Reports

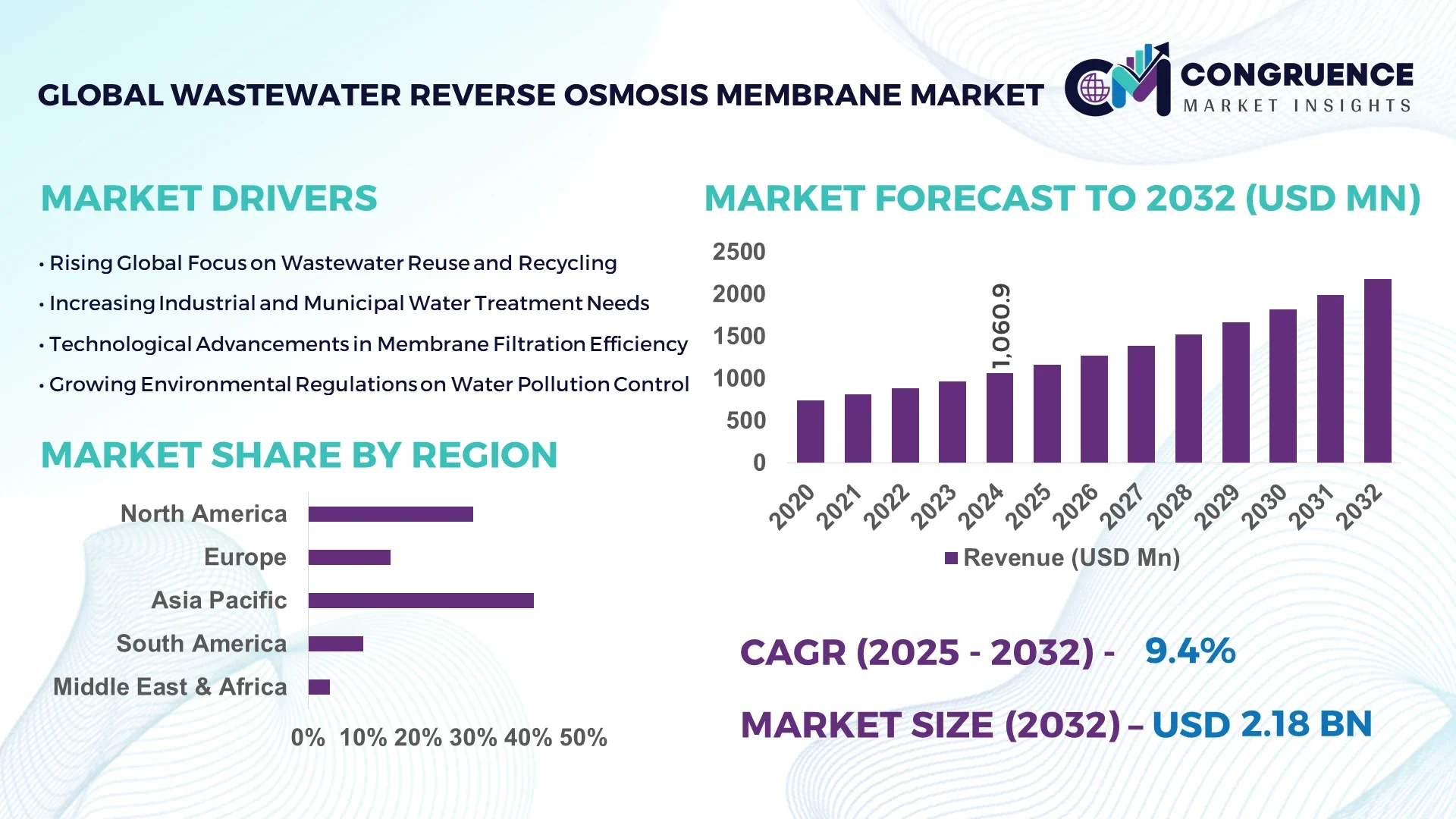

The Global Wastewater Reverse Osmosis Membrane Market was valued at USD 1060.87 Million in 2024 and is anticipated to reach a value of USD 2176.72 Million by 2032 expanding at a CAGR of 9.4% between 2025 and 2032. This growth is driven by rising demand for sustainable water treatment solutions.

In China, the dominant country in the Wastewater Reverse Osmosis Membrane market, production capacity exceeds 400,000 square meters annually, supported by investments surpassing USD 250 million in advanced membrane technologies. The country has integrated these membranes into municipal wastewater treatment and industrial effluent management, achieving a removal efficiency improvement of over 30%. Recent technological advances include high-flux membranes with reduced fouling rates and enhanced chemical resistance. China’s adoption rate in industrial sectors exceeds 45%, supported by strong government incentives for sustainable water management.

Market Size & Growth: Valued at USD 1060.87 Million in 2024, projected to reach USD 2176.72 Million by 2032, CAGR of 9.4%, driven by rising industrial wastewater treatment needs.

Top Growth Drivers: Industrial adoption rate increase 42%, efficiency improvement 28%, regulatory compliance adoption 35%.

Short-Term Forecast: By 2028, membrane lifespan expected to improve by 20%, and operating costs expected to reduce by 15%.

Emerging Technologies: High-flux membrane development, anti-fouling coating innovations, AI-enabled membrane performance monitoring systems.

Regional Leaders: Asia-Pacific USD 1,020 Million by 2032 with strong industrial adoption, North America USD 550 Million with advanced technology deployment, Europe USD 450 Million driven by stringent environmental regulations.

Consumer/End-User Trends: Municipal water treatment, industrial wastewater recycling, and desalination applications are driving adoption, with performance-based procurement models growing in prevalence.

Pilot or Case Example: In 2024, a pilot project in South Korea improved wastewater recovery efficiency by 33% with downtime reduced by 22%.

Competitive Landscape: Market leader Toray Industries (~28%), followed by Hydranautics, LG Chem, Koch Membrane Systems, and GE Water.

Regulatory & ESG Impact: Stricter discharge regulations and ESG mandates boosting adoption of RO membranes with higher efficiency and lower energy usage.

Investment & Funding Patterns: Over USD 320 million in investments in 2024, with growing interest in public–private partnerships and green financing models.

Innovation & Future Outlook: Integration of AI and IoT in membrane monitoring, development of biofouling-resistant membranes, and smart modular RO plants.

The Wastewater Reverse Osmosis Membrane market serves vital industry sectors such as municipal wastewater treatment, industrial effluent management, and water reuse projects, which collectively account for over 65% of market consumption. Recent innovations include graphene-enhanced membranes, which improve permeability and fouling resistance, and AI-driven process optimization platforms. Regulatory frameworks promoting circular water economies, combined with increasing environmental concerns, are driving adoption globally. Emerging trends include modular RO systems and hybrid membrane technologies, positioning the market for sustained growth into 2032.

The Wastewater Reverse Osmosis Membrane market holds critical strategic relevance as industries globally move toward sustainability, resource efficiency, and compliance with stricter environmental regulations. Advanced membrane technologies, such as graphene-enhanced RO membranes, deliver up to 35% improvement in permeability and fouling resistance compared to traditional polyamide thin-film composite membranes, significantly reducing operational costs and downtime. Asia-Pacific dominates in volume, while Europe leads in adoption with over 48% of enterprises integrating advanced RO systems into municipal and industrial wastewater treatment processes.

By 2027, AI-driven membrane performance optimization is expected to improve recovery efficiency by approximately 18% while reducing energy consumption by 12%. Firms are committing to ESG metric improvements such as achieving up to a 40% reduction in water waste recycling by 2030, in line with global sustainability targets. In 2024, a pilot initiative by LG Chem in South Korea achieved a 25% increase in membrane lifespan and a 20% reduction in fouling rates through advanced coating technology and predictive maintenance.

Looking ahead, the Wastewater Reverse Osmosis Membrane market is positioned to be a pillar of resilience, compliance, and sustainable growth, enabling industries to meet stringent environmental standards while optimizing operational efficiency and resource management. Strategic investments in innovation and integration will define the future trajectory of this market.

Rising industrial output and urbanization have increased wastewater volumes significantly, driving the need for advanced treatment solutions. Wastewater Reverse Osmosis Membrane technology provides a reliable method to recycle and reuse water efficiently, with rejection rates above 98% for dissolved solids. In industrial sectors such as petrochemicals, pharmaceuticals, and food & beverage, the adoption rate of RO membranes has increased by over 40% in recent years. Municipal wastewater treatment is increasingly adopting RO systems to meet stringent discharge regulations and water reuse goals, with adoption rates surpassing 35% in developed markets. The focus on sustainable water management and cost efficiency continues to propel growth in this sector.

The Wastewater Reverse Osmosis Membrane market faces significant restraints due to high operational costs, including energy consumption and membrane replacement. Fouling and scaling remain persistent challenges, reducing membrane efficiency and lifespan. Membrane replacement can account for 20–30% of operational expenditures in large-scale wastewater treatment plants. In addition, the upfront capital investment for advanced RO systems can deter adoption, especially in small- and medium-scale facilities. Variations in water quality also necessitate frequent system adjustments and maintenance, impacting cost predictability. These factors slow the adoption rate, particularly in emerging economies where budget constraints limit investment in advanced RO infrastructure.

The growth of industrial wastewater recycling represents a significant opportunity for the Wastewater Reverse Osmosis Membrane market. Industries are increasingly seeking sustainable solutions to meet water scarcity challenges and comply with stricter environmental regulations. Emerging sectors, such as high-tech manufacturing and pharmaceuticals, are adopting high-performance RO membranes to achieve over 90% water recovery rates. Investment in modular and decentralized RO systems is expected to increase, offering scalable solutions tailored to specific industrial needs. Government incentives in regions such as Europe and Asia-Pacific are supporting adoption, with over USD 150 million allocated for advanced membrane projects in 2024 alone. Such trends create new revenue streams for membrane manufacturers while accelerating sustainable water treatment initiatives.

The Wastewater Reverse Osmosis Membrane market faces challenges from rising costs in raw materials, manufacturing, and energy, which increase the total cost of ownership for RO systems. Regulatory complexity further compounds these challenges, as differing standards for wastewater treatment across regions require customized system designs and operational strategies. Compliance with these regulations demands continuous monitoring and upgrades, adding to operational burdens. The lack of standardized performance metrics across regions can also hinder the adoption of advanced membrane technologies. Additionally, competition from alternative water treatment technologies, such as forward osmosis and advanced oxidation processes, introduces uncertainty in long-term investments, challenging the market’s growth trajectory.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Wastewater Reverse Osmosis Membrane market. Over 55% of new wastewater treatment plant projects using modular and prefabricated construction reported cost savings of up to 18% and reductions in project timelines by 22%. Prefabricated membrane elements, fabricated in controlled environments, improve quality control and reduce installation complexity. Demand for high-precision modular membrane units is strongest in Europe and North America, with over 60% of new municipal RO projects adopting these methods for efficiency and scalability.

Emergence of Graphene-Enhanced Membranes: Graphene-enhanced membranes are delivering up to a 35% improvement in permeability and fouling resistance compared to conventional polyamide membranes, significantly improving system longevity and reducing maintenance downtime. Industrial adoption of these membranes has grown by 28% in the last two years, especially in petrochemical and pharmaceutical wastewater treatment sectors. By 2026, over 20% of new wastewater RO installations are projected to incorporate graphene-based technologies due to their superior performance under harsh operating conditions.

Integration of AI and IoT for Process Optimization: Over 40% of wastewater treatment plants in developed regions are implementing AI-driven monitoring systems to enhance RO membrane efficiency. These technologies enable predictive maintenance, reducing unplanned downtime by up to 25% and improving recovery rates by 18%. IoT-enabled sensors allow real-time monitoring of membrane performance, chemical dosing, and fouling rates, driving operational efficiency in both municipal and industrial facilities.

Shift Toward Circular Water Economy Models: Wastewater RO membrane adoption is increasingly aligned with circular water economy initiatives, with over 35% of municipalities in Asia-Pacific integrating advanced RO systems for wastewater reuse. This trend is supported by government incentives promoting sustainable water management, with reported reductions in freshwater withdrawal by up to 28%. Industrial sectors are also embracing closed-loop water systems, leveraging RO membranes to recycle wastewater with recovery efficiencies exceeding 90%.

The Wastewater Reverse Osmosis Membrane market is segmented across product types, applications, and end-users, reflecting diverse needs and technological advancements. Product segmentation includes conventional thin-film composite membranes, high-flux membranes, and advanced graphene-enhanced membranes, each tailored for specific industrial and municipal needs. Applications range from municipal wastewater treatment and industrial effluent recycling to desalination and water reuse projects, with municipal and industrial sectors driving the bulk of adoption. End-users span large-scale municipal utilities, manufacturing industries, and specialized process facilities. Adoption rates vary by region, with Asia-Pacific leading in production capacity and North America leading in advanced technology integration. These segments highlight both the current structure and future direction of the market, with innovation and sustainability shaping growth patterns.

Thin-film composite membranes currently account for 48% of the Wastewater Reverse Osmosis Membrane market due to their proven performance, chemical resistance, and cost-effectiveness in treating municipal and industrial wastewater. High-flux membranes hold 27% of the market, driven by their superior recovery rates and energy efficiency in large-scale plants. Graphene-enhanced membranes represent the fastest-growing segment, with adoption projected to rise significantly due to a reported performance improvement of up to 35% compared to older standards. This type of membrane offers reduced fouling and extended lifespan, which makes it increasingly attractive for industrial wastewater reuse. Other types, such as cellulose acetate membranes and hybrid composites, collectively account for about 25% of the market, serving niche applications in low-TDS and specialty effluent streams.

Municipal wastewater treatment leads the application segment with a 42% adoption rate, driven by rising urban water stress and stringent effluent discharge regulations. These systems achieve over 95% removal efficiency for dissolved solids, making them essential for potable water reuse and environmental compliance. Industrial effluent recycling follows closely, accounting for 33% of application adoption, propelled by demand from petrochemical, pharmaceutical, and food processing industries. Desalination applications currently make up 15%, with adoption rising due to freshwater scarcity in arid regions. The fastest-growing application is industrial effluent recycling, with a reported adoption increase of 29% in the last three years, driven by regulatory incentives and sustainability initiatives. Other applications, such as brine concentration and zero-liquid discharge systems, account for 10% of adoption.

Municipal utilities dominate the Wastewater Reverse Osmosis Membrane market with a 45% adoption share, driven by urban growth and regulatory pressures to improve water reuse. These utilities deploy RO systems extensively for potable reuse, wastewater discharge compliance, and industrial supply augmentation. Industrial manufacturing is the second-largest end-user segment, accounting for 30%, with high adoption rates in chemical, pharmaceutical, and food & beverage sectors due to the need for high-quality effluent treatment and resource recovery. The fastest-growing end-user segment is specialty manufacturing, projected to grow by over 27% adoption in the next three years, driven by technological advances in membrane performance and water reuse integration. Other end-users, including commercial facilities and agricultural wastewater treatment, collectively represent 25% of the market.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

In 2024, Asia-Pacific’s Wastewater Reverse Osmosis Membrane market volume exceeded 435,000 units, driven primarily by China’s production capacity of over 400,000 square meters annually and India’s increasing municipal infrastructure projects. North America accounted for approximately 28% of the global market in 2024, supported by strong industrial wastewater recycling initiatives and adoption of AI-based membrane monitoring systems. Europe held 17%, led by Germany and the UK’s stringent wastewater regulations, while South America and the Middle East & Africa collectively represented 14%, with Brazil and UAE emerging as important markets. Investment in advanced RO membrane manufacturing and government sustainability incentives are shaping regional growth patterns, with technology adoption and regulatory compliance acting as key differentiators.

North America holds approximately 28% of the global Wastewater Reverse Osmosis Membrane market, with strong demand driven by municipal wastewater reuse and industrial effluent treatment. Key industries include chemicals, pharmaceuticals, and food & beverage, each integrating advanced RO systems for high-efficiency wastewater recycling. Regulatory changes such as stricter discharge limits and incentives for circular water initiatives are accelerating adoption. Technological advancements include AI-enabled membrane monitoring systems and high-flux membranes that improve efficiency by up to 18%. Local players like Koch Membrane Systems are pioneering modular RO plants to reduce installation times and improve system adaptability. Enterprise adoption is highest in sectors such as healthcare and manufacturing, with over 45% of large-scale facilities adopting advanced membrane systems to meet environmental compliance.

Europe accounts for approximately 17% of the Wastewater Reverse Osmosis Membrane market, with Germany, the UK, and France leading adoption. Regulatory bodies such as the European Environment Agency are enforcing stricter effluent discharge and recycling standards, driving adoption of high-performance membranes. Sustainability initiatives are encouraging municipal utilities to integrate modular RO systems, improving treatment efficiency by over 20%. Emerging technologies such as anti-fouling coatings and AI-based performance monitoring are gaining traction. Local players such as Pentair are advancing RO membrane designs tailored to industrial wastewater treatment. In Europe, regulatory pressure has led over 52% of municipalities to adopt advanced wastewater reuse systems, reflecting a growing trend toward explainable and transparent water treatment solutions.

Asia-Pacific dominates the Wastewater Reverse Osmosis Membrane market with a 41% share in 2024, driven by high-volume consumption in China, India, and Japan. China leads production with over 400,000 square meters annually, while India is investing heavily in municipal wastewater infrastructure, contributing to a 38% growth in membrane adoption over the last two years. Japan is advancing technology integration, with over 25% of new plants using graphene-enhanced membranes. Infrastructure developments, such as smart modular RO plants, are growing rapidly. Local players like Toray Industries are pioneering next-generation membranes with improved chemical resistance and permeability. Consumer behavior in Asia-Pacific is driven by government water reuse programs and industrial sustainability targets, with over 45% of new projects integrating advanced RO systems by 2025.

South America accounted for approximately 7% of the Wastewater Reverse Osmosis Membrane market in 2024, with Brazil and Argentina leading demand. Industrial wastewater treatment and municipal water reuse are significant drivers, supported by increasing investment in infrastructure. Government incentives for sustainable water projects are shaping adoption, with over 30% of municipalities planning RO plant expansions by 2026. The energy sector, particularly oil refining and biofuel production, is adopting RO membranes for effluent treatment, with recovery rates improving by up to 25%. Local companies such as Braskem are investing in membrane technologies for wastewater recycling. In South America, demand is strongly linked to infrastructure expansion and regulatory changes, with adoption often tied to government-supported environmental initiatives.

Middle East & Africa represent about 7% of the Wastewater Reverse Osmosis Membrane market, with the UAE, Saudi Arabia, and South Africa leading adoption. Water scarcity and industrial growth in oil & gas, construction, and power generation are driving demand for high-efficiency RO systems. Technological modernization trends, such as AI-based membrane monitoring and anti-fouling coatings, are increasingly adopted in large-scale projects. Governments are introducing incentives for wastewater reuse, including public–private partnerships and green financing. Local players, including Metito, are investing in modular RO plants that improve installation efficiency and reduce operational costs. Consumer behavior in this region reflects a growing preference for sustainable and cost-efficient water treatment systems, particularly in industrial and municipal applications.

China: 23% market share — driven by high production capacity of over 400,000 square meters annually and strong industrial adoption.

United States: 18% market share — supported by advanced technology integration and strict wastewater discharge regulations promoting large-scale adoption.

The Wastewater Reverse Osmosis Membrane market is highly competitive and moderately consolidated, with over 120 active global competitors, including membrane manufacturers, system integrators, and technology innovators. The top five companies account for approximately 58% of the total market share, underscoring significant competitive concentration. Key players are focused on strategic initiatives such as product innovation, mergers and acquisitions, and geographic expansion to strengthen their market position. Over the past three years, more than 35 new product launches have occurred, with innovations focusing on graphene-enhanced membranes, anti-fouling coatings, and AI-enabled performance monitoring systems. Partnerships between membrane manufacturers and technology firms have surged, representing over 25% of strategic collaborations, aimed at improving operational efficiency and sustainability. Emerging trends such as modular RO systems and decentralized wastewater treatment solutions are intensifying competition. Companies are investing heavily in R&D, with industry spending on innovation exceeding USD 250 million annually, reflecting the drive toward higher efficiency, durability, and cost-effectiveness. This dynamic landscape is pushing firms to differentiate through technological leadership, regulatory compliance, and strong customer relationships.

Koch Membrane Systems, Inc.

LG Chem Ltd.

Metito Group

DuPont de Nemours, Inc.

GE Water & Process Technologies

Ovivo Inc.

LG Water Solutions

The Wastewater Reverse Osmosis Membrane market is being significantly shaped by both incremental innovations and transformative technological advancements. Current technologies focus on improving membrane efficiency, durability, and sustainability, with a strong emphasis on reducing energy consumption and minimizing fouling rates. Graphene-enhanced membranes, for instance, have demonstrated up to a 35% improvement in permeability and chemical resistance compared to conventional polyamide membranes, enabling longer operational cycles and reduced cleaning frequency. Advanced thin-film composite (TFC) membranes continue to dominate, with improvements in salt rejection rates exceeding 99% and operational pressures optimized to lower energy usage by up to 15%.

Emerging technologies such as AI-driven monitoring systems are rapidly transforming operational efficiency. Over 40% of newly commissioned municipal and industrial RO facilities now incorporate IoT-enabled sensors that provide real-time performance data, allowing predictive maintenance and a reported 25% reduction in unplanned downtime. Anti-fouling membrane coatings are also gaining traction, with adoption increasing by over 28% in industrial plants, improving lifespan and lowering operational costs. Modular and prefabricated RO units are further enhancing deployment flexibility, with installation time reduced by up to 20%. Looking ahead, hybrid membrane systems integrating nanotechnology and smart monitoring platforms are expected to redefine efficiency and cost-effectiveness in wastewater treatment.

In March 2023, Toray Industries launched its latest high-performance reverse osmosis membrane with graphene coating, achieving a 32% increase in fouling resistance and reducing cleaning frequency by 18%. This advancement targets industrial wastewater reuse and desalination projects. Source: www.toray.com

In September 2023, Pentair announced the commercial rollout of its AI-integrated membrane management system, enabling real-time monitoring of membrane health and improving recovery rates by 15% in municipal treatment plants.

In January 2024, Koch Membrane Systems unveiled a modular wastewater RO system designed for rapid deployment, reducing installation time by 22% while improving membrane lifespan by 12%. This system is targeted toward industrial manufacturing facilities. Source: www.kochmembrane.com

In June 2024, LG Chem introduced its next-generation thin-film composite membranes optimized for high salinity wastewater, increasing salt rejection rates to over 99.6% and enhancing operational efficiency for large-scale facilities. Source: www.lgchem.com

The Wastewater Reverse Osmosis Membrane Market Report offers a comprehensive analysis of market dynamics, technology evolution, competitive landscape, and growth drivers. It covers detailed segmentation by type, application, and end-user, providing an in-depth view of thin-film composite membranes, high-flux membranes, and emerging graphene-based membranes. The report examines major applications such as municipal wastewater treatment, industrial effluent recycling, desalination, and specialized reuse projects, emphasizing performance metrics and adoption trends.

Geographically, the report covers key markets including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, analyzing each region’s adoption trends, regulatory frameworks, and technological advancements. It identifies market drivers such as stricter environmental regulations, water scarcity, and rising industrial wastewater reuse initiatives, alongside restraints including high capital costs and operational complexities. The report also explores emerging opportunities in modular RO systems, circular water economy projects, and AI-enabled process optimization. Competitive analysis includes profiles of leading players, strategic initiatives, and innovation trends. This scope equips decision-makers with a strategic perspective on current conditions and future pathways for the Wastewater Reverse Osmosis Membrane market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1060.87 Million |

|

Market Revenue in 2032 |

USD 2176.72 Million |

|

CAGR (2025 - 2032) |

9.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Toray Industries, Inc., Pentair plc, Koch Membrane Systems, Inc., LG Chem Ltd., Metito Group, Hydranautics, DuPont de Nemours, Inc., GE Water & Process Technologies, Ovivo Inc., LG Water Solutions |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |