Reports

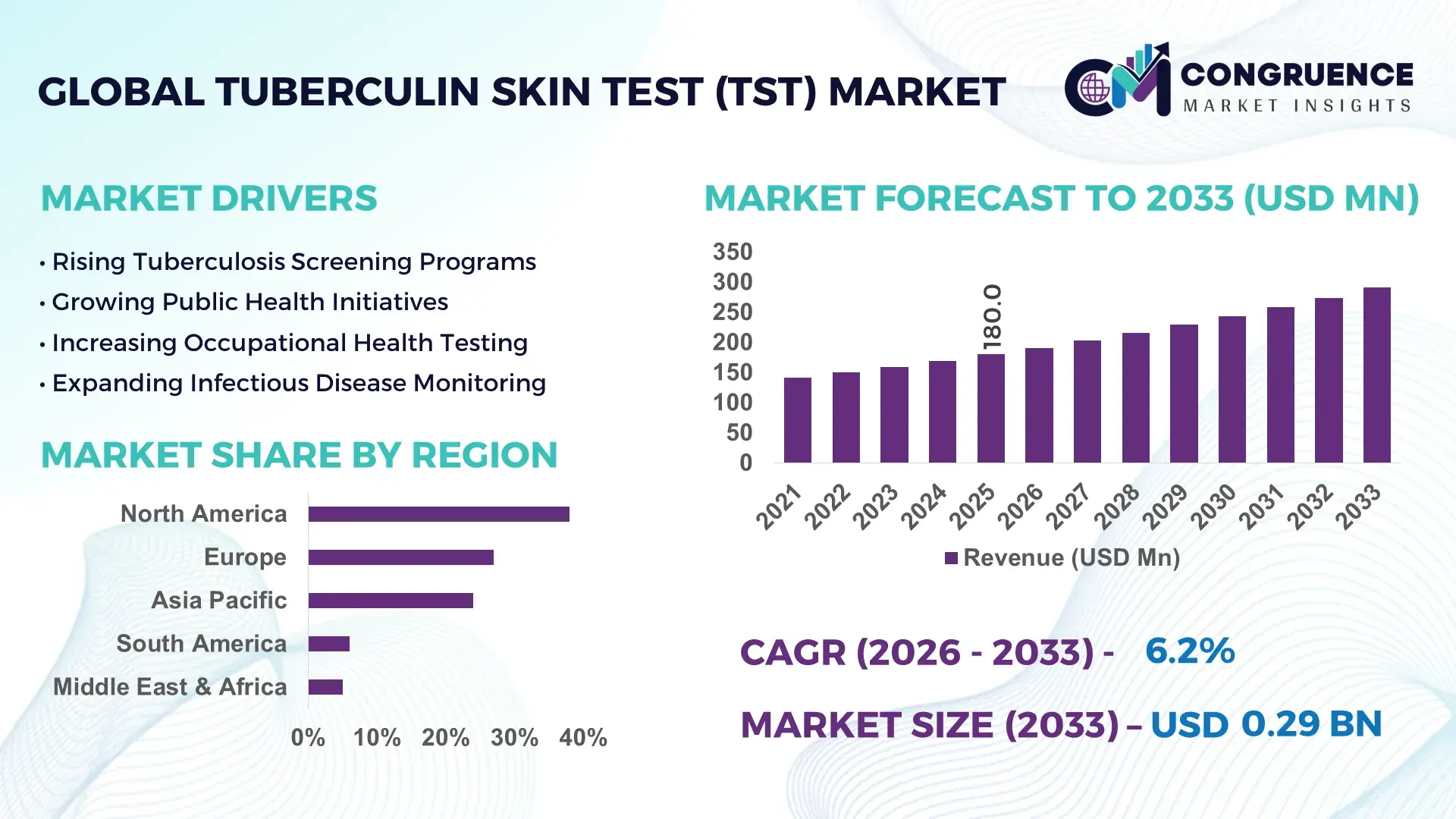

The Global Tuberculin Skin Test (TST) Market was valued at USD 180.0 Million in 2025 and is anticipated to reach a value of USD 291.3 Million by 2033 expanding at a CAGR of 6.2% between 2026 and 2033. Growth is being accelerated by expanding latent tuberculosis screening programs, occupational health compliance requirements, and government-backed tuberculosis elimination initiatives across high-burden countries.

The United States remains the dominant market, accounting for approximately 31% of global TST consumption, supported by annual screening requirements across healthcare, correctional, and public-sector workforces. In comparison, India records over 2.8 million tuberculosis cases annually and continues expanding public screening coverage under national TB elimination targets. The U.S. demonstrates higher test standardization and digital reporting adoption, while India leads in testing volume and public-health deployment scale. The renewed global focus on infectious disease surveillance following the COVID-19 period has further strengthened procurement activity and screening infrastructure.

Strategically, market participants that align manufacturing capacity, public-health partnerships, and diagnostic workflow integration with national screening mandates are positioned to secure long-term procurement advantages.

Market Size & Growth: USD 180.0 Million in 2025 with projected expansion to USD 291.3 Million by 2033, supported by rising latent TB screening coverage, workplace compliance programs, and public-health diagnostics modernization.

Top Growth Drivers: Occupational screening demand contributes ~28%, government TB-control initiatives ~34%, and healthcare workforce testing programs ~22% of annual procurement activity.

Short-Term Forecast: By 2028, digital result-tracking adoption is expected to improve screening workflow efficiency by nearly 20% across large healthcare systems.

Emerging Technologies: AI-enabled reporting platforms, digital patient-monitoring tools, and automated diagnostic record management are reducing administrative burden by 15–18%.

Regional Leaders: North America exceeds USD 90 Million, Asia-Pacific approaches USD 75 Million, and Europe surpasses USD 55 Million, each driven by structured screening protocols and healthcare modernization.

Consumer/End-User Trends: More than 60% of institutional testing demand originates from hospitals, public-health agencies, and occupational health programs.

Pilot/Case Example: In 2024, several U.S. healthcare networks integrated electronic TB screening systems, reducing reporting turnaround times by approximately 25%.

Competitive Landscape: One leading manufacturer controls roughly 24% market share, while key participants include Sanofi Pasteur, Par Sterile Products, Japan BCG Laboratory, and AJ Vaccines.

Regulatory & ESG Impact: Tuberculosis elimination frameworks in over 80 countries are improving screening access while strengthening public-health accountability metrics.

Investment & Funding: Global TB-control and screening programs attract more than USD 1.5 Billion annually through public-health funding, partnerships, and healthcare infrastructure expansion.

Innovation & Future Outlook: Advanced digital surveillance, integrated diagnostic platforms, and decentralized community screening models are reshaping next-generation tuberculosis detection strategies.

The Tuberculin Skin Test (TST) Market continues to benefit from sustained demand across public-health agencies, hospitals, occupational health networks, and immigration screening programs. Recent innovation focuses on digital result documentation, integrated surveillance platforms, and improved cold-chain management for biologic reagents. Nearly 40% of new screening initiatives now incorporate electronic reporting capabilities. Ongoing tuberculosis elimination policies and healthcare infrastructure upgrades across Asia and Africa are creating new deployment opportunities, setting the stage for broader strategic market development.

Tuberculin skin testing is becoming increasingly important within global infectious disease management strategies as governments, healthcare systems, and employers intensify efforts to identify latent tuberculosis infections before progression to active disease. The market's strategic value extends beyond diagnostics, supporting workforce compliance, public-health surveillance, immigration health assessments, and disease-control planning. Increased digitalization of screening records and modernization of healthcare infrastructure are strengthening testing program efficiency and traceability.

A notable market shift is the integration of digital health platforms into tuberculosis screening workflows. Facilities using electronic reporting systems have reported administrative workload reductions of nearly 20% compared with manual documentation processes. The United States leads in standardized occupational screening and digital deployment, while India demonstrates substantially higher testing volumes due to its disease burden and nationwide elimination initiatives. Over the next two to three years, healthcare providers are expected to expand electronic tracking systems across public-health networks, improving patient follow-up rates and reducing documentation delays.

Operationally, major suppliers are strengthening regional distribution networks, expanding manufacturing resilience, and pursuing partnerships with public-health agencies to secure long-term procurement contracts. Organizations deploying integrated screening and reporting solutions gain stronger compliance performance, improved operational visibility, and enhanced competitive positioning within the evolving tuberculosis diagnostics ecosystem.

Government-led tuberculosis elimination initiatives continue to represent the strongest structural growth catalyst. India accounts for approximately 27% of global tuberculosis cases, driving large-scale screening investments and procurement programs. More than 70% of occupational health screening protocols in developed healthcare systems incorporate tuberculosis testing requirements for frontline workers. Simultaneously, healthcare facilities are expanding latent infection surveillance following renewed infectious disease preparedness strategies. This regulatory and public-health focus directly increases recurring testing volumes and strengthens demand visibility for manufacturers. In response, suppliers are expanding production capacity, improving reagent availability, and establishing partnerships with healthcare authorities. A key strategic insight is that recurring compliance-driven testing generates more predictable demand patterns than outbreak-driven diagnostic procurement, supporting stronger long-term operational planning.

The market remains exposed to supplier concentration risks because a limited number of manufacturers account for a significant share of global purified protein derivative (PPD) production. Historical shortages have disrupted procurement cycles in multiple countries, while biologic product manufacturing requires strict quality-control standards that can extend production timelines by 15–20%. Cold-chain logistics also increase distribution complexity and operating costs. In the United States, healthcare providers have periodically relied on allocation programs during supply disruptions, affecting testing continuity. To mitigate these challenges, companies are pursuing supplier diversification, regional manufacturing expansion, and longer-term procurement agreements. A critical operational concern remains maintaining uninterrupted product availability while meeting stringent regulatory and quality requirements across multiple jurisdictions.

The convergence of tuberculosis screening with digital health infrastructure presents a significant growth opportunity. Approximately 40% of newly launched public-health screening initiatives now include electronic reporting and patient-tracking capabilities. Countries such as India, Indonesia, and the Philippines are expanding community-based screening networks, creating substantial untapped testing demand. Advanced digital platforms can reduce administrative processing times by nearly 20% while improving patient follow-up efficiency. Companies are responding through investments in connected diagnostics, data-management partnerships, and integrated public-health solutions. A particularly valuable opportunity lies in combining TST deployment with broader infectious disease surveillance programs, enabling healthcare systems to leverage existing infrastructure and reduce operational costs across multiple screening activities.

The primary long-term challenge involves maintaining consistent deployment amid increasing use of alternative tuberculosis diagnostic technologies. Interferon-gamma release assays (IGRAs) offer laboratory-based testing advantages in selected clinical settings, creating competitive pressure in higher-income healthcare markets. Healthcare organizations report up to 30% variation in tuberculosis screening protocols across institutions, complicating standardization efforts. Workforce training requirements, documentation consistency, and integration with digital health records further increase implementation complexity. Companies must invest in clinician education, workflow optimization, and interoperability solutions to sustain competitive relevance. The strongest market participants will be those that combine reliable product supply, digital integration capabilities, and public-health partnerships to ensure scalable and consistent deployment across diverse healthcare environments.

Digital Screening Workflow Expansion Healthcare institutions are accelerating digital tuberculosis screening management, with electronic documentation adoption increasing by nearly 35% over the past two years. More than 40% of large hospital networks now integrate test scheduling, reporting, and compliance tracking into centralized health information systems. This transition reduces administrative processing time by approximately 20% and improves follow-up compliance. Diagnostic suppliers are responding through software partnerships and integrated reporting platforms that strengthen operational efficiency while supporting stricter healthcare documentation requirements.

Supply Resilience and Localization Supply continuity has become a major operational priority following biologics manufacturing disruptions and transportation bottlenecks. Several healthcare systems have expanded inventory buffers by 15–20%, while procurement agencies increasingly favor multi-source supply contracts. In the United States, institutional buyers are emphasizing supplier diversification to reduce testing interruptions. Manufacturers are expanding regional distribution networks, increasing local warehousing capacity, and restructuring procurement strategies to improve product availability and strengthen customer retention.

Occupational Health Program Scaling Workforce screening requirements continue expanding across healthcare, correctional facilities, and public-sector organizations. More than 60% of institutional testing demand now originates from employee health programs, while annual screening compliance rates exceed 80% in many regulated healthcare environments. Rising workforce mobility and stricter infection-control standards are increasing testing frequency. Companies are investing in streamlined screening workflows, automated compliance management systems, and enterprise health partnerships to handle larger testing volumes with lower administrative burden.

Integration With Public Health Surveillance Tuberculosis elimination initiatives are increasingly linked with broader infectious disease monitoring frameworks. Approximately 30% of newly launched community screening projects now incorporate centralized surveillance databases and population-level reporting capabilities. India and several Southeast Asian countries are expanding digital case-tracking infrastructure to improve screening coverage and referral management. This shift enhances data visibility, accelerates intervention planning, and strengthens resource allocation. Diagnostic providers are aligning products with national surveillance systems and public-health partnerships to secure long-term deployment opportunities.

Single-Step TST remains the leading segment, accounting for an estimated 58% of global testing volume due to its simplicity, lower administration burden, and suitability for large-scale screening programs. Hospitals, occupational health providers, and public-health agencies continue to favor single-visit deployment models where rapid patient throughput is essential. Its operational advantages include lower staffing requirements, streamlined logistics, and easier integration into routine compliance programs. Manufacturers continue prioritizing production efficiency and distribution expansion to support consistent procurement demand across high-volume testing environments. Two-Step TST represents the fastest-growing segment, supported by increased adoption in healthcare worker screening, long-term care facilities, and high-risk occupational settings where baseline testing accuracy is critical. Utilization within institutional screening programs has increased by nearly 18% over the past three years as employers strengthen infection-control protocols. The Others category maintains strategic relevance in specialized clinical scenarios and pilot screening initiatives. Companies are expanding educational programs, refining testing protocols, and strengthening healthcare partnerships to support broader adoption of differentiated testing approaches. Investment priorities increasingly focus on improving workflow consistency and reducing interpretation variability across large screening networks.

Public Health Screening remains the dominant application segment, representing approximately 42% of global test utilization. National tuberculosis control programs, immigration screening requirements, and community surveillance initiatives continue to generate large-scale testing demand. Countries with elevated tuberculosis incidence rates are expanding outreach programs, increasing screening coverage, and integrating testing activities with broader infectious disease monitoring frameworks. The segment benefits from recurring government procurement cycles and established public-health infrastructure, creating stable demand patterns for suppliers. Occupational Health Testing is emerging as the fastest-growing application, supported by stricter workplace health standards and expanded screening requirements across healthcare, correctional, and public-sector organizations. Adoption within enterprise compliance programs has increased by roughly 20% since 2023. Hospitals and Diagnostic Laboratories remain essential application areas, contributing significant testing volumes through patient screening and referral-based diagnostics. Market participants are responding through workflow automation, digital reporting integration, and service partnerships that improve testing efficiency while supporting high-volume deployment. Demand is increasingly shifting toward applications requiring standardized documentation and long-term compliance tracking.

Government Health Agencies constitute the largest end-user segment, accounting for nearly 40% of total procurement activity due to their responsibility for national tuberculosis control programs, community screening campaigns, and surveillance initiatives. Large-scale purchasing agreements, centralized distribution systems, and public-health mandates support substantial testing volumes. These organizations increasingly emphasize data-driven screening programs and digital reporting capabilities, creating opportunities for suppliers offering integrated diagnostic and workflow solutions. Demand concentration remains strongest in countries actively pursuing tuberculosis elimination targets. Hospitals & Clinics represent the fastest-growing end-user category, with testing volumes increasing by approximately 16% over recent years as healthcare facilities strengthen employee screening and patient risk-assessment protocols. Diagnostic Centers continue expanding their role through outsourced testing services and institutional partnerships, while Research Institutes contribute to specialized studies, validation projects, and diagnostic innovation programs. Companies are adapting through customized procurement models, strategic partnerships, and expanded service offerings tailored to the unique operational requirements of each buyer group. Future demand is increasingly linked to integrated screening ecosystems rather than standalone diagnostic procurement.

North America accounted for the largest market share at 38.0% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

North America maintains its leading position through highly structured occupational health screening programs, advanced healthcare infrastructure, and mandatory tuberculosis surveillance protocols across healthcare facilities. The region contributes approximately 38% of global market activity, supported by extensive testing among healthcare workers, correctional institutions, and immigration programs. More than 70% of large healthcare systems utilize integrated electronic compliance tracking platforms that improve screening management and reporting accuracy. Ongoing investment in public-health modernization and workforce health monitoring continues to sustain procurement demand. Strategic partnerships between healthcare providers and diagnostic suppliers are strengthening distribution efficiency and ensuring consistent product availability across institutional networks.

United States Market Outlook: The United States represents the largest national market due to comprehensive healthcare workforce screening requirements and established public-health surveillance systems. Annual tuberculosis testing programs cover millions of healthcare professionals, government employees, and high-risk populations. Digital health integration continues advancing, with more than 60% of large healthcare networks utilizing centralized employee health management platforms. Regulatory consistency, strong purchasing power, and extensive occupational screening infrastructure provide suppliers with predictable procurement cycles and long-term contract opportunities.

Europe remains a significant market supported by harmonized healthcare standards, strong public-health systems, and growing emphasis on preventive disease management. The region accounts for nearly 27% of global testing demand, with adoption concentrated in institutional healthcare environments and migrant health screening programs. Several countries have expanded electronic health record integration, reducing administrative processing times by approximately 15%. Public-health agencies continue strengthening latent tuberculosis detection strategies through coordinated surveillance frameworks and standardized testing protocols. Diagnostic providers are increasingly collaborating with national healthcare authorities to improve accessibility and streamline screening workflows.

Germany Market Outlook: Germany leads the European market through its advanced healthcare infrastructure, strong occupational health framework, and extensive public-health monitoring capabilities. Large hospital systems and industrial employers maintain rigorous screening programs for healthcare personnel and high-risk workers. More than 80% of major healthcare institutions utilize digital patient management systems that support efficient test documentation and compliance tracking. The country's focus on healthcare modernization and workforce protection continues to create stable demand for diagnostic screening technologies.

Asia-Pacific represents the fastest-expanding market due to its large tuberculosis burden, expanding healthcare access, and increasing investment in disease surveillance infrastructure. The region contributes approximately 24% of global market activity while accounting for the largest testing volumes. Government-led screening initiatives have expanded by nearly 25% across several high-burden countries during recent years. Public-health agencies continue investing in laboratory networks, digital reporting systems, and community screening programs to improve early detection rates. Suppliers are scaling regional manufacturing, distribution, and partnership networks to support rising procurement requirements and improve market accessibility.

India Market Outlook: India serves as the most strategically important market in Asia-Pacific due to its large tuberculosis screening requirements and national elimination objectives. The country records one of the world's highest tuberculosis case burdens, driving extensive public-health testing programs. Government initiatives continue expanding screening coverage through community outreach, healthcare facility integration, and digital surveillance systems. More than 2.8 million tuberculosis cases are reported annually, creating sustained demand for large-scale diagnostic deployment. Manufacturers are increasingly prioritizing local partnerships, distribution expansion, and procurement alignment with national health initiatives.

South America continues strengthening its tuberculosis screening infrastructure through targeted public-health investments and expanded disease surveillance programs. The region accounts for approximately 6% of global market activity, with demand concentrated in urban healthcare networks and government-led screening initiatives. Several countries have increased tuberculosis detection funding by more than 10% in recent years to improve testing coverage among vulnerable populations. Despite infrastructure disparities between urban and rural areas, healthcare modernization efforts are improving diagnostic accessibility. Suppliers are focusing on distributor partnerships and localized logistics strategies to enhance product availability and support regional deployment requirements.

Brazil Market Outlook: Brazil dominates the South American market through its extensive public-health network and large-scale infectious disease monitoring programs. National tuberculosis control initiatives continue driving substantial testing demand across public healthcare facilities. The country's integrated healthcare system supports broad deployment of screening services, particularly in densely populated urban centers. Expanded digital reporting initiatives and strengthened surveillance capabilities are improving case identification and monitoring efficiency. Market participants increasingly view Brazil as a strategic gateway for broader regional expansion and partnership development.

The Middle East & Africa market is being shaped by healthcare infrastructure development, public-health modernization, and increased focus on infectious disease control. The region represents approximately 5% of global market activity but remains strategically important due to elevated tuberculosis prevalence in several countries. Healthcare investment programs have increased screening capacity by nearly 20% within selected public-health systems. Governments and international health organizations continue supporting diagnostic infrastructure upgrades, workforce training, and surveillance enhancement initiatives. Suppliers are strengthening distribution networks and collaborating with healthcare agencies to improve access to screening technologies across underserved populations.

South Africa Market Outlook: South Africa remains the most influential market within the region due to its substantial tuberculosis burden and established public-health response infrastructure. National disease-control programs support extensive screening initiatives across healthcare facilities and community health networks. The country continues investing in diagnostic capacity expansion, digital case monitoring, and integrated surveillance systems. Public-sector procurement remains a key market driver, while partnerships between healthcare authorities and diagnostic providers are improving testing accessibility. These operational advantages position South Africa as a central hub for tuberculosis screening activities across the African continent.

The Tuberculin Skin Test (TST) market is led by established biologics manufacturers including Sanofi Pasteur, Par Sterile Products, AJ Vaccines, Japan BCG Laboratory, and regional biologics suppliers competing for institutional procurement contracts. The top five players collectively control approximately 68% of global market activity, creating a moderately concentrated market structure. Global manufacturers compete through supply reliability and regulatory compliance, while regional producers compete primarily on pricing and localized distribution. Product availability influences nearly 35% of procurement decisions, whereas long-term public-health contracts account for over 40% of recurring demand. Companies are strengthening market positions through manufacturing expansion, healthcare partnerships, distribution integration, and digital reporting compatibility.

Competitive pressure is increasingly shifting toward supply-chain resilience after previous biologics shortages exposed procurement vulnerabilities. Regulatory approvals, biologics manufacturing expertise, and cold-chain infrastructure remain significant entry barriers. Winning requires uninterrupted supply, institutional trust, regulatory consistency, and strong public-health procurement relationships.

Par Sterile Products

AJ Vaccines

Japan BCG Laboratory

Serum Institute of India

Statens Serum Institut

Bio Farma

China National Biotec Group

GreenSignal Bio Pharma

Zydus Lifesciences

Biological E

Bharat Biotech

Indian Immunologicals

Bionet Asia

The technology landscape is evolving from standalone skin testing toward digitally connected tuberculosis screening ecosystems. Electronic screening management platforms are now deployed in approximately 40% of large institutional programs, improving administrative efficiency by nearly 20%. Digital scheduling, automated compliance tracking, and integrated health-record connectivity are reducing documentation errors and accelerating workforce screening operations. Organizations with centralized screening systems benefit from stronger regulatory compliance and lower operational overhead.

Emerging technologies increasingly focus on integration rather than replacing TST procedures. Digital surveillance platforms, cloud-based reporting tools, and AI-assisted tuberculosis screening workflows are becoming standard components of national disease-control programs. Traditional paper-based reporting can require 25–30% more administrative effort compared with integrated digital workflows. New-generation diagnostic ecosystems improve patient tracking, referral management, and screening visibility across healthcare networks. Public-health agencies and large hospital systems gain the greatest operational advantage because they manage high testing volumes and compliance-driven reporting requirements.

Between 2026 and 2028, technology investment will increasingly target connected surveillance infrastructure, automated screening coordination, and advanced data analytics. More than 50% of newly launched tuberculosis screening initiatives are expected to incorporate digital monitoring capabilities. Manufacturers that combine biologics expertise with workflow integration and health-data interoperability will strengthen competitive positioning. The most significant technology opportunity lies in linking TST deployment with broader infectious disease surveillance systems, creating measurable efficiency gains, improved resource allocation, and stronger public-health decision-making capabilities.

June 2025 – World Health Organization (WHO): WHO approved six computer-aided detection software products for tuberculosis screening following independent evaluation. The approval expanded validated digital screening options from earlier generations to six qualified platforms, strengthening large-scale screening efficiency and accelerating diagnostic workflow modernization. Source: www.who.int

August 2025 – World Health Organization (WHO): WHO released updated Target Product Profiles for tuberculosis screening tests, providing technology-agnostic guidance for future screening solutions. The framework supports multiple screening modalities and aims to improve accessibility, affordability, and operational deployment in high-burden settings.

October 2025 – WHO Ethiopia & Ministry of Health Ethiopia: Ethiopia launched a national AI-powered digital X-ray screening program for tuberculosis. The initiative established nationwide implementation guidelines and expanded health-worker training programs, strengthening screening capacity and accelerating case-finding activities across public-health networks.

March 2026 – World Health Organization: WHO intensified global tuberculosis elimination efforts through updated diagnostic recommendations and accelerated deployment guidance aimed at improving case detection efficiency. The initiative focuses on expanding access to innovative diagnostic technologies and reducing detection gaps in resource-constrained healthcare systems.

The report provides comprehensive analysis of the Tuberculin Skin Test (TST) market across key types including Single-Step TST, Two-Step TST, and other testing formats. Coverage extends across major applications such as public health screening, hospitals, diagnostic laboratories, and occupational health testing, alongside end-user evaluation covering hospitals & clinics, government health agencies, diagnostic centers, and research institutes. The assessment examines deployment trends, procurement patterns, screening workflow modernization, and evolving tuberculosis surveillance requirements across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The study evaluates competitive positioning, technology adoption, supply-chain dynamics, and regulatory developments influencing market direction between 2026 and 2033. More than 60% of market demand is linked to institutional and public-health screening programs, while digital reporting adoption continues expanding across healthcare systems. Strategic insights support investment prioritization, geographic expansion planning, partnership development, and product portfolio optimization. The report further examines emerging opportunities in connected screening platforms, surveillance integration, and next-generation tuberculosis detection ecosystems, enabling informed business and operational decision-making.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 180.0 Million |

| Market Revenue (2033) | USD 291.3 Million |

| CAGR (2026–2033) | 6.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Sanofi Pasteur; Par Sterile Products; AJ Vaccines; Japan BCG Laboratory; Serum Institute of India; Statens Serum Institut; Bio Farma; China National Biotec Group; GreenSignal Bio Pharma; Zydus Lifesciences; Biological E; Bharat Biotech; Indian Immunologicals; Bionet Asia |

| Customization & Pricing | Available on Request (10% Customization Free) |