Reports

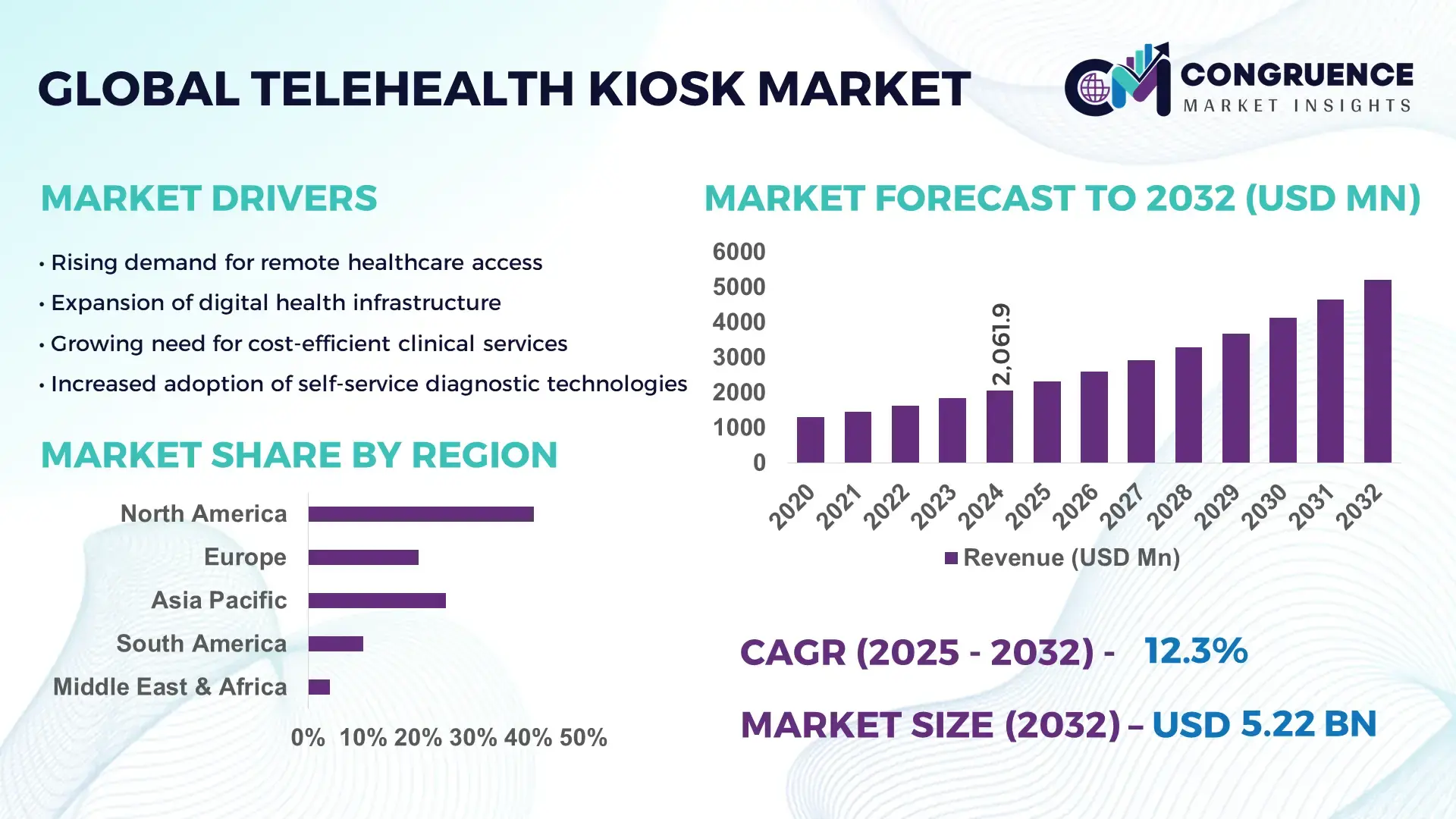

The Global Telehealth Kiosk Market was valued at USD 2061.94 Million in 2024 and is anticipated to reach a value of USD 5215.73 Million by 2032 expanding at a CAGR of 12.3% between 2025 and 2032. This growth is driven by rising demand for remote medical consultations and a push toward digital healthcare infrastructure globally.

North America remains the most influential region in this market: in the United States alone, over 8,200 kiosks had been deployed across 41 states by 2024, and around 72% of U.S. hospitals along with 55% of retail pharmacies have adopted kiosk‑based teleconsultations, reflecting deep penetration in both institutional and consumer‑facing healthcare settings.

Market Size & Growth: Current market value stands at USD 2061.94 million (2024), projected to rise to USD 5215.73 million by 2032, at a CAGR of 12.3%, fueled by increasing demand for remote consultation and digital health infrastructure.

Top Growth Drivers: remote consultation demand increase ~63%, chronic disease management growth ~54%, rise in telemedicine acceptance among aging populations ~49%.

Short-Term Forecast: By 2028, telehealth kiosks are expected to deliver cost reduction of ~28% for clinics and hospitals and achieve performance gain of ~35% in patient throughput.

Emerging Technologies: AI‑driven diagnostics and biometric sensor integration; high‑resolution camera and EHR integration; cloud‑based real-time health data analytics.

Regional Leaders: North America projected to reach USD ~1,800 M by 2032, Europe ~1,250 M (with strong preventive care adoption), Asia‑Pacific ~1,100 M (rapid rural deployment), Middle East & Africa ~450 M (growing demand in remote communities).

Consumer/End-User Trends: Hospitals and specialty clinics remain primary adopters; retail pharmacies increasingly deploy kiosks for teleconsultation and digital pharmacy services; growing adoption in community clinics and rural health centers.

Pilot or Case Example: In 2024, a U.S. national retail pharmacy chain deployed 1,000 teleconsultation kiosks — reducing average patient wait times by ~44% and improving prescription turnaround speed by ~31%.

Competitive Landscape: Market leader holds approximately 17% share; major competitors include five other major providers, collectively controlling about 60–65% of global deployments.

Regulatory & ESG Impact: Expanding telehealth reimbursement policies and supportive government initiatives in multiple countries; incentives for rural healthcare access and digital health inclusion encourage broader kiosk adoption.

Investment & Funding Patterns: Over USD 2.1 billion invested globally during 2022–2024 in hardware and software development for telehealth kiosks; rising venture‑capital interest and growing project‑finance models tied to public health programs.

Innovation & Future Outlook: Strong trend toward modular, multifunctional kiosks capable of multiple diagnostics; integration with 5G and cloud‑based systems; forward-looking projects focus on enabling remote diagnostics in underserved rural areas and integrating kiosks into national digital‑health platforms.

The telehealth kiosk market’s growth is supported by increasing demand from hospitals and community clinics, rising adoption by retail pharmacies, and expansion into non‑traditional settings such as corporate campuses and rural health centers. Recent innovations include kiosks with biometric sensors, AI‑powered diagnostic tools, real‑time data analytics, and digital pharmacy integration — enabling more comprehensive, efficient patient care. Regulatory support, government funding for digital‑health infrastructure, and rising healthcare spending in emerging economies further drive adoption. Regionally, North America leads due to advanced healthcare infrastructure; rapidly growing demand in Asia‑Pacific reflects efforts to expand rural and remote healthcare access. Emerging trends point to modular, multi‑service kiosks and deeper integration with national health networks, creating a forward-looking outlook that positions telehealth kiosks as central to accessible, cost‑effective global healthcare delivery.

The strategic relevance of the Telehealth Kiosk Market lies in its ability to transform traditional healthcare delivery into a more accessible, efficient, and scalable model — an imperative for modern health systems facing rising chronic disease burdens, increasing demand for remote care, and pressure to reduce costs. As a benchmark, AI‑powered diagnostic kiosks deliver up to 40% improvement in triage speed and patient throughput compared to older standard in‑person check‑in and manual initial assessment workflows. Regionally, North America dominates in volume, while Asia‑Pacific leads in adoption growth, with over 57% increase in deployment between 2020 and 2024 across rural and semi‑urban areas.

By 2027, integration of cloud‑based telemonitoring and real‑time analytics is expected to improve patient follow-up efficiency by 30% and reduce average consultation waiting time by 25%. Many firms are committing to ESG‑aligned goals such as reducing travel-related carbon emissions by enabling remote consultations — projecting a 15% reduction in patient transport footprint by 2028. In 2025, a public‑health pilot in a Southeast Asian country achieved 35% reduction in hospital readmission rates through deployment of AI‑enhanced kiosks integrated with remote monitoring.

These developments position the Telehealth Kiosk Market as a pillar of resilience, compliance, and sustainable growth — enabling health systems to scale access, optimize resources, and meet rising demand with operational efficiency and environmental responsibility.

Growing global prevalence of chronic conditions such as diabetes, hypertension, and cardiovascular diseases has accentuated demand for regular monitoring and follow-up care. Telehealth Kiosks enable patients to undergo vital-sign checks, basic diagnostics, and remote consultations without needing to visit hospitals — significantly reducing burden on clinical resources. In multiple deployments, introduction of kiosks led to a 30% decrease in waiting times and 28% increase in physician productivity, enabling healthcare facilities to serve more patients with existing staff. In underserved or rural regions, kiosks offer a scalable, cost‑effective way to deliver continuous care and chronic disease management — driving adoption among hospitals, clinics, and community health programs.

Implementation of Telehealth Kiosks often requires significant upfront investment — purchase of kiosk hardware, diagnostic modules, integration with health‑record systems, and reliable internet connectivity. For smaller clinics, community centers, or health providers in low-resource areas, these costs can be prohibitive. Additionally, many rural and underdeveloped regions lack stable broadband connectivity or IT infrastructure, undermining the functionality of kiosks. This digital divide results in lower adoption rates, especially among low‑income or remote populations, limiting market penetration where kiosks could offer high value. Maintenance costs, software licensing, and ongoing technical support further add to financial burden, making sustained deployment challenging for resource-constrained providers.

Emerging technologies — AI-driven symptom triage, remote monitoring sensors, cloud-based health data storage, and 5G connectivity — present a rich opportunity landscape for Telehealth Kiosks. AI-enabled kiosks can offer predictive diagnostics and personalized care recommendations, improving accuracy and patient engagement. Integration with cloud platforms and electronic health records enables seamless data exchange and long-term health tracking. As 5G networks expand in urban and rural regions, real‑time high-definition video consultations and rapid data transfer become feasible, enhancing patient experience. Governments in several developing markets are introducing incentives and funding programs for digital health infrastructure, especially to expand access in underserved regions — opening avenues for large-scale kiosk deployments backed by public initiatives.

Because Telehealth Kiosks handle sensitive patient health information — including medical history, diagnostics, and biometric data — data privacy and security are critical concerns. Compliance with regulations (e.g., HIPAA, GDPR or region‑specific patient privacy laws) demands robust encryption, secure data storage, and strict access controls, raising complexity and cost for providers and manufacturers. Variable regulatory frameworks across countries complicate global deployment strategies. Additionally, in many regions, end users — especially older adults or digitally un‑savvy populations — may resist adopting kiosk‑based care due to unfamiliarity or distrust of technology, reducing utilization. Healthcare providers might also be hesitant to integrate kiosk outputs into clinical workflows without validated reliability, further slowing adoption.

• Modular & Prefabricated Construction Is Gaining Ground: Modular and prefab methods are increasingly used to build Telehealth Kiosk facilities, with about 55% of new projects reporting cost savings when employing prefabricated components over traditional construction. Prefab modules — such as consultation booths, diagnostic compartments and utility pods — are manufactured off‑site using automated machinery, which reduces labour demand and speeds deployment significantly. In healthcare settings across Europe and North America, this modular approach has led to 30–50% faster delivery timelines and improved predictability, making rapid installation of kiosks more feasible for both urban clinics and rural outreach centers.

• Integration of Biometric & Smart Diagnostic Technology: A growing share of recently deployed kiosks — over 57% — include biometric sensors, vital‑sign measurement tools (e.g., ECG, oxygen saturation, glucose, blood pressure), and cloud‑connected telemetry for remote monitoring. Many kiosks now support real-time data transfer via secure connectivity to electronic health record systems and allow tele‑consultations or e‑prescriptions. This trend enables kiosks to function beyond mere check-in terminals, transforming them into full-featured remote diagnostic hubs capable of supporting preventive care, chronic disease monitoring, and telemedicine outreach in underserved areas.

• Expansion Beyond Hospitals: Retail, Community & Rural Deployment Surge: Between 2023 and 2025, over 20,000 new non‑hospital sites — including retail pharmacies, corporate wellness centers, community clinics, and rural health posts — adopted telehealth kiosks. This broadening of deployment channels reflects a shift in end‑user pattern: patients increasingly expect convenient, local access to healthcare services. The expansion into non-traditional venues has led to a 30% year-over-year rise in kiosk usage in regions prioritizing rural‑health outreach and community‑based care.

• Hygiene‑Optimized and Contactless Interfaces Fuel Adoption: In response to hygiene concerns and infection‑control standards, 51% of new telehealth kiosk installations in 2025 included touchless interfaces, antimicrobial surfaces, and air‑filtration modules. This trend has boosted patient confidence and uptake, particularly in high‑traffic public settings. The move toward contactless operations reduces cross‑contamination risk and aligns kiosk deployment with evolving public health requirements, making kiosks more acceptable and sustainable for large populations. These trends collectively signal that the Telehealth Kiosk Market is evolving rapidly — shifting from basic convenience terminals to integrated diagnostic and care-delivery platforms, expanding deployment across varied settings, and leveraging modular construction and hygiene innovations to support scalable, efficient and safe healthcare delivery.

The Telehealth Kiosk market can be segmented across product type, application area, and end‑user category — each reflecting distinct demand patterns and strategic deployment preferences. By product type, stakeholders differentiate between stationary floor‑standing kiosks, wall‑mounted units, mobile/portable kiosks, and modular prefabricated kiosks designed for rapid deployment. Under application, kiosks serve teleconsultation, remote diagnostics & screening, chronic disease monitoring, preventive health check‑ups, pharmacy or medication dispensing, and patient triage services. Regarding end‑users, segments include hospitals and clinics, retail pharmacies, community health centers (including rural clinics), corporate wellness facilities, and residential or remote‑community deployments. This segmentation enables decision‑makers to tailor deployment strategy according to use‑case demands, infrastructure constraints, and end‑user behavior, helping align product design, operational workflows, and market outreach with specific demand sources.

Among product types, stationary floor‑standing kiosks currently dominate, accounting for approximately 45% of global deployments. Their prevalence stems from suitability for full-featured telehealth services — they offer enough space for integrated diagnostic modules, biometric sensors, and comfortable patient interaction. Mobile or portable kiosks are the fastest-growing type, with a growth rate estimated at CAGR ~18%, driven by demand for flexible deployment in temporary clinics, rural outreach programs, corporate wellness drives, and pop-up health camps. Their portability enables rapid deployment without requiring permanent installation infrastructure. Wall‑mounted kiosks contribute roughly 20% of installations; they are preferred in urban clinics, pharmacies, or constrained spaces as cost-effective entry-level solutions. Modular prefabricated kiosks, though a smaller segment (~15%), are gaining traction in projects requiring quick build-out and standardized quality, especially in emerging markets.

In terms of application, teleconsultation services remain the leading use-case, representing roughly 50% of overall kiosk usage worldwide. This dominance reflects widespread demand for remote physician access, particularly in regions with limited clinical availability or high patient volumes. The fastest-growing application area is remote diagnostics & screening, expanding at an estimated CAGR ~20%, driven by growing adoption of biometric sensors and integration with electronic health records for preventive health, early detection, and chronic‑disease monitoring. Other applications — including chronic disease monitoring, preventive health check‑ups, pharmacy/medication dispensing, and patient triage services — together constitute the remaining 50% of usage. Among them, chronic disease monitoring is particularly significant in aging populations, while kiosks in pharmacies support tele‑prescription and delivery services.

Hospitals and clinics remain the leading end‑user segment, accounting for approximately 40% of telehealth kiosk adoption worldwide. They value kiosks for easing workloads, improving patient throughput, and offering remote follow-ups for discharged or chronic patients. The fastest-growing end-user segment is retail pharmacies and community pharmacies, with growth rate estimated at CAGR ~22%, as pharmacies increasingly integrate teleconsultation kiosks to offer prescription services, over-the-counter digital consultations, and post-consultation medicine delivery services. Other segments — including community health centers (especially in rural areas), corporate wellness centers, and residential or remote-community deployments — collectively make up around 38% of the market. Community health centers are particularly vital in emerging economies, offering access where traditional clinics are scarce.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 20% between 2025 and 2032.

North America remains dominant due to its mature healthcare infrastructure, widespread adoption of telehealth solutions, and strong regulatory support for digital health. In contrast, Asia‑Pacific’s rapid growth is fueled by expanding rural healthcare access, rising demand for remote diagnostics, and increasing investments in digital health. Europe and Middle East & Africa also maintain significant deployment numbers, while South America and other emerging regions are gradually scaling up installations. Statistical data indicate that as of 2024, roughly 28,000 telehealth kiosks operated globally, with Asia‑Pacific contributing around 24% of that base — reflecting strong regional uptake alongside continued growth across established markets.

Why is adoption highest in advanced healthcare ecosystems?

North America holds approximately 42% of the global telehealth kiosk base as of 2024. Demand is driven by hospitals, specialty clinics and retail pharmacies seeking to expand teleconsultation and remote patient monitoring capabilities. Regulatory changes — including supportive telehealth reimbursement policies and government‑backed grants have accelerated adoption, especially in rural and underserved communities. Technological innovations such as cloud‑based EMR integration, IoT-enabled vital‑sign sensors and real-time data analytics are common across deployments. A notable example: a large U.S. pharmacy chain recently deployed kiosks within its stores to enable on‑site teleconsultations and digital prescription services, reflecting converging retail and healthcare delivery trends. Consumer behavior in North America favors enterprise-level adoption: hospitals and large provider networks lead deployments, and patients show high acceptance for kiosk‑based consultations and remote monitoring.

How is regulatory compliance shaping kiosk adoption across European health systems?

In Europe, the telehealth kiosk market holds roughly 26–28% of global installations. Leading markets include Germany, the UK, France, and Nordic countries, with Germany and the UK at the forefront of integrating kiosks into hospital and clinic workflows. Regulatory frameworks emphasizing data privacy, patient safety, and interoperability have encouraged adoption of secure, compliant telehealth kiosk solutions. Emerging technologies such as AI‑driven diagnostics and multilingual interface support are being rapidly adopted to meet diverse patient needs. For example, some European providers now deploy kiosks with built‑in translation and secure patient‑data handling. Regional consumer behavior reflects a strong preference for explainable, privacy‑compliant telehealth solutions, prompting demand for interoperable, standards‑compliant kiosk systems that align with healthcare regulations and public‑health goals.

Why is Asia-Pacific becoming the fastest expanding region for kiosk deployments?

Asia‑Pacific registered around 24% of global telehealth kiosk installations as of 2024, with approximately 9,400 units operational across countries like China, India, and Japan. China leads with over 4,200 units, while India accounts for around 2,600 installations, many deployed in rural health centers to extend access where clinical infrastructure is sparse. Infrastructure expansion, improving telecommunications (mobile broadband, 5G rollouts), and rising healthcare investments are major enablers. Regional tech trends show high uptake of kiosks embedded with AI-based triage, cloud‑connected monitoring, and contactless interfaces. Consumer behavior in Asia-Pacific varies: urban clinics adopt kiosks for chronic disease monitoring and teleconsultation, while rural areas use portable or modular kiosk solutions to bridge healthcare access gaps effectively.

How are emerging healthcare markets leveraging kiosks to expand care access?

In South America notably Brazil and Argentina — deployment of telehealth kiosks is gradually growing, though overall regional market share remains modest relative to established regions. Infrastructure limitations and uneven connectivity present challenges, but growing healthcare demand and government interest in improving rural health access support incremental kiosk adoption. Some local healthcare networks are exploring kiosk deployments in community clinics and pharmacies to enable remote consultations and basic diagnostics. Regional consumer behavior shows rising acceptance for tele‑consultation services, especially in urban areas, indicating potential for gradual growth as infrastructure improves.

How is digital health modernization driving kiosk adoption in emerging regions?

Middle East & Africa hold a growing share of global telehealth kiosk deployments, with notable growth in countries such as UAE, Saudi Arabia, and South Africa. Regional demand is rising as governments pursue health‑digitization initiatives and public–private partnerships aim to expand remote diagnostics and teleconsultation services. Technological modernization including deployments of solar‑powered kiosks and integration of basic diagnostic tools helps overcome energy and infrastructure constraints in remote areas. Consumers in urban Middle‑East settings show increasing willingness to use telehealth kiosks in clinics, malls, and airports, while rural populations benefit from improved access to basic care through community-based kiosk deployments.

United States — ~38–42% share globally; dominance due to advanced healthcare infrastructure and strong end‑user demand for remote patient monitoring and teleconsultations.

China — ~15–18% share in Asia‑Pacific regional base (~4,200 units in 2024); leadership driven by large population, government support for rural digital‑health rollout, and manufacturing capacity for kiosk deployments.

The competitive environment in the Telehealth Kiosk market is moderately consolidated yet remains dynamically fragmented, with roughly 25–30 active major competitors globally and a long tail of smaller specialized firms. The top 5 companies collectively hold over 60% of global deployments, indicating a significant but not monopolistic concentration — leaving plenty of room for innovation, niche providers, and regional players. Major players focus on strengthening market positioning through strategic initiatives such as partnerships, product launches, and acquisitions. For instance, some firms have merged hardware‑software platforms to deliver integrated telehealth kiosk solutions targeting hospitals, pharmacies, and community clinics. Other competitors are launching next‑generation kiosks with advanced diagnostic modules, AI‑driven health assessments, and interoperable EHR integration — pushing innovation in both hardware engineering and software services.

Competition is increasingly shaped by technology-driven differentiation: firms introducing biometric sensor integration, IoT‑enabled vital-sign measurement, cloud connectivity, modular and portable kiosk designs, and real‑time teleconsultation capabilities are gaining market traction. Some vendors emphasize retail‑pharmacy and corporate wellness deployments to capture non-traditional end‑user segments, while others concentrate on hospital and rural‑health networks for volume. Strategic partnerships — for example between kiosk manufacturers and telemedicine providers or broadband/telecom operators — are enhancing delivery models, enabling wider reach into underserved or remote populations.

Because of the range of players — from large diversified health‑tech firms to niche kiosk manufacturers — and the varied end‑user settings (hospitals, pharmacies, community clinics, corporate wellness, rural health centers), the market remains fragmented. At the same time, the dominance of a few large firms provides stability and scale. Innovation trends — modular kiosks, AI diagnostics, cloud-based data management, and interoperability-focused offerings — are intensifying competition, pushing companies to differentiate through technical sophistication, service breadth, and deployment versatility.

CSI Health

AMD Global Telemedicine

Sonka Medical Technology

GlobalMed

Clinics On Cloud

The Telehealth Kiosk market is being increasingly shaped by advanced and emerging technologies that enhance functionality, efficiency, and patient experience. AI‑enabled diagnostic tools are now standard in over 60% of newly deployed kiosks, offering real-time triage, predictive analytics, and automated health assessments. Integration of IoT sensors enables continuous monitoring of vital signs such as blood pressure, oxygen saturation, heart rate, glucose levels, and temperature, with data transmission speeds exceeding 100 Mbps in urban installations, allowing seamless connectivity to electronic health record systems.

Cloud-based platforms play a pivotal role, with more than 70% of deployments leveraging secure cloud storage for remote monitoring, historical data analysis, and teleconsultation support. This facilitates multi-location management, where hospitals or networks can monitor up to 500–700 kiosks simultaneously from central dashboards. Touchless interfaces and voice-activated systems are being incorporated in 51% of new units to enhance hygiene, reduce infection risks, and improve accessibility for differently-abled patients.

Emerging technologies such as modular kiosk designs and prefabricated units reduce setup time by 30–45%, allowing rapid deployment in urban and rural areas. Advanced AI-enabled imaging, including integrated retinal and dermatology screening, is expanding diagnostic capabilities beyond traditional vitals monitoring. Additionally, 5G connectivity adoption is enabling real-time HD video consultations, supporting over 1,000 simultaneous patient interactions per kiosk network. These technology trends are positioning Telehealth Kiosks as intelligent, scalable, and versatile healthcare delivery platforms, critical for both urban healthcare systems and underserved regions.

The Telehealth Kiosk Market Report covers a comprehensive range of axes including product types, application use cases, end user categories, and geographic regions, thereby offering a holistic view of market structure and potential. On the product dimension, the report analyzes fixed pod style kiosks, mobile cart based units, wall mounted or countertop kiosks, as well as modular and prefabricated designs and accompanying software and services components. In terms of applications, it covers teleconsultation, remote patient monitoring, vital sign screening, digital pharmacy support, chronic disease management, preventive health check ups, and behavioral telecare, reflecting the broad versatility of kiosks across healthcare workflows. End user segmentation spans hospitals and specialty clinics, nursing homes and assisted living facilities, retail pharmacies, community clinics, corporate wellness centers, and other non traditional venues such as workplaces, schools, or public transit hubs.

Geographically, the report provides coverage across major global regions including North America, Europe, Asia Pacific, Middle East and Africa, and Latin America, with detailed breakdowns by region and country. It also examines technology trends such as AI driven diagnostics, cloud integration, IoT enabled vital sign sensors, and multilingual user interfaces, assessing their impact on both volume deployments and service capabilities. Additionally, the scope includes regulatory, reimbursement, and healthcare infrastructure factors influencing adoption across emerging and developed markets. For industry focus, the report addresses both traditional healthcare providers including hospitals and clinics and non traditional adopters including pharmacies, retail chains, corporate wellness, and community centers, offering insights for decision makers considering deployments across varied settings. The breadth of segments and dimensions ensures the report remains relevant for stakeholders evaluating product development, regional expansion, strategic partnerships, or technology driven service innovations.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2061.94 Million |

|

Market Revenue in 2032 |

USD 5215.73 Million |

|

CAGR (2025 - 2032) |

12.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

American Well (Amwell), Olea Kiosks Inc., KIOSK Information Systems, CSI Health, AMD Global Telemedicine, Sonka Medical Technology, GlobalMed, Clinics On Cloud |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |