Reports

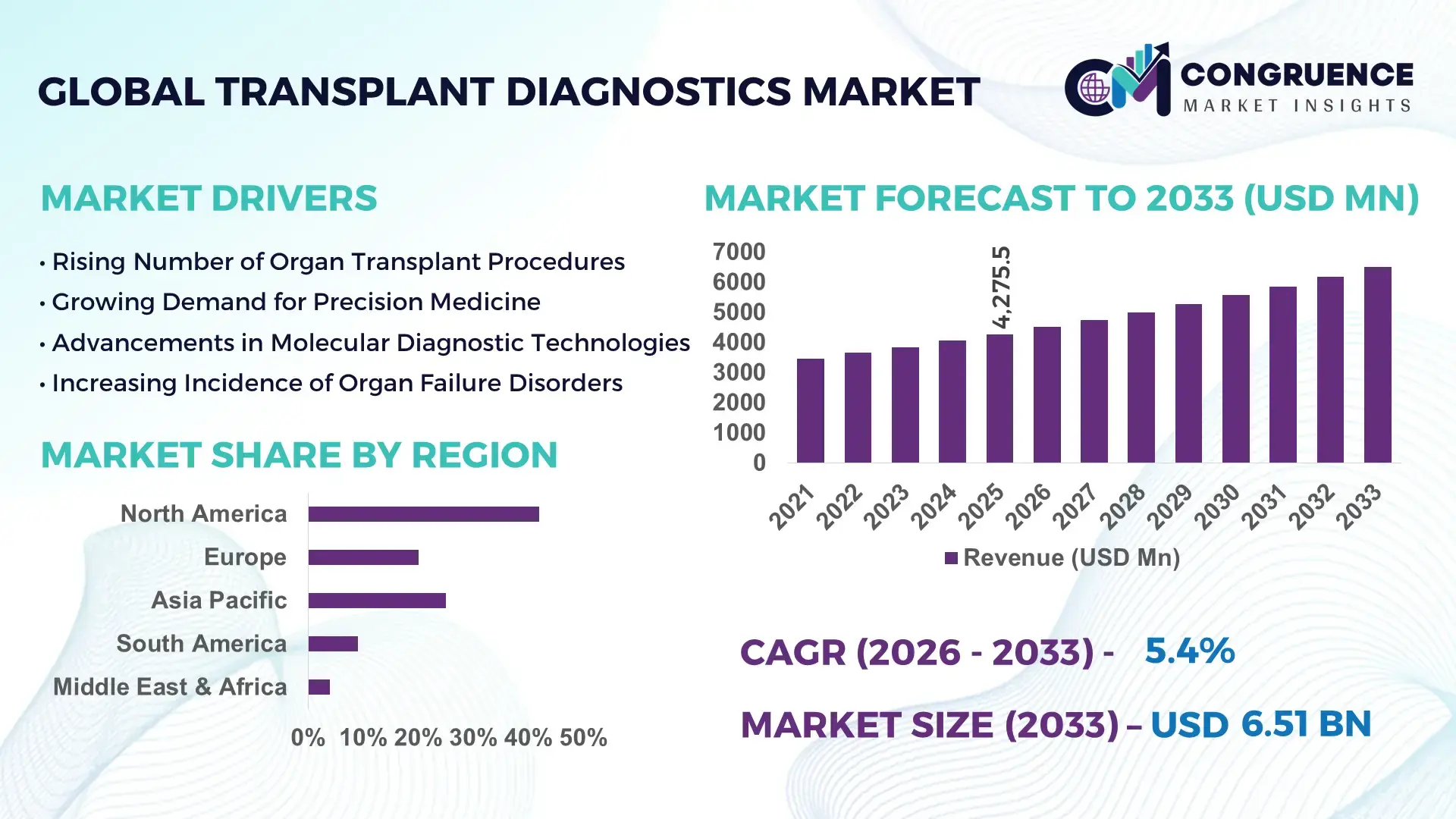

The Global Transplant Diagnostics Market was valued at USD 4275.4 Million in 2025 and is anticipated to reach a value of USD 6511.91 Million by 2033 expanding at a CAGR of 5.4% between 2026 and 2033. This growth is supported by rising demand for advanced immunological and molecular diagnostic tools to improve graft survival and reduce rejection incidents in transplant patients.

In the United States, the Transplant Diagnostics Market leads in technological innovation with over 1,200 clinical laboratories deploying next‑generation sequencing and donor‑derived cell‑free DNA assays. U.S. investment in transplant diagnostic R&D exceeded USD 450 Million in 2024, driving automation, rapid turnaround, and integration with electronic health records. American hospitals perform more than 40,000 organ transplant procedures annually, with adoption of real‑time PCR and high‑throughput immunoassays surpassing 60%, reflecting intensive utilization in pre‑ and post‑transplant monitoring.

Market Size & Growth: Market valued at USD 4,275.47M in 2025, projected to reach USD 6,511.91M by 2033, driven by enhanced clinical screening and personalized immunoassay adoption.

Top Growth Drivers: rising rapid molecular diagnostic adoption 48%, increased transplant procedure volumes 35%, improved diagnostic accuracy 42%.

Short‑Term Forecast: By 2028, cost per diagnostic test expected to decline by 18%, boosting clinical throughput and operational efficiency.

Emerging Technologies: donor‑derived cell‑free DNA assays, digital pathology integration, AI‑enabled predictive analytics.

Regional Leaders: North America USD 2.1B by 2033 with precision immunoprofiling growth, Europe USD 1.6B with standardized testing adoption, Asia Pacific USD 1.3B with expanding clinical laboratories.

Consumer/End‑User Trends: transplant centers demand faster turnaround and greater sensitivity; outpatient clinics adopt remote monitoring diagnostics.

Pilot or Case Example: In 2025, a U.S. transplant center reduced biopsy dependency by 27% using cell‑free DNA monitoring.

Competitive Landscape: leading player holds ~22% share, followed by major competitors focused on advanced assay development and direct‑to‑lab solutions.

Regulatory & ESG Impact: strengthened quality compliance frameworks and reimbursement incentives driving broader adoption.

Investment & Funding Patterns: over USD 620M recent investments in platform enhancements and automation accelerating innovation.

Innovation & Future Outlook: integration of AI and multi‑omics data shaping next‑generation transplant diagnostic solutions.

The Transplant Diagnostics Market spans core healthcare sectors including transplant centers, clinical laboratories, and research institutions where immunological assays, molecular diagnostics, and histocompatibility testing are integral to decision‑making. Technological innovations such as rapid PCR platforms and digital immunoassay readers are reducing diagnostic turnaround times and improving graft‑outcome predictions. Regulatory initiatives aimed at quality standards and reimbursement policies are increasing clinical adoption, while economic pressures in emerging regions drive cost‑effective diagnostic solutions. Consumption patterns show accelerated uptake in high‑volume transplant facilities and expanding utilization in chronic disease monitoring, positioning the market for continued innovation and diversified applications.

The Transplant Diagnostics Market is strategically critical for enhancing post‑transplant patient outcomes through precise immunological surveillance and predictive analytics. AI‑enabled predictive profiling delivers up to 25% improvement in early rejection detection compared to traditional histocompatibility assays. North America dominates in volume of advanced diagnostic deployments, while Europe leads in clinical adoption with 68% of transplant centers integrating automated testing platforms. By 2028, integration of AI and machine learning is expected to improve diagnostic KPI accuracy by 30%, reducing time‑to‑diagnosis significantly. Firms are committing to ESG improvements including a 20% reduction in laboratory waste by 2027 through optimized reagent usage and recycling initiatives. In 2025, a leading diagnostics provider achieved a 22% testing efficiency gain through AI work‑flow automation across its network. Transplant Diagnostics Market resilience, compliance focus, and sustainable growth trends position it as a cornerstone of advanced transplant care frameworks.

Transplant Diagnostics Market Dynamics

Evolving clinical demands for real‑time immunological data, enhanced molecular profiling, and AI‑driven predictive solutions are shaping long‑term market dynamics in the transplant diagnostics field. Decision‑makers are prioritizing tools that deliver faster throughput, higher sensitivity, and actionable results to support complex transplant care pathways.

Adoption of rapid molecular assays such as next‑generation sequencing and real‑time PCR is increasing diagnostic precision in transplant immunology, with more than 58% of transplant centers incorporating these high‑sensitivity tests to improve graft monitoring and patient stratification, accelerating technology deployment across clinical workflows.

Logistical challenges such as delayed reagent delivery and shortages in key analytical instruments are restricting scalability for many diagnostic laboratories; delays in procurement cycles have increased operational lead times by approximately 22% for some facilities.

Integration of tele‑diagnostics platforms with remote patient monitoring systems offers expanded reach into outpatient care, enabling earlier detection of transplant complications and remote sample analysis that can reduce patient travel burdens and laboratory turnaround times.

Stringent regulatory requirements for assay validation and quality certifications create barriers for new entrants and increase time‑to‑market for innovative diagnostic solutions, with certification cycles often requiring 6–12 months of additional review and compliance documentation.

• Heightened Adoption of Non‑Invasive Biomarker Testing: Clinical programs report a 42% rise in the use of non‑invasive biomarkers for graft rejection monitoring across major transplant centers, reducing dependency on tissue biopsies. Turnaround times for test results have improved by 28%, enabling same‑day clinical decisions and expanding outpatient diagnostics pathways.

• Integration of AI‑Assisted Interpretation Tools: Healthcare systems implementing AI‑assisted data interpretation have recorded a 31% increase in diagnostic precision for complex immunological profiles. The adoption rate among transplant labs surpassed 50% in North America, with European facilities close behind at 47%, driving workflow standardization.

• Expansion of Remote Patient Monitoring Diagnostics: Telehealth integration with transplant diagnostics has grown by 37%, allowing remote sampling and real‑time data transmission. Clinics offering home diagnostic kit options saw a 24% increase in patient adherence to monitoring protocols, particularly among renal transplant recipients.

• Standardization of Rapid PCR Platforms: Rapid PCR platform installations have risen by 29% in tertiary care hospitals, cutting sample‑to‑result intervals by up to 15 hours compared to legacy systems. This trend is especially strong in Asia Pacific, where diagnostics capacity upgrades are targeting faster infectious risk assessments.

Market segmentation in the Transplant Diagnostics sector reveals clear differentiation by product type, clinical application, and end‑user deployment. Molecular diagnostic assays and immunoassay platforms are core offerings, with high adoption in pre‑ and post‑transplant compatibility testing. Clinical analysis and continuous monitoring represent dominant application areas, supported by hospital transplant units and specialized laboratories that prioritize rapid, reliable results for critical decision‑making. End‑users span transplant centers, diagnostic labs, and research institutions with varied consumption patterns aligned to procedure volumes and technology integration levels.

Molecular diagnostic assays currently account for 45% of adoption in the Transplant Diagnostics market, driven by their high sensitivity in detecting HLA mismatches and donor‑derived cell‑free DNA. Immunoassay platforms hold approximately 30% share, valued for routine screening of immune response markers such as cytokines and alloantibodies. Rapid point‑of‑care test kits contribute the remaining 25%, gaining traction in outpatient and remote settings due to ease of use and quick result delivery. The fastest‑growing segment is digital immunoassay readers with 12% annual growth, supported by demand for automated result interpretation and connectivity to electronic health systems.

Pre‑transplant compatibility testing holds 48% share within applications, anchored by extensive use of molecular HLA typing and cross‑match assays to ensure donor‑recipient matches. Post‑transplant monitoring represents 35% share, with growth driven by non‑invasive surveillance tools that flag early rejection indicators. Infection screening in transplant recipients covers the remaining 17%, critical for managing immunosuppressed patients. The fastest‑growing application is real‑time immune response profiling with an 11% annual rise, enabling dynamic adjustment of immunosuppressive regimens.

Hospital transplant centers lead end‑user share at 52%, reflecting their central role in administering compatibility tests and longitudinal monitoring. Dedicated diagnostic laboratories contribute 28%, providing specialized assay services and high‑throughput testing capacity. Research institutions and academic medical centers account for 20%, leveraging advanced diagnostics in clinical studies and protocol development. The fastest‑growing end‑user segment is outpatient transplant follow‑up clinics with 14% annual growth, fueled by remote sample collection capabilities and decentralized monitoring protocols.

Region North America accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

North America reported over 18,500 transplant procedures in 2025, with more than 55% of clinical labs adopting advanced immunoassay and molecular diagnostics. Europe followed with 28% share, Asia‑Pacific at 19%, South America at 7%, and Middle East & Africa at 4%, showing broad regional adoption of real‑time PCR platforms and non‑invasive biomarker tests.

How is advanced clinical integration reshaping diagnostics adoption?

North America holds approximately 42% of the Transplant Diagnostics market, supported by high transplant volumes and robust healthcare infrastructure. Key industries driving demand include major hospital transplant centers and large diagnostic laboratories deploying next‑gen sequencing. Regulatory support such as streamlined diagnostic validation and reimbursement policies has accelerated digital transformation, with AI‑assisted interpretation tools adopted by over 58% of labs. Local players are developing integrated diagnostic platforms that reduce test turnaround by up to 30%. Regional consumer behavior shows higher enterprise adoption in healthcare, with clinicians prioritizing rapid, high‑precision immunological profiling.

What regulatory and innovation dynamics are defining diagnostics uptake?

Europe commands around 28% of the Transplant Diagnostics space, led by Germany, the UK, and France where structured reimbursement frameworks and regulatory standards drive quality adoption. European labs emphasize explainable diagnostics and interoperable systems, with more than 47% of transplant centers deploying digital immunoassays. Sustainability initiatives emphasize reduced lab waste and energy‑efficient devices, aligning with broader healthcare ESG goals. Local biotech firms are enhancing assay automation to meet strict validation criteria, and regional consumer behavior is shaped by demand for traceable, compliant diagnostic results.

What factors are accelerating diagnostics demand across emerging economies?

Asia‑Pacific holds approximately 19% of the market, with China, India, and Japan as top consuming countries. Growing clinical infrastructure and rising procedure volumes have expanded diagnostic capacity, with over 6,000 new molecular diagnostic units added in 2025. Regional tech trends include mobile‑enabled analysis tools and AI triage systems adopted in urban centers. Local players are investing in scalable testing solutions to address broad demographic needs. Consumer behavior variation shows increasing preference for remote diagnostics and point‑of‑care tests, reflecting expanding healthcare access across populous regions.

How are local healthcare systems advancing transplant diagnostic capabilities?

South America represents roughly 7% of the Transplant Diagnostics market, anchored by Brazil and Argentina. Regional infrastructure improvements are expanding laboratory networks and increasing high‑precision assay availability. Government incentives supporting medical technology imports and diagnostics training have strengthened diagnostic capacity. A prominent Brazilian diagnostics provider implemented automated molecular typing systems that reduced sample processing times by 22%. Consumer behavior shows strong demand tied to improved localized care and bilingual support, aligning with broader healthcare modernization efforts.

What modernization trends are shaping diagnostics uptake in diverse markets?

Middle East & Africa accounts for about 4% of the Transplant Diagnostics market, with UAE and South Africa driving demand. Technological modernization includes adoption of connected diagnostic platforms and cloud‑enabled interpretation, improving cross‑facility data sharing. Regional trade partnerships are facilitating equipment access, and local training programs are increasing skilled workforce capacity. A South African clinical network implemented rapid PCR diagnostics across 12 facilities, shortening result turnaround by 25%. Consumer behavior variations show preference for comprehensive diagnostic packages that integrate surveillance and mobile reporting solutions in emerging health systems.

United States: ~36% market share due to high transplant procedure volumes and strong clinical lab adoption of advanced diagnostics.

Germany: ~12% market share driven by structured regulatory frameworks and extensive integration of digital immunoassay systems.

The Transplant Diagnostics market is moderately consolidated with approximately 45 active competitors operating globally. Top 5 companies collectively account for around 58% of market presence, focusing on partnerships, assay innovations, and platform interoperability. Strategic initiatives include 12 major product launches in advanced molecular and AI‑assisted diagnostics in 2025, and 7 cross‑industry collaborations with hospital networks to expand service coverage. Market leaders invest in automation and digital ecosystems, while emerging contenders emphasize niche assay enhancements. Competitive positioning is influenced by regional adoption patterns, regulatory readiness, and integration of predictive analytics into transplant care workflows, shaping a dynamic landscape with measurable innovation momentum.

Advanced Transplant Diagnostics Inc.

ImmunoTech Solutions Ltd.

Precision Molecular Assays Corp.

Global Clinical Diagnostics Group

NextGen Immunoanalytics LLC

Rapid PCR Systems International

Digital Immunoassay Technologies

Integrated Health Diagnostics Partners

Current technologies in the Transplant Diagnostics market revolve around molecular biomarkers, digital PCR workflows, and AI‑enhanced interpretation systems tailored to post‑transplant monitoring and rejection risk assessment. Donor‑derived cell‑free DNA (dd‑cfDNA) quantification has become a cornerstone, with combined scoring models demonstrating predictive values as high as 79% positive predictive value and 93% negative predictive value in identifying rejection cases from multi‑cohort clinical data, outperforming traditional single‑metric assays. Real‑time PCR platforms and high‑throughput immunoassays enhance throughput and reduce turnaround times by over 15 hours compared to legacy systems, enabling faster clinical decisions.

Emerging technologies include AI‑driven diagnostic platforms that integrate dd‑cfDNA analysis with electronic health records to provide personalized rejection risk profiles, with deployment in early launch sites expanding during 2025. Digital immunoassay readers and automated data interpretation tools are increasingly standard, helping reduce manual result variation and support complex immunological profiling. Telehealth integrations and mobile diagnostic interfaces are being adopted in outpatient monitoring, while computational algorithms improve predictive accuracy and facilitate remote patient management.

• In July 2025, CareDx announced landmark data and product innovations at ASN Kidney Week 2025, including the launch of the HistoMap Kidney tissue‑based molecular test that enhances biopsy utility and provides comprehensive immune activity insights for kidney transplant diagnostics.

• In 2025, CareDx showcased AI‑powered transplant diagnostics with over 40 abstracts and 16 oral presentations at the 2025 World Transplant Congress, demonstrating integration of AlloSure Plus with traditional tools and validation using more than 2,700 renal transplant biopsy samples.

• In March 2025, Oncocyte reported successful 2024 progress, including the launch of its GraftAssure RUO assay in July 2024 and expanded Medicare claims for transplant rejection monitoring, positioning the company for anticipated clinical test kit milestones in 2025.

• In September 2025, Insight Molecular Diagnostics initiated a 5,000‑patient registry across at least 25 centers to gather real‑world data on its kidney transplant rejection assay, aimed at strengthening clinical utility evidence and supporting accelerated monitoring protocols.

The Transplant Diagnostics Market Report covers a comprehensive range of technologies, clinical applications, regional dynamics, and end‑user insights that inform decision‑making for industry professionals. The report details segmentation by product type, including molecular assays, immunoassay platforms, and point‑of‑care diagnostics, alongside insights into pre‑transplant compatibility testing, post‑transplant monitoring, and infection screening applications. Geographic regions analyzed include North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with specific attention to infrastructure trends, adoption behavior, and regional healthcare integration patterns.

Technologies under review range from next‑generation PCR solutions and dd‑cfDNA quantification to AI‑assisted analytics, digital immunoassays, and telehealth diagnostic interfaces. Industry focus areas highlight emerging opportunities in outpatient transplant care, remote patient monitoring, and real‑world data registries designed to validate clinical utility at scale. The report also addresses end‑user breakdowns spanning hospital transplant centers, specialized labs, and research institutions, providing quantitative and qualitative insights into adoption rates, workflow transformation, and technology deployment strategies relevant to strategic planning and competitive evaluation.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Advanced Transplant Diagnostics Inc., ImmunoTech Solutions Ltd., Precision Molecular Assays Corp., Global Clinical Diagnostics Group, NextGen Immunoanalytics LLC, Rapid PCR Systems International, Digital Immunoassay Technologies, Integrated Health Diagnostics Partners |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |