% longer wear duration than conventional acrylic alternatives while reducing skin irritation and lowering replacement frequency. North America remains the innovation leader through advanced wearable integration, whereas Asia-Pacific continues expanding production capacity with cost-efficient manufacturing and faster commercialization. Over the next two to three years, healthcare providers are expected to accelerate adoption of extended-wear monitoring devices as digital care pathways become standard clinical practice.

Companies are strengthening partnerships with wearable device manufacturers, investing in bio-compatible material research, and expanding regional manufacturing facilities to improve responsiveness and regulatory compliance. Recent deployments of multi-day glucose monitoring patches demonstrate how advanced adhesives improve patient adherence while simplifying device maintenance. Organizations that combine material innovation, resilient supply networks, and application-specific product development will secure stronger competitive positioning and long-term operational advantage in this evolving healthcare technology landscape.

The rapid deployment of continuous glucose monitors, cardiac monitoring patches, and remote patient monitoring platforms is strengthening demand for advanced wearable medical device adhesives. More than 65% of newly introduced wearable healthcare devices now require skin-compatible adhesives capable of multi-day attachment, while silicone-based formulations have improved long-wear performance by nearly 30%. The United States continues to accelerate FDA-cleared wearable technologies, encouraging suppliers to develop breathable, hypoallergenic adhesive systems. This transition is increasing demand for customized material formulations and automated coating technologies. In response, leading manufacturers are expanding production capacity, investing in specialty polymer research, and partnering with medical device developers to deliver application-specific adhesive solutions. Companies that integrate formulation expertise with scalable manufacturing gain stronger differentiation and faster commercialization.

Volatility in medical-grade silicone, acrylic polymers, and specialty coating materials continues to challenge production planning and cost optimization. More than 45% of adhesive manufacturers remain dependent on a limited supplier base for high-purity raw materials, while regulatory qualification processes can extend material substitution timelines by over 20%. Japan and Germany remain important sources of specialty medical-grade inputs, creating procurement pressure during supply disruptions. These structural constraints increase inventory costs, lengthen product validation cycles, and reduce manufacturing flexibility. To improve operational resilience, companies are diversifying supplier networks, localizing selected production activities, and securing long-term procurement agreements. Strengthening supply-chain transparency has become a competitive advantage for maintaining uninterrupted medical device manufacturing.

Next-generation bio-compatible adhesives present significant opportunities as wearable healthcare platforms become thinner, smarter, and capable of extended patient monitoring. More than 55% of product development programs now prioritize breathable and skin-sensitive adhesive technologies, while bio-based material adoption has increased by approximately 22% across medical material innovation projects. South Korea is expanding investments in flexible electronics and digital healthcare manufacturing, supporting integration between advanced sensors and specialty adhesives. Companies are strengthening R&D collaborations with research institutes and wearable device manufacturers to develop antimicrobial, moisture-resistant, and recyclable adhesive systems. A major strategic opportunity lies in creating multifunctional adhesive platforms that improve patient comfort while enabling integrated sensing capabilities without increasing device complexity.

Maintaining consistent adhesive performance across high-volume manufacturing remains a critical long-term challenge as wearable devices become increasingly sophisticated. Approximately 35% of manufacturers report greater process complexity when producing ultra-thin adhesive layers, while quality validation requirements can increase production lead times by nearly 18%. The United States continues to tighten expectations for medical device quality documentation and manufacturing traceability, increasing operational demands on suppliers. Variability in coating precision, sterilization compatibility, and long-duration skin performance directly affects deployment consistency and customer confidence. Companies are addressing these challenges through automated inspection systems, digital manufacturing technologies, workforce training, and advanced quality-control infrastructure to achieve reliable large-scale production and strengthen long-term competitive positioning.

Advanced Silicone Material Adoption Medical device manufacturers are rapidly shifting toward advanced silicone adhesive platforms that now account for nearly 62% of new wearable healthcare product developments. Extended wear duration has improved by approximately 28%, while skin irritation rates have declined by almost 20% through breathable adhesive formulations. Companies are expanding automated coating lines and investing in precision polymer engineering to improve manufacturing consistency. Regulatory emphasis on patient safety and long-duration monitoring continues to accelerate qualification of premium medical-grade adhesive systems.

Localized Manufacturing Expansion Supply-chain diversification is driving production localization across the United States, Germany, and South Korea, with more than 35% of manufacturers expanding regional sourcing networks to improve supply resilience. Procurement lead times have fallen by nearly 18% following localized material qualification. Companies are restructuring supplier portfolios, increasing inventory visibility, and adopting digital production planning to reduce operational disruptions while maintaining uninterrupted delivery of specialty adhesive materials for wearable healthcare devices.

Hybrid Functional Adhesive Platforms Manufacturers are integrating antimicrobial coatings, moisture management technologies, and flexible conductive materials into next-generation adhesive platforms. Around 42% of newly developed wearable devices now incorporate multifunctional adhesive layers that improve patient comfort and device stability. These integrated designs reduce replacement frequency and simplify device assembly, encouraging companies to strengthen collaborations with sensor developers and flexible electronics manufacturers to accelerate commercial deployment.

Automation Enhancing Quality Control Automated optical inspection, AI-assisted coating optimization, and digital process monitoring are transforming adhesive manufacturing operations. More than 48% of large-scale production facilities have introduced automated inspection technologies, reducing material defects by approximately 22% while improving production consistency. Rising quality expectations for wearable medical devices are encouraging companies to modernize manufacturing infrastructure, standardize production workflows, and deploy predictive maintenance systems that strengthen long-term operational efficiency.

Silicone adhesives represent the leading segment due to superior skin compatibility, extended wear capability, and excellent moisture resistance required for continuous glucose monitors and cardiac monitoring patches. They account for approximately 54% of total product utilization, supported by strong adhesion performance during multi-day monitoring. Acrylic adhesives remain widely adopted because of their cost efficiency and processing flexibility across disposable wearable devices. Hydrocolloid adhesives continue serving specialized wound-care wearables where moisture retention remains operationally important. Polyurethane and hybrid adhesive formulations are emerging as the fastest-growing category as manufacturers pursue thinner, flexible, and highly breathable wearable platforms. Nearly 30% of next-generation product development programs now evaluate hybrid adhesive technologies for improved durability and patient comfort. Companies are expanding specialty material portfolios, strengthening medical polymer research, and collaborating with wearable device manufacturers to develop customized adhesive systems for long-duration healthcare applications.

Continuous glucose monitoring represents the largest application segment as diabetes management increasingly relies on long-duration wearable sensors requiring dependable skin adhesion. Nearly 46% of wearable adhesive consumption is associated with glucose monitoring devices, reflecting high replacement frequency and expanding patient adoption. Cardiac monitoring follows closely as healthcare providers deploy ambulatory ECG patches for extended outpatient diagnostics. Drug delivery patches continue maintaining stable demand through controlled transdermal therapeutic applications. Remote patient monitoring is the fastest-growing application as healthcare systems expand virtual care infrastructure and home-based clinical management. More than 33% of healthcare organizations have accelerated deployment of connected monitoring technologies supporting long-term patient observation. Companies are enhancing adhesive durability, optimizing skin compatibility, and integrating flexible materials to support increasingly sophisticated wearable platforms across chronic disease management, diagnostic monitoring, and preventive healthcare programs.

Medical device manufacturers remain the dominant end-user group because they integrate wearable adhesives directly into commercial healthcare products requiring strict regulatory compliance and consistent production quality. Approximately 58% of adhesive procurement originates from established wearable device manufacturers producing glucose monitors, cardiac patches, and biosensor platforms. Hospitals and healthcare providers continue expanding utilization as remote patient monitoring programs become increasingly embedded within routine clinical practice. Home healthcare providers represent the fastest-growing end-user segment as long-term disease management shifts toward patient-centered monitoring outside traditional clinical facilities. Adoption has increased by nearly 27% through broader acceptance of connected healthcare technologies and digital monitoring ecosystems. Research organizations and contract development partners continue supporting material validation and product innovation, while adhesive manufacturers strengthen strategic partnerships, application engineering services, and customized product offerings to address evolving clinical and commercial requirements.

North America accounted for the largest market share at 39.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.3% between 2026 and 2033.

North America maintains its leadership through a well-established medical device manufacturing ecosystem, rapid commercialization of wearable healthcare technologies, and extensive deployment of remote patient monitoring solutions. The region contributes approximately 39.2% of global demand, supported by strong integration between adhesive manufacturers, medical device developers, and digital healthcare companies. More than 65% of newly commercialized wearable monitoring devices utilize advanced silicone-based adhesive systems designed for extended wear. Continued investment in automated manufacturing, material innovation, and regulatory-compliant production has strengthened regional competitiveness. Strategic collaborations between adhesive suppliers and wearable device manufacturers continue to accelerate product development while improving production efficiency, quality assurance, and supply-chain resilience across high-value healthcare applications.

United States Market Outlook: The United States remains the largest national market due to its concentration of wearable medical device manufacturers, advanced healthcare infrastructure, and continuous innovation in remote patient monitoring technologies. Approximately 70% of North America's wearable medical device production is concentrated in the country, supported by strong investment in digital health platforms and specialty material development. Manufacturers continue expanding domestic production capabilities while strengthening partnerships with healthcare technology companies to accelerate commercialization of next-generation wearable devices.

Europe remains a strategically important market through its emphasis on medical-grade quality standards, sustainable manufacturing, and advanced healthcare technology adoption. The region represents approximately 27.5% of global market activity, supported by established medical materials manufacturing and increasing deployment of long-duration wearable monitoring systems. More than 40% of newly developed adhesive formulations emphasize solvent-free processing and improved skin compatibility to align with evolving environmental and product safety expectations. Manufacturers continue investing in precision coating technologies, localized production, and collaborative product development to strengthen operational performance. Regulatory harmonization and modernization of medical manufacturing facilities continue supporting higher-value adhesive innovation across healthcare applications.

Germany Market Outlook: Germany serves as Europe's primary industrial hub for medical materials and advanced healthcare manufacturing. The country accounts for nearly 29% of regional medical adhesive production capacity and benefits from strong engineering capabilities and specialized polymer manufacturing expertise. Companies continue investing in automated production technologies and research partnerships that enhance material performance, manufacturing consistency, and long-term competitiveness within wearable healthcare applications.

Asia-Pacific is strengthening its competitive position through expanding medical device manufacturing capacity, cost-efficient production, and growing domestic healthcare technology adoption. The region contributes approximately 24.8% of global market demand while serving as a major production base for wearable healthcare components. More than 45% of global flexible electronics manufacturing supporting wearable devices is concentrated across key Asian industrial economies. Increasing investment in specialty polymers, automated coating technologies, and export-oriented manufacturing is improving production efficiency. Companies continue expanding regional manufacturing facilities and forming strategic supply partnerships to strengthen responsiveness and support growing international demand for advanced wearable medical adhesives.

China Market Outlook: China leads regional production through its extensive medical device manufacturing ecosystem and rapidly expanding digital healthcare industry. The country produces more than 50% of Asia-Pacific's wearable healthcare components and continues investing in advanced material manufacturing and intelligent production facilities. Domestic manufacturers are increasing research into medical-grade adhesive technologies while expanding partnerships with international wearable device companies to improve product quality and export competitiveness.

South America is experiencing increasing adoption of wearable healthcare technologies as healthcare modernization programs expand digital monitoring capabilities across hospitals and outpatient care facilities. The region accounts for approximately 5.2% of global market activity, with growing utilization of wearable diagnostic devices supporting higher demand for medical-grade adhesive materials. Healthcare investments have contributed to nearly 18% growth in remote monitoring deployments across major healthcare systems over recent years. Manufacturers are strengthening regional distribution networks and expanding technical support services to improve product availability. Although imported specialty materials remain important, increasing collaboration with regional healthcare providers is improving deployment consistency and market accessibility.

Brazil Market Outlook: Brazil represents the largest market in South America due to its expanding healthcare infrastructure, growing medical device sector, and increasing investment in digital health services. The country accounts for approximately 46% of regional wearable medical device demand and continues strengthening domestic medical manufacturing capabilities. Companies are expanding commercial partnerships with hospitals and healthcare providers while improving access to advanced wearable technologies through localized distribution strategies.

The Middle East & Africa market is progressing through sustained investment in healthcare infrastructure, digital transformation initiatives, and modernization of clinical services. The region contributes approximately 3.3% of global market demand, supported by increasing deployment of connected healthcare technologies and remote patient monitoring solutions. More than 22% of newly established digital healthcare programs across leading Gulf countries incorporate wearable monitoring technologies for chronic disease management. Companies are expanding regional partnerships, strengthening distribution capabilities, and investing in technical training to improve product adoption. Continued healthcare infrastructure modernization is creating opportunities for advanced medical adhesive suppliers supporting next-generation wearable devices.

Saudi Arabia Market Outlook: Saudi Arabia remains the region's most strategically significant market due to extensive healthcare modernization initiatives, increasing digital healthcare investments, and strong government support for advanced medical technologies. The country accounts for approximately 38% of Middle East wearable healthcare deployments and continues expanding hospital digitization and remote patient monitoring programs. International manufacturers are strengthening local partnerships and technical support capabilities to improve market access and accelerate adoption of advanced wearable medical device adhesive solutions.

Competition is led by 3M, Henkel AG & Co. KGaA, Avery Dennison Corporation, Scapa Healthcare, and Dow, while regional adhesive formulators compete through customized medical-grade solutions and cost-efficient manufacturing. The top five companies collectively control approximately 58% of the global market, creating a moderately consolidated structure. Global technology leaders compete on long-wear skin adhesion, regulatory compliance, and formulation performance, whereas regional suppliers emphasize rapid customization and localized delivery. More than 65% of premium wearable medical devices now specify silicone-based adhesive platforms, while automated coating technologies improve manufacturing efficiency by nearly 22%. Companies are expanding production capacity, strengthening OEM partnerships, and vertically integrating specialty material capabilities to secure supply continuity. Competition is shifting toward bio-compatible materials, solvent-free formulations, and integrated wearable system solutions rather than price alone. Strict medical qualification requirements, extensive product validation, and specialized manufacturing expertise remain major entry barriers. Success depends on combining material innovation, manufacturing precision, regulatory readiness, and strategic customer collaboration.

Henkel AG & Co. KGaA

Avery Dennison Corporation

Scapa Healthcare

Dow

Elkem ASA

H.B. Fuller Company

Lohmann GmbH & Co. KG

Nitto Denko Corporation

Adhex Technologies

Polymer Science, Inc.

Vancive Medical Technologies

Tesa SE

Advanced silicone adhesive technologies continue to define the market by delivering stronger skin compatibility, extended wear duration, and improved moisture resistance. More than 60% of newly developed wearable medical devices now utilize medical-grade silicone formulations, reducing device replacement frequency by approximately 25%. UV-curable and solvent-free adhesive systems are also gaining adoption because they shorten manufacturing cycles while improving environmental compliance. Companies investing in precision coating technologies benefit from higher production consistency and lower process waste.

Emerging technologies include bio-based polymers, antimicrobial adhesive coatings, conductive adhesive materials, and AI-enabled manufacturing inspection. Nearly 40% of large adhesive manufacturers have introduced automated quality monitoring that reduces coating defects by around 20%. Compared with conventional acrylic adhesive systems, next-generation silicone-hybrid formulations improve long-duration adhesion by nearly 30% while significantly reducing skin irritation. Medical device manufacturers integrating these technologies achieve greater product reliability and stronger differentiation in premium wearable healthcare applications.

Between 2026 and 2028, multifunctional adhesive platforms supporting biosensors, flexible electronics, and smart diagnostic patches are expected to become mainstream. Companies adopting automated material formulation, digital quality control, and customized adhesive engineering will strengthen manufacturing resilience and accelerate commercialization. Technology leadership will increasingly favor suppliers capable of integrating advanced materials with scalable production, regulatory compliance, and collaborative product development for next-generation wearable healthcare devices.

February 2024 – Henkel introduced Loctite 4011S and Loctite 4061S next-generation medical-grade instant adhesives formulated without CMR ingredients. The products demonstrated approximately 100% higher shear strength after extended heat exposure, improving durability for advanced medical device assembly. Source: www.henkel.com

March 2025 – Henkel launched Technomelt Supra PRO 301 Plus for high-speed pharmaceutical manufacturing, featuring an ultra-fast curing time of 160 milliseconds that improves production throughput and reduces cleaning interruptions. Source: www.henkel.com

July 2025 – Texas A&M University developed a water-based polyelectrolyte adhesive for wearable medical devices designed to improve comfort for allergy-prone users while maintaining long-term skin adhesion. Source: www.news.engineering.tamu.edu

September 2025 – Henkel expanded its medical device portfolio with new LED-curable Loctite adhesives supporting more than 40 biocompatibility-tested products for advanced medical device manufacturing.

The report provides comprehensive analysis of the wearable medical device adhesives market across major adhesive technologies, healthcare applications, end-user groups, and key geographical markets. It evaluates silicone, acrylic, hydrocolloid, polyurethane, and hybrid adhesive systems while assessing demand across continuous glucose monitoring, cardiac monitoring, drug delivery, remote patient monitoring, and other wearable healthcare applications. The study covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional deployment trends, manufacturing capabilities, and competitive positioning.

The report examines technology adoption patterns, with more than 60% of new wearable platforms utilizing advanced silicone-based adhesive systems and increasing deployment of multifunctional bio-compatible materials. It delivers strategic assessment of competitive dynamics, product innovation, manufacturing expansion, supply-chain developments, and investment priorities. Business insights support market entry planning, portfolio optimization, partnership evaluation, geographic expansion, competitive benchmarking, and long-term strategic decision-making across the 2026–2033 forecast period.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 115.0 Million |

| Market Revenue (2033) | USD 299.3 Million |

| CAGR (2026–2033) | 12.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | 3M; Henkel AG & Co. KGaA; Avery Dennison Corporation; Scapa Healthcare; Dow; Elkem ASA; H.B. Fuller Company; Lohmann GmbH & Co. KG; Nitto Denko Corporation; Adhex Technologies; Polymer Science, Inc.; Vancive Medical Technologies; Tesa SE |

| Customization & Pricing | Available on Request (10% Customization Free) |