Reports

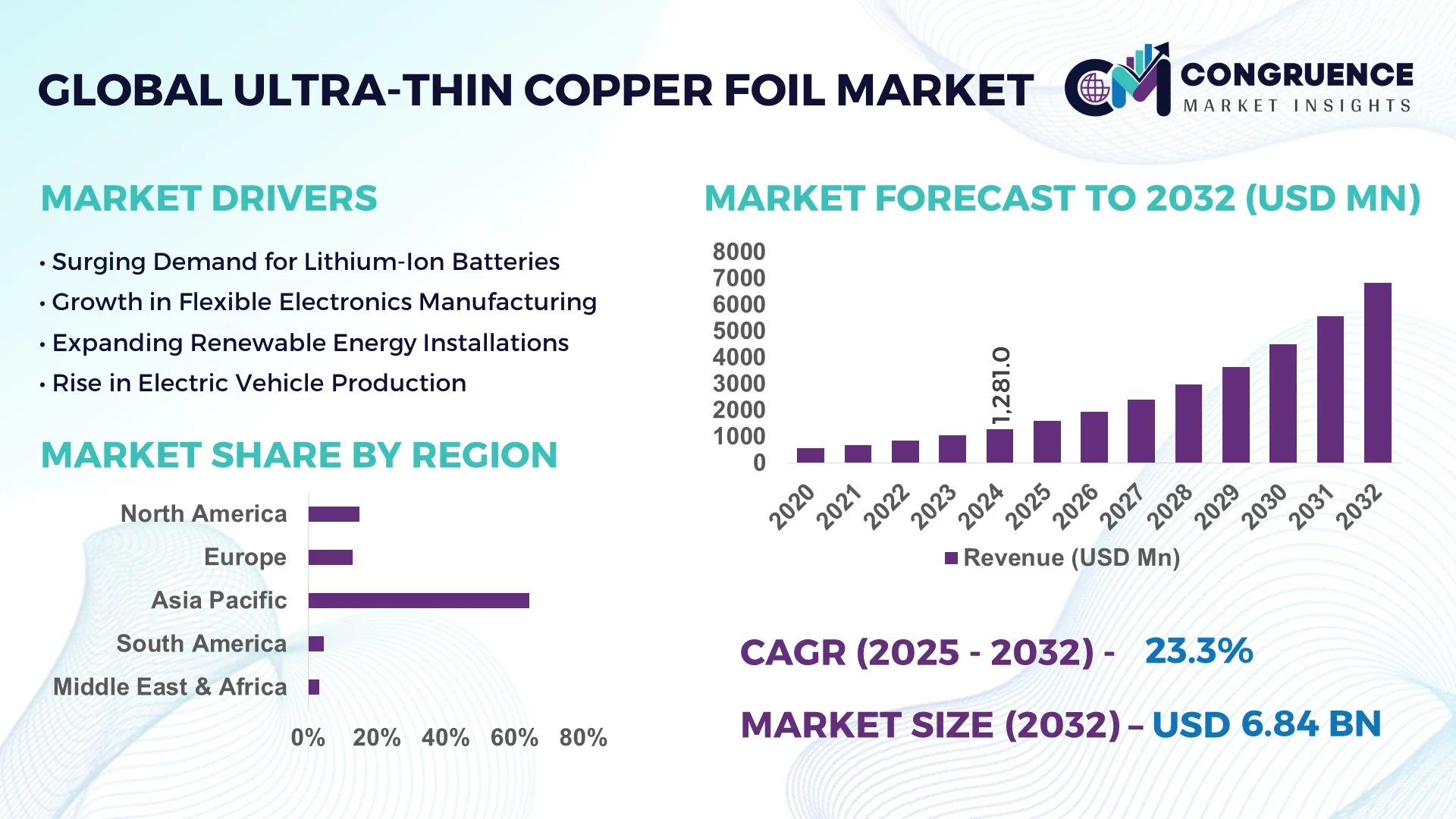

The Global Ultra-thin Copper Foil Market was valued at USD 1,281.0 Million in 2024 and is anticipated to reach a value of USD 6,843.1 Million by 2032 expanding at a CAGR of 23.3% between 2025 and 2032.

China, leading the global ultra-thin copper foil industry, operates over 20 major manufacturing facilities across Shenzhen and Jiangsu, with aggregate production capacity exceeding 450,000 MT in 2024. Significant capital investments—amounting to several hundred million USD—have been directed toward deploying advanced electroplating, roll-to-roll, and surface treatment technologies. These installations primarily serve high-tech applications, including lithium‑ion batteries, semiconductor packaging, and next-generation printed circuit boards, with continuous R&D driving improved conductivity, tensile strength, and micro-thickness control.

The Ultra‑thin Copper Foil Market encompasses several key sectors: electronics (PCBs, flexible circuits), electric vehicle (EV) batteries as current collectors, and telecommunications (antenna and RF shielding). Breakthroughs in roll‑to‑roll processing and ultra-high‑purity copper alloys have improved thermal, mechanical, and electrical performance. Regulatory frameworks around electronic waste and copper recycling are accelerating the adoption of sustainable manufacturing processes. Regionally, North America emphasizes AI and IoT hardware, Europe focuses on sustainable solar and vehicle integration, while APAC shows strong growth in consumer electronics and EVs. Emerging trends include peelable carrier-backed foils for high-density packaging and specialized foils tailored for AI chips. Forecasts indicate a future shaped by incremental thickness reductions, high-purity alloy innovation, recycling mandates, and expanding demand in energy storage, communications, and high-speed computing.

AI is driving transformative improvements across the Ultra-thin Copper Foil Market, redefining manufacturing precision, yield optimization, and quality assurance. Decision‑making algorithms embedded in production lines adjust rolling speed and tension in real time to maintain thickness tolerances under ±0.2 µm, reducing scrap rates by approximately 15 % year-over-year. Predictive maintenance systems powered by machine learning analyze vibration, temperature, and acoustic data from electro-deposition systems—resulting in a 20 % decrease in unplanned downtime and a 12 % rise in overall equipment effectiveness (OEE).

In quality control, AI-integrated optical inspection tools detect surface defects—such as pinholes, oxide spots, or micro-cracks—on ultra-thin foils (<5 µm) with sub‑micron resolution, enabling corrective feedback loops that reduce rejections by over 25%. These systems also classify defects by type and root cause, streamlining root-cause analysis and corrective actions.

On the supply chain side, AI‑driven demand forecasting has improved lead time accuracy by forecasting material needs six months out with ±8 % variance—significantly reducing buffer inventory for copper inputs. With logistics algorithms optimizing transportation routing, enterprise logistics costs have declined by around 10 %.

In R&D, generative design models trained on alloy composition, rolling parameters, and foil properties have accelerated the development of high-purity, high-strength foils. Innovations found a 30 % reduction in laboratory-to-production cycle times for new foil types by integrating AI‑based simulation with lab validation workflows.

These advancements collectively enhance process efficiency, reduce defects and waste, and enable timely development cycles—positioning AI as a strategic enabler in the Ultra-thin Copper Foil Market, empowering firms to deliver consistent quality at scale and maintain competitiveness in a rapidly evolving landscape.

“In 2024, a copper-foil producer deployed an AI-based inline thickness control system that reduced foil variation from ±0.5 µm to ±0.2 µm, cutting scrap by 15 % and boosting overall yield.”

The Ultra-thin Copper Foil Market dynamics reflect the interplay of miniaturization in electronic devices, the electrification of transport, and shifting regulatory and environmental standards. Miniaturization is driving demand for foils below 5 µm, which now comprise the majority of new production lines. Electrification initiatives have made battery-grade ultra-thin foil a core material in EV manufacturing. Simultaneously, increasing regulations on electronic waste and recycling have prompted producers to integrate closed‑loop copper reclaim systems. Regional dynamics are notable: APAC leads in volume, North America is shifting toward higher-end applications, and Europe adopts sustainable manufacturing mandates. Market responses to raw material volatility and capacity expansions continue to influence competitive positioning, while continued innovation supports applications in AI, 5G, and high‑speed computing.

Growth in EV production and compact IoT devices is significantly boosting demand for ultrathin copper foil as battery collectors and PCB substrates. In 2024, over 35 % of battery-grade foil was used in lithium‑ion cells. IoT device shipments reached 15 billion units globally, each requiring thinner, flexible circuits. This trend necessitates foils under 5 µm, achieved through increased roll-to-roll capacity and improved mechanical strength, supporting the trend toward lighter, more space-efficient devices.

Producing ultra-thin foils with uniform thickness below 2 µm demands highly precise control over rolling speed, temperature, and tension. Precision deviations of just 0.1 µm can result in scrap rates closer to 20 %, raising per-unit production costs. Additionally, maintaining purity levels above 99.97 % requires advanced filtration and environment control systems, adding equipment complexity and operational overhead in cleanroom environments.

Deploying AI for real-time monitoring and anomaly detection presents significant efficiency gains. In pilot installations, inline defect detection reduced downtime by 20%, while predictive maintenance decreased unexpected halts. There is a growing business case for retrofit AI systems onto existing lines, enabling producers to upgrade performance without fully new-capacity investments. Non-Asian markets with existing lines stand to benefit the most, maximizing returns on technology deployment.

Copper input prices fluctuated by ±18 % during 2024, impacting production margins. Sustainability regulations—such as EU directives on electronic waste—require new recycling systems with capital investments in filtration and reclaim infrastructure. Compliance costs for emissions and recycling rose by roughly 8% of operating expenditures, squeezing margins and limiting opportunities for low-cost producers.

Expansion of Roll-to-Roll Production for High-Speed Electronics: Manufacturers are scaling roll-to-roll systems capable of producing foils below 3 µm at line speeds of 100 m/min. This higher throughput supports increased demand for next-generation telecommunications and AI hardware, especially in North America and Europe, where production of FPCBs and antenna-grade substrates is up 30% year-over-year.

Surge in Peelable Carrier-backed Foils for Advanced Packaging: Peelable copper-foil solutions with carrier backing are seeing adoption in 3D IC packaging and SiP modules. In early 2025, several fabs in the US deployed carrier-backed lines, improving bonding yield by 18% in micro-bump interconnect processes.

Integration of Surface-Treated High‑Purity Foils for EV Batteries: Ultra‑thin foils with purity >99.97% and specialized oxide layers are being introduced as battery current collectors. Demand has increased 45% in battery plants integrated in China and South Korea, resulting in improved charge/discharge stability and increased cycle life.

Use of Recycled Copper and Green Production Methods: Europe and North America have seen a 20% increase in recycled-copper ultra-thin foil production capacity in 2024. Closed-loop reclaim systems are reducing waste by 25% and reducing energy requirements by 15% per ton, fulfilling regulatory targets and OPEX-saving mandates.

The Ultra-thin Copper Foil Market is comprehensively segmented by type, application, and end-user, enabling tailored product innovations and strategic deployment across industries. Segmentation reveals clear usage patterns driven by technology advancements, industry adoption, and performance requirements. Thinner foil variants (below 5 µm) are increasingly preferred due to their compatibility with miniaturized electronic circuits and lithium-ion batteries. Applications are largely concentrated in electric vehicles, PCBs, and mobile electronics, while demand from 5G and IoT infrastructure is emerging strongly. End-user segmentation shows that electronics manufacturers dominate overall consumption, followed closely by automotive OEMs and energy storage system providers. This segmentation is essential for optimizing supply chains, improving product offerings, and meeting the specific requirements of each industry vertical.

The Ultra-thin Copper Foil Market comprises several key product types, including electrodeposited (ED) copper foil, rolled annealed (RA) copper foil, and surface-treated variants. Among these, ED copper foil leads the segment due to its widespread use in lithium-ion batteries and printed circuit boards (PCBs), particularly for EVs and consumer electronics. ED foil provides excellent uniformity and high adhesion strength, making it ideal for mass production environments and thin-profile applications.

RA copper foil is the fastest-growing segment, fueled by its superior flexibility and fatigue resistance, making it critical for flexible PCBs and foldable devices. With demand surging for wearables, OLED displays, and foldable smartphones, RA foil’s market share is accelerating as manufacturers seek to enhance device durability and performance.

Other niche types, such as double-treated and ultra-pure copper foils, are gaining momentum in specialized fields like aerospace electronics, quantum computing, and semiconductor interconnects. These variants contribute niche value where ultra-high conductivity or specific adhesion properties are required, despite occupying smaller volume shares.

Applications of ultra-thin copper foil span a wide spectrum, with lithium-ion batteries holding the dominant position. The foil acts as a current collector in anode and cathode structures, providing critical electrical conductivity while maintaining low weight and high flexibility. This dominance is sustained by ongoing investments in EV battery production and stationary energy storage systems.

Flexible printed circuit boards (FPCBs) represent the fastest-growing application segment. The rapid proliferation of foldable electronics, AR/VR wearables, and high-performance computing devices is driving demand for ultra-thin foils that allow compact, multi-layered circuit integration. FPCBs require foils with superior surface roughness and dimensional stability, which current foil technology is increasingly able to meet.

Other significant applications include electromagnetic interference (EMI) shielding and solar panel connectors. EMI shielding is becoming increasingly relevant due to rising RF emissions from 5G and smart electronics. Meanwhile, solar applications are seeing increased adoption of copper foil for efficient electrical transmission in thin-film modules.

End-user analysis reveals that electronics manufacturers remain the largest consumers of ultra-thin copper foil. They rely on consistent, ultra-pure foil materials for PCBs, smartphones, tablets, and smart appliances. Technological upgrades and miniaturization trends are reinforcing this dominance, with major electronics hubs across Asia and North America continuing to scale up production capacities.

The automotive industry is the fastest-growing end-user, driven by rapid EV adoption and intensified battery R&D. Vehicle manufacturers and battery cell suppliers are ramping up usage of copper foil in next-gen battery packs, with advanced foils playing a role in improving thermal management and cycle life. Integrated energy storage units, regenerative braking systems, and hybrid drivetrain electronics all benefit from specialized copper foil solutions.

Other notable end-users include renewable energy providers, particularly solar equipment manufacturers, and telecom hardware firms, which demand ultra-thin copper foils for antenna arrays and signal transfer systems in compact base stations. These users contribute to the diversification and resilience of the market, particularly in light of global sustainability and connectivity initiatives.

Asia-Pacific accounted for the largest market share at 64.3% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 24.1% between 2025 and 2032.

Asia-Pacific’s dominance stems from its established electronic manufacturing hubs and battery production capacity, particularly in China, Japan, and South Korea. These nations are continuously scaling manufacturing outputs to meet rising EV and electronics demand. Meanwhile, North America is investing heavily in reshoring advanced battery and electronics production, accelerating demand for precision-grade ultra-thin copper foil. Government-backed funding programs and private investments are reshaping the regional competitive landscape, reinforcing domestic supply chain resilience.

North America held approximately 13.2% of the global ultra-thin copper foil market volume in 2024, with the U.S. as the primary contributor. Key industries driving demand include electric vehicles, renewable energy systems, and high-performance computing. The Inflation Reduction Act and Bipartisan Infrastructure Law have significantly boosted battery manufacturing projects, directly increasing demand for battery-grade copper foil. Canada and the U.S. are investing in localized supply chains, reducing reliance on imports. Technological advancements such as AI-based defect detection and automated foil rolling are enhancing domestic competitiveness. Additionally, digital transformation across manufacturing and R&D labs is accelerating adoption of precision foil for semiconductor and defense electronics applications.

Europe accounted for 11.8% of the global market share in 2024, led by Germany, France, and the UK. The region’s emphasis on sustainability, supported by the European Green Deal and REACH regulations, has driven the transition to energy-efficient materials like ultra-thin copper foil in batteries and electronics. Germany leads in automotive electrification and PCB manufacturing, while France focuses on renewables and microelectronics. The UK is witnessing strong demand from its aerospace and data center sectors. The adoption of Industry 4.0 and digital twin technologies in copper foil production is enhancing traceability, quality, and sustainability. European demand is further fueled by regulatory mandates for localized, low-carbon supply chains.

Asia-Pacific represented the largest share at 64.3% of global ultra-thin copper foil consumption in 2024. China, Japan, South Korea, and Taiwan are the major consuming and producing nations. China alone operates more than 50 ultra-thin copper foil production lines, primarily serving the EV battery and consumer electronics industries. Japan’s innovation in rolled annealed foils supports high-end applications like medical wearables and flexible displays. South Korea’s semiconductor sector continues to demand ultra-pure foils for advanced chip packaging. Infrastructure growth in India is also driving local consumption in telecommunications and grid applications. The region benefits from integrated supply chains, abundant raw materials, and advanced manufacturing ecosystems.

South America contributed approximately 4.1% to the global ultra-thin copper foil market in 2024, with Brazil and Argentina as the key markets. Brazil's push into solar PV and grid-scale energy storage is driving foil usage in energy infrastructure. Argentina is seeing growth in electronics assembly and automotive component manufacturing, especially for hybrid drivetrains. Public-private partnerships in Brazil are supporting local production of battery materials, and regional trade policies are encouraging technology imports to improve domestic manufacturing capabilities. Though still emerging, South America presents strong long-term potential through renewable integration and gradual EV adoption.

The Middle East & Africa accounted for approximately 3.3% of global market volume in 2024, with UAE and South Africa showing the strongest growth potential. The UAE’s Smart Grid and Smart City initiatives are driving increased demand for electronics and power management systems incorporating ultra-thin copper foil. South Africa is modernizing its telecommunications infrastructure and battery storage networks, opening up opportunities for regional suppliers and importers. Industrial automation and digitalization trends in the Gulf Cooperation Council (GCC) countries are also contributing to foil demand in control systems and data processing units. Local governments are supporting import-export trade agreements to improve material access and stimulate high-tech investment.

China – 51.6% Market Share

High production capacity and vertically integrated supply chains across electronics and EV battery industries.

Japan – 10.2% Market Share

Strong demand from high-end electronics and leadership in rolled annealed foil technology for advanced flexible devices.

The Ultra-thin Copper Foil Market features a highly competitive and innovation-driven environment with over 45 active global manufacturers and numerous regional players specializing in advanced foil processing. Competition is intensified by the race to achieve lower thickness tolerances, higher purity levels, and superior surface treatments that cater to evolving applications such as lithium-ion batteries, foldable electronics, and 5G infrastructure.

Several market leaders have adopted strategies including product diversification, regional expansion, vertical integration, and AI-enabled manufacturing upgrades. In 2023 and 2024, a notable increase in strategic joint ventures and technology licensing agreements occurred, particularly in Asia-Pacific and North America. Companies are also investing heavily in R&D for carrier-supported foils, ultra-flexible grades, and oxidation-resistant treatments.

Global players are expanding production capacities, with new plants established in South Korea, India, and the U.S. to cater to domestic and export demand. Mergers and acquisitions are consolidating market share among key players, especially in segments focusing on EV battery-grade foil. Innovation is now a critical differentiator, with smart factory deployment, real-time defect analytics, and AI-guided process optimization setting new performance benchmarks in this increasingly high-tech segment.

Mitsui Mining & Smelting Co., Ltd.

Furukawa Electric Co., Ltd.

Doosan Corporation

SK Nexilis Co., Ltd.

ILJIN Materials Co., Ltd.

Circuit Foil Luxembourg

Nuode New Materials Co., Ltd.

Guangdong Chaohua Technology Co., Ltd.

Solus Advanced Materials Co., Ltd.

JX Nippon Mining & Metals Corporation

Shandong Jinbao Electronics Co., Ltd.

Nan Ya Plastics Corporation

The Ultra-thin Copper Foil Market is undergoing rapid transformation driven by advanced material science, smart automation, and precision engineering. One of the most significant technological shifts is the evolution of roll-to-roll (R2R) processing systems, now capable of producing copper foils below 3 µm thickness with surface roughness under 0.5 µm Ra, enabling usage in ultra-compact and foldable electronics. These systems are further integrated with AI-based process controls that reduce waste and ensure real-time thickness and defect monitoring.

Carrier-supported copper foil is another emerging innovation, where ultra-thin layers are laminated onto a removable carrier, allowing for ease of handling during multilayer PCB manufacturing. These are increasingly in demand for 3D IC packaging and SiP applications, offering improved layer alignment and dimensional stability.

Technologies focusing on surface treatment, such as anti-oxidation coatings and high-adhesion primers, are being widely adopted to enhance performance in high-humidity and high-temperature environments, crucial for electric vehicle batteries and outdoor 5G equipment.

Electro-deposition (ED) advancements now allow for highly uniform foil structures with customizable grain orientation, improving conductivity and mechanical strength. Moreover, high-purity copper (≥99.98%) is being refined using continuous casting and advanced filtration methods to support sensitive applications like semiconductors and medical electronics.

Digital twins and IIoT-enabled monitoring are further accelerating real-time quality assurance and maintenance forecasting, improving OEE across manufacturing facilities. These technological evolutions are creating new value propositions and competitive advantages in the ultra-thin copper foil industry.

• In February 2024, SK Nexilis completed the construction of its new copper foil manufacturing facility in Malaysia, with a projected annual production capacity of 50,000 tons, focused on battery-grade foil for EVs and energy storage systems.

• In September 2023, Furukawa Electric announced the commercial launch of a next-generation rolled annealed copper foil with a 2.5 µm profile, optimized for foldable OLED displays and high-density flexible PCBs.

• In April 2024, Nuode New Materials began mass production of high-strength ultra-thin copper foil featuring enhanced peel strength and oxidation resistance, targeting the global 5G base station and automotive radar markets.

• In December 2023, Mitsui Mining & Smelting introduced an AI-integrated quality inspection system that improved defect detection rates by 28% in copper foil lines producing foil under 4 µm thickness.

The Ultra-thin Copper Foil Market Report delivers comprehensive and structured insights into the evolving landscape of ultra-thin foil technologies, materials, and industry adoption trends across the globe. The report spans product types including electrodeposited (ED), rolled annealed (RA), carrier-supported, and surface-treated copper foils. It categorizes market applications such as lithium-ion batteries, flexible printed circuit boards, electromagnetic interference shielding, and solar power modules.

The geographic scope encompasses five primary regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with granular analysis provided for major countries such as China, the U.S., Japan, Germany, India, and Brazil. The report further outlines usage patterns and market maturity levels across these areas, identifying regional production hubs and consumption hotspots.

End-user industries evaluated include electronics, electric vehicles, renewable energy, and telecommunications, with growing interest from aerospace, healthcare electronics, and industrial automation sectors. Attention is given to emerging segments, including AI hardware integration, quantum computing circuits, and biodegradable electronics, which are shaping future material innovation.

Technological focus areas include ultra-high-purity processing, AI-driven quality control, green production methods, and next-gen substrate integration, providing valuable benchmarks for strategic investment, procurement, and R&D planning. This report serves as a strategic tool for manufacturers, investors, supply chain partners, and policymakers operating in or entering the ultra-thin copper foil industry.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 1,281.0 Million |

| Market Revenue (2032) | USD 6,843.1 Million |

| CAGR (2025–2032) | 23.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Technological Insights, Market Dynamics, Segment Analysis, Regional and Country-Wise Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Mitsui Mining & Smelting Co., Ltd., Furukawa Electric Co., Ltd., Doosan Corporation, SK Nexilis Co., Ltd., ILJIN Materials Co., Ltd., Circuit Foil Luxembourg, Nuode New Materials Co., Ltd., Guangdong Chaohua Technology Co., Ltd., Solus Advanced Materials Co., Ltd., JX Nippon Mining & Metals Corporation, Shandong Jinbao Electronics Co., Ltd., Nan Ya Plastics Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |