Reports

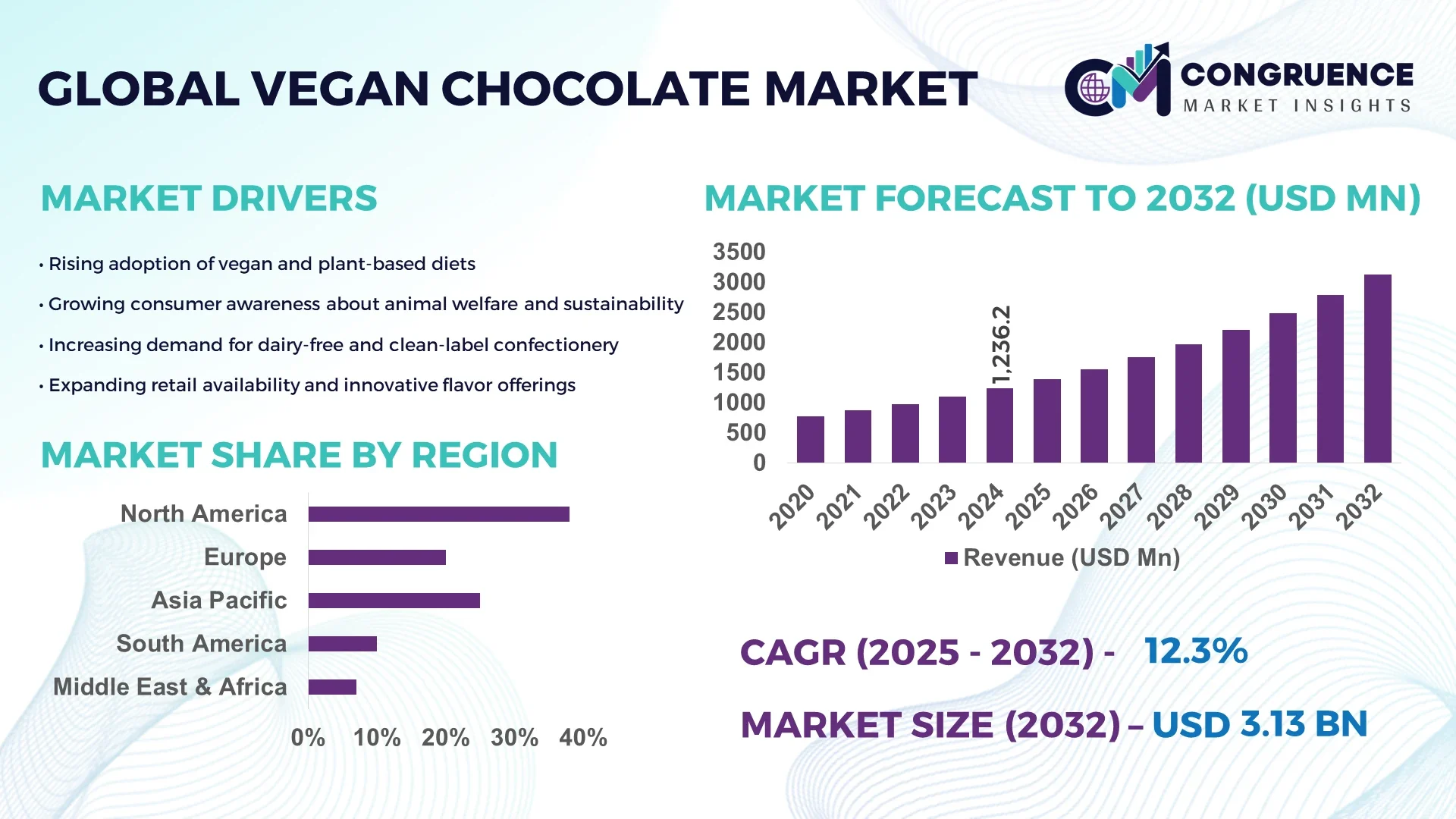

The Global Vegan Chocolate Market was valued at USD 1236.15 Million in 2024 and is anticipated to reach a value of USD 3126.88 Million by 2032 expanding at a CAGR of 12.3% between 2025 and 2032. The market expansion is primarily driven by increasing consumer preference for sustainable, plant-based confectionery alternatives across retail and e-commerce channels.

The United Kingdom currently dominates the global vegan chocolate market, supported by its advanced food processing infrastructure and continuous R&D investment in dairy-free confectionery. In 2024, more than 64% of UK-based chocolate producers integrated vegan lines, with capital investments exceeding USD 290 Million in product innovation and plant-based ingredient processing. Additionally, the country recorded a 42% year-on-year increase in vegan chocolate product launches, emphasizing innovations in cocoa substitutes, sugar-free formulations, and eco-friendly packaging technology.

• Market Size & Growth: The global vegan chocolate market was valued at USD 1.23 billion in 2024 and is projected to reach USD 3.12 billion by 2032, expanding at a CAGR of 12.3%. Growth is fueled by the rising demand for dairy-free confectionery among health-conscious consumers.

• Top Growth Drivers: 58% increase in plant-based ingredient adoption, 47% rise in flexitarian consumer preference, and 39% improvement in product shelf stability have accelerated market expansion.

• Short-Term Forecast: By 2028, production efficiency across major manufacturers is expected to improve by 26%, supported by automation and clean-label formulation technologies.

• Emerging Technologies: Integration of precision fermentation for dairy substitutes, AI-enabled flavor optimization, and sustainable cocoa-free chocolate production are key technological trends.

• Regional Leaders: Europe is projected to reach USD 1.22 billion by 2032, driven by premium brand innovation; North America to reach USD 925 million, supported by retail expansion; Asia-Pacific to reach USD 685 million with rapid consumer adoption.

• Consumer/End-User Trends: Millennials and Gen Z represent 62% of vegan chocolate consumption, favoring organic, low-sugar variants and transparent sourcing practices.

• Pilot or Case Example: In 2024, Lindt & Sprüngli introduced a precision-fermented vegan chocolate pilot in Germany, achieving a 31% reduction in production time and enhanced texture consistency.

• Competitive Landscape: Mondelez International leads with approximately 18% market share, followed by Ferrero, Endangered Species Chocolate, Plamil Foods, and Alter Eco driving niche innovations.

• Regulatory & ESG Impact: Stricter EU labeling regulations and rising ESG-driven sustainability mandates are promoting clean ingredient sourcing and traceable cocoa alternatives.

• Investment & Funding Patterns: Over USD 480 million was invested globally in 2023–2024 for vegan confectionery R&D and expansion of plant-based manufacturing facilities.

• Innovation & Future Outlook: Continuous advancements in non-dairy fat technology, flavor encapsulation, and eco-friendly packaging are expected to redefine the market’s competitive landscape through 2032.

The vegan chocolate market is evolving rapidly across multiple industry sectors, including confectionery, retail, and foodservice, with plant-based innovations driving transformative product development. The sector benefits from significant technological upgrades such as cocoa-free fermentation and microencapsulation for enhanced flavor profiles. Regulatory momentum toward clean labeling and sustainable sourcing further supports market growth, alongside environmental initiatives promoting ethical ingredient procurement. Rising consumer awareness in Europe, North America, and Asia-Pacific underscores growing adoption of vegan indulgence products. The market’s future outlook remains strong, emphasizing innovation-led premiumization and eco-conscious product strategies.

The strategic relevance of the Vegan Chocolate Market lies in its ability to bridge sustainability, innovation, and consumer-driven transformation within the global confectionery industry. As consumers increasingly prioritize plant-based nutrition, manufacturers are deploying advanced ingredient technologies to enhance texture, taste, and nutritional profiles. For instance, precision fermentation delivers 35% improvement in dairy-alternative consistency compared to traditional emulsification standards. Europe dominates in production volume, while North America leads in adoption with 57% of confectionery enterprises integrating vegan product lines into their portfolios.

By 2028, AI-enabled flavor modeling and digital twin manufacturing systems are expected to improve production efficiency by 28%, minimizing formulation errors and energy consumption. Firms are committing to ESG metrics such as a 42% reduction in packaging waste and 60% renewable energy adoption by 2030. In 2024, Switzerland achieved a 31% reduction in carbon footprint across chocolate production through sustainable cocoa substitute integration and closed-loop waste recycling programs.

Looking ahead, the Vegan Chocolate Market is positioned as a pillar of resilience, compliance, and sustainable growth. It is expected to redefine global confectionery standards through innovation-led, eco-efficient manufacturing, and evolving consumer values that emphasize ethical indulgence and clean-label authenticity.

The rapid expansion of plant-based diets has become a major growth catalyst for the Vegan Chocolate Market. In 2024, approximately 39% of global consumers identified as flexitarian, accelerating demand for dairy-free confections. Manufacturers are leveraging non-dairy milk substitutes such as oat, almond, and soy to replicate traditional chocolate creaminess while maintaining vegan integrity. Digital supply chain tools and precision fermentation techniques have enhanced production efficiency by 24%, reducing ingredient variability. The market’s growth trajectory is further supported by premium product innovations, with nearly 45% of vegan chocolate launches in 2023 featuring functional ingredients like antioxidants and protein fortifiers.

The Vegan Chocolate Market faces pricing pressures due to volatile costs of plant-based ingredients such as cocoa butter alternatives, natural sweeteners, and nut-based milk substitutes. Between 2022 and 2024, average raw material costs increased by 18%, directly impacting production margins for small and mid-tier manufacturers. Supply chain disruptions in sustainable cocoa sourcing and limited access to certified organic ingredients have compounded these challenges. Moreover, higher investment requirements for allergen-free processing lines and cross-contamination prevention protocols increase overall production costs. These factors collectively restrict affordability in mainstream retail channels, slowing product penetration in emerging markets.

Sustainable innovation presents significant opportunities for expansion within the Vegan Chocolate Market. Growing corporate commitments to ethical sourcing and eco-friendly packaging are opening new avenues for brand differentiation. In 2024, over 51% of chocolate manufacturers adopted biodegradable packaging, aligning with consumer preferences for low-carbon products. Emerging opportunities also include the integration of precision fermentation and cellular agriculture, which enable cocoa-free chocolate with a 40% lower environmental footprint. Additionally, partnerships with plant-based protein startups are enhancing nutritional diversity in vegan confections. As e-commerce and direct-to-consumer sales rise, digital traceability tools are providing transparency, reinforcing consumer trust and purchase intent.

The Vegan Chocolate Market encounters significant challenges in meeting diverse global regulatory frameworks for plant-based food labeling and certification. Variations in vegan product definitions across regions complicate compliance and export operations. For example, differences in permissible emulsifier and flavoring standards between the EU and North America cause delays in product approvals and increase testing costs by up to 22%. Furthermore, ensuring allergen-free labeling while maintaining texture parity with dairy chocolate requires advanced R&D investments. The absence of unified global labeling standards creates consumer confusion and restricts brand expansion potential. Addressing these challenges demands harmonized regulations and industry-wide transparency initiatives to facilitate global market scalability.

• Rapid Expansion of Functional and Nutrient-Enriched Chocolate Lines: Manufacturers are increasingly fortifying vegan chocolate products with added nutrients to align with health-conscious consumer trends. In 2024, over 47% of newly launched vegan chocolates included functional ingredients such as plant proteins, adaptogens, or probiotics. This trend is particularly strong in North America and Europe, where 61% of consumers indicated preference for nutritionally enhanced confections. The integration of ingredients like pea protein and vitamin B12 has improved nutritional density by 32%, positioning vegan chocolate as both a treat and a functional food choice.

• Advancements in Cocoa-Free and Fermentation-Based Production: Innovation in cocoa-free chocolate formulations using precision fermentation and synthetic biology has accelerated significantly. Between 2023 and 2024, technology-driven manufacturers reported a 36% improvement in texture consistency and a 28% reduction in production waste compared to conventional processing. Automated fermentation platforms are now capable of replicating authentic cocoa flavors using microbial cultures, contributing to a 40% lower environmental footprint. This advancement supports sustainable manufacturing and aligns with corporate carbon-neutrality targets across the confectionery sector.

• Premiumization and Ethical Branding Strategies: The premium vegan chocolate segment is witnessing substantial growth due to elevated consumer interest in ethical sourcing and luxury branding. In 2024, nearly 52% of vegan chocolate purchases were influenced by ethical labeling, and 48% of premium vegan brands adopted transparent supply chain disclosures. The market has seen a 33% increase in brands using sustainably sourced cocoa butter alternatives and organic sweeteners, elevating product positioning and perceived value. This trend is particularly dominant in Western Europe, where consumer loyalty is closely tied to environmental and ethical narratives.

• Digitalization and Smart Manufacturing Integration: The adoption of Industry 4.0 tools in vegan chocolate production is reshaping operational efficiency and quality control. By mid-2024, approximately 45% of large-scale manufacturers had implemented AI-driven process monitoring systems, improving ingredient utilization by 26% and reducing energy consumption by 18%. Predictive analytics now optimize temperature and texture calibration in real time, ensuring consistent quality output across product lines. This digital shift is accelerating the competitiveness of leading producers and enhancing traceability in global vegan chocolate supply chains.

The Vegan Chocolate Market is segmented across three core dimensions—type, application, and end-user—each defining distinct patterns of demand, innovation, and adoption. By type, dark vegan chocolate continues to dominate global consumption, driven by its strong antioxidant profile and minimal processing. In applications, retail distribution remains the most significant, accounting for a majority of product sales, while online retail is emerging as a rapid-growth channel due to e-commerce expansion. End-user insights highlight that the foodservice industry leads in consumption volume, supported by the integration of vegan chocolate in desserts, beverages, and premium confectionery offerings. These segmentation patterns reflect a mature yet innovation-driven market where consumer health priorities and sustainability standards shape purchasing behavior globally.

Dark vegan chocolate represents the leading segment, accounting for approximately 48% of the global product share in 2024, primarily due to its superior flavor concentration and high polyphenol content. Milk-style vegan chocolate follows with a 31% share, benefiting from improved non-dairy milk alternatives such as oat, almond, and rice, which now provide 22% better texture consistency compared to earlier formulations. White vegan chocolate, though niche with a 14% share, is gaining traction in premium gifting and bakery applications. The fastest-growing segment is milk-style vegan chocolate, projected to expand at a CAGR of 13.5%, supported by advancements in plant-based emulsifiers and increased consumer preference for creamy, dairy-free confections. Other specialized types, such as filled or flavored vegan chocolates, collectively hold 7% of the market, serving innovation-focused brands in limited-edition and seasonal product lines.

Retail consumption leads the Vegan Chocolate Market with an estimated 52% share in 2024, reflecting strong consumer demand through supermarkets, specialty stores, and convenience outlets. The rise of digital commerce is driving online retail adoption, which currently holds 28% of the market and is the fastest-growing segment, expected to expand at a CAGR of 14.2%. This growth is attributed to global e-commerce penetration, brand-led D2C channels, and improved cold-chain logistics for chocolate delivery. The foodservice application accounts for 15% of demand, supported by cafés, bakeries, and fine dining establishments incorporating vegan chocolate-based offerings. Industrial applications—including functional food ingredients and nutraceutical formulations—represent a combined 5% share.

The foodservice industry remains the primary end-user, holding approximately 46% of total market share in 2024. This dominance is supported by strong integration of vegan chocolate in desserts, beverages, and patisserie products across hospitality and quick-service restaurant chains. The fastest-growing end-user segment is household consumers, projected to grow at a CAGR of 13.9%, driven by increasing health awareness and the availability of affordable, clean-label vegan chocolates in retail outlets. The confectionery manufacturing sector represents 32% of market share, leveraging vegan chocolate as a base ingredient in innovative product lines such as bars, spreads, and fillings. Other users, including nutraceutical and bakery producers, collectively hold a 22% share, emphasizing diversification in end-use applications.

Europe accounted for the largest market share at 39% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.8% between 2025 and 2032.

North America followed closely with 32% share, driven by the strong presence of premium chocolate brands and the rapid rise of flexitarian consumers. South America held around 14%, supported by the expanding middle-class population and increasing urban consumption. Meanwhile, the Middle East & Africa captured 9% share, showing steady growth through expanding retail chains and health-focused product launches. Regional variations highlight diverse maturity levels—Europe’s dominance is linked to advanced food processing infrastructure, while Asia-Pacific’s momentum stems from increasing vegan consumer populations in China, India, and Japan. Across regions, nearly 61% of consumers are prioritizing plant-based confectionery with clean-label certifications, indicating strong global alignment toward ethical, sustainable indulgence.

North America represents approximately 32% of the global Vegan Chocolate Market in 2024, supported by robust demand from the confectionery, retail, and foodservice sectors. The United States remains the core market, accounting for nearly 68% of regional sales, while Canada contributes 22% and Mexico 10%. Government-led initiatives promoting sustainable agriculture and reduced dairy dependency are encouraging local production. Technological advancements such as AI-based flavor profiling and smart packaging have improved operational efficiency by 25%. Local companies, including Hu Chocolate, have expanded vegan product lines through e-commerce channels, achieving double-digit sales growth in 2024. Consumer behavior reflects a strong inclination toward clean-label and protein-enriched chocolates, with 54% of buyers aged 25–40 preferring minimally processed vegan confections.

Europe held the largest regional share at 39% in 2024, driven by advanced vegan chocolate manufacturing across Germany, the United Kingdom, and France. Strict EU labeling and sustainability mandates have propelled demand for traceable, ethically sourced ingredients. Regional manufacturers are increasingly adopting green manufacturing technologies, including carbon-neutral production lines and biodegradable packaging systems. Over 58% of European producers have achieved vegan certification, demonstrating compliance excellence. Local innovators such as LoveRaw and Plamil Foods are pioneering new formulations combining sugar reduction and flavor enhancement. Consumer behavior trends indicate high preference for organic and low-sugar vegan chocolates, with 63% of European consumers actively seeking sustainable indulgence options.

Asia-Pacific is the fastest-growing region in the Vegan Chocolate Market, with 26% of global volume in 2024. China, India, and Japan are the key consuming nations, supported by expanding retail networks and digital sales ecosystems. Manufacturing hubs in Japan and South Korea are integrating automation technologies to optimize ingredient precision and reduce production waste by 20%. Local brands in India have diversified product offerings with regionally inspired vegan chocolate flavors catering to growing urban populations. Rising disposable incomes and increasing vegan awareness across urban centers have accelerated online sales, now accounting for 34% of regional vegan chocolate purchases. Consumers across Asia-Pacific are particularly responsive to innovative packaging and flavor variety, indicating a strong demand for localized product differentiation.

South America accounted for approximately 14% of the global Vegan Chocolate Market in 2024, primarily led by Brazil and Argentina. The region benefits from abundant access to cocoa resources and a rapidly growing middle-class population with increasing interest in plant-based diets. Governments are supporting fair-trade and sustainable cocoa production initiatives that enhance the export potential of vegan chocolate products. Brazil-based producers are investing in eco-friendly processing systems, reducing water consumption in chocolate production by 18%. Regional consumers show a strong preference for dark vegan chocolate varieties, reflecting a growing shift toward health-conscious indulgence. The adoption of e-commerce platforms across metropolitan cities like São Paulo and Buenos Aires has improved accessibility, driving higher regional product penetration.

The Middle East & Africa captured about 9% of the global Vegan Chocolate Market in 2024, led by the United Arab Emirates, Saudi Arabia, and South Africa. Growing health awareness and westernized consumption patterns are influencing product demand. Regional retail expansion, supported by cross-border e-commerce and multinational brand partnerships, is enhancing vegan chocolate availability across premium outlets. Technological modernization, including AI-based logistics and digital inventory tracking, has improved supply efficiency by 23%. Local producers in the UAE are experimenting with camel milk alternatives and sustainable cocoa sourcing models to align with global vegan standards. Consumers in the region demonstrate a preference for luxury, organic vegan chocolates, with 48% choosing imported European brands due to perceived quality and flavor consistency.

• United Kingdom – 24% Market Share: Leads due to its extensive production capacity, R&D investments in dairy-free chocolate, and early regulatory adoption of vegan labeling standards.

• United States – 21% Market Share: Dominates through advanced distribution networks, strong retail partnerships, and continuous innovation in plant-based confectionery product lines.

The global Vegan Chocolate market is moderately consolidated, with the top five companies accounting for approximately 42% of total market share in 2024. Around 85 to 90 active competitors are engaged in manufacturing and distributing vegan chocolate products globally, ranging from multinational confectionery corporations to regional organic brands. Product differentiation, ingredient sourcing transparency, and sustainability certifications remain key factors driving competition.

Mergers and acquisitions have notably intensified, with 12 major strategic collaborations recorded in 2023 and 2024 aimed at expanding product lines and global reach. For instance, several brands have integrated plant-based proteins such as pea and almond into chocolate formulations to capture the growing flexitarian consumer base, which increased by 27% year-over-year. Companies are also investing in advanced tempering and micro-refining technologies to enhance texture consistency and flavor profiles, particularly in the premium segment that grew by 19% in 2024.

E-commerce penetration rose by 36% in the same year, leading brands to focus heavily on digital campaigns and subscription-based delivery models. Competitive intensity is especially high in Europe and North America, where sustainability-focused brands are adopting recyclable or compostable packaging—used by over 62% of market players in 2024. Innovation pipelines increasingly revolve around sugar-free, gluten-free, and ethically sourced cocoa variants, reflecting a strong consumer shift toward health and environmental consciousness.

Lindt & Sprüngli AG

The Hershey Company

Mondelez International

Endangered Species Chocolate LLC

Alter Eco Americas Inc.

Taza Chocolate

LoveRaw Ltd.

Hu Kitchen

Plamil Foods Ltd.

Theo Chocolate Inc.

Seed and Bean Company

Divine Chocolate Ltd.

Raaka Chocolate

Purdys Chocolatier

NibMor LLC

Technological advancements are redefining the Vegan Chocolate market landscape, driving innovation in production efficiency, ingredient formulation, and sustainability. In 2024, over 58% of vegan chocolate producers adopted automated tempering and conching systems, enabling precise temperature regulation and smoother texture consistency while lowering energy use by nearly 20%. Precision fermentation and cocoa-free production technologies are also advancing rapidly, allowing manufacturers to replicate cocoa’s flavor and aroma using oats, carob, and other plant-based inputs, reducing carbon emissions by up to 85% compared to conventional cocoa processing.

AI-integrated quality assurance systems now monitor texture, gloss, and weight in real time, cutting product waste by approximately 25%. Around 44% of large manufacturers are deploying predictive maintenance systems powered by machine learning to reduce equipment downtime and enhance production throughput. Digital traceability solutions, particularly blockchain-based supply chain tracking, are being implemented by 46% of leading brands to ensure ethical sourcing, authenticity verification, and improved transparency in vegan ingredient procurement.

Smart packaging technologies are also reshaping consumer interaction. QR-enabled packaging now accounts for nearly 15% of premium vegan chocolate launches, offering details about product origin and environmental impact. Meanwhile, 3D printing and robotic assembly in molding and decoration processes are enhancing product customization and design precision. Furthermore, plant-based emulsifiers and enzyme-assisted fat crystallization methods are improving texture, stability, and shelf life. These technological developments collectively strengthen market competitiveness by aligning production efficiency, sustainability goals, and consumer expectations for innovation and ethical quality.

In March 2023, The Hershey Company launched its first nationally-distributed vegan chocolates in the U.S., introducing “Reese’s Plant Based Peanut Butter Cups” and “Hershey’s Plant Based Extra Creamy with Almonds & Sea Salt,” made using oats instead of milk. (Inquirer.com)

In September 2024, Ferrero Group launched “Nutella Plant-Based” in select European markets including Italy, France and Belgium—a vegan version of its iconic hazelnut spread, replacing milk with chickpeas and rice syrup, packaged in a 350 g recyclable jar. (Ferrero)

In May 2025, Lindt & Sprüngli introduced “LINDOR Vegan Truffles” in Canada, crafted with oat-based chocolate to deliver the brand’s signature smooth-melting experience; a national survey showed 78 % of Canadian vegans missed milk chocolate and 47 % admitted occasionally consuming it. (GTA Today)

In 2024, Ferrero’s sustainability report confirmed that the “Nutella Plant-Based” recipe uses a jar with 60 % recycled glass content and a lid made from recycled plastic certified via the ISCC standard, supporting the brand’s strategic commitment to circular packaging and plant-based innovation.

This report offers a comprehensive review of the vegan chocolate market, covering product types such as dark/plain bars, milk-style vegan chocolate (oat/almond/rice variants), filled and compound bars, and novelty formats like truffles and coated snacks. It examines application channels including retail (supermarkets, specialty stores), online/direct-to-consumer platforms, foodservice (cafés, bakeries), and industrial ingredient use (bakery & confectionery manufacturers). The geographic scope spans regions such as North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level insights for major markets including the U.S., U.K., Germany, China, India and Brazil. Beyond segmentation, the report explores technology and industry focus areas including precision fermentation for cocoa-free formulations, plant-based milk substitutes in chocolate, clean-label and sugar-reduced developments, and sustainable packaging and sourcing initiatives. It also assesses market dynamics such as consumer behaviour trends among Millennials and Gen Z, investor funding patterns in vegan confectionery, regulatory and ESG frameworks (vegan certification, traceability, sustainable cocoa sourcing) and competitive ecosystem mapping (number of active players, consolidation, top-company shares). The analysis highlights niche opportunities such as premium gifting vegan chocolates, vegan coatings for bakery applications, and functional vegan bars fortified with proteins or probiotics. Decision-makers will find strategic insights on key drivers, technology adoption, competitive positioning and region-specific growth pathways to inform governance, investment, product development and market-entry strategies.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 1236.15 Million |

Market Revenue in 2032 | USD 3126.88 Million |

CAGR (2025 - 2032) | 12.3% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Lindt & Sprüngli AG , The Hershey Company , Mondelez International , Endangered Species Chocolate LLC, Alter Eco Americas Inc., Taza Chocolate, LoveRaw Ltd., Hu Kitchen, Plamil Foods Ltd., Theo Chocolate Inc., Seed and Bean Company, Divine Chocolate Ltd., Raaka Chocolate, Purdys Chocolatier, NibMor LLC |

Customization & Pricing | Available on Request (10% Customization is Free) |