Reports

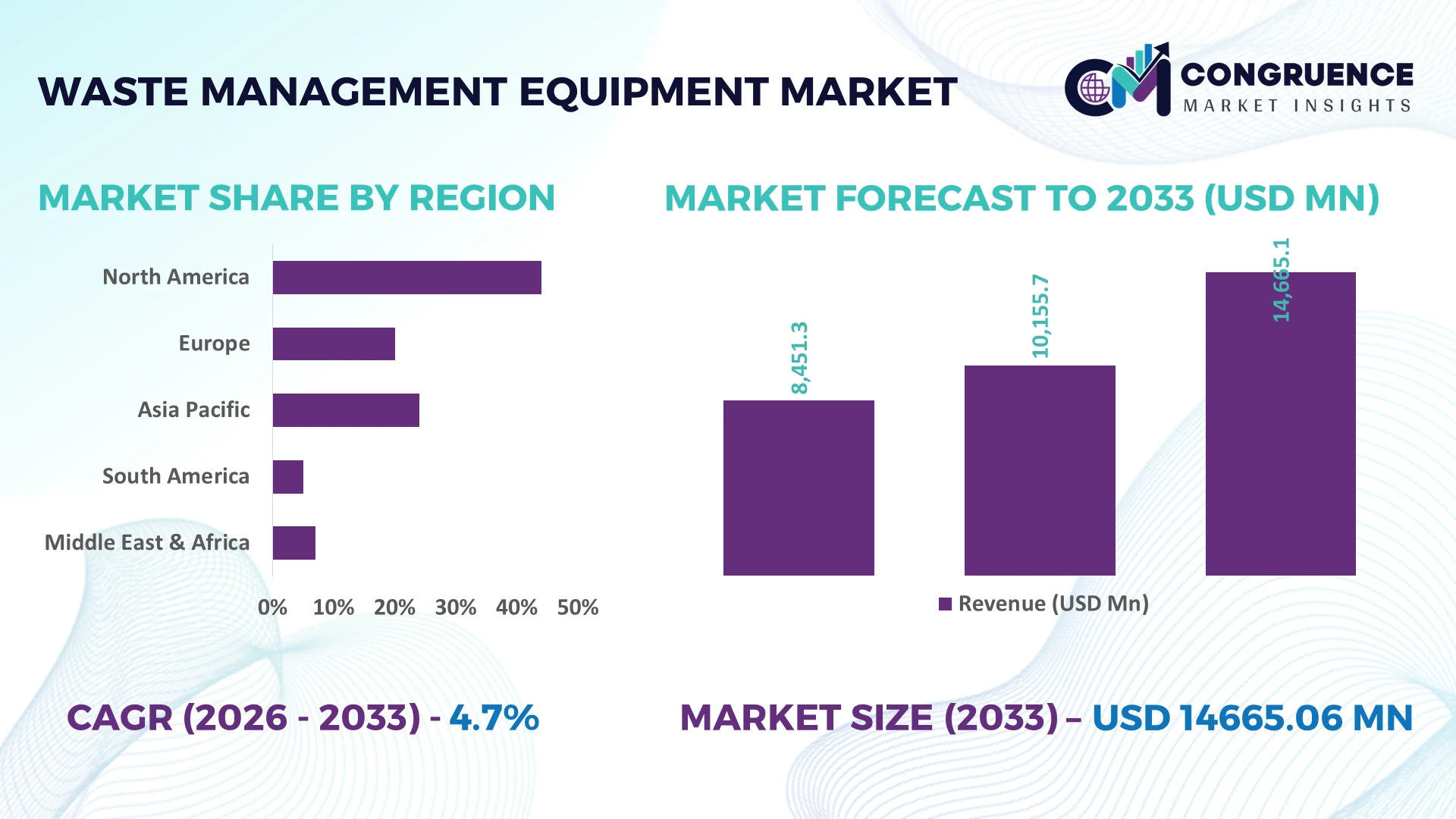

The Global Waste Management Equipment Market was valued at USD 10155.71 Million in 2025 and is anticipated to reach a value of USD 14665.06 Million by 2033 expanding at a CAGR of 4.7% between 2026 and 2033. Growth is supported by rising investments in automated material recovery facilities, stricter landfill diversion targets, expanding municipal solid waste processing capacity, and rapid deployment of AI-enabled sorting, electric collection equipment, and high-throughput recycling systems.

China remains the dominant country, accounting for approximately 30% of global waste treatment capacity, supported by large-scale municipal infrastructure investments and extensive manufacturing activity, while Germany leads Europe in advanced recycling equipment adoption with recycling rates exceeding 67%. Following continued global supply-chain diversification and post-pandemic infrastructure modernization through 2026, smart sensor integration across modern processing facilities has expanded by over 40%, strengthening operational efficiency and equipment utilization.

Manufacturers and investors should prioritize automated, digitally connected equipment platforms in high-capacity markets where regulatory compliance and processing efficiency increasingly determine long-term competitive positioning.

Market Size & Growth: USD 10155.71 million (2025) to USD 14665.06 million (2033) at 4.7% CAGR, driven by AI-enabled sorting equipment and recycling infrastructure modernization.

Top Growth Drivers: Automated sorting adoption +28%, recycling capacity expansion +22%, municipal infrastructure investment +18% accelerate global equipment demand.

Short-Term Forecast: By 2028, automated facilities improve material recovery efficiency by 20% while reducing operating costs by 15%.

Emerging Technologies: AI vision systems, robotic sorting, and electric waste collection fleets increase processing accuracy by over 30%.

Regional Leaders: Asia-Pacific approaches USD 6.3 billion, Europe USD 3.9 billion, North America USD 3.2 billion, supported by advanced recycling and circular economy initiatives.

Consumer/End-User Trends: More than 55% of large municipalities prioritize automated waste processing and smart fleet monitoring.

Pilot/Case Example: In 2026, an AI-enabled material recovery facility improved sorting accuracy by 35% and reduced manual handling requirements by 25%.

Competitive Landscape: Leading manufacturers collectively control about 38% of the global market alongside several regional equipment specialists expanding through localized production.

Regulatory & ESG Impact: Landfill diversion targets and emission standards increase recycled material recovery by over 20% across multiple developed markets.

Investment & Funding: More than USD 8 billion supports recycling infrastructure, automation upgrades, and regional manufacturing expansion amid global supply-chain realignment.

Innovation & Future Outlook: Autonomous collection vehicles, predictive maintenance, and digital twin platforms strengthen productivity while enabling high-growth circular waste management strategies.

Increasing deployment of automated collection vehicles, optical sorting systems, and connected fleet management platforms is reshaping operational performance across municipal and industrial waste operations. Recycling, construction, manufacturing, and commercial facilities remain the strongest demand centers, while AI-enabled equipment improves material recovery rates by more than 30%. Tightening environmental regulations and localized equipment manufacturing further reinforce long-term technology adoption, setting the stage for the strategic discussion.

The Waste Management Equipment Market has become strategically important as governments, industrial operators, and private waste service providers prioritize infrastructure modernization, circular economy targets, and digital waste tracking. Competitive advantage increasingly depends on deploying intelligent collection, sorting, and processing systems that improve throughput while lowering operational costs. Supply-chain restructuring since 2025 has encouraged manufacturers to localize component sourcing and expand regional production, reducing lead times by nearly 20% and improving equipment availability for municipal and industrial projects.

AI-enabled optical sorting systems now achieve material identification accuracy above 95%, compared with approximately 80% for conventional manual and mechanical sorting methods, while reducing labor requirements by nearly 30%. Japan emphasizes robotics and smart facility integration to maximize efficiency within limited land availability, whereas India is expanding large-scale municipal waste infrastructure to address rising urban waste volumes. Over the next two to three years, digital fleet monitoring and predictive maintenance adoption is expected to exceed 50% among major municipal operators, improving equipment uptime and reducing maintenance interruptions.

A practical example is the deployment of connected material recovery facilities integrating AI vision, automated conveyors, and sensor-based monitoring, enabling higher recycling output with fewer operational disruptions. Equipment manufacturers are strengthening competitiveness through technology partnerships, localized assembly, and software-enabled service models that create recurring value beyond hardware sales. Organizations capable of combining automation, digital intelligence, and sustainable operations will secure stronger long-term positioning as procurement increasingly prioritizes lifecycle performance rather than equipment acquisition alone.

Rapid modernization of municipal waste infrastructure and industrial recycling operations is accelerating demand for advanced waste management equipment. More than 60% of newly commissioned material recovery facilities now incorporate automated sorting technologies, while AI-enabled systems improve material recovery efficiency by over 30% and reduce contamination by approximately 25%. China continues expanding integrated waste treatment infrastructure through large-scale urban development programs, encouraging equipment suppliers to increase localized manufacturing capacity. This structural shift improves processing efficiency, lowers operating costs, and strengthens compliance with stricter environmental standards. Leading companies are responding through robotics investments, digital platform integration, and strategic partnerships that combine equipment manufacturing with predictive maintenance and lifecycle service capabilities, creating stronger customer retention and operational differentiation.

Uneven infrastructure development and component supply volatility continue limiting efficient equipment deployment across several developing economies. Delivery timelines for specialized automation components remain approximately 15% longer than pre-disruption levels, while imported electronic systems increase procurement costs by nearly 18% for some equipment categories. India and several emerging industrial markets still face limited high-capacity processing infrastructure, slowing equipment utilization despite rising waste volumes. These constraints directly affect project scalability, maintenance planning, and contractor profitability. Manufacturers are reducing exposure by localizing component production, expanding multi-supplier procurement strategies, and securing long-term supply agreements for electronic controls, hydraulic systems, and industrial sensors to improve production stability and cost predictability.

The integration of AI, industrial IoT, and digital asset management platforms creates significant opportunities beyond conventional equipment sales. Smart fleet management reduces fuel consumption by approximately 15%, while predictive maintenance lowers unexpected equipment downtime by nearly 25%. Germany is accelerating deployment of digitally connected recycling facilities under circular economy initiatives, encouraging equipment manufacturers to integrate software, analytics, and automation into complete operational ecosystems. Companies are increasing investment in modular equipment architecture, robotics research, and cloud-enabled monitoring platforms that support remote diagnostics and continuous optimization. This transition enables recurring service revenue while strengthening customer relationships through measurable productivity improvements and data-driven operational performance.

Integrating advanced waste management equipment across diverse municipal systems, private contractors, and recycling facilities remains a major execution challenge. More than 40% of legacy facilities operate with incompatible monitoring platforms, increasing system integration complexity and extending implementation schedules. Growing digital connectivity also expands cybersecurity exposure for connected processing equipment and fleet management networks, requiring stronger protection of operational technology environments. The United States continues upgrading aging waste infrastructure, but interoperability between legacy assets and intelligent automation remains inconsistent. Equipment suppliers must invest in standardized communication protocols, workforce training, cybersecurity capabilities, and scalable software architectures to ensure reliable deployment, maintain operational continuity, and preserve long-term competitiveness across increasingly connected waste management ecosystems.

Smart Sorting System Expansion AI-enabled optical sorting has become a standard upgrade across modern recycling facilities, improving material identification accuracy beyond 95% while reducing manual sorting requirements by nearly 30%. Labor shortages and stricter recycling quality standards are accelerating deployment, prompting equipment manufacturers to expand robotics partnerships and integrate machine vision software into complete processing lines for higher throughput and lower contamination.

Fleet Electrification Gains Momentum Electric waste collection vehicles now represent more than 18% of new municipal procurement programs in several developed countries, while connected route optimization reduces fuel consumption by approximately 15% and collection time by 12%. Companies are restructuring service operations through telematics integration, battery partnerships, and predictive maintenance platforms to improve fleet availability amid tightening emission regulations.

Modular Equipment Deployment Accelerates Demand is shifting toward modular compactors, shredders, and sorting systems that reduce installation time by nearly 25% and improve operational flexibility by over 20%. Industrial facilities increasingly prefer scalable equipment configurations that support phased capacity expansion. Manufacturers are responding by standardizing component platforms, regionalizing production, and offering configurable systems that shorten project implementation cycles.

Digital Lifecycle Service Models Equipment suppliers are expanding beyond hardware by embedding remote diagnostics, predictive analytics, and cloud-based asset management into service contracts. Connected monitoring reduces unplanned downtime by approximately 22% while increasing maintenance scheduling efficiency by nearly 28%. Large enterprises in Germany and Japan are strengthening long-term supplier partnerships focused on performance guarantees, software upgrades, and lifecycle optimization instead of one-time equipment procurement.

Sorting Equipment represents the leading segment because automated material separation has become essential for improving recycling efficiency, regulatory compliance, and operational productivity. Modern optical sorting platforms deliver over 95% identification accuracy while reducing contamination by approximately 30%, making them the preferred investment for municipal recovery facilities and industrial recycling plants. Compactors remain widely deployed for volume reduction and transportation efficiency, while Balers continue supporting recyclable material handling through improved storage density and logistics optimization. Crushers retain strategic importance in construction and demolition waste processing where material recovery is increasingly prioritized.

Shredders are emerging as the fastest-growing equipment category as industrial recycling, electronic waste processing, and secure material destruction expand. Advanced shredding systems improve processing throughput by nearly 25% while lowering downstream sorting requirements. Manufacturers are strengthening product portfolios through AI integration, modular equipment architecture, and localized production strategies that improve service responsiveness. Investment priorities increasingly favor intelligent equipment capable of integrating with digital monitoring platforms, creating stronger operational visibility and long-term asset performance.

Recycling remains the leading application as governments and industrial operators prioritize resource recovery, landfill diversion, and circular material flows. Automated recycling facilities now process approximately 35% more recoverable material than conventional operations using advanced sorting and material handling equipment. Waste Collection continues representing a large installed equipment base where fleet modernization and digital route optimization improve operational efficiency. Waste Processing facilities increasingly integrate automated conveying, shredding, and separation systems to maximize recovery while reducing manual intervention.

Waste Processing is the fastest-growing application as integrated facilities adopt robotics, AI inspection, and automated material recovery technologies. Composting gains momentum through expanding organic waste diversion programs, while Landfills increasingly deploy compactors and monitoring systems focused on extending site utilization and environmental compliance. Equipment manufacturers are scaling automation platforms, expanding service networks, and introducing integrated processing solutions that address multiple waste streams. Demand is steadily shifting toward facilities capable of combining collection, processing, and recycling into unified operational ecosystems.

Municipalities remain the dominant end-user because public waste collection, transfer stations, and recycling infrastructure require continuous investment in high-capacity equipment. More than 60% of large urban waste modernization projects include automated compactors, sorting systems, or connected fleet technologies. Waste Management Companies closely follow, expanding equipment fleets to improve operational efficiency and meet stricter service-level agreements. Manufacturing facilities increasingly deploy specialized shredders and compactors to manage production waste internally while improving resource recovery performance.

Recycling Companies represent the fastest-growing end-user segment as higher-quality material recovery becomes commercially important. Automated processing increases sorting productivity by approximately 30%, encouraging operators to invest in intelligent equipment and digital monitoring systems. Construction companies continue adopting crushers and shredders for demolition waste recovery, while manufacturers respond through customized equipment packages, flexible financing models, and long-term maintenance agreements. Competitive positioning increasingly depends on delivering application-specific systems that improve operational efficiency while supporting evolving sustainability objectives.

North America accounted for the largest market share at 34.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 5.8% CAGR between 2026 and 2033.

Strategic Modernization Through Intelligent Waste Infrastructure

North America maintains the highest market share due to extensive municipal infrastructure, advanced recycling networks, and widespread deployment of automated waste processing equipment. More than 65% of large municipal material recovery facilities have adopted AI-assisted sorting or digital monitoring platforms, improving operational efficiency and reducing manual intervention. Fleet electrification, predictive maintenance, and smart routing continue reshaping waste collection operations. Public-private partnerships supporting recycling infrastructure upgrades and automated transfer stations have accelerated equipment replacement cycles, while manufacturers are expanding service-based maintenance models and localized component supply to improve fleet uptime and operational resilience.

United States Market Outlook: The United States leads the regional market through large-scale municipal procurement, extensive private waste management operations, and continuous investment in automated processing facilities. More than 70% of high-capacity recycling facilities utilize advanced optical sorting or robotic handling technologies. Equipment manufacturers continue strengthening domestic production, digital service platforms, and long-term maintenance agreements to improve operational performance while supporting stricter environmental compliance and circular resource management objectives.

Circular Economy Policies Accelerate Technology Deployment

Europe remains a highly advanced market driven by strict recycling regulations, landfill diversion policies, and modernization of waste processing infrastructure. Approximately 58% of newly upgraded municipal recycling facilities now integrate automated sorting technologies and intelligent material handling systems. Equipment demand increasingly favors energy-efficient compactors, shredders, and connected processing equipment capable of improving resource recovery. Manufacturers are expanding technology collaborations and localized engineering capabilities while integrating automation with digital monitoring platforms to enhance equipment utilization and regulatory compliance across industrial and municipal applications.

Germany Market Outlook: Germany serves as the regional technology leader through advanced recycling infrastructure, strong engineering capabilities, and broad industrial automation adoption. Recycling rates exceeding 67% continue driving investment in intelligent sorting, high-capacity shredding, and digital process control systems. Domestic equipment manufacturers increasingly focus on robotics integration, predictive maintenance software, and modular equipment platforms that strengthen operational efficiency while supporting evolving circular economy requirements.

Urban Infrastructure Expansion Drives Equipment Scale

Asia-Pacific represents the fastest-expanding market as rapid urbanization, industrialization, and infrastructure investment increase demand for advanced waste management systems. More than 45% of newly commissioned waste processing projects incorporate automated sorting or intelligent monitoring technologies, reflecting accelerated modernization across major urban centers. Manufacturing capacity expansion, localized equipment production, and government-supported waste infrastructure programs continue improving deployment speed and reducing procurement costs. Companies are strengthening regional supply chains while expanding production facilities to meet increasing municipal and industrial equipment requirements.

China Market Outlook: China dominates the regional market through extensive municipal infrastructure development, strong manufacturing capabilities, and large-scale deployment of integrated waste processing facilities. The country accounts for approximately 30% of global waste treatment capacity, encouraging sustained investment in AI-enabled sorting equipment, automated recycling systems, and high-capacity processing technologies. Domestic manufacturers continue expanding intelligent equipment portfolios while increasing exports to emerging infrastructure markets.

Infrastructure Upgrades Strengthen Operational Demand

South America is experiencing steady equipment adoption as municipalities modernize collection systems and expand recycling capacity to address growing urban waste volumes. Approximately 22% of newly approved municipal waste projects include automated processing equipment or digital fleet management capabilities. Although infrastructure disparities remain across several countries, investment in transfer stations, recycling facilities, and waste logistics is improving equipment utilization. Manufacturers are supporting market expansion through distributor partnerships, localized service networks, and modular equipment solutions designed for varied operational conditions.

Brazil Market Outlook: Brazil leads the regional market through its extensive municipal waste generation, expanding recycling initiatives, and improving urban infrastructure. Large metropolitan areas continue investing in automated compactors, transfer stations, and waste processing equipment to improve operational efficiency. Equipment suppliers are strengthening regional partnerships, expanding technical support networks, and introducing adaptable product configurations that meet diverse municipal and industrial waste management requirements across the country.

National Infrastructure Programs Reshape Waste Operations

The Middle East & Africa market is advancing through government-backed infrastructure modernization, smart city development, and increasing investment in integrated waste management systems. Around 20% of newly planned urban infrastructure projects now incorporate automated waste collection or processing technologies. Growing emphasis on landfill diversion, recycling capacity, and operational efficiency encourages deployment of intelligent equipment across municipal and commercial applications. Equipment suppliers are expanding regional partnerships, service capabilities, and localized technical support to strengthen long-term project execution and operational reliability.

Saudi Arabia Market Outlook: Saudi Arabia leads regional investment through national infrastructure development, industrial diversification, and large-scale environmental modernization programs. Advanced waste processing facilities and smart municipal projects increasingly deploy automated compactors, sorting systems, and connected fleet technologies. Equipment manufacturers are expanding local partnerships, technical training programs, and after-sales service capabilities to support rising deployment volumes while improving operational efficiency and long-term infrastructure performance.

The competitive landscape is shaped by Caterpillar Inc., Komatsu Ltd., Terex Corporation, Dover Corporation, and McCloskey International, competing against specialized regional equipment manufacturers and automation-focused technology providers. Global OEMs compete on integrated product portfolios, digital service capabilities, and manufacturing scale, while regional players focus on customized equipment, faster delivery, and lower ownership costs. The top five participants collectively account for approximately 36% of market activity, creating a moderately consolidated structure. Competition increasingly centers on automation, lifecycle support, and localized supply chains rather than equipment pricing alone. AI-enabled sorting solutions improve processing efficiency by over 30%, while predictive maintenance reduces unplanned downtime by nearly 22%, giving technology leaders a measurable operational advantage. Companies are expanding production facilities, forming software partnerships, strengthening dealer networks, and vertically integrating component manufacturing to secure supply continuity. The competitive shift favors intelligent equipment ecosystems over standalone machinery, raising entry barriers through software integration, service infrastructure, and engineering expertise. Winning requires scalable automation, localized manufacturing, digital service capability, and dependable lifecycle performance.

Caterpillar Inc.

Komatsu Ltd.

Terex Corporation

Dover Corporation

McCloskey International

SSI Shredding Systems, Inc.

TOMRA Systems ASA

Machinex Industries Inc.

CP Manufacturing, Inc.

BHS-Sonthofen GmbH

Komptech GmbH

Eggersmann GmbH

Lindner Recyclingtech GmbH

Bollegraaf Recycling Solutions

Automation, artificial intelligence, and industrial IoT are redefining waste management equipment performance across collection, sorting, and processing operations. AI-powered optical sorting systems now achieve material recognition accuracy above 95%, improving recovery efficiency by more than 30% compared with conventional mechanical sorting. Over 45% of newly commissioned large material recovery facilities incorporate connected sensors and cloud-based monitoring, enabling operators to optimize throughput, reduce contamination, and improve equipment utilization. Manufacturers integrating digital control platforms gain stronger differentiation through higher processing consistency and data-driven operational management.

Emerging technologies focus on robotics, autonomous material handling, predictive maintenance, and digital twin platforms. Predictive maintenance reduces unexpected downtime by approximately 25%, while robotic sorting lowers manual labor requirements by nearly 30%. Compared with legacy maintenance models, connected diagnostic platforms shorten repair cycles by almost 20% and improve asset availability. Global equipment leaders benefit most by integrating software, automation, and service contracts into complete operational ecosystems that strengthen customer retention and recurring value creation.

Between 2026 and 2028, autonomous waste collection systems, edge AI, and modular processing platforms will become mainstream across large municipal and industrial facilities. Adoption of intelligent fleet management is expected to exceed 55% among advanced operators, improving route efficiency and reducing fuel consumption by approximately 15%. Companies investing early in software-enabled equipment, cybersecurity, and interoperable automation platforms will secure faster project deployment, stronger operational resilience, and sustainable competitive positioning as procurement increasingly prioritizes lifecycle performance over standalone equipment specifications.

March 2026 – Machinex expanded its strategic partnership with Coastal Waste & Recycling to deliver four advanced Material Recovery Facility (MRF) projects across Florida, with two additional systems scheduled to begin operations in 2026. The expansion strengthens long-term recycling infrastructure capacity and reinforces Machinex's turnkey automation leadership.

May 2025 – TOMRA launched its next-generation Event Solution for reusable cups at Oslo's Intility Arena, supporting high-volume collection and reuse operations. The digital system is designed for venues handling up to 20,000 visitors, demonstrating scalable circular waste collection technology with lower single-use packaging dependency.

March 2026 – TOMRA partnered with Sulayr to advance tray-to-tray food packaging recycling through automated sorting technology. The collaboration targets high-purity food-grade material recovery, improving recycled plastic quality while supporting closed-loop packaging systems across commercial recycling operations.

February 2026 – SWANA and the Environmental Research & Education Foundation (EREF) signed a Memorandum of Understanding to strengthen research, education, and technical collaboration across the waste and resource management sector. The initiative expands industry knowledge-sharing through joint programs, supporting improved operational practices and workforce development.

The report delivers comprehensive analysis across the complete waste management equipment value chain, covering major equipment types including compactors, balers, shredders, crushers, and sorting equipment. It evaluates applications spanning waste collection, recycling, landfills, composting, and waste processing, together with demand across municipalities, recycling companies, manufacturing, construction, and waste management companies. The assessment includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while examining automation, AI-enabled sorting, digital fleet management, and intelligent processing technologies shaping modern operations.

The study benchmarks more than 10 leading industry participants, analyzes evolving deployment patterns, technology adoption, competitive positioning, and regional investment priorities between 2026 and 2033. It highlights operational trends such as increasing automation adoption, modular equipment deployment, predictive maintenance integration, and localized manufacturing strategies. The report supports investment planning, product portfolio optimization, market expansion, partnership evaluation, and competitive decision-making by identifying high-priority segments, emerging deployment opportunities, and strategic technology pathways across mature and developing waste management ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 10155.71 Million |

Market Revenue in 2033 | USD 14665.06 Million |

CAGR (2026 - 2033) | 4.7% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Caterpillar Inc., Komatsu Ltd., Terex Corporation, Dover Corporation, McCloskey International, SSI Shredding Systems, Inc., TOMRA Systems ASA, Machinex Industries Inc., CP Manufacturing, Inc., BHS-Sonthofen GmbH, Komptech GmbH, Eggersmann GmbH, Lindner Recyclingtech GmbH, Bollegraaf Recycling Solutions |

Customization & Pricing | Available on Request (10% Customization is Free) |