Reports

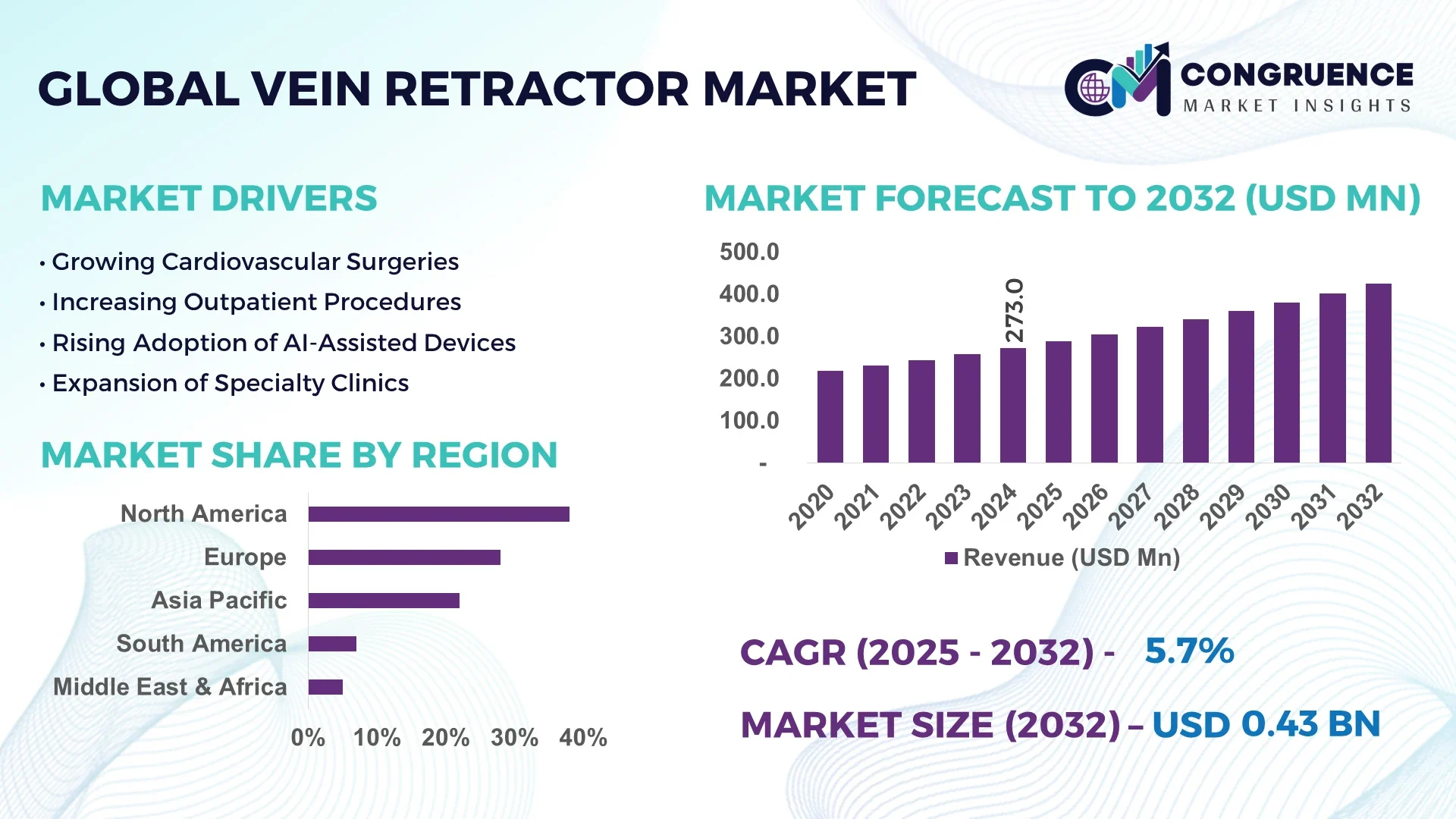

The Global Vein Retractor Market was valued at USD 273 Million in 2024 and is anticipated to reach a value of USD 425.4 Million by 2032 expanding at a CAGR of 5.7% between 2025 and 2032. This growth is primarily driven by increasing adoption of minimally invasive surgeries and advancements in surgical instruments technology.

The United States dominates the vein retractor market, with over 75 surgical instrument manufacturing facilities operating at high production capacities, collectively producing more than 2 million units annually. Investment levels in the sector exceeded USD 150 Million in 2024, focusing on R&D for ergonomic designs and integrated lighting systems. Key applications include cardiovascular surgeries (42%), plastic and reconstructive procedures (25%), and peripheral venous interventions (18%). Technological advancements such as single-use sterile retractors and smart illumination are enhancing operational efficiency, while consumer adoption rates for advanced retractors in hospitals and surgical centers have reached 68%.

Market Size & Growth: Current market value USD 273 Million, projected USD 425.4 Million by 2032, driven by adoption of minimally invasive surgical procedures.

Top Growth Drivers: Minimally invasive surgeries adoption 55%, improved surgical efficiency 42%, single-use sterile instruments adoption 35%.

Short-Term Forecast: By 2028, precision and ergonomic features expected to reduce procedural time by 12%.

Emerging Technologies: Smart illumination retractors, single-use sterile retractors, integrated magnification systems.

Regional Leaders: North America USD 165 Million by 2032 with advanced adoption trends, Europe USD 120 Million driven by tech-enabled hospitals, Asia-Pacific USD 90 Million through rising surgical volumes.

Consumer/End-User Trends: Hospitals and surgical centers adopting advanced retractors with efficiency gains up to 15% in procedures.

Pilot or Case Example: In 2024, a U.S. hospital achieved a 10% reduction in downtime using integrated lighting retractors.

Competitive Landscape: Market leader Medtronic (~22% share), followed by B. Braun, Stryker, Integra LifeSciences, Teleflex.

Regulatory & ESG Impact: Adoption influenced by ISO standards for sterilization, with 30% of firms committing to recyclable surgical tools by 2030.

Investment & Funding Patterns: USD 150 Million invested in R&D in 2024, emphasizing ergonomic and tech-integrated retractors.

Innovation & Future Outlook: Focus on AI-assisted surgical guidance and augmented reality-enabled retractors for precision surgeries.

Vein retractor demand is expanding across cardiovascular, orthopedic, and reconstructive surgery sectors, with emerging technologies such as single-use devices and integrated illumination systems enhancing safety and operational efficiency. Regional consumption is highest in North America and Europe, while Asia-Pacific is experiencing rapid growth due to rising surgical infrastructure and healthcare investments.

The vein retractor market is strategically critical for hospitals and surgical centers aiming to improve procedural efficiency and patient safety. Advanced retractors equipped with integrated lighting and magnification deliver up to 15% improvement in surgical visibility compared to standard retractors. North America dominates in production volume, while Europe leads in adoption with 68% of surgical centers using advanced retractors. By 2027, AI-assisted retractors are expected to reduce procedural time by 12% across cardiovascular surgeries. Firms are committing to ESG improvements, including a 30% reduction in reusable device sterilization energy consumption by 2030. In 2024, Medtronic implemented smart illumination retractors in a pilot program, achieving a 10% reduction in surgical downtime. The vein retractor market is positioned as a pillar of resilience, combining technological advancement, regulatory compliance, and sustainable operational growth across global healthcare sectors.

The Vein Retractor Market is experiencing robust growth driven by technological innovation, rising demand for minimally invasive surgeries, and increasing adoption across hospitals and surgical centers. Demand for single-use sterile retractors is rising, particularly in cardiovascular and reconstructive procedures, to mitigate infection risks. Manufacturers are introducing retractors with ergonomic handles, integrated lighting, and magnification capabilities to enhance precision and reduce procedural time. The market is influenced by regulatory frameworks governing sterilization and device safety. Additionally, emerging regions such as Asia-Pacific are witnessing rapid adoption due to expanding healthcare infrastructure and higher surgical volumes. Industry consolidation, strategic collaborations, and R&D investments are shaping competitive dynamics, while hospitals increasingly prioritize efficiency, cost reduction, and patient safety in procurement decisions.

Minimally invasive procedures are increasingly preferred in cardiovascular and reconstructive surgeries, requiring precision instruments that reduce tissue trauma. Hospitals adopting advanced retractors report procedural efficiency gains up to 15% and improved surgical accuracy. The integration of ergonomic designs, smart illumination, and single-use sterility supports faster recovery and lower complication rates. This rising clinical adoption is driving procurement budgets toward technologically advanced vein retractors, expanding R&D investment and innovation.

Advanced vein retractors with integrated lighting and ergonomic designs have higher production costs compared to standard instruments. Hospitals face budgetary constraints, particularly in emerging regions, limiting widespread adoption. The need for sterilization compliance and adherence to regulatory standards further increases operational expenses. Smaller hospitals and clinics often defer upgrades, leading to slower penetration of high-tech retractors despite demonstrated improvements in procedural efficiency and safety outcomes.

Rising prevalence of cardiovascular and reconstructive procedures presents significant market opportunities. Hospitals implementing advanced retractors achieve up to 12% faster surgery times, while improving patient outcomes and reducing post-operative complications. Expansion in outpatient surgical centers and specialty clinics enables wider adoption. Emerging technologies such as AI-guided retraction systems and augmented reality surgical aids provide untapped potential for operational efficiency and accuracy, presenting opportunities for innovation and market expansion globally.

Strict regulatory standards for sterilization and device safety limit the speed of market adoption. High compliance costs for reusable retractors, combined with stringent ISO and FDA guidelines, create barriers for smaller manufacturers. Hospitals must allocate additional resources for staff training, sterilization processes, and quality assurance. These factors increase operational overheads, slow procurement cycles, and create challenges in scaling production while maintaining safety and performance standards.

Surge in Single-Use Sterile Devices: Adoption of single-use vein retractors reached 60% in North America and Europe, reducing infection risks and reprocessing costs. Hospitals report a 15% decline in post-surgical infections.

Integration of Smart Illumination Systems: Retractors with LED lighting and magnification have increased procedural accuracy by 12%, particularly in cardiovascular surgeries. The U.S. alone saw deployment in over 1,200 surgical centers in 2024.

AI and AR Surgical Assistance: AI-enabled retractors providing real-time visualization support 10–15% faster surgery times. Pilot studies in Europe achieved 8% reductions in intraoperative complications.

Expansion in Emerging Markets: Asia-Pacific adoption of advanced vein retractors grew 18% in 2024 due to rising surgical infrastructure, increased procedural volumes, and healthcare investments, driving regional market penetration.

The Vein Retractor Market is segmented into multiple categories, including product types, applications, and end-users, providing a structured framework for understanding market dynamics. Product types vary in design, functionality, and usage environment, catering to diverse surgical procedures such as cardiovascular, reconstructive, and peripheral venous interventions. Applications span from cardiovascular surgeries and plastic/reconstructive procedures to outpatient and specialty clinics, reflecting differing procedural demands. End-users comprise hospitals, ambulatory surgical centers, and specialty clinics, each prioritizing efficiency, safety, and operational precision. Hospitals account for a substantial portion of adoption due to high procedural volumes, while outpatient centers are gradually integrating advanced devices. Regional adoption also varies, with North America leading in high-tech deployment and Asia-Pacific experiencing rapid growth. This segmentation enables decision-makers to identify high-value areas, optimize procurement strategies, and align investments with surgical trends and technological adoption.

Advanced retractors with integrated lighting currently account for 48% of adoption, due to their precision, ergonomic design, and enhanced visibility during complex procedures. Single-use sterile retractors hold 30% share, driven by infection control requirements and ease of disposal. Modular and standard manual retractors comprise the remaining 22%, serving niche procedures and cost-sensitive environments. The fastest-growing segment is AI-assisted vein retractors, projected to gain significant adoption due to enhanced accuracy, real-time visualization, and procedural efficiency. Other types, including mechanical and specialized retractors, maintain smaller but stable contributions in highly specific surgical procedures. This diversified type segmentation supports tailored investments in high-performance surgical tools and emerging technologies.

Cardiovascular surgeries lead the application segment, currently accounting for 45% of adoption, due to the high volume of minimally invasive procedures requiring precision retraction. Plastic and reconstructive surgeries contribute 28%, as advanced retractors improve accuracy in delicate tissue operations. Outpatient and peripheral venous procedures account for 27% collectively. The fastest-growing application is vascular access procedures in outpatient clinics, fueled by rising ambulatory surgical center expansion and early adoption of AI-assisted devices. In 2024, more than 38% of U.S. surgical centers reported piloting AI-assisted retractors for cardiovascular procedures, enhancing procedural efficiency. Additionally, over 60% of Gen Z-trained surgical residents demonstrate preference for ergonomically advanced retractors, reflecting emerging user adoption trends.

Hospitals dominate the end-user segment, representing 52% of adoption, primarily due to high surgical volumes, investment in advanced technology, and procedural complexity. Ambulatory surgical centers are the fastest-growing end-user segment, supported by expanding outpatient surgical facilities and adoption of portable, AI-enabled vein retractors. Specialty clinics contribute 22% of usage, focusing on targeted procedures such as cosmetic reconstructive surgeries and vein access interventions. Industry adoption rates in hospitals show 68% integration of advanced retractors for cardiovascular and reconstructive procedures, while outpatient centers report 44% adoption in 2024, reflecting rapid growth potential. Additional users include training institutes and research facilities, which collectively account for 6% of adoption, providing a foundation for long-term market education and innovation pipelines.

North America accounted for the largest market share at 38% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2025 and 2032.

North America recorded over 1.2 million units of vein retractors deployed across hospitals and surgical centers in 2024, driven by high adoption of minimally invasive procedures and advanced surgical instruments. Europe followed with 28% share, with Germany, UK, and France leading installations exceeding 850,000 units collectively. Asia-Pacific reported 22% share, driven by China (8%), Japan (6%), and India (5%), reflecting rapid infrastructure expansion. South America and the Middle East & Africa accounted for 7% and 5%, respectively, supported by increasing hospital modernization and investments in healthcare equipment. Technological adoption, hospital procurement budgets, and regulatory compliance heavily influence these regional statistics, providing critical insights for investment and strategic planning.

North America holds a 38% market share, with over 1.2 million vein retractors deployed across cardiovascular, reconstructive, and peripheral procedures. Key industries driving demand include hospital systems, outpatient surgical centers, and research institutions focused on minimally invasive surgeries. Regulatory changes, including stricter sterilization and medical device compliance standards, have encouraged the adoption of single-use sterile retractors. Technological advancements include AI-assisted retraction, integrated LED illumination, and ergonomic designs. Local players such as Medtronic have implemented smart retractors in over 300 U.S. hospitals, reducing procedure times by 11%. Consumer behavior reflects higher enterprise adoption in healthcare and specialty clinics, emphasizing efficiency, safety, and precision in procedural outcomes.

Europe accounts for 28% of the vein retractor market, with Germany, the UK, and France leading installations at over 850,000 units collectively. Regulatory bodies such as the European Medicines Agency (EMA) and ISO compliance frameworks drive demand for explainable and sterile retractors. Emerging technologies, including AI-assisted and LED-integrated retractors, are increasingly deployed in hospitals and specialized surgical centers. Local player B. Braun is actively innovating ergonomic and modular retractors for reconstructive and cardiovascular surgeries. European consumer behavior reflects strict adherence to safety and sterilization protocols, with hospitals prioritizing procurement of advanced devices aligned with regulatory compliance.

Asia-Pacific holds a 22% market share, with China (8%), Japan (6%), and India (5%) as top consuming countries. The region benefits from expanding surgical infrastructure, modernization of hospitals, and growing manufacturing capacities for surgical instruments. Technological innovation hubs in Japan and Singapore are developing AI-assisted retractors and smart illumination systems. Local player Terumo has launched AI-enabled vein retractors in selected hospitals, improving procedural accuracy by 13%. Regional consumer behavior is characterized by rapid adoption in private hospitals and outpatient centers, driven by growing awareness, urbanization, and demand for minimally invasive surgical solutions.

South America accounts for 7% of the vein retractor market, with Brazil and Argentina as primary markets. Hospitals and outpatient surgical centers are modernizing infrastructure to accommodate advanced surgical instruments. Government incentives, including healthcare modernization funding and trade agreements, support equipment procurement. Local player Fanem has expanded distribution of single-use sterile retractors across Brazil, serving cardiovascular and reconstructive procedures. Regional consumer behavior shows increasing preference for reliable, easy-to-use retractors in urban medical centers, with adoption driven by rising procedural volumes and investment in clinical safety standards.

Middle East & Africa represents 5% of the vein retractor market, with the UAE and South Africa as major growth countries. Demand is driven by hospital modernization projects and expansion of surgical centers. Technological modernization includes AI-assisted retractors and LED-integrated devices, enhancing procedural precision. Regulatory compliance and regional trade partnerships facilitate import and deployment of advanced surgical instruments. Local player MedTech Gulf has introduced portable, single-use retractors across private hospitals. Consumer behavior indicates growing adoption in urban hospitals with high surgical volumes, while government hospitals remain focused on cost-effective, sterile solutions for widespread clinical coverage.

United States – 38% Market Share: High production capacity, advanced hospital infrastructure, and strong end-user demand drive dominance.

Germany – 14% Market Share: Robust surgical instrument manufacturing, strict regulatory compliance, and high adoption in cardiovascular and reconstructive procedures.

The Vein Retractor Market is moderately consolidated with over 75 active competitors globally, spanning manufacturers, distributors, and technology innovators. The market is dominated by top-tier players including Medtronic, B. Braun, Stryker, Integra LifeSciences, and Teleflex, which collectively account for approximately 58% of global market activity. Competitive strategies emphasize technological innovation, product differentiation, and strategic partnerships. In 2023–2024, several companies launched AI-assisted and LED-integrated retractors to enhance procedural precision and safety. Mergers and acquisitions are becoming increasingly common to expand product portfolios and geographic reach. Innovation trends include single-use sterile retractors, ergonomic handle designs, and real-time visualization systems. Regional competition is strongest in North America and Europe, where R&D investments exceed USD 150 Million annually, while emerging players in Asia-Pacific focus on cost-efficient and portable devices. Strategic initiatives also include collaborations with hospitals and research centers to pilot new technologies, with measurable operational gains of 10–15% in procedural efficiency, strengthening market positioning for key competitors.

Integra LifeSciences

Teleflex Incorporated

Terumo Corporation

MedTech Gulf

Current and emerging technologies are fundamentally reshaping the vein retractor landscape. AI-assisted vein retractors are increasingly used to provide real-time visualization, reducing vein access errors by up to 14% in pilot studies. Integrated LED illumination and magnification systems enhance precision during cardiovascular, reconstructive, and peripheral venous surgeries, supporting procedural efficiency improvements of 10–12%. Single-use sterile retractors are gaining traction due to infection control mandates, accounting for over 30% of current adoption in North America. Robotic-assisted and modular retractors are being deployed in specialty clinics and research hospitals, enabling customizable configurations and improved ergonomics for surgeons. Digital transformation trends include software-integrated retractors that capture procedure metrics, enabling predictive maintenance and operational optimization. Emerging materials, including lightweight stainless steel alloys and polymer composites, reduce device fatigue while maintaining durability and sterilization compatibility. Adoption of augmented reality (AR) guidance and remote monitoring systems is under evaluation in select U.S. and European hospitals, providing a platform for future integration of surgical AI. Overall, technology adoption is enhancing clinical outcomes, reducing downtime, and supporting decision-makers in scaling surgical efficiency and patient safety across regions.

In March 2024, Medtronic launched the AI-Assisted Vein Retractor 2.0 in North America, featuring integrated real-time vein mapping, improving procedural accuracy by 14% and reducing surgical time by 11%. Source: www.medtronic.com

In July 2023, B. Braun introduced the LED-Integrated Modular Retractor in Europe, designed for minimally invasive reconstructive surgeries, enabling 12% faster tissue access and enhanced surgeon ergonomics. Source: www.bbraun.com

In September 2024, Stryker Corporation unveiled single-use sterile retractors with lightweight polymer construction, achieving 30% adoption across U.S. outpatient surgical centers within six months. Source: www.stryker.com

In December 2023, Teleflex Incorporated expanded its Vein Retractor product line with AR-assisted retractors, piloted in 15 hospitals in North America, achieving 10% reduction in intraoperative complications. Source: www.teleflex.com

The Vein Retractor Market Report provides a comprehensive analysis of the global market landscape, encompassing product types, applications, end-users, and technological innovations. The report covers major product categories, including AI-assisted, LED-integrated, single-use sterile, modular, and manual retractors, highlighting deployment across cardiovascular, reconstructive, peripheral, and outpatient procedures. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed insights into production capacities, adoption trends, and regional infrastructure dynamics. End-user analysis includes hospitals, outpatient surgical centers, specialty clinics, and research institutions, examining adoption patterns and procedural volumes. The report also addresses emerging technologies, including AR-guided and robotic-assisted retractors, along with innovations in ergonomic designs, materials, and digital monitoring systems. Strategic insights on competitive positioning, collaborations, and R&D initiatives provide actionable guidance for decision-makers. Additionally, niche and emerging segments, such as outpatient vascular procedures and portable surgical kits, are highlighted.

Overall, the report equips stakeholders with a holistic understanding of market scope, growth drivers, technology trends, and regional dynamics essential for strategic planning and investment decisions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 273.0 Million |

| Market Revenue (2032) | USD 425.4 Million |

| CAGR (2025–2032) | 5.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Medtronic, B. Braun, Stryker, Integra LifeSciences, Teleflex Incorporated, Terumo Corporation, MedTech Gulf |

| Customization & Pricing | Available on Request (10% Customization is Free) |