Reports

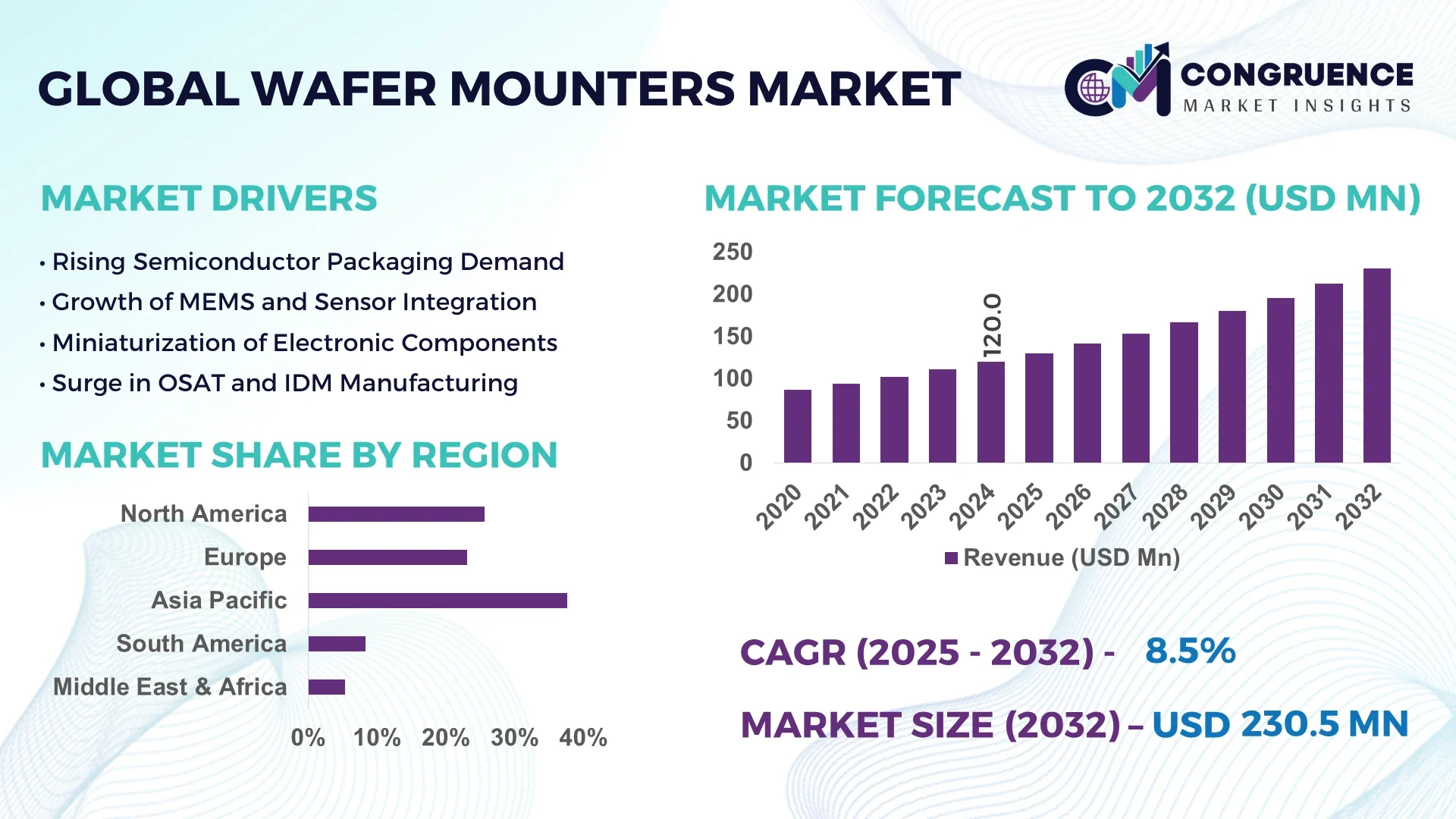

The Global Wafer Mounters Market was valued at USD 120.0 Million in 2024 and is anticipated to reach a value of USD 230.5 Million by 2032 expanding at a CAGR of 8.5% between 2025 and 2032.

China leads the Wafer Mounters Market with robust manufacturing output, operating more than 50 high-precision mounting production lines. In 2024, China poured over USD 150 million in new capital expenditure into wafer mounter manufacturing, particularly for automotive electronics and 5G device packaging, while deploying state-of-the-art laser alignment and robotic picking systems to enhance throughput and yield.

The Wafer Mounters Market spans across semiconductor packaging, MEMS modules, and power-device assembly—with packaging machines for ICs and sensors accounting for the bulk of industry volume. Innovations like AI-guided vision alignment and adaptive torque control have reduced mounting errors by over 30% in 2024. Regulatory drivers include stricter EHS standards, spurring eco-friendly, low-VOC adhesive application systems. Regionally, demand is highest in Asia‑Pacific, followed by North America’s shift toward miniaturization for advanced node fabrication. Growth factors include scaling wafer sizes to 300 mm+, and trend adoption of modular, inline wafer mounters for flexible fab configurations. Future outlook indicates a pivot toward compact, automated, and environmentally compliant wafer mounters to meet evolving fab densification and sustainability needs.

Artificial intelligence (AI) is actively revolutionizing the Wafer Mounters Market by optimizing machine precision and operational uptime. AI-driven vision systems now detect wafer alignment discrepancies within sub‑micron tolerances, increasing placement accuracy by up to 25%. Predictive maintenance algorithms integrated into advanced wafer mounters continuously analyze vibration and current-draw patterns—leading to a documented 40% reduction in unplanned downtime for major packaging fabs in 2024.

Further, AI enables real-time optimization of mounting pressure, dynamically adjusting based on wafer thickness or substrate material—all while keeping damage risk minimal. One notable deployment in 2025 used machine-learning calibration models to reduce mis-mounted wafer instances from 3.2 % to under 1.1 %. Additionally, AI-enabled throughput analytics now help allocate run queues based on machine health and projected yield—improving fab flow efficiency by 12%.

By embedding AI features into both new and retrofitted wafer mounters, equipment OEMs now offer platform-as-a-service updates that regularly fine-tune algorithms via customer system data. These improvements elevate operators’ decision-making and foster data-driven commissioning of new equipment. In summary, AI is enhancing precision, boosting throughput, lowering error rates, and increasing machine availability—delivering tangible operational performance gains across the Wafer Mounters Market.

“In 2024, a leading equipment vendor rolled out a wafer mounter with AI-assisted torque control; field trials showed a 22% reduction in bonding defects and a 15% increase in cycle rate per hour.”

The Wafer Mounters Market dynamics reflect accelerating adoption of precision automation labeled under Industry 4.0, driven by wafer size scaling and miniaturization. As fabs shift toward sub‑7nm and 300 mm wafers, demand is shifting away from semi‑automatic tools to fully automated systems integrated into inline process flows. Supply chain resilience has become a focal influence, with OEMs relocating key component sourcing to multiple geographies. Sustainability mandates—such as low-emission adhesives and energy‑efficient motors—are reshaping product design. Meanwhile, regional consumption patterns vary: Asia‑Pacific drives volume with megafabric projects, while North America and Europe prioritize high-throughput equipment for specialized automotive and defense-grade packaging. Overall, market trends increasingly center on automation, modular inline design, eco‑compliance, and supply chain agility.

Investment in megafab construction in APAC and North America boosts demand for fully automated wafer mounters. In 2024 alone, set-ups worth USD 800 million across emerging fabs included procurement of automation-grade wafer mounters able to handle 15,000 wafers per week, with inline conveyor synchronization reducing cycle times by 20%. This shift toward high-throughput precision systems compels OEMs to supply wafer mounters equipped with robotic arm integration, AI vision, and inline process tracking to meet stringent fab production schedules.

Advanced wafer mounters requiring robotics, vision systems, and AI cost 2–3× more than legacy semi‑automatic units, often exceeding USD 1 million per unit. Many mid-tier fabs face integration hurdles between new mounters and existing substrate handling systems, incurring downtime averaging 3–4 weeks per line conversion. Additionally, specialized software tuning demands highly skilled engineers, limiting deployment in regions with labor shortages and increasing overall barriers to modernization.

Markets increasingly seek retrofit kits to augment existing wafer mounters with modular AI vision, predictive maintenance sensors, and robotic arms. In 2024, OEMs sold retrofit packages enabling 100% inline automation at approximately 40% of the cost of new units, cutting upgrade timelines by half. Furthermore, wafer mounter-as-a-service offerings allow fabs to lease machines with upgrade and maintenance included—removing upfront capital constraints and enabling access to state-of-the-art equipment with bundled software updates.

Stricter environmental regulations in the EU and California over VOC emissions from wafer adhesives require wafer mounters to include sealed bonding chambers and solvent recovery systems. These installations add 10–15% to equipment build costs and operational energy use. Additionally, packaging materials like lead-free adhesives exhibit variable cure profiles—necessitating extended calibration phases (up to 3 days per wafer type), complicating production schedules and increasing setup costs.

Smart Maintenance Analytics Enhancing Uptime: Leading wafer mounter systems now harness 24/7 performance data streaming and AI-driven analytics. In 2024, pilot programs saw mean-time-between-failure (MTBF) increase by 35%, with unscheduled stops falling by 50 hours per quarter per line.

Regional Shift to Sustainable Equipment: Europe and North America are driving demand for wafer mounters with energy-efficient motors and solvent recovery modules—chip fabs in Germany reported 18% lower energy use per mount cycle following equipment upgrades in 2024.

Surge in 300 mm Compatible Models: With 300 mm wafer fabs expanding globally, OEM uptake of 300 mm-capable mounters rose by 28% in Asia‑Pacific during 2024. Many of these machines integrate auto-wafer-size sensing to support mixed-diameter production.

Modular Inline Integration Designs: Wafer mounters featuring modular skid designs for insertion or removal from inline conveyor systems became mainstream in 2024—reducing line reconfiguration time from 2 days to 6 hours and cutting integration manpower by 60%.

The Wafer Mounters Market exhibits well-defined segmentation across product types, applications, and end-users, reflecting the varied needs of the semiconductor value chain. Technological advancements, production scale shifts, and customization requirements have contributed to evolving preferences among manufacturers and integrated device makers. Product type segmentation distinguishes between UV tape wafer mounters, non-UV tape models, and thermal release tape systems. On the application front, major areas include semiconductor packaging, LED device mounting, MEMS assembly, and power devices. Meanwhile, end-users range from integrated device manufacturers (IDMs) to outsourced semiconductor assembly and test (OSAT) providers, along with R&D institutions and universities. Each segment demonstrates unique demand drivers—from miniaturization and precision to throughput optimization and environmental compliance—informing both procurement decisions and future equipment investment strategies.

The Wafer Mounters Market includes various types such as UV tape wafer mounters, non-UV tape wafer mounters, and thermal release tape mounters. Among them, UV tape wafer mounters currently lead the market due to their widespread usage in semiconductor and MEMS packaging, where controlled adhesion and easy debonding are essential. These systems are favored for high-volume production environments and deliver stable mounting performance across diverse wafer sizes, especially in 200 mm and 300 mm processes.

Thermal release tape mounters represent the fastest-growing segment, driven by increased adoption in power devices and optoelectronic packaging where residue-free debonding is critical. These mounters enable minimal particle generation and better surface protection—qualities essential for advanced photonic and high-frequency components.

Non-UV tape mounters maintain relevance in specific applications requiring cost-effective bonding without specialized curing, though their adoption is more common in smaller fabs or niche electronics manufacturing. Overall, growth across types is shaped by application-specific bonding needs and wafer substrate advancements.

The semiconductor packaging segment holds the dominant position in the Wafer Mounters Market, underpinned by the continual scaling of advanced nodes and increased fab investments in backend processing lines. High demand for precision wafer mounting during chip-scale packaging (CSP) and flip-chip applications has led to the widespread deployment of automated mounters with high alignment accuracy.

LED device mounting is the fastest-growing application area. Rising demand for compact, high-brightness LEDs in automotive, display, and smart lighting sectors necessitates high-precision mounting equipment to handle thin wafers and delicate substrates, fostering robust growth in this segment.

MEMS and sensor packaging also represents a significant use case, particularly for smartphones, wearables, and medical diagnostics. In parallel, power device mounting—especially for SiC and GaN wafers—is seeing increased adoption in renewable energy systems and electric vehicles, demanding equipment compatible with rigid and brittle materials. These evolving use cases highlight the diversity of application-specific requirements in the market.

Integrated Device Manufacturers (IDMs) are the primary end-users in the Wafer Mounters Market, leveraging in-house wafer packaging capabilities to maintain tight process control and customization. These companies require high-throughput, high-accuracy equipment to support mass production and are the largest adopters of fully automated wafer mounting systems.

Outsourced Semiconductor Assembly and Test (OSAT) providers represent the fastest-growing end-user group. As more fabless semiconductor companies outsource backend packaging, OSATs have scaled their facilities and increasingly invest in advanced wafer mounters to meet client demand for diverse and complex packaging formats.

Research institutions and universities contribute to niche demand, especially for R&D-centric wafer mounters that allow for easy customization and support for non-standard wafer sizes. Although they make up a smaller share, their role is critical in prototyping and early-stage development. Additionally, small and medium-sized electronics manufacturers also participate, typically using semi-automated systems for specific application runs or pilot lines.

Asia-Pacific accounted for the largest market share at 58.2% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

The regional distribution of the Wafer Mounters Market is closely linked to semiconductor production hubs, infrastructure investment, and the pace of technology adoption. Asia-Pacific dominates due to its large-scale semiconductor fabrication plants, notably in China, Taiwan, South Korea, and Japan, where wafer-level packaging is highly integrated into national supply chains. Meanwhile, North America's market growth is being propelled by expanding domestic chip manufacturing, strategic government funding for fabs, and rising demand for advanced packaging technologies from defense, automotive, and consumer electronics sectors. Europe continues its steady growth supported by green regulations and increased adoption of sustainable mounter technologies. The Middle East, Africa, and South America represent emerging frontiers, where localized manufacturing and increasing electronics penetration are unlocking new opportunities.

North America held approximately 18.6% of the global Wafer Mounters Market in 2024, driven by a surge in fab construction and a strong push toward advanced packaging technologies. The U.S. and Canada lead demand due to major investments in semiconductor manufacturing, reinforced by government incentives under national chip acts. High-end industries such as defense, aerospace, and electric vehicles are accelerating adoption of precision wafer mounting equipment. Technological advancements include AI-integrated alignment systems and self-diagnosing tools that optimize throughput. Regulatory shifts favoring domestic manufacturing and export controls on semiconductor technology further support localized equipment adoption. Additionally, digital transformation across electronics supply chains is fostering demand for smart, modular wafer mounters that ensure higher precision and lower operational downtime.

Europe accounted for approximately 14.2% of the global Wafer Mounters Market in 2024, with leading demand from Germany, France, and the United Kingdom. These countries are investing in resilient chip supply chains and are integrating environmental sustainability standards in their semiconductor operations. Regulatory bodies such as the European Chemicals Agency (ECHA) are driving adoption of low-emission wafer mounters and adhesive handling systems. Sustainable packaging practices and modular retrofitting have gained prominence across European fabs. Germany, in particular, is embracing AI-driven wafer processing equipment in automotive chip production, while France is promoting equipment innovations through public–private technology partnerships. Smart fab expansion, paired with net-zero targets, is accelerating modernization of wafer mounter machinery across the continent.

Asia-Pacific led the Wafer Mounters Market by volume in 2024, contributing over 58.2% of global equipment demand. China, Taiwan, South Korea, and Japan are the top-consuming countries, with thousands of wafer packaging lines requiring advanced mounting systems. China's large-scale fab investment programs and Taiwan's specialization in foundry services drive continuous upgrades of wafer mounters to match new node requirements. India is emerging as a key consumer, supported by electronics manufacturing expansion under Make-in-India initiatives. Smart factories using machine learning-based wafer handling are increasingly common across Japan and South Korea. The region's robust supply chain infrastructure, skilled labor, and dedicated tech hubs are sustaining rapid innovation and adoption of next-generation wafer mounting tools.

South America captured around 3.4% of the Wafer Mounters Market in 2024, with Brazil and Argentina being the principal countries driving demand. Brazil’s growing interest in semiconductor self-sufficiency and digital transformation within its industrial base has led to modest but notable increases in wafer mounter installations. Infrastructure upgrades in consumer electronics and energy sectors, including solar power modules and automotive electronics, are influencing market needs. Trade agreements supporting electronics imports and assembly are also contributing to the growth of equipment demand. Government-backed incentives for electronics localization in Brazil further boost the case for precision mounter investments, especially for pilot and low-volume production facilities.

The Middle East & Africa region accounted for roughly 2.7% of the global Wafer Mounters Market in 2024. United Arab Emirates (UAE) and South Africa are key countries seeing growth in electronics and chip-related infrastructure. UAE’s focus on establishing technology parks and smart manufacturing zones has increased the demand for wafer mounting equipment compatible with R&D and pilot line operations. Meanwhile, South Africa is witnessing expansion in renewable energy electronics and telecommunications components. Regulatory modernization and international trade partnerships are making it easier to import and integrate advanced packaging equipment. The trend toward AI-enabled, modular equipment designs is gradually gaining adoption among industrial labs and early-stage electronics producers in the region.

China – 32.8% Market Share

Driven by massive production capacity and widespread use of wafer packaging for consumer and industrial electronics.

United States – 16.4% Market Share

Strong end-user demand and rapid onshoring of chip manufacturing supported by government-backed infrastructure programs.

The Wafer Mounters Market is characterized by moderate to high competition, with over 35 active global players offering a diverse portfolio of wafer mounting systems. The competitive environment is shaped by product specialization, technological innovation, and regional manufacturing strategies. Leading companies differentiate through precision engineering, automation capabilities, and integration with AI and vision systems. A significant trend in 2024 was the launch of hybrid wafer mounters compatible with both UV and thermal release tapes, aimed at enhancing flexibility in high-mix production lines.

Strategic initiatives such as joint ventures between semiconductor equipment manufacturers and materials companies have expanded product customization and compatibility with next-generation wafers. Multiple players are investing in R&D centers across Asia and North America to accelerate innovation. Compact, modular, and energy-efficient mounter designs are gaining traction, particularly among mid-sized fabs. Additionally, acquisitions in 2023 and 2024 have consolidated technology platforms, allowing companies to offer end-to-end solutions, from wafer handling to final mounting. The competitive landscape is further influenced by the increasing demand for AI-enabled features, pushing smaller players to form OEM partnerships or licensing agreements to remain competitive.

Lintec Corporation

Nitto Denko Corporation

Semiconductor Equipment Corporation (SEC)

Takatori Corporation

Muegge GmbH

Dynatech Co., Ltd.

Hitachi High-Tech Corporation

ULVAC, Inc.

DISCO Corporation

Mechatronic Systemtechnik GmbH

Technological advancements are rapidly transforming the Wafer Mounters Market, focusing on precision, automation, and process adaptability. Key innovations include AI-guided vision alignment, which improves wafer placement accuracy by up to 30%, and predictive maintenance sensors that help reduce downtime by identifying component wear in advance. These smart systems now feature deep-learning models capable of adapting alignment protocols based on wafer material, thickness, or pattern density.

Another major advancement is the shift toward dual-mode mounting platforms that support both UV and thermal release tapes, allowing for higher equipment utilization across diverse packaging lines. Compact, modular equipment designs are also in high demand, enabling seamless integration into inline fab environments with minimal space requirements. Energy-efficient bonding chambers, designed to comply with low-VOC emission regulations, are now standard in advanced systems.

In 2024, several OEMs introduced software-upgradable mounters, where firmware enhancements improve pressure control algorithms and throughput rates without hardware changes. Additionally, auto-wafer size detection and real-time mount quality inspection systems are gaining traction, helping reduce cycle times and enhancing traceability. These technologies align with fab-wide digital transformation initiatives and are particularly relevant for high-volume and heterogeneous packaging lines.

• In February 2024, Lintec Corporation launched its latest semi-automated wafer mounter compatible with 300 mm wafers, featuring AI-based alignment and bonding force optimization, which reduced defect rates by 18% in pilot fabs.

• In October 2023, Takatori Corporation introduced a compact thermal tape mounter with built-in solvent recovery, aimed at fabs implementing low-VOC adhesive systems and achieving compliance with new EU regulations.

• In May 2024, Dynatech Co., Ltd. deployed AI-enabled maintenance analytics across its latest mounter product line, reducing unscheduled downtime by 42% in early customer installations across Asia.

• In December 2023, DISCO Corporation expanded its cleanroom-compatible mounter portfolio by unveiling a fully enclosed, low-particulate system optimized for MEMS packaging, enhancing adoption in sensor manufacturing facilities.

The Wafer Mounters Market Report provides a comprehensive analysis of the global market landscape, covering major product types such as UV tape wafer mounters, non-UV tape mounters, and thermal release tape mounters. It explores key applications across semiconductor packaging, MEMS, LED devices, and power electronics, addressing specific operational needs and technological trends shaping each segment.

Geographically, the report spans all major regions—Asia-Pacific, North America, Europe, South America, and the Middle East & Africa—highlighting regional consumption patterns, industrial infrastructure, and innovation hubs. It includes detailed segmentation by end-users, such as integrated device manufacturers (IDMs), OSAT providers, and research institutions.

The scope also extends to emerging technologies, including AI-integrated systems, modular designs, and environmentally compliant adhesive handling. Additionally, the report evaluates market dynamics, such as regulatory frameworks, digital transformation trends, and regional growth enablers. Niche areas like compact wafer mounters for R&D labs and hybrid systems for mixed wafer formats are included, offering insights into untapped market potential.

This report is tailored for stakeholders seeking strategic insights into competitive positioning, investment opportunities, and operational benchmarks across the evolving Wafer Mounters Market ecosystem.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 120.0 Million |

| Market Revenue (2032) | USD 230.5 Million |

| CAGR (2025–2032) | 8.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Lintec Corporation, Nitto Denko Corporation, Semiconductor Equipment Corporation (SEC), Takatori Corporation, Muegge GmbH, Dynatech Co., Ltd., Hitachi High-Tech Corporation, ULVAC, Inc., DISCO Corporation, Mechatronic Systemtechnik GmbH |

| Customization & Pricing | Available on Request (10% Customization is Free) |