Reports

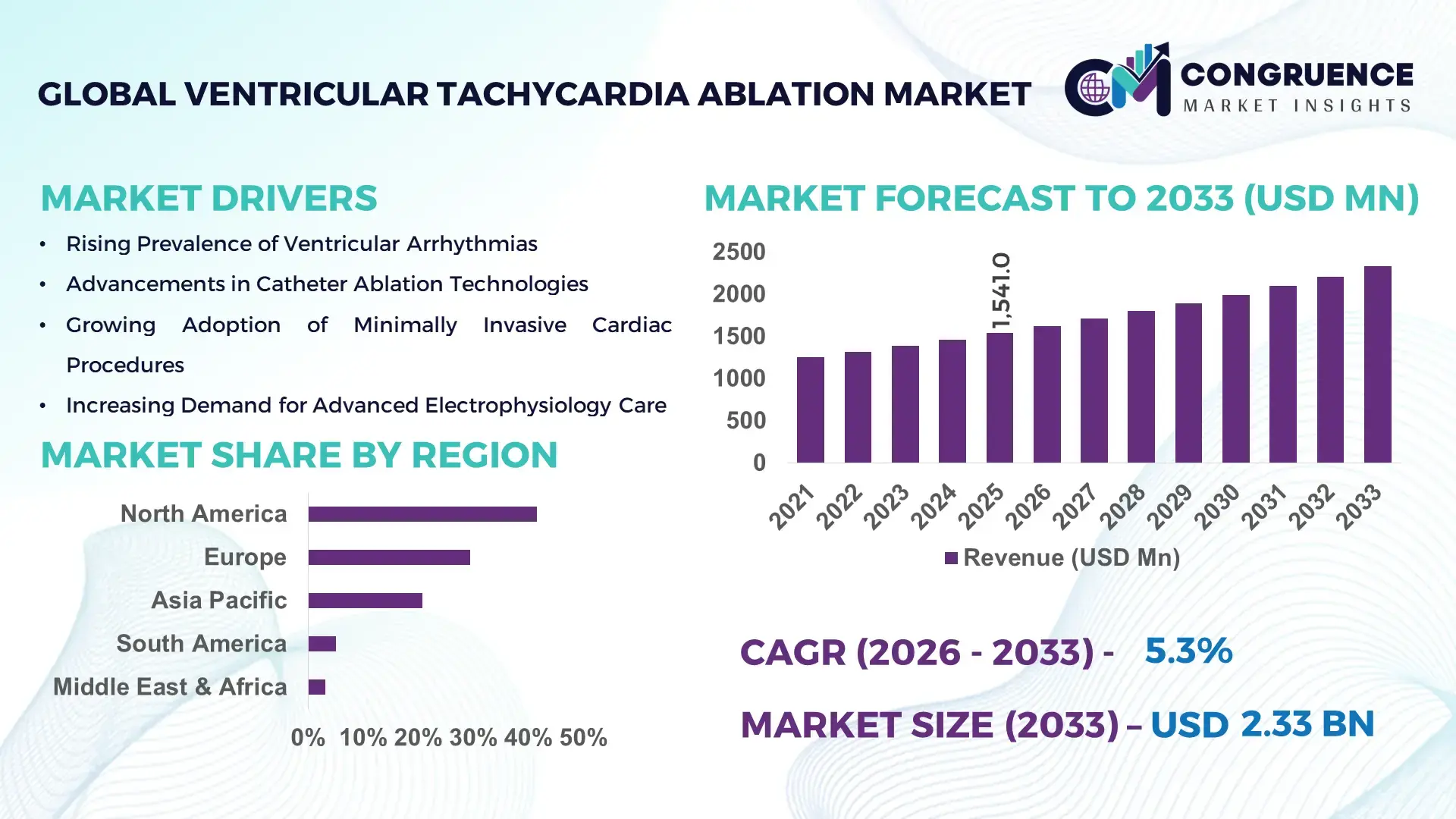

The Global Ventricular Tachycardia Ablation Market was valued at USD 1,541.0 Million in 2025 and is anticipated to reach a value of USD 2,327.6 Million by 2033 expanding at a CAGR of 5.29% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by the rising prevalence of ventricular arrhythmias, increasing procedural success rates, and wider adoption of minimally invasive electrophysiology interventions in tertiary care settings.

The United States represents the most influential country in the Ventricular Tachycardia Ablation Market, supported by advanced electrophysiology infrastructure and high procedural volumes. More than 2,300 hospitals in the U.S. are equipped with dedicated EP labs, and over 60% of complex VT ablation procedures are performed in large academic or multi-specialty cardiac centers. Annual VT ablation procedures exceed 55,000 cases, supported by continuous investments in 3D electroanatomical mapping systems, robotic catheter navigation, and contact-force sensing technologies. The country accounts for the highest adoption of next-generation ablation catheters, with penetration rates above 70% in tertiary hospitals. Additionally, strong clinical trial activity and annual investments exceeding USD 450 million in cardiac rhythm management R&D continue to accelerate technology upgrades and procedural standardization.

Market Size & Growth: Valued at USD 1,541.0 Million in 2025 and projected to reach USD 2,327.6 Million by 2033, growing at a CAGR of 5.29%, supported by expanding electrophysiology lab capacity and higher VT diagnosis rates.

Top Growth Drivers: Rising VT incidence (↑38%), adoption of 3D mapping systems (↑42%), and improvement in ablation success rates (↑31%).

Short-Term Forecast: By 2028, procedure-related complication rates are expected to decline by approximately 18% due to precision-guided ablation tools.

Emerging Technologies: High-density electroanatomical mapping, contact-force sensing ablation catheters, and AI-assisted arrhythmia localization platforms.

Regional Leaders: North America (USD 892 Million by 2033, early tech adoption), Europe (USD 654 Million, standardized EP protocols), Asia Pacific (USD 512 Million, rapid hospital expansion).

Consumer/End-User Trends: Tertiary hospitals and cardiac specialty centers account for over 65% of procedures, with outpatient EP labs growing steadily.

Pilot or Case Example: In 2024, a U.S.-based EP network reduced VT recurrence rates by 22% using AI-enabled mapping integration.

Competitive Landscape: Market leader holds ~34% share, followed by Biosense Webster, Abbott Laboratories, Boston Scientific, Medtronic, and Biotronik.

Regulatory & ESG Impact: Stricter device safety standards and low-radiation procedure mandates are accelerating adoption of advanced mapping systems.

Investment & Funding Patterns: Over USD 1.1 Billion invested globally in EP lab upgrades and VT ablation technologies during the last three years.

Innovation & Future Outlook: Integration of AI-driven mapping and robotic navigation is expected to redefine procedural efficiency and clinical outcomes.

Ventricular Tachycardia Ablation Market demand is primarily driven by tertiary hospitals contributing nearly 58% of procedures, followed by specialty cardiac centers at 29%. Recent innovations include ultra-high-density mapping catheters and low-fluoroscopy workflows. Regulatory focus on patient safety, expanding reimbursement coverage, and rising VT prevalence in aging populations are reshaping regional consumption patterns, particularly in North America and Asia Pacific, while AI-enabled ablation planning is emerging as a key future trend.

The Ventricular Tachycardia Ablation Market holds strategic importance within the global cardiovascular care ecosystem due to its direct impact on reducing sudden cardiac death risk and long-term hospitalization costs. As ventricular tachycardia prevalence rises with aging populations and increasing ischemic heart disease cases, healthcare systems are prioritizing definitive interventional therapies over long-term pharmacological management. Advanced catheter ablation procedures now demonstrate significantly improved outcomes, with AI-guided electroanatomical mapping delivering nearly 27% higher lesion accuracy compared to conventional fluoroscopy-based techniques.

From a regional perspective, North America dominates in procedure volume, while Europe leads in structured adoption, with approximately 62% of electrophysiology centers utilizing standardized VT ablation protocols. Asia Pacific is emerging rapidly, supported by increasing EP lab installations and clinician training initiatives. By 2028, AI-assisted mapping and robotic navigation are expected to reduce average procedure time by nearly 20%, improving lab throughput and cost efficiency.

Compliance and ESG considerations are also influencing market pathways. Hospitals are committing to radiation exposure reduction targets of up to 40% by 2030 through zero- or near-zero fluoroscopy ablation workflows. In 2024, Japan achieved a 19% reduction in VT recurrence rates through nationwide deployment of high-density mapping platforms combined with physician training programs.

Looking ahead, the Ventricular Tachycardia Ablation Market is positioned as a pillar of resilience and sustainable growth, aligning advanced clinical outcomes with regulatory compliance, digital integration, and long-term healthcare cost optimization.

The Ventricular Tachycardia Ablation Market dynamics are shaped by technological advancement, evolving clinical guidelines, and increasing procedural volumes across developed and emerging healthcare systems. The shift from pharmacological rhythm control toward interventional electrophysiology solutions has accelerated demand for precision ablation technologies. Hospitals are investing heavily in high-density mapping systems, contact-force sensing catheters, and integrated imaging platforms to improve procedural safety and outcomes. Training programs and certification standards for electrophysiologists are expanding globally, further supporting market penetration. However, cost sensitivity in emerging regions and complex regulatory approval pathways continue to influence adoption rates. Overall, the market reflects a balance between innovation-driven growth and structural constraints related to infrastructure, reimbursement, and skilled workforce availability.

The increasing global burden of ventricular arrhythmias is a primary driver for the Ventricular Tachycardia Ablation Market. Ventricular tachycardia is increasingly diagnosed in patients with ischemic cardiomyopathy and heart failure, with incidence rates rising by over 30% among individuals aged above 65 years. Clinical evidence shows catheter ablation reduces VT recurrence by nearly 45% compared to antiarrhythmic drug therapy alone. As a result, hospitals are prioritizing ablation as a first-line or early-intervention strategy. The growing pool of high-risk cardiac patients, combined with improved procedural success rates exceeding 80% in experienced centers, continues to expand demand for advanced VT ablation solutions worldwide.

High capital and operational costs remain a significant restraint for the Ventricular Tachycardia Ablation Market. Establishing a fully equipped electrophysiology lab requires investments exceeding USD 3–5 million, including mapping systems, imaging platforms, and ablation equipment. Additionally, disposable catheter costs can account for over 35% of per-procedure expenses. In many developing regions, limited reimbursement coverage and budget constraints restrict access to advanced ablation technologies. Shortages of trained electrophysiologists further compound adoption challenges, slowing market penetration outside major urban and tertiary healthcare centers.

Technological integration presents substantial opportunities for the Ventricular Tachycardia Ablation Market. The convergence of AI-driven mapping, robotic catheter navigation, and real-time imaging is enabling more precise lesion delivery and reduced recurrence rates. Emerging markets are investing in regional cardiac centers, increasing access to advanced EP procedures. Additionally, outpatient and same-day discharge VT ablation models are gaining traction, improving patient throughput and reducing hospital stay durations by up to 25%. These developments open new avenues for device manufacturers, software providers, and service partners across global healthcare systems.

Regulatory complexity and workforce limitations pose ongoing challenges for the Ventricular Tachycardia Ablation Market. Approval timelines for new ablation technologies can extend beyond 24 months, delaying commercialization. Simultaneously, the global shortage of trained electrophysiologists limits procedural scalability, particularly in emerging economies. Advanced VT ablation requires extensive operator expertise, with learning curves spanning several years. These factors create uneven adoption patterns and restrict rapid deployment of next-generation technologies despite strong clinical demand.

Expansion of AI-Driven Electroanatomical Mapping: AI-enabled mapping platforms are increasingly used to identify complex VT circuits with higher precision. Adoption rates have surpassed 48% in advanced EP labs, reducing mapping time by nearly 30% and improving procedural accuracy by over 20%.

Shift Toward Low- and Zero-Fluoroscopy Procedures: Hospitals are adopting low-radiation workflows, achieving fluoroscopy time reductions of up to 60%. Nearly 52% of newly commissioned EP labs now prioritize minimal radiation VT ablation protocols to improve clinician and patient safety.

Growing Use of High-Density Mapping Catheters: High-density mapping catheters are now utilized in more than 45% of VT ablation procedures, enabling detailed substrate characterization and reducing VT recurrence rates by approximately 18% within 12 months post-procedure.

Rising Adoption in Emerging Healthcare Markets: Asia Pacific and Latin America are witnessing rapid adoption, with VT ablation procedure volumes increasing by over 35% in urban cardiac centers. Government-backed cardiac care expansion programs are accelerating access to advanced electrophysiology interventions.

The Ventricular Tachycardia Ablation Market is segmented by type, application, and end-user, reflecting differences in procedural complexity, clinical settings, and patient profiles. By type, segmentation highlights varying ablation technologies designed to address distinct VT substrates, ranging from ischemic scar-related arrhythmias to structurally normal hearts. Application-based segmentation differentiates use cases such as ischemic VT, non-ischemic cardiomyopathy-related VT, and idiopathic VT, each with different procedural volumes and success benchmarks. End-user segmentation underscores the concentration of procedures in advanced care settings, where infrastructure, skilled electrophysiologists, and access to high-end mapping systems are critical. Across segments, adoption is strongly correlated with availability of electrophysiology labs, procedural safety requirements, and the shift toward precision-guided, minimally invasive cardiac interventions. This segmentation framework helps stakeholders identify high-utilization segments, technology adoption patterns, and operational priorities across healthcare systems.

The market by type is primarily segmented into radiofrequency (RF) ablation systems, cryoablation systems, and emerging adjunctive ablation technologies. Radiofrequency ablation systems dominate the segment, accounting for approximately 63% of total adoption, due to their proven efficacy in creating durable lesions and their compatibility with advanced 3D electroanatomical mapping platforms. RF systems are widely preferred for scar-related VT, where precise lesion depth and continuity are essential, and procedural success rates exceed 80% in experienced centers.

Cryoablation systems hold nearly 22% adoption, mainly used in specific anatomical regions where tissue preservation and catheter stability are critical. However, hybrid and pulsed-field–assisted ablation technologies represent the fastest-growing type, expanding at an estimated CAGR of 11.8%, driven by their potential to reduce collateral tissue damage and shorten procedure times. These systems are gaining traction in complex VT cases and repeat ablation procedures.

Other niche technologies, including adjunctive imaging-integrated ablation tools and experimental energy sources, collectively account for the remaining 15% share, serving specialized clinical scenarios and research-driven applications.

In 2025, a national cardiac research initiative reported the clinical use of pulsed-field–assisted VT ablation in over 1,200 procedures, demonstrating a 21% reduction in post-procedural ventricular tissue injury compared to conventional RF-only approaches.

By application, ischemic ventricular tachycardia represents the leading segment, accounting for nearly 48% of total procedures, as VT commonly arises from post-myocardial infarction scar tissue. These cases require complex substrate mapping and extensive lesion sets, driving higher utilization of advanced ablation systems. Non-ischemic cardiomyopathy-related VT follows with around 32% adoption, supported by improved imaging integration and growing recognition of VT risk in dilated and hypertrophic cardiomyopathies.

Idiopathic VT, although representing a smaller clinical burden, is the fastest-growing application segment, expanding at an estimated CAGR of 9.6%, driven by earlier diagnosis and increased referral of younger patients for definitive ablation rather than long-term drug therapy. Other applications, including congenital heart disease–related VT and post-surgical arrhythmias, collectively contribute approximately 20% of total procedures, serving highly specialized patient populations.

Consumer and clinical adoption trends indicate that in 2025, over 41% of tertiary hospitals globally reported increased referrals for VT ablation as first-line interventional therapy, while nearly 36% of electrophysiologists expanded ablation indications for non-ischemic VT due to improved procedural safety.

In 2024, a multinational cardiac registry documented VT ablation deployment across more than 180 specialized centers, reducing recurrent VT hospitalizations for ischemic patients by 24% within one year.

End-user segmentation shows that hospitals with dedicated electrophysiology laboratories are the leading end-users, accounting for approximately 67% of VT ablation procedures. These institutions benefit from integrated imaging, surgical backup, and multidisciplinary cardiac teams, enabling management of complex and high-risk VT cases. Specialty cardiac centers represent about 21% adoption, focusing on high-volume ablation programs and referral-based care models.

Ambulatory and outpatient electrophysiology centers constitute the fastest-growing end-user segment, expanding at an estimated CAGR of 8.9%, supported by shorter procedure times, improved anesthesia protocols, and same-day discharge pathways. Other end-users, including academic research institutions and government cardiac programs, collectively account for the remaining 12% share, contributing to training, innovation, and protocol development.

Adoption statistics indicate that in 2025, 44% of large hospital networks reported increased investment in VT ablation capacity, while nearly 29% of outpatient EP centers began offering VT ablation for selected low-risk patients, reflecting a shift toward decentralized care models.

In 2025, a government-supported cardiac care expansion program enabled over 90 regional hospitals to introduce VT ablation services, increasing national procedural access by 18% within two years.

North America accounted for the largest market share at 41.6% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2026 and 2033.

North America’s dominance is supported by high procedural volumes, with more than 55,000 ventricular tachycardia ablation procedures performed annually, advanced electrophysiology lab density exceeding 6.2 labs per million population, and early adoption of AI-assisted mapping systems in over 60% of tertiary hospitals. Europe follows closely with a 29.4% share, driven by standardized treatment protocols and cross-border cardiac care initiatives. Asia-Pacific currently represents around 20.8% of global procedures, but rapid hospital expansion, rising VT diagnosis rates above 9% annually in urban populations, and increasing government healthcare expenditure are accelerating uptake. South America and the Middle East & Africa together account for the remaining 8.2%, reflecting gradual infrastructure development and selective adoption in major cardiac centers.

The region holds approximately 41.6% of the global Ventricular Tachycardia Ablation Market, supported by a dense network of tertiary hospitals and specialized electrophysiology centers. Demand is primarily driven by the healthcare sector, particularly large hospital systems and academic medical centers managing complex arrhythmia cases. Regulatory frameworks emphasize patient safety and device performance, encouraging rapid integration of next-generation ablation catheters and 3D mapping platforms. Technological advancements include AI-enabled electroanatomical mapping and robotic catheter navigation, now utilized in nearly 58% of high-volume centers. A leading local player has expanded its EP device manufacturing capacity by 18% to support growing procedural demand. Regional consumer behavior reflects higher acceptance of minimally invasive cardiac interventions, with over 65% of eligible VT patients opting for ablation over long-term drug therapy.

Europe accounts for nearly 29.4% of the Ventricular Tachycardia Ablation Market, with Germany, the UK, and France collectively contributing over 62% of regional procedures. Strong regulatory oversight and emphasis on procedural transparency have driven adoption of high-density mapping and low-fluoroscopy ablation techniques. Sustainability and radiation-reduction initiatives have led to a 46% decline in fluoroscopy time per procedure across major centers. Emerging technologies such as MRI-integrated mapping systems are increasingly deployed, particularly in Western Europe. A regional device manufacturer has partnered with university hospitals to roll out standardized VT ablation training across 12 countries. Consumer behavior is shaped by regulatory pressure, with clinicians favoring explainable, data-driven ablation workflows to meet compliance and reporting requirements.

Asia-Pacific represents around 20.8% of global VT ablation volumes, ranking as the fastest-growing regional market. China, India, and Japan together account for more than 70% of regional procedures, supported by rapid hospital construction and cardiac center expansion. Over 1,100 new electrophysiology labs have been commissioned across the region in the last five years. Manufacturing localization of ablation catheters and mapping components is reducing device costs by nearly 22%, improving accessibility. Regional innovation hubs are advancing AI-assisted mapping and cloud-based procedural analytics. A prominent regional player has introduced locally manufactured RF ablation systems, increasing procedural availability across 140 secondary hospitals. Consumer behavior reflects strong growth in urban populations, with rising awareness and earlier referral for interventional VT management.

South America accounts for approximately 5.1% of the Ventricular Tachycardia Ablation Market, with Brazil and Argentina representing over 68% of regional demand. Infrastructure development is concentrated in metropolitan cardiac centers, where EP lab availability has increased by 27% over recent years. Government-backed healthcare modernization programs and import duty adjustments on medical devices are supporting technology inflow. While adoption remains selective, regional cardiac institutes are increasingly investing in advanced mapping systems. A local distributor has expanded service coverage to 35 additional hospitals, improving device uptime and training support. Consumer behavior shows growing preference for definitive interventional solutions among insured urban populations, while access in rural areas remains limited.

The Middle East & Africa region holds around 3.1% of global VT ablation activity, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Healthcare modernization programs are driving investment in advanced cardiac centers, particularly in Gulf countries, where EP lab capacity has grown by over 30% since 2020. Technological modernization includes adoption of zero-fluoroscopy workflows and tele-mentoring for complex ablation cases. Regulatory reforms and regional trade partnerships are easing access to advanced devices. A leading hospital group has established a dedicated arrhythmia center performing over 1,200 VT ablations annually. Consumer behavior reflects increasing trust in high-end specialty care, particularly among medical tourism patients.

United States – 34.2% Market Share: Dominates the Ventricular Tachycardia Ablation Market due to high EP lab density, advanced technology adoption, and large procedure volumes.

Germany – 9.8% Market Share: Leads in Europe supported by standardized cardiac care pathways, strong hospital infrastructure, and early adoption of precision ablation technologies.

The Ventricular Tachycardia Ablation Market features a moderately consolidated competitive environment, with a core group of specialized medical technology firms commanding substantial technological influence and procedural adoption. Across the global market, there are 30+ active competitors ranging from multinational medical device corporations to innovative regional electrophysiology (EP) technology developers. The top five companies collectively command an estimated 52–58% combined share of the total market, reflecting significant concentration among leading players while leaving room for niche innovators and regional challengers. Key market leaders include Medtronic, Biosense Webster (Johnson & Johnson division), Boston Scientific, Abbott Laboratories, and Biotronik, each with established portfolios of mapping systems, ablation catheters, and integrated electrophysiology solutions.

Strategic initiatives are shaping competition: firms are launching next-generation pulsed field ablation (PFA) technologies, AI-enabled mapping platforms, and robotic navigation systems to differentiate their offerings and improve clinical outcomes. Partnerships, such as joint ventures to advance AI-enhanced ablation workflows, are gaining momentum. Several players have received regulatory designations or approvals for novel VT-focused platforms, accelerating clinical adoption. Competitive dynamics also include product launches, mapping system enhancements, and targeted acquisitions aimed at expanding procedural coverage and ecosystem integration. Innovation trends influencing market positioning include non-thermal ablation energy sources, real-time lesion assessment tools, and cloud-connected analytics. As a business environment, the market is defined by technology leadership, strategic alliances, and sustained investment in procedural accuracy and safety technologies.

Abbott Laboratories

BIOTRONIK SE & Co. KG

Siemens Healthineers AG

Stereotaxis Inc.

MicroPort Scientific Corporation

Asahi Kasei Corporation

Elekta AB

EBR Systems, Inc.

LivaNova plc

Thermedical, Inc.

Schiller AG

Acutus Medical

APN Health

Technology innovation remains central to competitive advantage in the Ventricular Tachycardia Ablation Market, with current and emerging solutions reshaping procedural accuracy, safety, and accessibility. Pulsed field ablation (PFA) is one of the most promising energy modalities being developed for VT; early feasibility data show 82% freedom from recurrent ventricular arrhythmias and a 98% reduction in episodes at six months using novel high-voltage focal PFA systems, highlighting deep scar penetration with minimal thermal injury. These advancements are positioned to address the longstanding challenge of transmural lesion creation in scar-related VT.

Ultra-low temperature cryoablation techniques (ULTC) have shown substantial efficacy, with clinical studies reporting 94% elimination of VT in selected patient cohorts, reinforcing cryoenergy’s role in targeted substrate modification. Electrophysiology mapping technologies continue to evolve, featuring high-density 3D mapping with sub-millimeter resolution to enhance substrate characterization and procedural planning. Robotic and magnetic navigation systems provide micro-precision catheter control, improving access to complex ventricular substrates and reducing operator variability.

The integration of artificial intelligence (AI) into mapping systems is enabling real-time lesion assessment and predictive analytics, while cloud-connected procedural data platforms are facilitating remote collaboration and longitudinal outcome tracking. Advancements in imaging-integration (e.g., MRI or CT fusion with electroanatomical maps) help clinicians visualize complex cardiac anatomy and tailor ablation strategies. Combined, these technologies are expanding the clinical utility of VT ablation, reducing procedure times, and enhancing safety profiles. For decision-makers, prioritizing investments in solutions that optimize accuracy, procedural workflow, and data integration will be key to maintaining competitive positioning in this rapidly advancing market landscape.

• In April 2025, Field Medical Inc. closed a successful financing round of USD 40 million to advance its pulsed field ablation (PFA) technology specifically for ventricular tachycardia, enabling completion of pilot studies (VCAS and Field PULSE) and preparing for the VERITAS pivotal VT trial. Source: www.biospace.com

• In October 2025, initial human feasibility data for a high-voltage focal pulsed field ablation system demonstrated 82% freedom from recurrent VT/VF or ICD therapy and a 98% reduction in VT/VF burden at six months, highlighting effectiveness of PFA in treating scar-related VT and advancing the technology toward pivotal trials. Source: medicalxpress.com

• In July 2025, Boston Scientific received expanded FDA labeling for its FARAPULSE™ Pulsed Field Ablation System, broadening the indication to include treatment of drug-refractory, symptomatic persistent atrial fibrillation—a pivotal regulatory step for pulsed field ablation technologies that support broader electrophysiology adoption. Source: news.bostonscientific.com

• In October 2025, Johnson & Johnson MedTech (Biosense Webster) launched the CORE-VA real-world evidence registry to capture ventricular arrhythmia ablation practices, aiming to enhance clinical understanding of VT ablation outcomes and inform care standards across multiple centers. Source: www.jnjmedtech.com

The scope of the Ventricular Tachycardia Ablation Market Report encompasses a comprehensive analysis of technology portfolio segmentation, application focus domains, end-user deployment patterns, and geographic penetration dynamics. The report evaluates key product types including radiofrequency ablation systems, pulsed field ablation, cryoablation modalities, and adjunctive navigation technologies, assessing their performance in clinical environments and procedural workflows. Segmentation by application spans ischemic VT, non-ischemic cardiomyopathy-related VT, and idiopathic VT, providing detailed insights into clinical demand drivers, procedural complexity profiles, and usage patterns across hospital and specialty centers.

Geographically, the report examines regional markets such as North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering volume data, facility adoption rates, and infrastructure evolution insights tailored to decision-makers evaluating expansion, investment, or policy impact. End-user classification includes tertiary hospitals, specialty cardiac centers, ambulatory EP labs, and academic research institutions, highlighting differentiation in procedural volumes and technology uptake. The report also covers innovation ecosystems, tracking emerging technologies like AI-integrated mapping, robotic navigation, and real-time lesion assessment tools, and how these influence clinical outcomes, operational efficiency, and competitive positioning.

Focus areas extend to regulatory dynamics, training and education trends, reimbursement landscapes, and customer behavior variations that influence adoption curves across diverse healthcare systems. By integrating data on procedural efficiencies, technology performance benchmarks, and strategic market initiatives, the report supports stakeholders in market entry planning, product development prioritization, and resource allocation decisions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,541.0 Million |

| Market Revenue (2033) | USD 2,327.6 Million |

| CAGR (2026–2033) | 5.29% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Medtronic plc, Biosense Webster (Johnson & Johnson MedTech), Boston Scientific Corporation, Abbott Laboratories, BIOTRONIK SE & Co. KG, Siemens Healthineers AG, Stereotaxis Inc., MicroPort Scientific Corporation, Asahi Kasei Corporation, LivaNova plc, Acutus Medical, Inc., EBR Systems, Inc., APN Health |

| Customization & Pricing | Available on Request (10% Customization Free) |