Reports

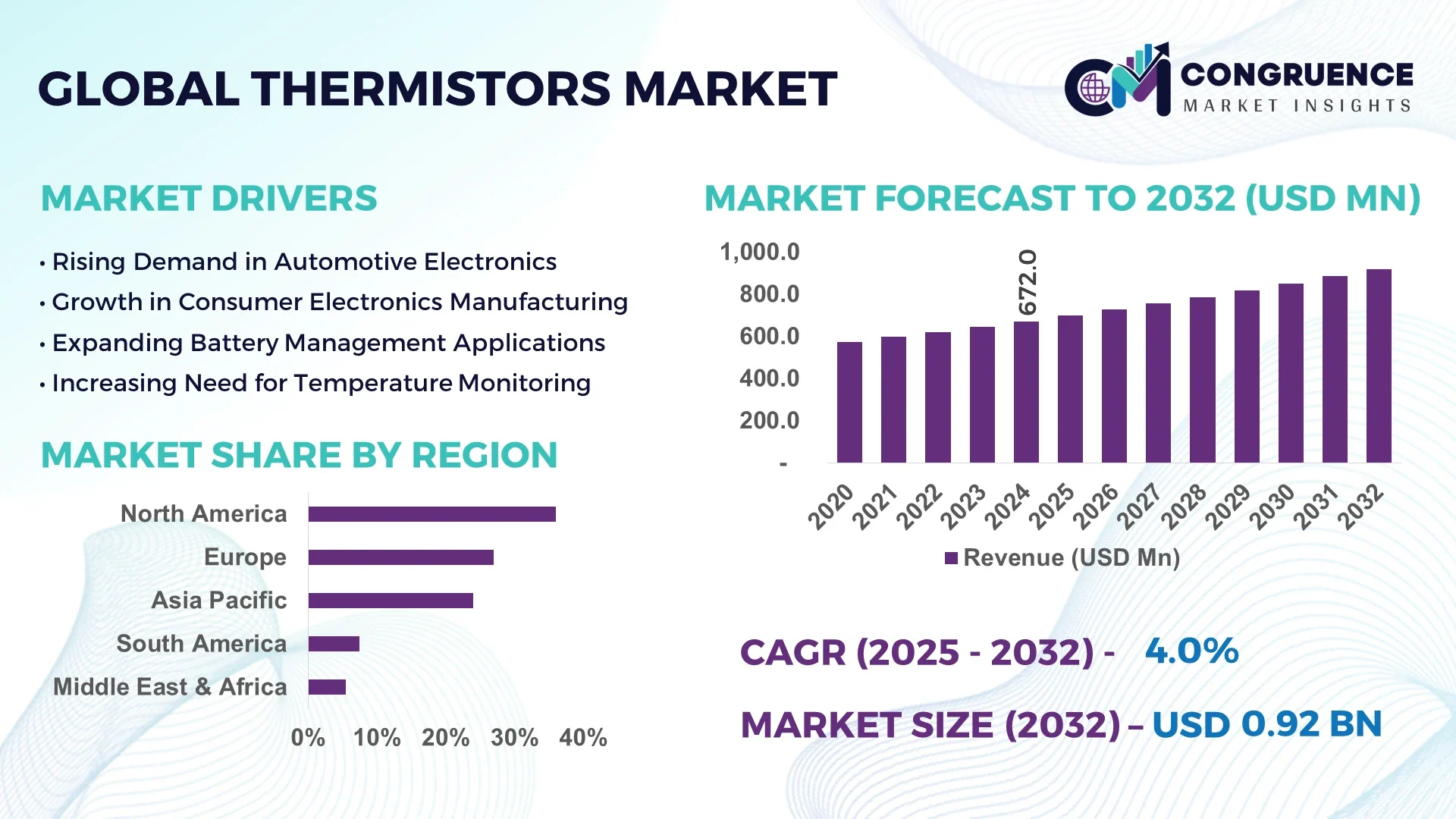

The Global Thermistors Market was valued at USD 672 Million in 2024 and is anticipated to reach a value of USD 919.67 Million by 2032 expanding at a CAGR of 4.0% between 2025 and 2032.

The United States holds the dominant position in the thermistors market with extensive deployment across automotive, consumer electronics, and industrial automation sectors. The nation’s robust semiconductor manufacturing infrastructure supports continued demand for thermistors.

The thermistors market is experiencing strong growth due to the rising adoption of temperature sensing technologies in modern electronic devices. Thermistors, particularly Negative Temperature Coefficient (NTC) types, are widely used in battery management systems, HVAC systems, and smart home appliances. Growing applications in electric vehicles (EVs) and medical devices are boosting the demand for highly accurate thermal sensors. In 2024, over 40% of thermistors were used in automotive applications alone, driven by their critical role in battery protection and climate control. Additionally, the increasing demand for miniaturized and surface-mount thermistors is pushing manufacturers to invest in R&D and automation technologies. Asia-Pacific remains a key production hub, with countries like China and South Korea expanding their thermistor manufacturing capabilities. Global supply chains are focusing on maintaining high sensitivity and reliability in thermistor production for diverse end-use applications including aerospace, energy storage, and IoT systems. The industry is evolving with growing focus on flexible and printed thermistors for next-gen wearables and medical monitoring equipment.

Artificial Intelligence is significantly transforming the thermistors market by enhancing design optimization, predictive maintenance, and real-time performance analytics. AI-driven modeling tools are enabling manufacturers to simulate thermistor behavior under diverse environmental conditions, improving thermal sensitivity and response time. This is crucial for industries such as electric vehicles and industrial automation where accurate temperature control is critical. AI algorithms are also being integrated into advanced manufacturing processes to reduce defects, ensure uniform resistance values, and enhance long-term stability of thermistors.

The integration of AI with smart sensors is paving the way for thermistors to play a central role in intelligent systems. AI-powered data analytics from thermistor-equipped devices are being used in HVAC, medical diagnostics, and environmental monitoring systems to optimize energy usage and detect anomalies proactively. In automotive applications, AI systems analyze thermistor inputs for managing battery temperature, engine heat, and in-cabin climate efficiently, thus improving safety and energy efficiency. AI is further being used for supply chain optimization, reducing lead times for thermistor orders and predicting component demand with higher accuracy. With rising demand for automation, AI’s role in thermistor testing, inspection, and quality control is growing rapidly, resulting in cost savings and product reliability enhancements. This transformation is expected to continue with deep learning and edge computing integration.

“In January 2024, TDK Corporation introduced an AI-assisted thermistor quality inspection system at its Nagaoka Techno Factory in Japan. The system uses deep learning algorithms to detect microscopic structural inconsistencies in thermistors during production, improving detection accuracy by over 20% compared to traditional visual methods.”

The thermistors market is influenced by a variety of dynamic factors, ranging from technological advancements to shifts in global economic trends. As industries continue to push the boundaries of automation, the demand for accurate and reliable temperature sensing solutions is increasing. Thermistors, known for their high precision and stability in temperature measurement, are being integrated into numerous applications across automotive, healthcare, energy, and consumer electronics sectors. The growing need for energy-efficient solutions, particularly in electric vehicles and renewable energy applications, is driving innovation in thermistor technology. Additionally, regulations promoting the use of environmentally friendly technologies are encouraging companies to adopt sustainable production practices. However, challenges such as the complexity of manufacturing high-precision thermistors at scale, along with global supply chain disruptions, continue to pose hurdles for market players.

The rise in temperature-sensitive electronic devices is fueling the growth of the thermistors market. With the expanding use of electronic components in consumer goods, healthcare equipment, and industrial systems, thermistors are becoming essential in ensuring reliable temperature control. In 2024, nearly 35% of global thermistor production was driven by the consumer electronics segment, primarily smartphones, laptops, and wearables, where precise thermal management is crucial. Additionally, the automotive sector is rapidly adopting thermistors for efficient battery management in electric vehicles (EVs), where overheating risks are mitigated by temperature monitoring systems. The rise of automation and IoT systems in homes and industries is further driving the adoption of thermistors in smart devices, HVAC systems, and robotics, contributing significantly to market expansion.

Manufacturing advanced thermistors, especially those with high precision and reliability, involves significant costs. The materials used, such as high-quality metal oxide semiconductors, and the precision engineering required to produce thermistors with exact resistance properties add to production expenses. As the demand for miniaturized and highly sensitive thermistors grows, the complexity of manufacturing these components increases, leading to higher production costs. For instance, companies that focus on developing thermistors for aerospace and medical devices face stricter quality control measures and certification requirements, which add to the overall cost. These high manufacturing costs pose challenges, especially for small to medium-sized enterprises looking to scale production while maintaining competitive pricing.

The rapidly expanding electric vehicle (EV) market presents a significant growth opportunity for the thermistors market. Thermistors play a crucial role in monitoring battery temperature, preventing overheating, and ensuring the safety and efficiency of EV batteries. The global shift towards sustainable transportation is driving demand for more advanced thermal management solutions, where thermistors are integral. In 2024, thermistors accounted for nearly 20% of the total sensors used in electric vehicle temperature management systems. As governments and automakers increasingly invest in the development and production of electric vehicles, thermistor suppliers stand to benefit from the growing need for reliable and high-performance temperature sensors in EVs. Additionally, thermistors are used in the thermal management of electric charging stations, making them essential for the overall growth of the electric vehicle infrastructure.

Supply chain disruptions and material shortages have been significant challenges for the thermistors market. The COVID-19 pandemic and subsequent global supply chain issues have resulted in delays and price hikes for key raw materials such as metals and ceramics used in thermistor production. These disruptions have led to higher production lead times and an imbalance between supply and demand. Moreover, as thermistor manufacturers expand into more specialized and niche markets, such as medical and aerospace, the requirement for high-quality, rare materials adds to supply chain complexities. Companies must also navigate geopolitical tensions and tariffs that affect material costs and availability, which can impede production schedules and ultimately impact profitability in the thermistors market.

• Rise in Electric Vehicles (EVs): The electric vehicle (EV) industry has significantly influenced the thermistors market. As EVs become more prevalent, the need for accurate temperature sensing for battery management systems grows. Thermistors are critical in monitoring battery temperatures to ensure safety and longevity. In 2024, approximately 25% of global thermistor demand was attributed to the automotive sector, with a particular focus on electric vehicles. This trend is expected to strengthen as governments and manufacturers continue to push for cleaner, greener vehicles.

• Growth in Renewable Energy Applications: The rise in renewable energy installations, such as solar and wind, is increasing the need for thermistors to monitor temperatures in power conversion systems, inverters, and other electrical equipment. Thermistors help ensure efficient operations and prevent overheating in sensitive electronics. In regions like North America and Europe, where renewable energy installations are expanding rapidly, thermistors are becoming more integrated into the energy management systems of solar and wind farms.

• Advancements in Wearable Electronics: The growing market for wearable electronics is fueling demand for compact and highly sensitive thermistors. Devices like fitness trackers, smartwatches, and health-monitoring tools require precise temperature measurements to ensure optimal performance. With the market for wearables expected to see rapid growth, the demand for miniaturized thermistors is also increasing. In 2024, the wearable electronics segment accounted for nearly 15% of the global thermistor market.

• Integration in IoT Devices: The Internet of Things (IoT) has seen exponential growth in recent years, driving the need for thermistors in a wide range of applications. Thermistors are commonly used in IoT-enabled temperature sensors that provide real-time monitoring for smart homes, industrial automation, and agriculture. As more devices connect to the internet and require precise temperature regulation, thermistors are becoming more integrated into everyday products. This trend is particularly strong in Asia-Pacific, where the adoption of IoT technology is rapidly expanding.

The global thermistors market is categorized by type, application, and end-user insights. The market is divided into different thermistor types, including Negative Temperature Coefficient (NTC) thermistors, Positive Temperature Coefficient (PTC) thermistors, and varistor thermistors. Thermistors are used across various applications such as automotive systems, consumer electronics, medical devices, and industrial automation, with automotive and consumer electronics being the leading sectors. The end-users of thermistors include industries such as automotive, healthcare, electronics, and energy, with automotive and electronics showing the highest demand.

Thermistors are primarily classified into three categories: Negative Temperature Coefficient (NTC) thermistors, Positive Temperature Coefficient (PTC) thermistors, and varistor thermistors. NTC thermistors are the most commonly used, as their resistance decreases as the temperature rises, making them ideal for applications that require accurate temperature sensing. NTC thermistors dominate the market, accounting for a substantial portion of global thermistor usage. Their widespread applications, particularly in automotive and consumer electronics, contribute to their market leadership. PTC thermistors, which have a resistance that increases with temperature, are commonly used in overcurrent protection and self-regulating heating applications. Although PTC thermistors hold a smaller share, they are gaining popularity, particularly in the automotive and industrial sectors, due to their ability to function as resettable fuses. Varistor thermistors are used mainly in surge protection devices, but their market share is smaller compared to NTC and PTC thermistors. Despite their limited use, they are essential for protecting sensitive electronics from voltage spikes. NTC thermistors remain the fastest-growing segment, particularly as they find applications in energy-efficient technologies and electric vehicle systems, where high precision and reliability are crucial.

The thermistor market is driven by various applications across multiple industries, including automotive, consumer electronics, healthcare, energy, and industrial automation. The automotive industry is the leading application sector, with thermistors being used in battery management systems, engine temperature sensors, and climate control systems in vehicles. The increasing adoption of electric and hybrid vehicles has significantly boosted demand for thermistors in automotive applications, with this segment accounting for the largest share of the thermistor market. In consumer electronics, thermistors are used in devices like smartphones, wearables, and smart home products, where they help in regulating temperatures to ensure safety and performance. The growing demand for smart electronics and wearable devices is contributing to the expansion of thermistor use in this sector. Healthcare applications of thermistors include temperature monitoring in medical devices, such as thermometers, infusion pumps, and respiratory equipment. The healthcare sector is experiencing growth due to the increasing demand for wearable health-monitoring devices and advanced medical technologies. The industrial automation sector is another significant application area for thermistors, with their use in temperature sensing for equipment and machinery in manufacturing and processing industries. Among all these, the automotive sector leads in market share, while the consumer electronics and healthcare segments are witnessing the fastest growth.

Thermistors are utilized across various end-user industries, with the automotive, healthcare, electronics, and energy sectors being the most prominent. In the automotive sector, thermistors are in high demand, especially due to their use in electric vehicle battery management systems, engine sensors, and climate control systems. The automotive industry is the largest end-user of thermistors, accounting for the largest portion of the global market. This sector is expected to continue driving growth due to the increasing adoption of electric vehicles and the growing need for advanced thermal management systems. The healthcare industry is another significant end-user, as thermistors are essential for temperature sensing in medical devices. The demand for healthcare solutions, including wearable health-monitoring devices and remote patient monitoring systems, is driving growth in the thermistor market. In the electronics industry, thermistors are used in a wide range of applications, including smartphones, wearables, and home appliances. The increasing demand for these devices has led to a surge in thermistor usage. The energy sector, particularly in renewable energy applications such as solar and wind power, also contributes to the thermistor market. Thermistors are used in power management and battery systems to monitor temperature and ensure optimal performance. Among these sectors, automotive remains the largest end-user, while the healthcare sector is growing at the fastest rate due to innovations in medical technology and increasing consumer demand for health-monitoring solutions.

North America accounted for the largest market share at 36%in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2025 and 2032.

North America’s stronghold in the thermistors market is attributed to its advanced automotive, electronics, and healthcare sectors. The region also benefits from a well-established industrial base and high demand for temperature regulation solutions. On the other hand, Asia-Pacific’s rapid expansion is fueled by growing manufacturing activities, increasing adoption of electric vehicles, and the rising demand for consumer electronics and energy-efficient solutions.

Pioneering Innovation and Smart Solutions

The North American thermistors market continues to lead globally, driven by significant demand from the automotive and electronics industries. The increasing popularity of electric vehicles (EVs) in the region has further bolstered the demand for thermistors, particularly for battery management and temperature regulation. Automotive manufacturers in the United States and Canada are focusing on enhancing electric vehicle performance, which requires advanced thermal management systems that rely heavily on thermistors. In the electronics sector, the demand for precise temperature monitoring in devices such as smartphones, wearables, and home appliances is driving growth. As technological advancements in these areas continue to evolve, the need for high-performance thermistors is expected to persist, ensuring North America's continued dominance in the global market.

A Hub for Advanced Technology and Automotive Integration

Europe's thermistor market is characterized by a high demand for energy-efficient solutions and automotive applications. Countries like Germany and France are leading in the adoption of thermistors for electric vehicles, smart grid systems, and industrial automation. Europe is home to several leading automotive manufacturers that incorporate thermistors in their battery management systems, which is vital for ensuring optimal performance and safety in electric vehicles. Additionally, with the European Union's growing emphasis on sustainability, there is an increasing demand for thermistors in renewable energy systems for temperature monitoring. The automotive and industrial automation sectors are expected to remain the key contributors to market growth in Europe, with a focus on reducing emissions and improving energy efficiency.

Rapid Growth Fueled by Industrial Expansion and IoT Adoption

Asia-Pacific is witnessing rapid growth in the thermistors market, driven primarily by the expansion of the manufacturing sector and the increasing adoption of consumer electronics. Countries like China, Japan, and South Korea are at the forefront of thermistor usage, especially in the automotive, electronics, and industrial sectors. In China, the automotive industry is transitioning towards electric vehicles, leading to higher demand for thermistors for temperature control and battery management systems. Japan’s technological advancements in electronics also contribute significantly to the market, with thermistors being used extensively in temperature-sensitive devices. The booming electronics manufacturing industry in India and Southeast Asia further drives the demand for thermistors, particularly in temperature sensors and protection systems.

Emerging Markets and Increased Industrialization

South America is experiencing steady growth in the thermistors market, primarily due to the increasing demand for consumer electronics and automotive applications. Brazil is the largest market in the region, with a focus on improving automotive safety and performance through advanced temperature management solutions. The growing electronics industry in countries like Argentina and Chile is also contributing to the demand for thermistors, particularly in smart devices and home appliances. As the region continues to industrialize, the need for thermistors in industrial automation and energy-efficient systems is anticipated to rise, presenting opportunities for market expansion.

Expanding Infrastructure and Rising Tech Demand

The Middle East and Africa are witnessing a steady rise in the thermistors market, largely driven by growing industrialization and technological advancements. The demand for thermistors is particularly strong in countries like the United Arab Emirates and Saudi Arabia, where the automotive and oil and gas industries are flourishing. In the automotive sector, thermistors are crucial for temperature regulation in vehicles, while the energy sector requires thermistors for monitoring and control in power generation systems. The increasing focus on sustainable energy solutions and the push for electric vehicles in the region are expected to contribute significantly to the market's growth. As industries across the region continue to modernize, thermistors will play a critical role in temperature sensing and protection applications.

United States: Holds the largest market share at 24%due to its strong automotive and electronics sectors.

Germany: Holds 18%market share, driven by its robust automotive industry and focus on electric vehicle adoption.

The thermistors market is highly competitive, with key players vying for market share through innovations and strategic partnerships. Companies are investing in new technologies to improve the precision and efficiency of thermistors, especially for applications in the automotive, electronics, and healthcare industries. The market is dominated by global players with a strong presence in various regions. Companies are increasingly focusing on expanding their production capabilities and improving product offerings to cater to the growing demand for advanced thermistors, especially in emerging markets. Strategic mergers and acquisitions are also playing a critical role in strengthening market positions. Furthermore, several players are establishing joint ventures and collaborations to enhance their technological capabilities and broaden their product portfolios. In terms of regional competition, North America and Europe are key hubs for technological advancements and manufacturing excellence, while Asia-Pacific has been witnessing significant growth due to the rising demand from automotive and industrial applications.

Murata Manufacturing Co., Ltd.

Amphenol Corporation

Panasonic Corporation

Vishay Intertechnology, Inc.

TE Connectivity Ltd.

Honeywell International Inc.

Semitec Corporation

Bourns, Inc.

TT Electronics Plc

The thermistors market has been significantly impacted by technological advancements aimed at enhancing performance, durability, and efficiency in various applications. One major innovation is the development of high-precision thermistorsthat can offer enhanced temperature sensitivity for critical applications in automotive, industrial, and healthcare sectors. These thermistors are designed to provide more accurate temperature measurements, ensuring that systems relying on temperature data, such as electric vehicle batteries or medical devices, operate within safe and optimal ranges.The integration of IoT capabilitiesinto thermistors is another technological trend driving growth. Thermistors embedded with IoT sensors allow for real-time monitoring of temperature data, enabling predictive maintenance and remote diagnostics, especially in industrial applications. This not only enhances system reliability but also minimizes downtime and maintenance costs.

Miniaturizationis also a key technological development in the thermistor market. With the growing demand for compact devices in wearable technology and medical monitoring, thermistors are being designed to occupy smaller spaces while maintaining high functionality. This miniaturization trend is particularly evident in the medical sector, where thermistors are used in wearable health devices that track body temperature. Additionally, advanced materialsare being utilized to enhance thermistor performance. New formulations, including ceramic-based thermistors, offer improved resistance to temperature extremes, vibration, and humidity, making them suitable for use in harsh environmental conditions such as industrial machinery or automotive systems. These innovations are helping manufacturers meet the increasing demand for more reliable, durable, and accurate temperature sensors across a wide range of applications.

• In December 2023, Vishay Intertechnology announced the launch of its new series of high-precision thermistors, designed for automotive applications. These thermistors are specifically engineered to support temperature measurement and control in electric vehicle (EV) battery systems, ensuring greater performance and longevity.

• In January 2024, Honeywellunveiled a line of smart thermistorsintegrated with IoT capabilities, enabling real-time monitoring of temperature in HVAC systems. This new technology aims to provide more energy-efficient solutions by allowing for predictive maintenance and reducing operational costs.

• In March 2024, Panasonicexpanded its thermistor offerings by introducing a new series of high-temperature-resistant thermistors. These thermistors are capable of withstanding temperatures up to 300°C, making them ideal for use in industrial equipment and heavy machinery applications that operate under extreme conditions.

• In June 2024, TDK Corporationannounced its partnership with leading automotive manufacturers to develop advanced thermistors for autonomous vehicles. These thermistors are designed to monitor critical components in electric drive systems, ensuring optimal temperature regulation and preventing overheating in the high-performance components of autonomous vehicles.

The thermistors market is expected to witness substantial growth driven by increasing demand across various industries, including automotive, consumer electronics, industrial automation, and healthcare. Thermistors, being temperature-sensitive resistors, play a critical role in applications where precise temperature measurement and control are essential. In automotive, the rise of electric vehicles (EVs) has boosted the demand for thermistors in battery management systems, helping optimize performance and enhance safety. In consumer electronics, thermistors are crucial for regulating temperature in devices like smartphones, laptops, and home appliances, ensuring longevity and energy efficiency.

In industrial applications, thermistors are used in manufacturing processes that require accurate temperature monitoring to ensure product quality and safety. Moreover, the healthcare sector has seen growing adoption of thermistors in medical devices for monitoring body temperature and environmental conditions in critical care units. As the adoption of IoT devices increases, the integration of thermistors into smart sensors and devices is further expanding, creating significant growth opportunities in the market.

The report also highlights the evolving technologies in thermistor production, such as advanced materials and manufacturing techniques, that are expected to enhance product efficiency and reliability. The geographical analysis within the report reveals regions like North America, Europe, and Asia-Pacific are key markets, with Asia-Pacific showing strong growth potential due to industrial expansion and technological advancements.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 672 Million |

|

Market Revenue in 2032 |

USD 919.67 Million |

|

CAGR (2025 - 2032) |

4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Murata Manufacturing Co., Ltd., Amphenol Corporation, Panasonic Corporation, Vishay Intertechnology, Inc., TE Connectivity Ltd., Honeywell International Inc., Semitec Corporation, Bourns, Inc., TT Electronics Plc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |