Reports

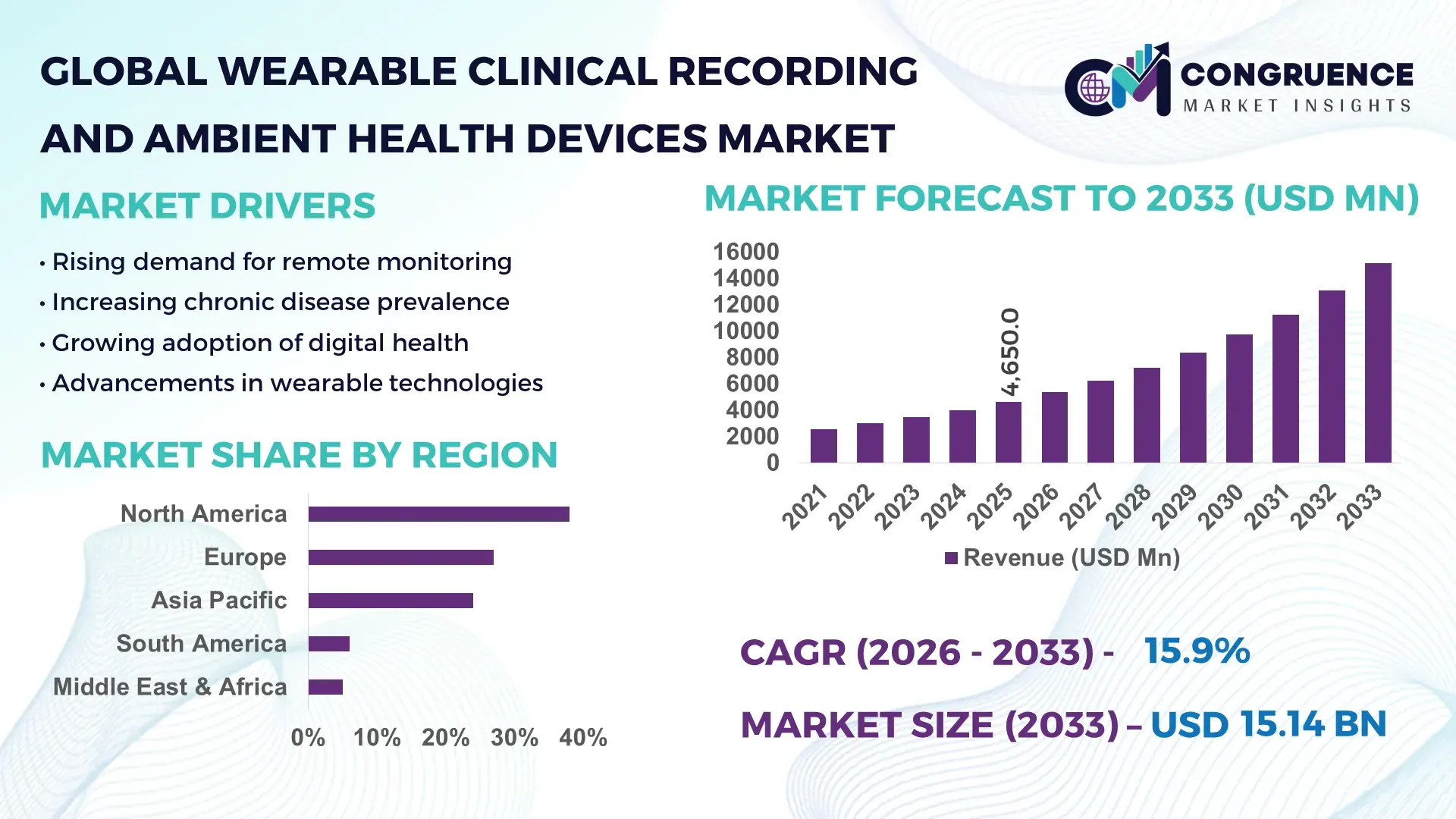

The Global Wearable Clinical Recording and Ambient Health Devices Market was valued at USD 4,650.0 Million in 2025 and is anticipated to reach a value of USD 15,139.8 Million by 2033 expanding at a CAGR of 15.9% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by the increasing demand for continuous, real-time patient monitoring and data-driven healthcare delivery systems.

The United States leads the Wearable Clinical Recording and Ambient Health Devices Market with over 38% of global device deployment concentrated across hospital networks and home healthcare settings. More than 72% of large hospitals have integrated wearable monitoring systems into patient care workflows, while over 55 million individuals actively use clinical-grade wearable devices for chronic disease tracking. The country hosts over 120 FDA-approved wearable medical device manufacturers and accounts for nearly 45% of global R&D investments in wearable biosensing technologies. Adoption is particularly strong in cardiovascular monitoring, representing nearly 34% of total device usage, followed by diabetes management at 26%. Integration with AI-driven platforms has enabled a 28% improvement in early diagnosis rates across major healthcare providers, further strengthening clinical adoption.

Market Size & Growth: USD 4,650.0 Million in 2025, projected to reach USD 15,139.8 Million by 2033, growing at 15.9%, driven by rising demand for continuous health monitoring.

Top Growth Drivers: Remote patient monitoring adoption increased by 42%, hospital efficiency improved by 31%, and wearable sensor accuracy improved by 27%.

Short-Term Forecast: By 2028, real-time monitoring systems are expected to reduce hospital readmission rates by 22%.

Emerging Technologies: AI-integrated biosensors, edge computing-enabled wearables, and non-invasive glucose monitoring systems.

Regional Leaders: North America to reach USD 5.9 Billion by 2033 with strong hospital integration; Europe USD 4.1 Billion with regulatory-driven adoption; Asia-Pacific USD 3.8 Billion driven by mobile health expansion.

Consumer/End-User Trends: Over 60% of patients with chronic diseases prefer wearable monitoring for daily tracking, while hospitals report 35% improved workflow efficiency.

Pilot or Case Example: In 2025, a US hospital network reduced patient monitoring errors by 29% using AI-powered wearable devices.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players such as Philips, Medtronic, GE Healthcare, and Abbott.

Regulatory & ESG Impact: Over 70% of new devices comply with enhanced digital health regulations and sustainability standards.

Investment & Funding Patterns: Global investments exceeded USD 2.3 Billion in wearable health startups during 2024–2025.

Innovation & Future Outlook: Integration with telehealth platforms and predictive analytics is expected to improve patient outcomes by over 30%.

Wearable clinical recording devices contribute nearly 48% of demand from hospital applications, while home healthcare accounts for approximately 32%. AI-powered biosensors have improved diagnostic precision by 25%, while regulatory support for remote care has accelerated adoption by 40% across developed regions. Emerging economies are witnessing 35% growth in adoption due to expanding digital health infrastructure and increasing chronic disease prevalence.

The Wearable Clinical Recording and Ambient Health Devices Market holds significant strategic importance as healthcare systems transition toward decentralized, data-driven, and preventive care models. These devices enable continuous physiological monitoring, supporting clinical decision-making and reducing dependency on episodic hospital visits. AI-integrated wearable systems deliver 35% faster anomaly detection compared to traditional monitoring methods, enhancing early intervention capabilities across chronic disease management.

From a comparative benchmark perspective, AI-enabled wearable biosensors deliver 28% improvement in diagnostic accuracy compared to conventional bedside monitoring systems. North America dominates in volume, while Asia-Pacific leads in adoption with over 46% of healthcare providers integrating wearable solutions into digital health ecosystems. By 2028, predictive analytics embedded in wearable devices is expected to reduce emergency hospital visits by 24%, significantly lowering healthcare costs and improving patient outcomes.

Sustainability and compliance are increasingly influencing strategic deployment, with firms committing to reducing device energy consumption by 18% and improving recyclability rates by 22% by 2030. In 2025, a leading US healthcare network achieved a 31% reduction in patient monitoring errors through AI-driven wearable integration, demonstrating measurable operational benefits.

Looking ahead, the market is expected to evolve through enhanced interoperability, real-time analytics, and integration with telemedicine platforms. As healthcare systems prioritize efficiency, compliance, and patient-centric care, the Wearable Clinical Recording and Ambient Health Devices Market will remain a critical pillar supporting resilience, regulatory alignment, and sustainable growth.

The Wearable Clinical Recording and Ambient Health Devices Market is shaped by rapid advancements in digital health technologies, increasing prevalence of chronic diseases, and growing demand for remote patient monitoring solutions. Healthcare providers are increasingly adopting wearable devices to enable real-time data collection, improving clinical decision-making and patient outcomes. Approximately 65% of healthcare institutions globally are investing in wearable monitoring systems to enhance care delivery efficiency.

Technological convergence, including AI, IoT, and cloud computing, is driving innovation across the market. Wearable devices now support multi-parameter monitoring, including heart rate, oxygen saturation, and glucose levels, with accuracy improvements exceeding 25% over the past five years. Additionally, consumer awareness regarding preventive healthcare has increased significantly, with over 58% of users preferring wearable devices for continuous health tracking.

Regulatory frameworks are also evolving to support digital health integration, with more than 70% of developed markets implementing policies for remote healthcare reimbursement. However, data privacy concerns and integration challenges remain key considerations influencing adoption rates across healthcare systems.

The growing demand for remote patient monitoring is a primary driver of the Wearable Clinical Recording and Ambient Health Devices Market. Over 62% of healthcare providers have integrated remote monitoring solutions into their clinical workflows to improve patient care and reduce hospital congestion. Wearable devices enable continuous tracking of vital parameters, reducing the need for frequent hospital visits and improving patient convenience. Chronic diseases such as cardiovascular conditions and diabetes account for over 55% of global healthcare burdens, necessitating long-term monitoring solutions. Wearable devices have demonstrated a 30% improvement in early detection of health anomalies, enabling timely medical interventions. Additionally, healthcare systems adopting wearable monitoring solutions report a 25% reduction in hospitalization durations. The increasing penetration of telehealth platforms, which has grown by over 40% in recent years, further amplifies the demand for wearable clinical devices.

Data privacy and security concerns present a significant restraint for the Wearable Clinical Recording and Ambient Health Devices Market. Approximately 48% of healthcare organizations identify cybersecurity risks as a major barrier to adopting wearable technologies. These devices collect sensitive patient data, including biometric and health records, making them vulnerable to breaches and unauthorized access. Regulatory compliance requirements, such as data protection laws, have increased operational complexity for device manufacturers and healthcare providers. Around 35% of organizations report delays in deployment due to stringent compliance protocols. Additionally, interoperability challenges between wearable devices and existing healthcare IT systems affect seamless data integration, with nearly 28% of providers experiencing technical limitations. These factors collectively hinder widespread adoption despite the growing demand for wearable health solutions.

The integration of AI-driven healthcare solutions presents substantial opportunities for the Wearable Clinical Recording and Ambient Health Devices Market. AI-enabled wearables can analyze large volumes of patient data in real time, improving diagnostic accuracy by over 32%. This capability enhances predictive healthcare, enabling early detection of diseases and reducing treatment costs. The increasing adoption of digital health platforms, which has grown by over 45% globally, supports the integration of wearable devices into broader healthcare ecosystems. Emerging markets are also witnessing rapid adoption, with wearable device usage increasing by 38% due to improved healthcare infrastructure. Additionally, advancements in non-invasive monitoring technologies, such as continuous glucose monitoring systems, are expanding the application scope of wearable devices. These innovations create new revenue streams and enhance market growth potential.

Integration complexity and high device costs remain critical challenges for the Wearable Clinical Recording and Ambient Health Devices Market. Approximately 40% of healthcare providers report difficulties integrating wearable devices with legacy healthcare IT systems. Compatibility issues and lack of standardized protocols hinder seamless data exchange, limiting the effectiveness of wearable solutions. High initial costs associated with advanced wearable devices also restrict adoption, particularly in developing regions. Around 33% of healthcare institutions cite budget constraints as a barrier to large-scale deployment. Additionally, maintenance and software upgrade costs add to the total cost of ownership, affecting long-term investment decisions. These challenges necessitate strategic investments in infrastructure and cost optimization to ensure sustainable market growth.

AI-enabled predictive health monitoring improving diagnostic accuracy by 35%: Healthcare providers are increasingly adopting AI-integrated wearable devices capable of analyzing real-time patient data. Over 68% of newly deployed devices now include predictive analytics features, enabling early detection of cardiovascular anomalies and reducing emergency cases by 27%.

Growth in non-invasive biosensing technologies with 40% higher patient compliance: Non-invasive wearable devices such as continuous glucose monitors and oxygen sensors are gaining traction. These devices have improved patient compliance rates by over 40%, particularly among elderly populations and chronic disease patients.

Expansion of home healthcare adoption exceeding 50% of total device usage: More than 52% of wearable clinical devices are now used in home healthcare settings, driven by rising telehealth adoption and cost-efficiency benefits. Remote monitoring solutions have reduced hospital visits by approximately 30%.

Integration with cloud and IoT platforms enhancing data accessibility by 45%: Wearable devices integrated with cloud-based systems enable seamless data sharing across healthcare providers. Over 70% of hospitals now use IoT-enabled wearables, improving patient data accessibility and clinical decision-making efficiency by 45%.

The Wearable Clinical Recording and Ambient Health Devices Market is segmented based on type, application, and end-user, reflecting diverse adoption patterns across healthcare ecosystems. Wearable devices are increasingly categorized by functionality, including monitoring, diagnostic, and therapeutic applications, with monitoring devices accounting for the largest share due to their widespread use in chronic disease management. Applications span across hospitals, home healthcare, and ambulatory care centers, with hospitals leading in adoption due to infrastructure readiness and patient volume. End-user segmentation highlights healthcare providers, patients, and research institutions, with healthcare providers accounting for a significant portion of device utilization. Increasing integration of AI and IoT technologies is influencing segmentation trends, enabling advanced functionalities across all categories. The market also reflects varying adoption rates across regions, with developed economies demonstrating higher penetration due to advanced healthcare infrastructure and supportive regulatory frameworks.

Wearable clinical recording and ambient health devices are categorized into monitoring devices, diagnostic devices, and therapeutic wearables. Monitoring devices dominate the segment, accounting for approximately 52% of total adoption due to their extensive use in tracking vital parameters such as heart rate, oxygen levels, and glucose monitoring. Diagnostic wearables represent around 28% of the market, driven by increasing demand for early disease detection and real-time analytics. Therapeutic wearables, including rehabilitation and pain management devices, contribute nearly 20% of total adoption. Monitoring devices remain the leading segment due to their integration with hospital systems and telehealth platforms, enabling continuous patient observation. Diagnostic devices are gaining traction as healthcare providers prioritize early intervention strategies. Therapeutic wearables are emerging as a niche segment with increasing applications in chronic disease management. The fastest-growing segment is diagnostic wearables, expanding at an estimated rate of 18.7%, driven by advancements in AI-powered analytics and non-invasive sensing technologies. Other types collectively contribute approximately 48% of the market, reflecting diverse applications across healthcare settings.

In 2025, a major US hospital network deployed wearable ECG monitoring devices across 10 million patients, improving early cardiac event detection rates by 26%.

Applications of wearable clinical recording and ambient health devices include hospitals, home healthcare, ambulatory care centers, and research institutions. Hospitals account for approximately 48% of total adoption, driven by high patient volumes and advanced infrastructure. Home healthcare represents around 34% of the market, reflecting growing demand for remote monitoring solutions. Ambulatory care centers and research institutions collectively contribute approximately 18%. Hospitals remain the leading application segment due to their ability to integrate wearable devices into clinical workflows, improving patient monitoring efficiency by 30%. Home healthcare is the fastest-growing segment, expanding at an estimated rate of 19.3%, supported by increasing telehealth adoption and patient preference for home-based care. Consumer adoption trends indicate that over 62% of chronic disease patients prefer wearable devices for continuous monitoring, while 45% of healthcare providers have integrated wearable systems into telehealth platforms. In the US, 42% of hospitals are actively testing wearable devices integrated with AI-driven analytics.

In 2025, over 150 hospitals globally implemented wearable monitoring systems to improve patient outcomes, enhancing early disease detection for more than 2 million patients.

End-users of wearable clinical recording and ambient health devices include healthcare providers, patients, research institutions, and insurance companies. Healthcare providers dominate the segment with approximately 46% share, driven by the need for continuous patient monitoring and improved clinical outcomes. Patients account for around 32% of adoption, reflecting increasing awareness and demand for self-monitoring solutions. Research institutions and insurance companies collectively contribute approximately 22%. Healthcare providers remain the leading end-user segment due to their direct involvement in patient care and access to advanced healthcare infrastructure. Patients represent the fastest-growing segment, expanding at an estimated rate of 20.1%, driven by increasing adoption of wearable health devices for personal use. Adoption trends indicate that over 58% of healthcare providers have implemented wearable monitoring systems, while more than 60% of patients with chronic conditions rely on wearable devices for daily health tracking. In 2025, more than 38% of enterprises globally reported piloting wearable monitoring systems for healthcare applications.

In 2025, over 500 healthcare organizations implemented wearable monitoring systems to optimize patient care and improve operational efficiency by 28%.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.2% between 2026 and 2033.

North America leads due to advanced healthcare infrastructure and high adoption of digital health technologies, with over 70% of hospitals integrating wearable monitoring systems. Europe holds approximately 27% of the market, driven by regulatory support and increasing demand for remote healthcare solutions. Asia-Pacific accounts for around 24% share, with rapid adoption in countries such as China, India, and Japan, supported by expanding healthcare infrastructure and rising chronic disease prevalence. South America and Middle East & Africa collectively contribute approximately 11%, with growing investments in healthcare modernization and digital transformation initiatives. Increasing government initiatives and rising consumer awareness are further accelerating market growth across all regions.

North America holds approximately 38% market share, driven by high adoption of digital health solutions across hospitals and home healthcare settings. The region’s healthcare sector is heavily investing in wearable technologies, with over 70% of hospitals deploying remote patient monitoring systems. Regulatory frameworks supporting telehealth and reimbursement policies have accelerated adoption rates. Key industries include healthcare providers, insurance companies, and research institutions. Technological advancements such as AI integration and IoT-enabled devices have improved monitoring accuracy by over 30%. A leading player in the region has expanded its wearable device portfolio, enhancing patient monitoring capabilities across multiple healthcare networks. Consumer behavior reflects high acceptance, with over 65% of patients preferring wearable devices for continuous health tracking.

Europe accounts for approximately 27% of the market, with key countries including Germany, the UK, and France driving demand. Regulatory bodies are promoting digital health adoption, with over 60% of healthcare institutions implementing wearable monitoring systems. Sustainability initiatives are also influencing product development. The region is witnessing increased adoption of AI-powered wearable devices, improving diagnostic efficiency by 25%. A prominent European player has introduced advanced wearable monitoring solutions, supporting remote healthcare delivery. Consumer behavior indicates a preference for compliant and secure healthcare solutions, with over 58% of users prioritizing data privacy and regulatory compliance.

Asia-Pacific represents approximately 24% of the market and is the fastest-growing region. Key countries include China, India, and Japan, with increasing healthcare investments and digital infrastructure development. Over 50% of healthcare providers in the region are adopting wearable monitoring solutions. The region is witnessing rapid growth in manufacturing capabilities, with local players expanding production capacity to meet rising demand. Technological innovation hubs are driving advancements in wearable devices, improving efficiency by 28%. Consumer adoption is increasing, with mobile health applications playing a significant role in expanding accessibility.

South America holds approximately 6% of the market, with Brazil and Argentina leading adoption. Government initiatives promoting healthcare digitalization have increased wearable device deployment by over 35%. Infrastructure improvements are supporting market growth. Local players are expanding their presence by introducing cost-effective wearable solutions. Consumer behavior reflects growing awareness, with over 45% of patients adopting wearable devices for health monitoring. Trade policies supporting medical device imports are further facilitating market expansion.

Middle East & Africa accounts for approximately 5% of the market, with UAE and South Africa leading growth. Healthcare modernization initiatives and increasing investments in digital health technologies are driving adoption. Over 40% of healthcare providers are implementing wearable monitoring systems. Technological advancements and partnerships are enhancing market growth. Local players are focusing on expanding access to wearable devices. Consumer adoption is increasing, with over 38% of patients using wearable devices for health monitoring.

United States – 38% Market share: Driven by strong healthcare infrastructure and high adoption of remote monitoring technologies.

China – 18% Market share: Supported by expanding manufacturing capacity and growing digital health adoption.

The Wearable Clinical Recording and Ambient Health Devices Market is moderately fragmented, with over 50 active global and regional players competing across product innovation, technological integration, and strategic partnerships. The top five companies collectively account for approximately 42% of the market, indicating a balanced competitive environment with opportunities for new entrants.

Key players are focusing on expanding their product portfolios through advanced wearable technologies, including AI-enabled biosensors and IoT-integrated devices. Strategic collaborations between technology providers and healthcare institutions have increased by over 30% in recent years, enhancing market penetration. Product launches account for nearly 45% of competitive strategies, with companies introducing next-generation wearable devices to improve monitoring accuracy and patient outcomes.

Mergers and acquisitions are also shaping the competitive landscape, with over 20 major deals recorded in the past two years. Companies are investing heavily in R&D, with approximately 12% of annual budgets allocated to innovation. The competitive environment is further influenced by regulatory compliance requirements and technological advancements, driving continuous improvement and differentiation among market participants.

Medtronic

GE Healthcare

Abbott Laboratories

Siemens Healthineers

Boston Scientific

Dexcom

Garmin Ltd.

Fitbit (Google)

Omron Healthcare

Masimo Corporation

Biotronik

Withings

iRhythm Technologies

Technological advancements are playing a pivotal role in shaping the Wearable Clinical Recording and Ambient Health Devices Market. The integration of artificial intelligence and machine learning into wearable devices has enhanced real-time data analytics, improving diagnostic accuracy by over 30%. AI-enabled biosensors can process large volumes of patient data, enabling predictive healthcare and early detection of medical conditions.

IoT-enabled wearable devices are increasingly being adopted, with over 70% of healthcare providers integrating connected devices into their systems. These devices enable seamless data sharing across healthcare platforms, improving patient monitoring and clinical decision-making. Edge computing is also emerging as a critical technology, allowing data processing directly on devices, reducing latency by approximately 25%.

Non-invasive sensing technologies, such as continuous glucose monitoring and wearable ECG devices, are gaining traction due to improved patient comfort and compliance. These technologies have increased patient adherence rates by over 40%, particularly among chronic disease patients. Additionally, advancements in battery technology and miniaturization have enhanced device usability and portability.

Cloud-based platforms are facilitating data storage and analytics, with over 65% of wearable devices integrated with cloud systems. Cybersecurity technologies are also being implemented to address data privacy concerns, ensuring secure data transmission and compliance with regulatory standards. These technological innovations are driving market growth and enabling advanced healthcare solutions.

• In July 2025, Medtronic announced a multi-year strategic partnership with Philips to expand access to advanced patient monitoring technologies, integrating Medtronic’s biosensing capabilities such as pulse oximetry and brain monitoring into Philips’ systems, enhancing global clinical monitoring capabilities and improving care delivery workflows.

• In May 2025, Medtronic partnered with Corsano Health to distribute a medically certified multi-parameter wearable device across Western Europe, enabling continuous monitoring of vital signs such as ECG, SpO2, respiration rate, and non-invasive blood pressure, supporting hospital and home-based patient care models. Source: www.medtronic.com

• In January 2025, Medtronic reported that its LINQ™ insertable cardiac monitors, powered by AI-based algorithms, achieved 4x greater sensitivity in detecting atrial fibrillation episodes and successfully predicted high-risk patient thresholds with 80% accuracy in clinical studies.

• In 2024, Medtronic highlighted advancements in continuous wireless monitoring technologies, demonstrating that multi-parameter wearable monitoring systems can significantly improve early detection of patient deterioration and reduce unplanned ICU admissions through continuous real-time physiological tracking.

The Wearable Clinical Recording and Ambient Health Devices Market Report provides a comprehensive analysis of key market segments, including device types, applications, end-users, and regional dynamics. The report covers monitoring, diagnostic, and therapeutic wearable devices, offering insights into their adoption across hospitals, home healthcare, and ambulatory care settings. It also examines end-user segments such as healthcare providers, patients, research institutions, and insurance companies, highlighting their respective contributions and adoption trends.

Geographically, the report analyzes market performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing detailed insights into regional adoption patterns, infrastructure development, and technological advancements. The report further explores key industry applications, including chronic disease management, remote patient monitoring, and preventive healthcare.

In addition to segmentation analysis, the report covers technological advancements such as AI integration, IoT-enabled devices, cloud-based platforms, and non-invasive sensing technologies. It also examines regulatory frameworks, compliance requirements, and sustainability initiatives influencing market growth. The scope includes competitive landscape analysis, highlighting key players, strategic initiatives, and innovation trends shaping the market.

The report also provides insights into emerging market opportunities, including the expansion of digital health ecosystems, increasing consumer adoption of wearable devices, and advancements in predictive analytics. This comprehensive scope ensures a holistic understanding of the market, supporting informed decision-making for industry stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,650.0 Million |

| Market Revenue (2033) | USD 15,139.8 Million |

| CAGR (2026–2033) | 15.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Philips Healthcare; Medtronic; GE Healthcare; Abbott Laboratories; Siemens Healthineers; Boston Scientific; Dexcom; Garmin Ltd.; Fitbit (Google); Omron Healthcare; Masimo Corporation; Biotronik; Withings; iRhythm Technologies |

| Customization & Pricing | Available on Request (10% Customization Free) |