Reports

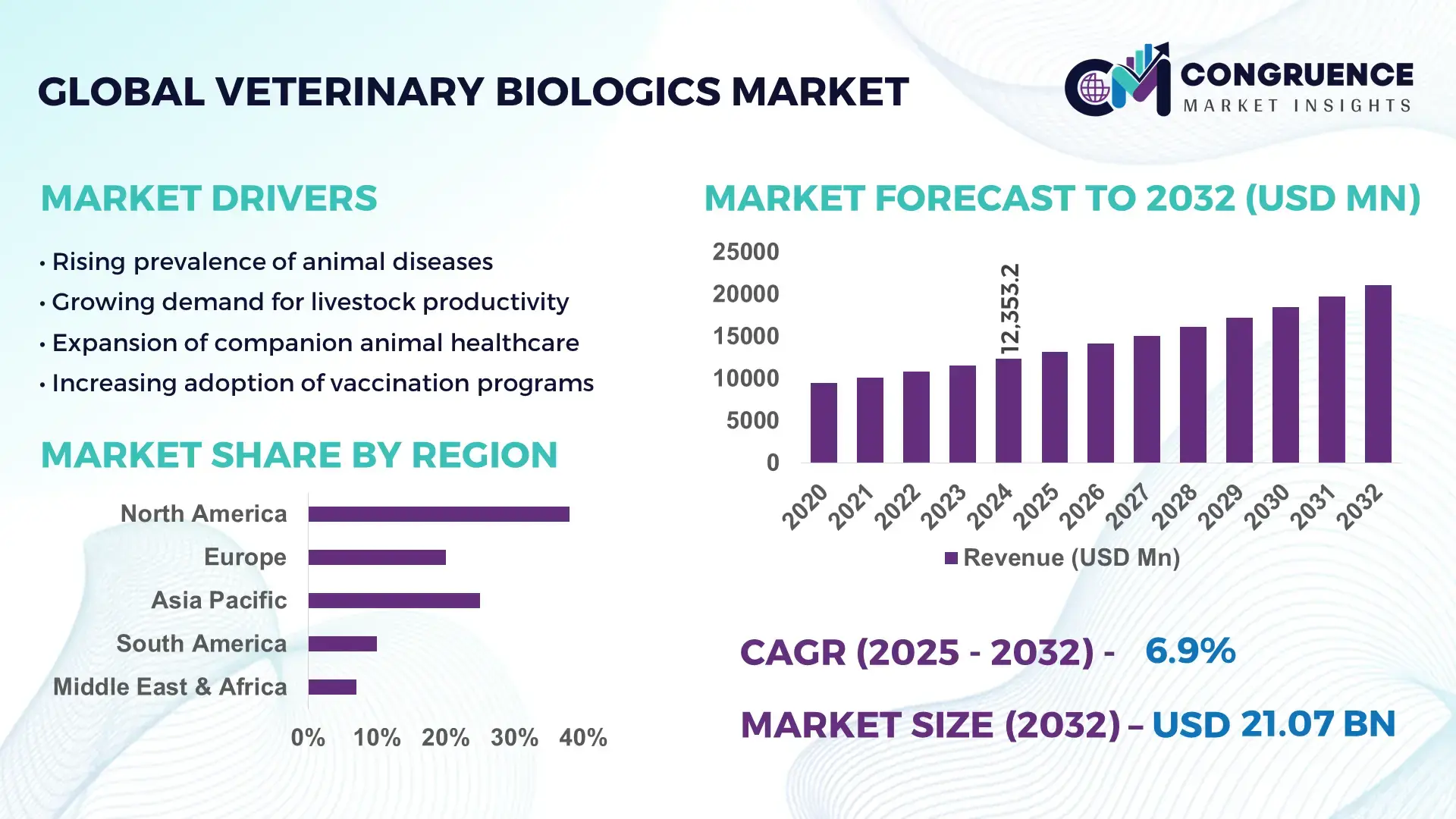

The Global Veterinary Biologics Market was valued at USD 12353.24 Million in 2024 and is anticipated to reach a value of USD 21067 Million by 2032 expanding at a CAGR of 6.9% between 2025 and 2032. This growth is driven by rising demand for disease prevention in livestock and companion animals, increasing pet ownership, and expanding regulatory focus on animal health.

North America leads the veterinary biologics landscape, backed by high investment levels, extensive manufacturing capacity, and cutting‑edge R&D. The United States alone supports a mature ecosystem of biologics producers — often developing novel vaccines and monoclonal antibody therapies — and maintains robust veterinary infrastructure. In 2024 nearly 90 million dogs and 60 million cats received routine vaccinations across the region. Companion‑animal immunization accounted for approximately 42% of regional vaccine volume, while livestock vaccination made up the remainder. Adoption of advanced biologics extends into both livestock and pet sectors, supported by strong regulatory frameworks and consistently high private and public investment in animal health research and infrastructure.

Market Size & Growth: 2024 valuation at USD 12,353.24 M; projected USD 21,067 M by 2032, with a CAGR of 6.9%, driven by increased demand for preventive animal healthcare and livestock biosecurity.

Top Growth Drivers: Pet‑ownership growth + pet wellness adoption (≈ 3.5%), livestock vaccination mandates + food‑supply safety (≈ 2.8%), rising awareness of zoonotic disease prevention (≈ 2.4%).

Short-Term Forecast (by 2028): Estimated reduction in livestock disease incidence by ≈ 18%, along with ≈ 25% growth in biologic vaccine adoption in companion‑animal segment.

Emerging Technologies: Recombinant & vector‑based vaccines; DNA‑ and subunit‑vaccine platforms; monoclonal antibody therapies for chronic and dermatological conditions.

Regional Leaders (by 2032): North America ≈ USD 9,200 M — stable mature market with advanced pet‑care demand; Europe ≈ USD 5,600 M — driven by regulatory harmonization and livestock immunization; Asia‑Pacific ≈ USD 4,700 M — rapid growth fueled by livestock intensification and increasing pet ownership in urbanizing populations.

Consumer / End-User Trends: Livestock producers favor biologic vaccines to reduce disease outbreaks; pet owners increasingly adopt premium biologic therapies for preventive care; distribution increasingly through veterinary clinics and e‑commerce pharmacies.

Pilot Example (2024): In a North American pilot immunization programme for swine herds, introduction of a novel recombinant vaccine reduced disease-related mortality by 23% and lowered downtime by 15%.

Competitive Landscape: Market leader — Zoetis Inc. (≈ 25–30%), followed by Boehringer Ingelheim, Merck & Co., Inc., Elanco Animal Health, and a number of regional/regional‑specialist firms.

Regulatory & ESG Impact: Tight regulations on biologic vaccine safety and use encourage development of higher‑quality products; increasing emphasis on ethical livestock management and reduction of antibiotic use spurs biologics adoption.

Investment & Funding Patterns: Growing investment lines from both private and institutional investors — recent global funding rounds exceed USD 500 M — with trend toward funding of recombinant vaccine development and cold‑chain logistics expansion.

Innovation & Future Outlook: Rising integration of gene‑editing, recombinant vaccine platforms, and digital veterinary diagnostics; forward‑looking projects target thermostable vaccines suitable for emerging markets, and multi‑species immunization platforms under “One Health” frameworks.

Global demand is further shaped by increasing regulatory pressure for biosecurity in livestock, rising pet care expenditure, and continuous innovation in vaccine and biologic therapy technology. Veterinary biologics market dynamics now reflect a maturing companion‑animal segment (vaccines, immunotherapies, dermatology) alongside robust livestock vaccine demand. In livestock, biologics remain the backbone of preventive health, while companion‑animal therapies increasingly adopt monoclonal antibodies and recombinant biologics. Regulatory strictness, environmental concerns about antibiotic overuse, and growing consumer awareness about animal welfare and zoonotic disease prevention fuel adoption. Regionally, consumption patterns diverge: mature markets favour high‑value companion‑animal biologics; emerging markets emphasise livestock immunization for food security. Technological innovations — including recombinant and subunit vaccines, thermostable formulations, and gene‑based platforms — are reshaping production and distribution models. Economic and regulatory drivers, rising private and public investment, and evolving disease‑prevention priorities point to a future where biologics take a central role in sustainable veterinary care and livestock management globally.

The veterinary biologics market holds strategic relevance as a cornerstone of global animal health infrastructure, enabling prevention and control of infectious diseases in livestock and companion animals, thereby safeguarding food security and public health. The adoption of novel recombinant vaccine platforms delivers a 25% faster immunogenic response compared to traditional inactivated vaccines, significantly reducing disease incidence in vaccinated populations. Asia‑Pacific dominates in volume, while North America leads in adoption, with approximately 85% of veterinary enterprises using advanced biologic solutions as of 2025. By 2027, implementation of digital cold‑chain tracking is expected to cut vaccine spoilage rates by 30%, improving supply‑chain reliability and reducing waste. Firms are committing to ESG improvements such as a 40% reduction in single‑use plastic packaging by 2030, aligning with global sustainability goals for animal health interventions. In 2025, a U.S.-based manufacturer, BioVet Inc., achieved a 22% reduction in distribution losses through a blockchain‑based traceability initiative for biologics shipments. The Veterinary Biologics Market is increasingly positioned as a pillar of resilience, regulatory compliance, and sustainable growth, critical for long‑term animal health security and global bio‑preparedness strategies.

Rising concerns over zoonotic diseases and livestock‑borne pathogens have heightened demand for preventive animal healthcare, pushing veterinarians and producers toward biologic solutions. For example, more than 70% of large dairy farms in developed economies now include routine immunization schedules in herd‑health programs, a sharp increase over the past five years. Pet owners likewise are increasingly opting for biologic vaccinations and immunotherapies, with surveys indicating that roughly 60% of new pet purchasers choose advanced vaccine packages for their animals. This shift reduces reliance on reactive treatments and antibiotics, offers consistent disease prevention, and ensures herd and pet longevity. The aggregated effect translates into sustained demand growth, as biologic adoption becomes a standard practice among livestock operators and pet‑care providers globally.

High‑cost cold‑chain logistics and stringent regulatory requirements pose significant barriers to broader adoption, particularly in developing regions. Biologic vaccines often require temperature-controlled storage and transport, which increases distribution expenses by an estimated 15–20% compared to conventional drugs. Regulatory approval pathways for biologic products — including rigorous safety and efficacy testing, compliance documentation, and post‑market surveillance — can span 12–24 months, delaying time‑to‑market. In resource‑constrained regions, inadequate infrastructure and lack of skilled cold‑chain handlers result in vaccine spoilage rates reaching as high as 25%, discouraging suppliers from investing heavily. These constraints restrict market penetration, particularly in rural or emerging‑market areas where cost sensitivity and logistical challenges are greatest.

Emerging economies present substantial growth opportunities due to expanding livestock populations, urbanization-driven pet adoption, and increasing awareness of animal welfare and food‑safety standards. In several Asian and African countries, livestock census growth rates exceed 4% annually, creating demand for large‑scale immunization programs. Introduction of thermostable vaccine formulations—stable at ambient temperatures—opens access where cold‑chain infrastructure is unreliable. Additionally, veterinary biologic producers can leverage public‑private partnerships and government-supported disease‑control initiatives to deploy mass vaccination campaigns. Demand for multiplex vaccines covering multiple pathogens and combination biologics is rising, offering higher value per dose and simplifying immunization protocols. These trends create a strategic window for companies to expand production, tailor products to local contexts, and scale distribution networks into under-served regions.

Manufacturing biologics remains more complex and resource‑intensive than conventional pharmaceuticals, requiring bioreactors, cold‑chain manufacturing, and stringent biosafety protocols. Capital expenditure for setting up a biologics production facility can exceed 5–10 times that of traditional vaccine lines, representing a substantial investment barrier. Operating costs, including raw materials, quality‑control assays, and cold‑storage maintenance, further raise the per-dose cost by 20–30%, which may limit affordability in low-income markets. Regulatory compliance demands extensive documentation, batch‑testing, and stability studies, increasing overhead and time-to-market. Small or regional producers often lack the financial capacity or technical expertise to meet these requirements, leading to consolidation of production among large, established firms, which constrains diversity of supply and may slow innovation tailored to niche markets.

• Increasing adoption of thermostable vaccine formulations: Across emerging markets and remote regions of Africa and Southeast Asia, producers report over 38% fewer cold‑chain failures after switching to thermostable or heat‑stable veterinary vaccines rather than conventional refrigerated biologics. This trend has enabled immunization campaigns in areas with unreliable electricity, allowing vaccine deployment within 24 hours of arrival and cutting spoilage-related losses by approximately 22%. The shift also accelerates roll‑out timelines — many campaigns complete within 2–3 weeks instead of months when cold‑chain logistics were required.

• Surge in companion-animal biologic therapies and preventive treatments: Over the past 24 months, demand for biologic therapeutics and advanced vaccines among pet owners has climbed by approximately 45%, driven by rising pet adoption rates and wellness-focused veterinary care. Prescription biologic immunotherapies for chronic conditions (e.g., dermatological, orthopedic) now account for nearly 30% of new pet‑care product introductions. This has prompted veterinary clinics and animal hospitals to expand biologics capacity by ~25% to meet the growing demand for preventive and long-term care services.

• Transition from traditional vaccines to recombinant and subunit biologics in livestock: In the livestock segment, nearly 60% of new biologics in development pipelines are recombinant or subunit-based rather than inactivated whole‑pathogen vaccines. These newer biologics offer more precise immune responses and longer duration of protection, reducing the frequency of booster doses by up to 40%. As a result, producers covering large herds are shifting toward these newer formats to improve herd immunity and reduce overall vaccination cycles by roughly one-third over a typical production cycle.

• Expansion of digital supply‑chain traceability and cold‑chain logistics integration: The industry is increasingly leveraging blockchain-enabled traceability systems and IoT‑enabled temperature monitoring. Early adopters — primarily in North America and Europe — cite a 22% reduction in distribution losses and an 18% faster delivery time for biologic shipments. Adoption of such technology is expected to support compliance with stricter regulatory and animal‑welfare standards, improve transparency across distribution channels, and build resilience against cold‑chain disruptions or spoilage risks in large‑scale immunization programs.

The Veterinary Biologics market is segmented across multiple dimensions — by product type, by application (animal type and disease category), and by end-user/distribution channel. This segmentation reveals how demand is distributed between vaccines, therapeutics, diagnostics, and other biologic offerings; how different animal categories (livestock, companion animals, aquatic, equine) and disease prevention versus therapeutic applications shape demand; and which channels (clinics, hospitals, farms, retail) and end-users drive uptake. Such a structure allows industry stakeholders and analysts to identify high-value niches, allocate resources strategically, and design tailored go-to-market plans based on type, application, and user dynamics.

The leading type in the market is vaccines, accounting for approximately 78.6% of total biologics consumption in 2024. Vaccines maintain market dominance due to their essential role in preventive animal health, widespread adoption in both livestock and companion-animal sectors, and regulatory mandates requiring immunization for trade and public-health reasons. Within vaccines, formats include live-attenuated, inactivated/killed, subunit, recombinant, toxoid, DNA, and vector-based platforms, giving producers flexibility to target a broad spectrum of pathogens across species.

The fastest-growing type segment is inactivated/killed vaccines and subunit/recombinant vaccines, reflecting a shift toward safer, more stable, and regulatory-friendly biologics; uptake of these newer vaccine types is increasing as manufacturers move away from live-attenuated forms due to biosafety or cold-chain constraints. Other types — including antiserums and antibodies (monoclonal or polyclonal), immunomodulators, and diagnostic kits — collectively represent the remaining roughly 21.4% of the market. These niches serve post-exposure treatment, chronic therapy (especially in companion animals), immune support, or disease-surveillance needs, making them relevant for specialty applications rather than mass immunization.

By application — meaning animal type and purpose (livestock versus companion, preventive vaccination versus therapeutic/diagnostics) — the livestock segment remains the largest application area; in 2024 livestock animals accounted for nearly 58.9% of biologics usage. This reflects heavy immunization activity in cattle, poultry, swine, and other farm animals to prevent endemic and trade-sensitive diseases.

The fastest-growing application is in the companion-animal segment, driven by rising pet ownership, increased demand for preventive wellness, and growing adoption of advanced biologic therapies for chronic conditions. Companion-animal biologics usage is expanding rapidly as more pet owners treat pets as family members and invest in long-term health solutions. Other applications include aquatic animals, equine species, and niche livestock or exotic/wild animals, as well as therapeutic uses (serums, monoclonal antibodies) and diagnostics — together these make up the remaining ~40–45% of overall application volume.

The leading end-user segment in the Veterinary Biologics market is veterinary hospitals and clinics, which together account for roughly 45–50% of biologic product distribution and administration. These facilities are primary nodes for companion-animal care, routine livestock vaccination campaigns, and therapeutic biologics administration.

The fastest-growing end-user category is direct-to-farm/institutional users — large-scale livestock farms, integrated poultry operations, and commercial animal producers — as they increasingly invest in bulk vaccination programs and herd-health biologics to meet food-safety regulations, export requirements, and productivity targets. Smaller segments include retail pharmacies and online/e-commerce distribution for companion-animal biologics, research institutes, and specialized veterinary pharmacies; together these contribute the remaining ~20–25% of the market.

North America accounted for the largest market share at 38.30% in 2024 however, Asia‑Pacific is expected to register the fastest growth, expanding at a comparatively higher growth rate between 2025 and 2032.

This reflects a mature biologics demand base in North America alongside rapidly expanding livestock production, rising pet ownership and increasing regulatory support in Asia‑Pacific, which together are amplifying biologics adoption in those markets.

Is the mature market infrastructure driving stable biologics demand?

North America held about 38.30% of the global veterinary biologics market in 2024. Demand is driven by both high companion‑animal care and intensive livestock operations — pet vaccination and health services remain robust, while large‑scale cattle, swine and poultry farms continue routine immunization. Regulatory frameworks and proactive animal‑health policies support biologics adoption; government-backed animal health programmes and stringent disease‑control mandates encourage widespread vaccine and biologic usage. Technological advances and digital transformation — such as automated cold‑chain logistics, digital record‑keeping for herd health, and widespread use of recombinant and DNA-based vaccine platforms — are enhancing distribution efficiency and product efficacy. Local players and multinational firms in the region continuously invest in R&D and launch new biologic formulations, reinforcing the mature market’s capacity. Regional consumer behavior favors regular preventive care for pets and livestock — higher disposable income and awareness lead to high rates of pet‑vaccination compliance and livestock immunization in commercial farms.

Is regulatory rigor and animal‑welfare focus shaping biologics demand?

Europe accounted for a significant portion of the global veterinary biologics market alongside North America, with a substantial share in 2024. Key markets such as Germany, the United Kingdom, France, Italy and Spain drive demand across both companion‑animal and livestock segments. Regulatory bodies enforce strict animal‑welfare and biosecurity standards, fostering demand for high‑quality, safe biologic vaccines and therapies. These sustainability and regulatory pressures encourage adoption of recombinant, subunit and vector-based vaccines over older live‑attenuated types. European producers respond with advanced biologic portfolios, and market behavior reflects rising demand for explainable, traceable, and ethically produced biologic products. Consumers across Europe display cautious but consistent uptake of biologics, particularly in pet care and livestock disease prevention, bolstered by regulatory mandates and growing preference for premium vaccine quality.

Is rapid livestock growth and pet adoption driving biologics expansion?

Asia-Pacific ranks as the fastest-growing regional market in biologics, with rapid expansion in both livestock and companion‑animal segments. Major consuming countries include China, India, Japan and several Southeast Asian nations, where rising livestock populations and intensifying poultry, swine, and cattle farming increase demand for vaccines and biologic disease‑control solutions. Concurrently, burgeoning urbanisation and higher disposable income fuel rapid growth in pet ownership, increasing demand for companion-animal vaccines and therapies. Manufacturing capacity is expanding: regional producers and contract‑manufacturers are scaling up biologics production to meet growing local demand, and investment in cold‑chain infrastructure and vaccine distribution networks is rising. Technological adoption is strong, with deployment of thermostable vaccines, recombinant platforms, and bulk‑volume livestock‑vaccine production. Regional consumer behavior reflects pragmatic uptake — farmers prioritize herd‑health and food‑safety compliance, while pet owners increasingly invest in preventive biologic care for pets, often via both clinics and emerging e‑commerce veterinary channels.

Is growing agricultural demand and regulatory shifts supporting biologics uptake?

In South America, major markets such as Brazil and Argentina represent key demand centers driven by large‑scale livestock farming and export‑oriented meat production. The regional biologics market share is smaller compared to global leaders, but increasing investment in livestock immunization programs, rising awareness of zoonotic disease risks, and improving farm‑health regulations have begun to stimulate growth. Infrastructure upgrades — including cold‑chain distribution and veterinary‑service expansion — support broader biologics deployment. Local players and distributors are gradually increasing coverage across rural and peri‑urban farming zones. Regional consumer behavior is driven by livestock producers seeking reliable disease-control solutions to protect yields and meet export hygiene standards, while pet biologic adoption remains nascent but growing in urban centers. Government incentives and trade policies favor vaccination compliance for export certification, boosting biologics demand in commercial farms.

Is emerging demand and infrastructure development creating biologics growth potential?

Middle East & Africa currently represents a smaller share of the global veterinary biologics market, but shows promising growth potential. Growth is fueled by rising livestock and small‑ruminant farming, expanding commercial poultry and dairy sectors, and increasing awareness about animal‑health standards. Major growth countries include South Africa, UAE and select North African nations, where government‑backed vaccination drives and animal‑welfare regulations are beginning to take root. Infrastructure development — cold‑chain logistics, improved veterinary‑service networks, and local biologic manufacturing capacity — is underway in several markets. Local players and distributors are establishing distribution networks to improve access to biologics in remote or rural areas. Regional consumption is currently skewed toward livestock immunization rather than companion‑animal care, reflecting farming-driven demand, though pet‑care segments are slowly emerging in urban centers.

United States — ~ 25–30% share of global biologics demand; dominance driven by high production capacity, mature veterinary infrastructure, and extensive companion‑animal and livestock vaccination programmes.

China — significant regional demand in Asia‑Pacific; leadership backed by rapidly expanding livestock and poultry farming, rising pet adoption, and increasing investments in biologic manufacturing and distribution capacity.

The global Veterinary Biologics market exhibits a moderately concentrated competitive environment, with a mix of large-scale multinationals and numerous regional or local firms. There are dozens of active competitors worldwide, yet the top five companies account for roughly 55–65% of total market demand and production capacity. This concentration reflects a market where a handful of firms wield substantial influence, while many smaller players operate in specialized or regional niches. Major industry participants have reinforced their positions through aggressive strategic initiatives — including product launches, acquisitions, joint ventures, and expansion of biologic vaccine manufacturing facilities. Recent moves include expansion of high-capacity biologics manufacturing and R&D plants, and adoption of advanced recombinant and DNA-based vaccine platforms, signaling a shift toward innovation-driven competition.

Innovation trends — such as development of monoclonal antibody treatments for companion animals, thermostable vaccines for livestock in challenging climates, and expansion of cold-chain logistics — are increasingly shaping competitive dynamics. Firms investing in next-generation biologics and enhanced supply-chain capabilities tend to gain strategic advantage over legacy-only producers. Despite dominance of a few large firms, the presence of over 120 smaller producers and regional manufacturers globally ensures that the market remains partially fragmented, with niche competition especially in emerging markets, specialty vaccines, and regional biologics production.

Competitive positioning now hinges on breadth of product portfolio (livestock, companion animals, aquaculture), global distribution footprint, investment in biologics R&D, and agility in regulatory compliance and supply-chain management.

Zoetis Inc.

Merck & Co., Inc.

Boehringer Ingelheim GmbH

Elanco Animal Health Incorporated

Ceva Santé Animale

Virbac Group

Hester Biosciences Limited

Phibro Animal Health Corporation

The Veterinary Biologics market is experiencing a significant technological transformation, driven by innovations that enhance efficacy, safety, and delivery of animal vaccines and therapeutics. Recombinant and subunit vaccines now account for approximately 42% of newly developed biologics, offering more precise immune responses and longer-lasting protection compared to traditional inactivated or live-attenuated vaccines. These advanced formulations reduce booster frequency by up to 35% in large-scale livestock operations, optimizing herd management and lowering operational disruptions. DNA and vector-based vaccines are increasingly utilized in companion animals, covering chronic conditions such as dermatological and orthopedic disorders. These platforms support targeted immunogenicity and reduce adverse reactions, resulting in measurable improvements in animal health outcomes. Thermostable vaccines, which can maintain efficacy at ambient temperatures for up to 30 days, are now being deployed in remote and rural livestock regions, cutting vaccine spoilage rates by approximately 25% and streamlining distribution logistics.

Digital and IoT-enabled cold-chain monitoring systems are widely adopted in North America and Europe, ensuring real-time temperature tracking and reducing vaccine losses during transit. Blockchain-based traceability solutions are also emerging, enabling complete visibility of the supply chain and compliance with stricter regulatory requirements. Automation in vaccine production — including high-throughput bioreactors, robotic filling lines, and AI-guided quality control — is enhancing precision and scalability. These technologies allow producers to increase output by nearly 20% while maintaining batch consistency, supporting rapid response to disease outbreaks. The integration of data analytics, predictive modeling, and AI-driven formulation design further accelerates innovation, allowing faster development of next-generation biologics tailored to regional disease profiles.

Collectively, these technological advancements are reshaping the Veterinary Biologics landscape, offering measurable improvements in vaccine efficiency, operational reliability, and disease management across both livestock and companion-animal segments.

In mid‑2023, Zoetis launched Protivity — the first modified‑live vaccine for Mycoplasma bovis in beef and dairy calves — delivering a 74% reduction in lung lesions and improved herd health outcomes by six weeks of age. (Veterinary Practice)

In 2024, Zoetis expanded its diagnostics and biologics portfolio by approving combination vaccines and parasiticides for livestock globally, including a new cattle endectocide and enhanced salmon vaccine, while also launching AI‑powered diagnostic tools such as its updated hematology and urine‑analysis platforms. (Zoetis)

In March 2024, Boehringer Ingelheim and Ceva Animal Health were selected by French authorities to supply 61 million additional doses of bird flu vaccine for ducks, following a nationwide campaign to stem outbreaks of highly pathogenic avian influenza — a key step in large‑scale poultry immunization programs. (Reuters)

In late 2024, Zoetis’s global operations expanded manufacturing and distribution footprint: the company acquired a major manufacturing site in Melbourne and scaled up its U.S. distribution hub, supporting long‑term supply of vaccines and biologics across multiple species including livestock, companion animals, and aquaculture. (investor.zoetis.com)

The Veterinary Biologics Market Report encompasses a comprehensive evaluation of biologic products for animals, including vaccines (live‑attenuated, modified-live, inactivated, recombinant, subunit), parasiticides, immunotherapies, diagnostics, and combination biologics for livestock, companion animals, aquaculture, and exotic species. It covers regional segmentation across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, analysing differences in adoption, infrastructure, regulatory environment, and species‑specific demand patterns. Within application layers, the report examines preventive vaccination for livestock (cattle, swine, poultry, aquaculture), companion‑animal immunizations and therapies, parasite control treatments, and diagnostic biologics. It also reviews technological segments — including traditional biologics, recombinant and vector‑based vaccines, AI‑enabled diagnostics, and cold‑chain logistics — assessing penetration, regulatory compliance, and innovation readiness. The report further addresses key end‑users: large commercial farms, smallholder livestock producers, veterinary hospitals and clinics, pet owners, aquaculture farms, and institutional buyers.

The scope extends to niche and emerging market segments such as aquaculture biologics, fish‑vaccine developments, and cross‑species combination biologics. It also includes an assessment of biologic distribution and supply‑chain infrastructure, manufacturing capacity expansion, and regional readiness for cold‑chain or thermostable vaccine adoption. Moreover, the report evaluates market dynamics shaped by regulatory policies, animal‑welfare norms, antibiotic‑reduction mandates, and increasing demand for preventive and sustainable animal‑health solutions. Overall, the report serves as a strategic resource for decision‑makers, providing a holistic view of product types, applications, geography, technology trends, and user segments — highlighting both mature markets and high‑growth opportunities across the global veterinary biologics industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 12353.24 Million |

|

Market Revenue in 2032 |

USD 21067 Million |

|

CAGR (2025 - 2032) |

6.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Zoetis Inc., Merck & Co., Inc., Boehringer Ingelheim GmbH, Elanco Animal Health Incorporated, Ceva Santé Animale, Virbac Group, Hester Biosciences Limited, Phibro Animal Health Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |