Reports

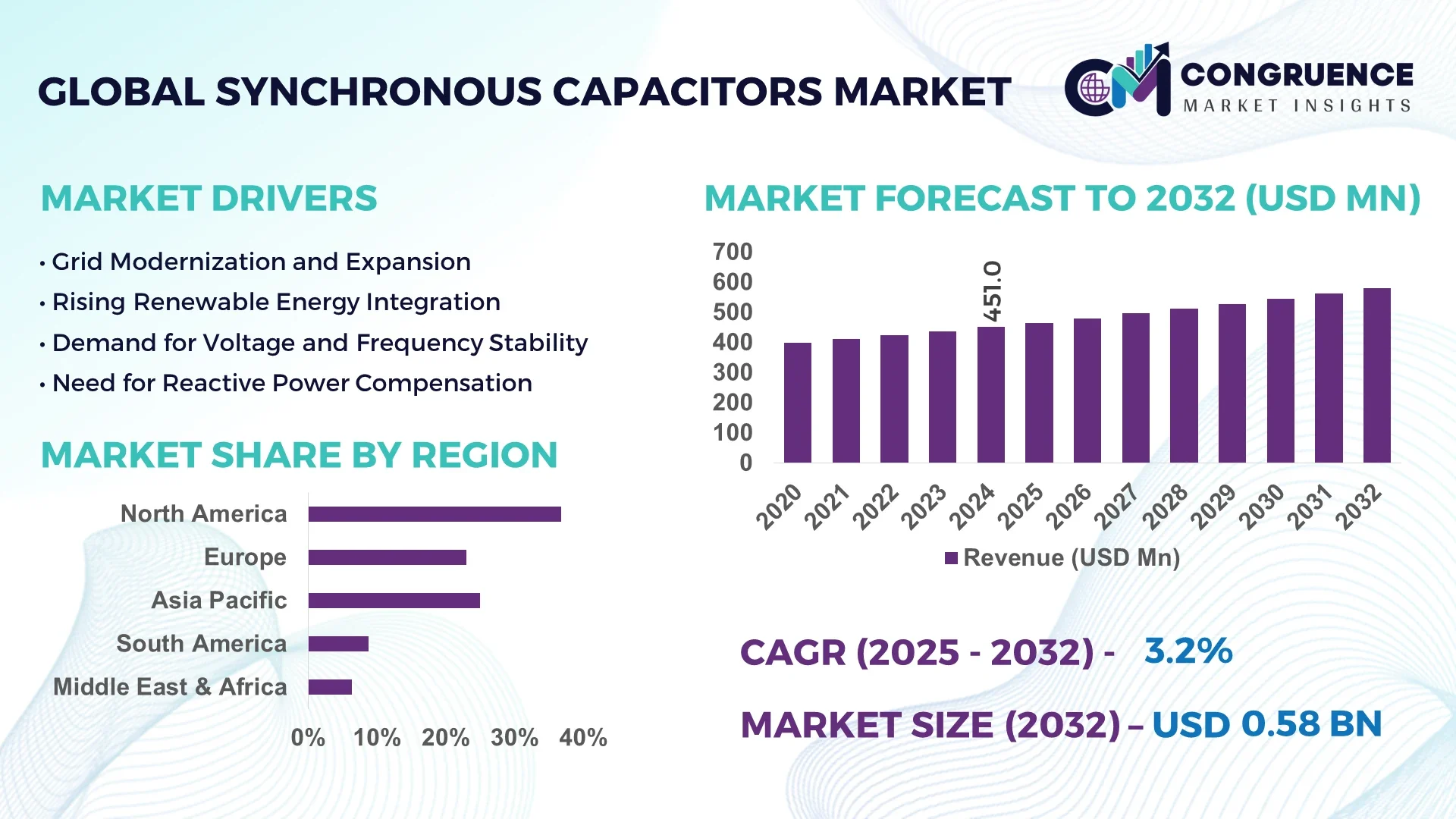

The Global Synchronous Capacitors Market was valued at USD 451 Million in 2024 and is anticipated to reach a value of USD 580.24 Million by 2032 expanding at a CAGR of 3.2% between 2025 and 2032.

In the United States, synchronous capacitor production capacity has seen significant enhancement with over 45 dedicated manufacturing units integrating advanced voltage stability systems and grid support technologies, supported by increased investments in industrial automation and high-voltage transmission applications.

The Synchronous Capacitors Market continues to gain traction across power generation, industrial manufacturing, and heavy-load utility segments due to the growing need for reactive power compensation and voltage regulation in aging grids. Recent technological innovations such as hybrid synchronous condenser systems, modular capacitor banks, and real-time monitoring units are reshaping operational frameworks across North America, Europe, and Asia-Pacific. Regulatory drivers focusing on grid stability, decarbonization mandates, and the integration of renewable energy sources are boosting the adoption of synchronous capacitors across utilities and industrial sectors. Furthermore, regional consumption patterns indicate a steady rise in demand for these capacitors in substations and large industrial plants to mitigate voltage fluctuations while improving power factor efficiency. The emergence of digital monitoring, predictive maintenance tools, and remote diagnostics in the synchronous capacitors market reflects a shift towards condition-based asset management, supporting utilities in reducing downtimes and optimizing operational costs while aligning with sustainability targets.

Artificial Intelligence is revolutionizing the Synchronous Capacitors Market by enhancing operational efficiency, predictive maintenance, and system optimization across manufacturing and deployment stages. Through AI-driven condition monitoring systems, synchronous capacitors are now integrated with predictive analytics to identify insulation deterioration, vibration patterns, and thermal performance deviations in real-time, allowing utility operators to schedule maintenance proactively and reduce unplanned outages. In the Synchronous Capacitors Market, AI-based digital twins are being employed to simulate performance under various load conditions, helping manufacturers design capacitors with optimized voltage support and reduced harmonic distortions tailored to dynamic grid conditions.

AI integration within the Synchronous Capacitors Market is also transforming operational workflows by enabling real-time fault diagnostics and intelligent grid synchronization, improving power factor control while reducing energy wastage. Machine learning algorithms are enhancing the tuning of control systems within synchronous capacitors, ensuring voltage stability in grids with fluctuating renewable energy inputs, and supporting automated grid balancing. Advanced AI-powered asset management platforms are helping utilities and industrial users track synchronous capacitor health indicators remotely, thereby extending asset life cycles and minimizing downtime while lowering maintenance costs. As the Synchronous Capacitors Market continues to align with digital transformation, AI is playing a pivotal role in automating testing procedures, refining control logic, and improving data-driven decision-making, which is crucial for modernizing the global grid infrastructure.

"In 2024, a leading U.S.-based grid solutions provider deployed an AI-powered predictive monitoring system across 30 synchronous capacitor installations, achieving a 12% reduction in reactive power losses and enhancing voltage regulation accuracy by 9% across high-demand industrial regions."

The Synchronous Capacitors Market is undergoing a strategic shift driven by increasing investments in grid infrastructure modernization and the integration of renewable energy sources across utility and industrial landscapes. As demand for reactive power compensation and voltage regulation intensifies, utilities and heavy industries are actively adopting synchronous capacitors to enhance grid stability and support fluctuating power loads. Recent industry dynamics reflect a growing focus on digital monitoring, predictive maintenance, and hybrid capacitor system integration within the Synchronous Capacitors Market, aligning operational frameworks with evolving environmental and regulatory standards. Additionally, advancements in modular design, smart controllers, and AI-enabled grid synchronization are enabling manufacturers and utilities to address evolving consumer and industrial needs while supporting grid resilience goals.

Grid modernization initiatives and the rapid integration of renewable energy systems are significantly driving growth within the Synchronous Capacitors Market. Utilities are prioritizing the deployment of synchronous capacitors to stabilize voltage and support reactive power management, addressing the variability inherent in renewable energy sources such as solar and wind. In 2024, global installed renewable energy capacity crossed 4,000 GW, intensifying the need for voltage support equipment to balance the grid. As countries enhance their transmission and distribution infrastructure, synchronous capacitors are deployed to reduce system losses while improving power factor efficiency in high-load areas. This driver is further reinforced by government-led grid stability projects and decarbonization policies, which position synchronous capacitors as critical tools in maintaining system reliability under dynamic load conditions.

High installation complexity and ongoing maintenance requirements are key restraints within the Synchronous Capacitors Market. These systems demand precise alignment, advanced insulation management, and continuous monitoring to ensure reliable operation under heavy grid loads. In industrial settings, synchronous capacitor units require specialized personnel for installation and maintenance, which increases operational costs and can delay deployment timelines. Additionally, older grid infrastructures, particularly in developing regions, face compatibility challenges when integrating modern synchronous capacitors, necessitating additional infrastructure upgrades. These factors collectively limit widespread adoption, particularly among small and medium-sized utilities, despite the operational benefits that synchronous capacitors provide in reactive power management.

The growing adoption of digital monitoring and predictive maintenance solutions presents a significant opportunity within the Synchronous Capacitors Market. The integration of IoT sensors, AI-driven analytics, and remote diagnostic tools within synchronous capacitor systems allows utilities to track health indicators, vibration data, and thermal conditions in real-time, improving operational efficiency and reducing unexpected downtimes. In 2024, multiple utilities across Europe and North America initiated the rollout of AI-based monitoring systems in capacitor banks to enhance asset management, resulting in measurable operational cost reductions. This trend opens opportunities for manufacturers to differentiate their offerings with smart, digitally enabled synchronous capacitors while supporting utility providers in meeting grid modernization and sustainability targets.

A significant challenge in the Synchronous Capacitors Market is the shortage of skilled personnel required for the installation, calibration, and ongoing maintenance of these systems, compounded by supply chain constraints affecting component availability. Advanced synchronous capacitors require precision engineering and sophisticated integration with grid control systems, demanding specialized technical expertise that is not uniformly available across all regions. Additionally, global supply chain disruptions impacting the availability of critical components such as insulated windings, voltage regulators, and monitoring sensors have led to extended lead times in 2024, affecting project timelines. These challenges impact scalability and the ability of utilities to meet immediate grid stability and modernization needs using synchronous capacitors.

• Expansion of Renewable Integration Projects: The Synchronous Capacitors Market is witnessing rising adoption driven by large-scale renewable energy integration projects globally. In 2024, over 150 new solar and wind projects above 100 MW integrated synchronous capacitors into their grid connection systems to stabilize voltage and manage reactive power. Utilities in Europe and Asia-Pacific are particularly focused on deploying synchronous capacitors in substations to handle load variability from renewable sources, ensuring smoother grid operation while reducing voltage fluctuations during peak and off-peak generation periods.

• Deployment of Digital Monitoring Solutions: A notable trend in the Synchronous Capacitors Market is the increased use of IoT-enabled monitoring and control systems in capacitor installations. Utilities and industrial players are investing in digital twin technology for synchronous capacitors, providing real-time analytics on vibration, insulation status, and thermal profiles. In 2024, over 20% of newly deployed synchronous capacitor banks included AI-powered predictive maintenance modules, enhancing asset reliability while reducing unplanned maintenance downtime.

• Rise in Modular and Prefabricated Installations: The market is shifting towards modular and prefabricated synchronous capacitor units to reduce project timelines and site labor dependency. These pre-assembled systems are increasingly used in North America and Europe, where substation upgrade timelines are critical. In 2024, modular capacitor installations accounted for over 30% of new utility projects, ensuring faster integration with existing grid systems and supporting immediate voltage stabilization requirements.

• Focus on High-Voltage Transmission Applications: High-voltage transmission infrastructure projects are driving demand in the Synchronous Capacitors Market, with utilities requiring robust voltage support across extensive grid networks. In 2024, several high-voltage direct current (HVDC) transmission lines integrated synchronous capacitors to enhance grid resilience and voltage control over long distances. These applications are particularly prominent in Asia, supporting expanding urban centers and industrial clusters with stable, reliable power.

The Synchronous Capacitors Market is segmented based on type, application, and end-user, allowing for precise targeting within the industry landscape. Types of synchronous capacitors include fixed and variable systems, which cater to different operational needs in voltage regulation and reactive power compensation. Key application areas cover substations, industrial power distribution, and high-voltage transmission projects, where synchronous capacitors improve grid stability and power factor efficiency. From an end-user perspective, the market serves utilities, heavy industries, and independent power producers, with utilities leading adoption due to the rising focus on grid modernization and renewable integration. Emerging trends indicate growing demand in industrial plants to manage heavy reactive loads, while the expansion of renewable projects is driving further need for synchronous capacitor integration across diverse applications.

Fixed synchronous capacitors lead the market segment due to their robust design and ease of deployment in grid stabilization and power factor correction applications across utilities and industrial sectors. These capacitors are frequently used in substations for voltage regulation and reactive power management, providing stability in regions with high load variations. Variable synchronous capacitors are the fastest-growing type, supported by their ability to adapt to dynamic grid conditions, especially in renewable energy integration projects requiring flexible voltage support. This flexibility allows utilities to manage rapid fluctuations in generation and demand, improving operational reliability. Other types, including hybrid synchronous capacitors that combine capacitor banks with advanced control systems, are gaining traction in projects demanding higher operational efficiency, particularly in industrial power distribution networks seeking reduced harmonic distortions and energy losses during heavy-load operations.

Substations represent the leading application in the Synchronous Capacitors Market, driven by their critical role in maintaining voltage stability and enhancing reactive power control within distribution and transmission networks. The widespread focus on upgrading aging grid infrastructure across North America and Europe has further increased deployment within substations. Industrial power distribution is the fastest-growing application, as heavy industries adopt synchronous capacitors to mitigate voltage fluctuations and improve energy efficiency in manufacturing facilities. The growing emphasis on maintaining uninterrupted operations in industries such as steel, cement, and chemical manufacturing fuels this rise. High-voltage transmission projects also contribute to the market, leveraging synchronous capacitors to stabilize power flows across extensive transmission lines, particularly in regions expanding renewable capacity to urban centers.

Utilities are the leading end-user segment in the Synchronous Capacitors Market, driven by ongoing grid modernization efforts and renewable energy integration across their distribution and transmission systems. Their focus on voltage stabilization and efficient reactive power management for uninterrupted power delivery necessitates consistent investments in synchronous capacitor installations. Heavy industries are the fastest-growing end-user segment, as sectors including steel, petrochemical, and automotive manufacturing increasingly require stable power quality to prevent equipment damage and operational downtime during high-load operations. Independent power producers are also emerging as relevant contributors to the market, deploying synchronous capacitors in their renewable generation facilities to enhance grid connectivity while ensuring compliance with stability and reactive power standards.

North America accounted for the largest market share at 36.8% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

The Synchronous Capacitors Market demonstrates strong regional variation, with North America leading due to established power infrastructure and widespread utility investments, while Asia-Pacific shows rapid growth driven by infrastructure development and industrial expansion. Europe maintains stable demand for synchronous capacitors with high environmental standards and grid modernization efforts, while South America and the Middle East & Africa are gradually increasing adoption in line with industrialization and energy diversification projects. Across these regions, demand is further supported by increasing renewable energy integration, high-voltage transmission expansions, and advanced grid stabilization initiatives aligned with sustainability goals.

Holding a market share of 36.8%, the Synchronous Capacitors Market in this region benefits from high demand across utilities and industrial power consumers seeking grid stabilization and reactive power management. Key industries driving demand include oil & gas, heavy manufacturing, and renewable energy integration, each requiring stable voltage control to maintain efficient operations. Regulatory support through grid modernization programs and government incentives for renewable energy integration continues to encourage capacitor deployments. Technological advancements such as digital monitoring systems and AI-driven predictive maintenance within synchronous capacitor units are being adopted by utilities to optimize grid operations while reducing maintenance-related downtimes across the region.

Capturing 28.4% of the global market share, the Synchronous Capacitors Market in this region sees strong participation from Germany, the UK, and France, driven by their advanced energy infrastructure and renewable energy commitments. Regulatory bodies like ENTSO-E and local governments enforce stringent grid stability standards, requiring utilities to adopt synchronous capacitors to manage reactive power effectively. Sustainability initiatives such as the European Green Deal encourage capacitor deployments within renewable energy projects. The region is witnessing rapid adoption of emerging technologies, including digital twin models for monitoring capacitor performance and modular capacitor systems to enhance integration with existing substations and high-voltage transmission networks.

Holding the fastest growth position, the Synchronous Capacitors Market in this region is led by China, India, and Japan, supported by large-scale manufacturing and infrastructure expansion projects. In 2024, the region accounted for 24.7% of global market volume, with rising demand from high-load industries and utilities seeking voltage stabilization and efficient power factor correction. China’s infrastructure growth and India’s grid modernization initiatives drive capacitor installations in substations and industrial plants, while Japan focuses on maintaining grid reliability alongside renewable integration. Regional technology hubs are fostering innovation in capacitor design, including modular and hybrid capacitor systems, facilitating advanced grid stability and efficient load management.

In this region, Brazil and Argentina lead capacitor adoption within the Synchronous Capacitors Market, which captured 5.3% of global market share in 2024. The region’s energy infrastructure projects, including hydropower and renewable expansions, are fueling demand for synchronous capacitors to manage reactive power in transmission networks. Brazil’s focus on grid modernization and Argentina’s industrial expansion necessitate voltage stabilization solutions to support operational efficiency in the power sector. Government incentives, such as tax reductions on grid improvement projects, are further encouraging deployments, while trade policies are facilitating the import of advanced capacitor technologies to support industrial growth across the region.

Driven by oil & gas, utilities, and construction sectors, the Synchronous Capacitors Market in this region accounted for 4.8% of global share in 2024, with strong activity in the UAE and South Africa. The demand is driven by large-scale industrial operations requiring grid stability and voltage control to maintain efficiency in high-load environments. Technological modernization initiatives, including the adoption of digital monitoring and AI-enabled capacitor systems, are gradually being integrated to optimize grid management. Local regulations encouraging energy diversification and regional trade partnerships for importing advanced power management technologies are further supporting market expansion within utility and industrial infrastructure projects.

United States – 29.5% Market Share

High production capacity and extensive utility grid infrastructure requiring voltage stabilization and reactive power management.

China – 18.2% Market Share

Strong end-user demand driven by rapid industrialization and grid modernization initiatives supporting heavy-load management and power quality enhancement.

The competitive landscape of the Synchronous Capacitors Market is characterized by the presence of over 50 active global and regional players focusing on delivering advanced reactive power compensation and voltage regulation solutions. The market sees intense competition driven by innovation in modular capacitor systems, digital monitoring integrations, and the adoption of AI-powered predictive maintenance within capacitor banks. Companies are actively engaging in partnerships with grid modernization programs and renewable energy integration projects, strengthening their positioning across utility and industrial applications. Several market players have expanded manufacturing capacities in North America and Asia-Pacific to cater to rising demand, while others have introduced modular and prefabricated synchronous capacitor solutions to reduce installation timelines and operational costs. Strategic initiatives such as technology licensing, cross-border collaborations, and the development of hybrid capacitor systems are influencing competition, allowing manufacturers to offer differentiated products with enhanced operational flexibility and grid stability benefits. The competitive environment is further shaped by continuous R&D investments in smart monitoring and automation, which are pivotal in addressing evolving customer needs in the Synchronous Capacitors Market.

Siemens Energy

General Electric (GE)

ABB Ltd.

Eaton Corporation

WEG Industries

Toshiba Energy Systems & Solutions Corporation

Mitsubishi Electric Corporation

Hyosung Heavy Industries

Nissin Electric Co., Ltd.

Fuji Electric Co., Ltd.

Technological advancements are significantly shaping the Synchronous Capacitors Market, enabling utilities and industrial users to enhance voltage regulation, reactive power management, and grid stability. The integration of IoT sensors and AI-powered predictive analytics in synchronous capacitors allows real-time monitoring of parameters such as vibration, insulation condition, and thermal behavior, reducing unplanned outages and maintenance costs. The deployment of digital twin models enables simulation of capacitor performance under varying grid loads, aiding utilities in optimizing operational strategies while ensuring system reliability.

Emerging hybrid synchronous capacitor systems, which combine conventional capacitor functionalities with advanced power electronic controllers, are gaining traction to improve dynamic voltage support and reduce harmonic distortions in grids with high renewable penetration. Modular and prefabricated capacitor units are being developed to accelerate installation processes and enable flexible deployment across substations and industrial facilities. Innovations in advanced insulation materials and high-efficiency synchronous motors are further improving system durability and operational effectiveness. Additionally, synchronous capacitors are increasingly being integrated with SCADA systems for seamless grid management, enabling remote configuration and automated voltage support. These technological developments in the Synchronous Capacitors Market are critical for modernizing aging grid infrastructures while aligning with sustainability and efficiency goals in power transmission and distribution networks.

• In March 2024, Siemens Energy launched a new modular synchronous condenser system equipped with integrated monitoring sensors to enhance grid stability across renewable-heavy networks, supporting utilities in optimizing voltage regulation with reduced installation timelines.

• In February 2024, GE successfully deployed advanced synchronous capacitors in a major substation project in Texas, enhancing reactive power compensation capabilities to support a 500 MW wind farm integration into the local grid while reducing voltage fluctuation events.

• In October 2023, ABB introduced an AI-driven condition monitoring platform for synchronous capacitors, providing real-time thermal, vibration, and insulation health analytics to utilities, which improved predictive maintenance and reduced maintenance downtime by up to 15%.

• In May 2023, WEG Industries expanded its manufacturing facility in Brazil to produce high-capacity synchronous capacitors designed for high-voltage transmission lines, addressing increasing demand from South American utilities for advanced voltage support solutions.

The Synchronous Capacitors Market Report comprehensively covers global and regional analysis across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, focusing on the deployment of synchronous capacitors in utility grids, high-voltage transmission projects, industrial facilities, and renewable integration systems. The report examines market segmentation by type, including fixed, variable, and hybrid synchronous capacitors, and by application, encompassing substations, industrial power distribution, and transmission network stability enhancement.

It includes analysis of technological innovations, such as the integration of digital monitoring, predictive maintenance tools, and modular capacitor systems, along with the adoption of advanced insulation and power electronic controllers to improve operational efficiency. The report also explores the impact of regulatory standards driving voltage stabilization and reactive power management within modern grids, while detailing emerging trends like the use of AI-based digital twins and remote monitoring to optimize asset management.

Additionally, the scope covers competitive landscape mapping, highlighting key players’ strategic initiatives, product launches, facility expansions, and regional development programs influencing market growth. The report captures insights into the increasing need for synchronous capacitors in managing reactive power challenges in grids with high renewable penetration while addressing demand for energy efficiency and grid modernization initiatives globally. This structured and factual analysis serves as a decision-support tool for manufacturers, utilities, and industrial stakeholders planning investments in the Synchronous Capacitors Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 451 Million |

|

Market Revenue in 2032 |

USD 580.24 Million |

|

CAGR (2025 - 2032) |

3.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens Energy, General Electric (GE), ABB Ltd., Eaton Corporation, WEG Industries, Toshiba Energy Systems & Solutions Corporation, Mitsubishi Electric Corporation, Hyosung Heavy Industries, Nissin Electric Co., Ltd., Fuji Electric Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |