Reports

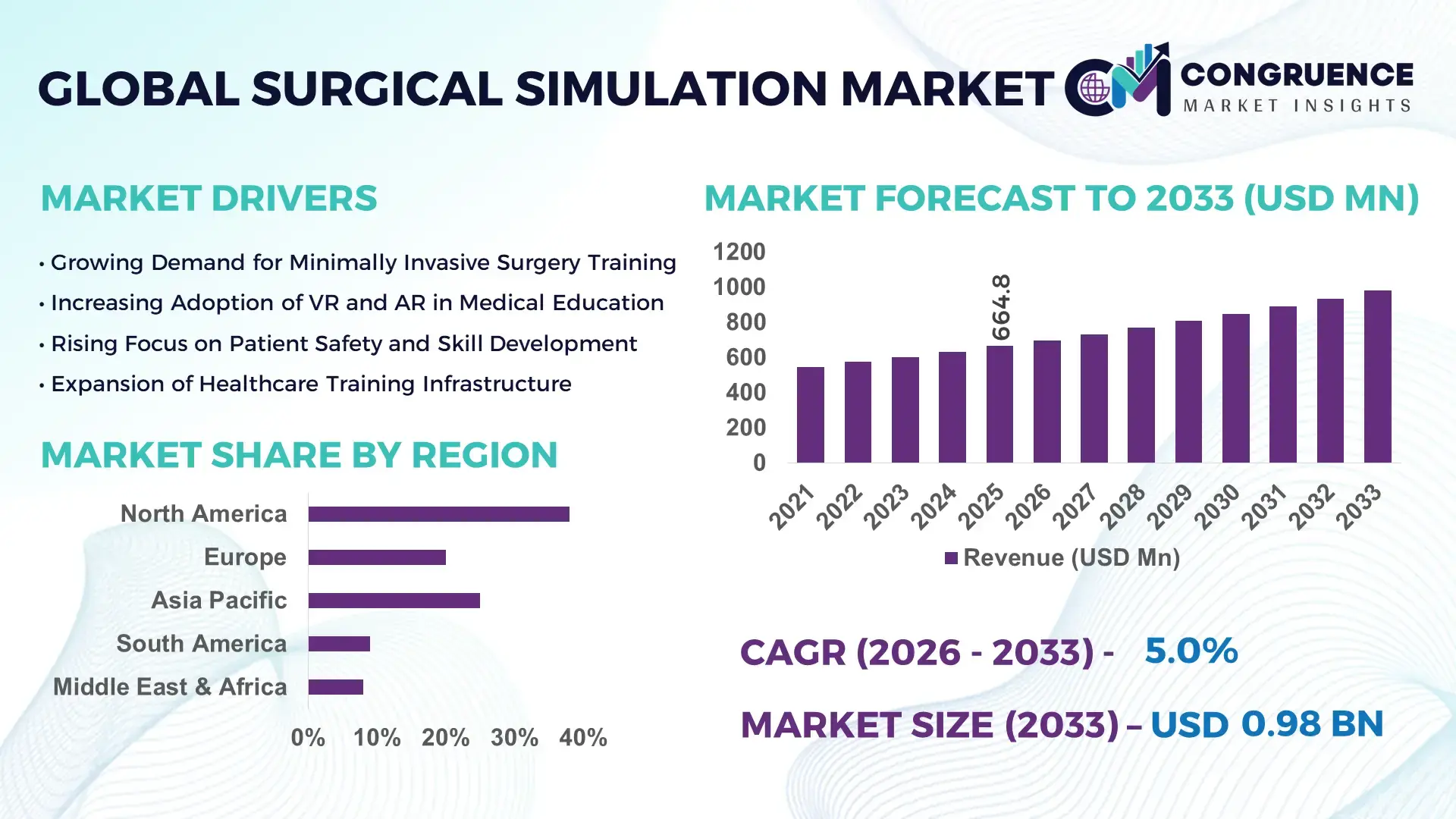

The Global Surgical Simulation Market was valued at USD 664.8 Million in 2025 and is anticipated to reach a value of USD 982.22 Million by 2033 expanding at a CAGR of 5% between 2026 and 2033. Growth is supported by increasing adoption of digital surgical training solutions designed to enhance clinical precision, reduce medical errors, and strengthen workforce readiness in modern healthcare environments.

In the United States, the surgical simulation industry shows strong production capabilities supported by more than 150 advanced medical simulation centers operating within teaching hospitals and research universities. Annual investment in healthcare training technologies exceeds USD 350 Million, while more than 60% of accredited surgical residency programs integrate immersive simulation platforms. Hospitals and academic institutions deploy simulation technologies across orthopedic surgery, cardiovascular procedures, laparoscopic techniques, and robotic-assisted surgical training. Over 1,200 residency programs utilize structured simulation-based learning models, and training delivered through digital surgical simulation systems has increased by nearly 30% in recent years, reflecting expanding institutional adoption and technology integration.

• Market Size & Growth: The surgical simulation market reached USD 664.8 Million in 2025 and is projected to grow to USD 982.22 Million by 2033, expanding at a CAGR of 5%, driven by rising demand for advanced clinical training systems and technology-enabled surgical education platforms worldwide.

• Top Growth Drivers: Simulation-based training adoption increased by 48%, operational efficiency improvements reached 35%, and surgical error reduction initiatives contributed approximately 27% growth momentum across hospitals and medical education institutions.

• Short-Term Forecast: By 2028, healthcare organizations implementing next-generation surgical simulation solutions are expected to achieve up to 22% reduction in training costs and around 18% improvement in procedural competency among surgeons and residents.

• Emerging Technologies: Integration of immersive virtual reality surgical environments, artificial intelligence–driven performance analytics, and cloud-enabled collaborative simulation platforms is transforming modern surgical training and digital healthcare education systems.

• Regional Leaders: North America is projected to reach nearly USD 380 Million by 2033 supported by advanced healthcare infrastructure, Europe is expected to approach USD 270 Million through strong academic medical training programs, and Asia-Pacific may exceed USD 230 Million due to expanding hospital investments and medical education modernization.

• Consumer/End-User Trends: Teaching hospitals, medical universities, and specialized surgical training institutes represent the largest adoption segment, with over 55% of institutions integrating simulation technologies for minimally invasive and robotic surgery training programs.

• Pilot or Case Example: In 2024, a structured hospital training initiative utilizing advanced surgical simulation platforms reported a 26% improvement in surgical performance accuracy and reduced procedural preparation time by approximately 19% within residency programs.

• Competitive Landscape: The market leader CAE Healthcare holds roughly 18% share, followed by major participants including 3D Systems, Mentice, Gaumard Scientific, and Simbionix.

• Regulatory & ESG Impact: Healthcare training standards and patient safety frameworks are promoting wider adoption of simulation-based certification programs, while environmentally efficient digital training solutions are reducing reliance on traditional resource-intensive surgical education models.

• Investment & Funding Patterns: Recent global investment in surgical simulation technologies has exceeded USD 420 Million, reflecting increased venture capital participation, strategic partnerships, and expansion of medical technology innovation programs.

• Innovation & Future Outlook: Advancements in haptic feedback technology, AI-assisted surgical assessment systems, and remote collaborative training environments are expected to redefine the future of surgical education and scalable clinical training worldwide.

Healthcare education institutions, defense medical training programs, and specialized surgical centers collectively account for more than 70% of total demand for surgical simulation technologies. Recent innovations include high-fidelity anatomical simulation models, cloud-integrated surgical planning platforms, and AI-powered performance monitoring tools that enhance training outcomes. Regulatory frameworks promoting standardized surgical training and growing investments in hospital infrastructure across emerging economies are accelerating adoption. North America and Europe continue to demonstrate strong utilization in robotic and minimally invasive procedure training, while Asia-Pacific is experiencing rapid expansion of simulation laboratories in medical universities. Future growth is expected to be supported by integrated digital training ecosystems, remote simulation learning platforms, and expanding collaboration between healthcare providers and medical technology developers.

The strategic relevance of the Surgical Simulation Market is closely tied to healthcare system modernization, workforce readiness, and patient safety optimization. Healthcare institutions are increasingly integrating advanced digital surgical training platforms to improve procedural outcomes and reduce dependency on traditional training environments. For instance, immersive virtual reality surgical simulation delivers nearly 40% improvement in procedural accuracy compared to conventional cadaver-based training methods, enabling surgeons to rehearse complex operations repeatedly without clinical risk. Hospitals and medical universities are allocating structured budgets toward simulation infrastructure, with large academic healthcare systems deploying multi-specialty training labs capable of supporting more than 20 surgical disciplines simultaneously.

From a regional perspective, United States dominates in training volume and simulation infrastructure capacity, while Asia-Pacific leads in adoption expansion, with nearly 52% of newly established medical universities integrating simulation-based surgical education platforms. By 2028, artificial intelligence–driven surgical analytics and adaptive learning systems are expected to improve training efficiency and reduce surgical preparation time by approximately 25%, particularly in robotic and minimally invasive surgery programs.

Compliance and sustainability goals are also shaping industry strategies. Healthcare organizations and simulation technology providers are committing to ESG-driven targets, including 30% reduction in training resource waste and reusable simulation modules by 2030. In 2024, Mentice expanded digital simulation deployments across hospital networks, enabling measurable improvements in surgical skill assessment and reporting approximately 21% enhancement in clinician performance evaluation efficiency through AI-enabled training analytics.

The growing global adoption of minimally invasive and robotic-assisted surgeries is significantly increasing demand for surgical simulation technologies. Hospitals performing advanced laparoscopic and robotic procedures require specialized training environments that allow surgeons to practice complex techniques before live operations. More than 12 million minimally invasive procedures are conducted globally each year, prompting medical institutions to invest in simulation-based skill development. Robotic surgery platforms require structured training modules that can replicate real-time surgical scenarios, enabling clinicians to refine precision, coordination, and decision-making. Simulation-based training programs have demonstrated up to 30% improvement in surgical proficiency and reduction in procedural errors among residents and newly trained surgeons. Additionally, medical universities are integrating simulation labs within surgical departments to ensure standardized skill development across multiple specialties such as orthopedics, neurology, and cardiovascular surgery. As surgical procedures become more technologically advanced, simulation-driven training programs are becoming an essential component of modern healthcare education and clinical performance improvement.

Despite growing adoption, the Surgical Simulation Market faces limitations due to the significant cost associated with high-fidelity simulation systems and specialized infrastructure. Advanced surgical simulators equipped with immersive visualization, haptic feedback, and artificial intelligence analytics require substantial capital investment by hospitals and medical institutions. Establishing a full-scale simulation training center can require multiple simulation units, dedicated technical staff, and continuous software upgrades. Smaller hospitals and developing healthcare systems often struggle to allocate funds for such investments, which slows adoption in certain regions. In addition, maintaining simulation hardware, updating training modules, and ensuring compatibility with evolving surgical technologies adds operational complexity. Training faculty members and clinicians to effectively utilize advanced simulation systems also requires time and structured programs. These financial and operational barriers create uneven deployment across healthcare institutions, particularly where medical education funding or healthcare infrastructure expansion is limited.

Rapid digital transformation in healthcare is creating new opportunities for the Surgical Simulation Market, particularly through remote learning platforms and cloud-connected simulation ecosystems. Medical institutions are increasingly adopting virtual training modules that allow surgeons to participate in collaborative training sessions across different geographic locations. Tele-simulation programs enable experienced specialists to guide surgical trainees remotely, improving accessibility to advanced training resources. The expansion of digital medical education infrastructure is also encouraging the development of modular simulation platforms that can support multiple surgical disciplines within a single training environment. Emerging markets are investing in new medical universities and training centers, creating demand for scalable simulation systems capable of supporting thousands of trainees annually. Furthermore, advancements in data analytics allow training platforms to provide personalized feedback and performance benchmarking, enabling institutions to track competency development more effectively. These developments are opening pathways for technology providers to expand into new healthcare ecosystems and strengthen global training networks.

One of the major challenges facing the Surgical Simulation Market is aligning simulation technologies with evolving regulatory frameworks and healthcare training standards. Medical education authorities and accreditation bodies require structured validation of training programs, which means simulation platforms must demonstrate consistent performance evaluation capabilities. Integrating simulation systems with hospital training workflows, robotic surgery platforms, and clinical data systems can also be technically complex. Healthcare institutions often operate diverse digital infrastructures, making seamless interoperability between simulation software and hospital systems difficult to achieve. Additionally, ensuring realism and accuracy in surgical scenarios requires continuous updates in anatomical modeling, procedural datasets, and software algorithms. As surgical techniques evolve, simulation providers must frequently upgrade content and hardware capabilities. These integration and compliance requirements increase development timelines and operational complexity for both healthcare providers and technology manufacturers operating within the Surgical Simulation Market.

• Expansion of AI-Enabled Surgical Performance Analytics: Artificial intelligence integration is transforming the Surgical Simulation market by enabling real-time performance tracking and objective skill evaluation. Nearly 62% of newly installed surgical simulators in large teaching hospitals now include AI-driven assessment tools that measure precision, instrument handling, and response time. Training programs using AI analytics have reported up to 28% faster competency validation among surgical residents and a 19% improvement in procedural accuracy during advanced laparoscopic and robotic training modules. Technology providers such as Mentice are incorporating automated benchmarking systems that allow hospitals to standardize training outcomes across multiple departments and surgical specialties.

• Rapid Adoption of Virtual Reality–Based Surgical Training Platforms: Virtual reality simulation environments are becoming a core component of modern surgical education infrastructure. Approximately 58% of medical universities have integrated VR-based simulation labs within their surgical training departments, enabling trainees to perform hundreds of simulated procedures annually without clinical risk. Hospitals deploying immersive VR surgical training have observed up to 31% improvement in hand-eye coordination and procedural efficiency during minimally invasive surgeries. In regions such as United States, more than 120 academic medical institutions operate VR simulation facilities supporting multi-disciplinary surgical education programs.

• Growth of Robotic Surgery Simulation Programs in Medical Institutions: With robotic surgery procedures increasing globally, healthcare organizations are expanding simulation programs tailored for robotic-assisted operations. Over 45% of tertiary care hospitals now provide dedicated robotic surgery simulators within their training ecosystems. Surgeons completing structured robotic simulation training demonstrate around 26% reduction in operational errors and improved procedural confidence. Training platforms aligned with robotic systems from companies like Intuitive Surgical are being adopted widely, allowing clinicians to practice complex surgical maneuvers before performing live procedures.

• Emergence of Cloud-Connected Collaborative Simulation Networks: Healthcare institutions are increasingly adopting cloud-enabled surgical simulation platforms that allow remote collaboration, shared training modules, and centralized performance monitoring. Approximately 47% of new simulation deployments now support remote training access across multiple hospital campuses. This model enables up to 35% increase in training participation among geographically dispersed surgical teams. In Asia-Pacific, several medical universities have established interconnected simulation networks capable of supporting more than 3,000 trainees annually, strengthening regional medical education infrastructure and accelerating standardized surgical skill development.

The Surgical Simulation Market segmentation reflects the evolving needs of modern healthcare training and the growing integration of digital medical education tools. The market is broadly categorized by types of simulation technologies, application areas within surgical training, and key end-users adopting these solutions. Simulation platforms are increasingly deployed to support minimally invasive procedures, robotic surgery, and complex specialty training programs across hospitals and medical universities. Around 65% of large teaching hospitals worldwide now integrate structured simulation modules into surgical residency programs to enhance procedural readiness and reduce training risks. Technology-driven segmentation is also influenced by the increasing use of immersive digital environments that provide measurable skill assessment and real-time feedback. Adoption patterns indicate strong utilization of advanced simulators in orthopedics, neurosurgery, and cardiovascular training. Meanwhile, emerging healthcare systems are investing in new simulation laboratories within academic institutions to support growing numbers of surgical trainees and expand clinical education capacity.

The Surgical Simulation Market by type includes virtual reality surgical simulators, augmented reality simulation platforms, physical or anatomical simulators, and cloud-enabled simulation systems designed for remote collaboration and training. Virtual reality simulators currently represent the leading segment, accounting for approximately 41% of adoption because they enable immersive procedural training environments and provide measurable performance metrics for surgical trainees. Augmented reality simulation systems hold around 23% share and are widely used for anatomy visualization and guided surgical training modules, particularly in complex procedures that require layered visualization of internal structures. Cloud-connected surgical simulation platforms are the fastest-growing type with an estimated growth rate of about 8.5% annually. This growth is driven by increasing demand for remote training capabilities, collaborative surgical education, and scalable digital learning infrastructure that allows institutions to connect multiple training facilities simultaneously. These systems also enable centralized performance monitoring and standardized training modules across healthcare networks. Physical anatomical simulators and hybrid systems collectively contribute nearly 36% of the market landscape, maintaining relevance in foundational surgical skill training where tactile feedback and manual practice are essential. These simulators are widely deployed in orthopedic and cardiovascular surgical education programs to provide early-stage procedural familiarity.

The application segmentation of the Surgical Simulation Market includes surgical education and academic training, minimally invasive surgery training, robotic-assisted surgery training, and specialty surgical simulations such as neurology and cardiovascular procedures. Surgical education and academic training currently lead the segment with approximately 44% adoption, as medical universities and teaching hospitals rely on simulation platforms to train large volumes of surgical residents and medical students in controlled learning environments. Minimally invasive surgery training accounts for around 26% of application use, reflecting the global increase in laparoscopic and endoscopic procedures that require precision-focused training before live operations. Robotic-assisted surgery training is the fastest-growing application area with an estimated growth rate of about 9.1% annually. The expansion of robotic surgery programs in hospitals is driving demand for specialized simulators that allow surgeons to practice complex operations and refine procedural accuracy. Specialty surgical simulations collectively represent about 30% of application deployment, particularly within tertiary healthcare institutions focusing on advanced clinical procedures. These simulations often involve high-fidelity anatomical models and scenario-based learning modules that support complex decision-making during surgery.

End-user segmentation within the Surgical Simulation Market includes hospitals, academic medical institutions, specialized surgical training centers, and medical device manufacturers. Hospitals represent the leading end-user segment with approximately 46% adoption, as healthcare providers increasingly incorporate simulation systems into surgical training programs, clinical skill development, and ongoing professional education for surgeons. Academic medical institutions account for nearly 34% of the market due to the growing need to train large numbers of medical students and residents within standardized educational frameworks. These institutions often operate advanced simulation laboratories designed to support multiple surgical specialties and interdisciplinary training programs. Specialized surgical training centers are the fastest-growing end-user group with an estimated growth rate of about 8.7% annually. The rise of fellowship-level training programs and advanced robotic surgery education is contributing to this expansion, particularly in regions investing heavily in medical education infrastructure. Medical device companies and research organizations collectively represent about 20% of adoption, using simulation platforms to test surgical tools, validate procedural workflows, and support clinician training aligned with new surgical technologies.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

The global Surgical Simulation Market shows clear regional performance variations influenced by healthcare infrastructure investment, number of medical training institutions, and adoption of digital surgical education technologies. North America recorded deployment of more than 320 advanced surgical simulation centers across hospitals and universities, while Europe operates over 240 structured clinical training laboratories supporting simulation-based surgical programs. Asia-Pacific is rapidly expanding its training capacity, with more than 180 new simulation labs established across medical universities between 2022 and 2025. Latin America and the Middle East & Africa are also witnessing gradual adoption, supported by healthcare modernization initiatives and cross-border medical education partnerships. Globally, more than 65% of large teaching hospitals use simulation-based surgical education, and nearly 48% of new surgical residency programs launched after 2023 include digital simulation training as a mandatory curriculum component.

How are advanced clinical training ecosystems shaping surgical education transformation?

The North America Surgical Simulation Market holds approximately 38% market share, supported by strong healthcare infrastructure and widespread integration of digital medical training technologies. Key industries driving demand include academic medical institutions, tertiary hospitals, and medical device development programs. The region hosts more than 150 accredited medical universities and over 1,200 surgical residency programs, many of which utilize structured simulation-based training modules to improve clinical preparedness. Regulatory frameworks encouraging patient safety standards and competency-based training have accelerated adoption of simulation technologies across hospitals. Advanced digital transformation initiatives are promoting the use of virtual reality, augmented reality, and AI-based surgical analytics platforms for performance tracking. A notable regional player, CAE Healthcare, continues expanding training solutions across hospital networks and research institutions. Consumer behavior patterns show higher enterprise adoption in healthcare education, with nearly 60% of large hospitals integrating simulation-driven surgical training programs.

How are standardized medical training frameworks accelerating adoption of advanced surgical simulation technologies?

The Europe Surgical Simulation Market accounts for nearly 27% of global adoption, driven by structured healthcare education systems and regulatory emphasis on clinical training quality. Major markets such as Germany, the United Kingdom, and France collectively host more than 110 major medical universities integrating simulation laboratories into surgical education. Regulatory bodies promoting standardized medical training and patient safety initiatives are encouraging hospitals to incorporate simulation-based competency programs. Sustainability initiatives within healthcare institutions are also supporting digital training systems that reduce reliance on traditional resource-intensive training methods. Emerging technologies including AI-driven simulation assessment tools and mixed-reality surgical environments are increasingly deployed across European teaching hospitals. A regional participant, Mentice, has expanded advanced interventional simulation platforms used in multiple clinical training programs. Consumer behavior patterns in the region show strong institutional demand driven by regulatory pressure that prioritizes explainable and standardized surgical simulation outcomes.

What factors are accelerating adoption of digital surgical training platforms across healthcare institutions?

The Asia-Pacific Surgical Simulation Market ranks among the fastest expanding regions, accounting for nearly 22% of global deployment volume and continuing to increase as healthcare education infrastructure expands. Leading consuming countries include China, India, and Japan, which collectively represent more than 65% of regional medical training investments in simulation technologies. Rapid growth in medical universities and teaching hospitals has led to the establishment of over 180 new simulation laboratories between 2022 and 2025. The region is also witnessing strong innovation hubs focused on digital healthcare education technologies and robotic surgical training systems. Companies such as 3D Systems are supporting anatomical model development and simulation tools used by training institutions. Regional consumer behavior indicates strong growth driven by digital healthcare platforms, mobile-based training tools, and government-supported medical education modernization programs across large population centers.

How are healthcare modernization initiatives supporting clinical training expansion?

The South America Surgical Simulation Market represents approximately 7% of global adoption, with Brazil and Argentina leading regional deployment of simulation technologies in teaching hospitals and medical universities. Brazil alone accounts for nearly 45% of the region’s surgical training infrastructure, supported by expanding healthcare education programs and public-private partnerships. Infrastructure improvements in healthcare facilities and growing investments in advanced clinical training are supporting gradual market development. Government-backed initiatives promoting medical education and clinical safety standards are encouraging hospitals to integrate simulation-based surgical training. Regional training networks are also forming to improve access to advanced medical education across multiple countries. Hospitals in major urban centers are adopting digital surgical training tools to enhance clinician readiness. Consumer behavior trends show growing demand linked to multilingual training platforms and localization of simulation modules tailored to regional medical education systems.

What role does healthcare infrastructure modernization play in surgical training adoption?

The Middle East & Africa Surgical Simulation Market holds close to 6% share of global adoption, supported by investments in healthcare infrastructure and clinical training modernization programs. Countries such as the United Arab Emirates and South Africa are leading regional development of advanced medical training facilities and simulation-based education programs. Healthcare systems in the region are increasingly integrating digital learning environments to support surgical skill development across expanding hospital networks. Government-supported healthcare transformation initiatives and international partnerships are encouraging adoption of advanced simulation technologies. Technological modernization trends include deployment of virtual surgical training systems and AI-enabled performance evaluation tools in major medical centers. Regional institutions are also focusing on capacity building, with several training hospitals developing simulation labs capable of supporting more than 1,000 trainees annually. Consumer behavior shows increasing demand for technology-enabled medical education aligned with international training standards.

United States – 34% share in the Surgical Simulation Market: Strong network of medical universities, extensive surgical residency programs, and advanced healthcare technology adoption support dominant training infrastructure.

Germany – 11% share in the Surgical Simulation Market: High concentration of teaching hospitals, structured medical education frameworks, and strong demand for precision surgical training technologies drive consistent market leadership.

The Surgical Simulation market demonstrates a moderately fragmented competitive structure with over 35 active global and regional technology providers developing advanced surgical training platforms. The top five companies collectively control nearly 46% of the global competitive positioning, driven by continuous innovation in virtual reality simulators, robotic surgery training modules, and AI-enabled performance analytics. Market leaders are focusing on strategic expansion through product innovation, hospital partnerships, and integration of digital learning ecosystems across healthcare institutions. In the past three years, more than 25 new surgical simulation platforms have been launched globally, emphasizing immersive environments, haptic feedback technology, and cloud-connected training capabilities.

Competition is intensifying as medical universities and hospitals expand simulation-based training programs. Around 60% of large teaching hospitals now evaluate simulation vendors based on AI-driven analytics capabilities and multi-specialty training compatibility. Several companies are also investing in collaborations with academic medical institutions to co-develop procedure-specific training systems. Additionally, mergers and strategic partnerships have increased by nearly 18% between 2023 and 2025, reflecting industry consolidation efforts and technology integration initiatives. Innovation trends shaping competition include mixed reality surgical planning tools, patient-specific anatomical modeling using 3D printing, and remote simulation platforms supporting distributed training networks. More than 40% of new product developments focus on robotic surgery simulation, reflecting the growing complexity of modern surgical procedures. Vendors are also expanding service-based training ecosystems that allow healthcare organizations to standardize competency evaluation across multiple facilities.

CAE Healthcare

Surgical Science Sweden AB

Mentice

VirtaMed

Simulab Corporation

3D Systems Healthcare

Gaumard Scientific

Intelligent Ultrasound Group

Kyoto Kagaku Co., Ltd.

Limbs & Things

Inovus Medical

Surgical Theater

FundamentalVR

Technological innovation is significantly transforming the Surgical Simulation Market as healthcare organizations invest in advanced digital training systems designed to improve surgical precision and workforce preparedness. Virtual reality and augmented reality technologies are widely deployed across modern surgical training laboratories, with more than 58% of newly established simulation centers integrating immersive digital environments. These systems allow clinicians to practice complex procedures repeatedly using highly detailed anatomical models built from thousands of medical imaging datasets. Modern simulation platforms now include motion tracking, instrument positioning sensors, and real-time feedback engines that can evaluate surgical actions during training sessions. Artificial intelligence is becoming an essential component of advanced surgical simulation solutions. AI-enabled systems can analyze over 120 measurable performance indicators such as instrument accuracy, procedural time, and decision-making efficiency. Hospitals implementing AI-supported training platforms have recorded improvements of nearly 20% in competency assessments among surgical trainees. These technologies also support personalized learning modules, allowing trainees to focus on specific skills requiring improvement while maintaining standardized training benchmarks across institutions.

Another important technology trend involves patient-specific simulation and surgical planning tools. Healthcare providers are increasingly using 3D anatomical models created from CT and MRI imaging data to replicate complex surgical cases before performing live procedures. More than 40% of large teaching hospitals now incorporate personalized anatomical simulation for advanced surgical training and preoperative planning, particularly in neurosurgery and cardiovascular interventions. Cloud-based collaborative simulation systems are also expanding rapidly across healthcare networks. Approximately 47% of new surgical simulation deployments now include remote access capabilities that allow multiple hospitals and training institutions to share simulation modules and performance data through centralized platforms. Additionally, robotic surgery simulation technologies are enabling clinicians to practice advanced robotic-assisted procedures in controlled environments before entering operating rooms. These integrated technologies are strengthening digital surgical education ecosystems and enabling healthcare organizations to standardize training outcomes while improving overall surgical preparedness.

• In January 2024, CAE Healthcare announced a strategic collaboration with GigXR to expand multimodal healthcare simulation solutions integrating physical, digital, and immersive technologies. The initiative supports medical schools, hospitals, and training institutions in implementing scalable surgical and clinical simulation curricula worldwide. Source: company press release

• In January 2024, SimHawk partnered with CAE Healthcare to enhance ultrasound education using combined cloud-based simulation and high-fidelity manikin systems such as the Vimedix platform. The collaboration aims to improve procedural training efficiency and expand simulation-driven learning across clinical education programs. Source: company press release

• In June 2025, Treatment.com AI launched a Medical Education Suite featuring AI-simulated patients and real-time performance assessment tools. The platform was deployed at the University of Minnesota Medical School with more than 240 students, enabling scalable clinical training and demonstrating measurable cost efficiencies in simulation-based education. Source: company announcement

• In December 2025, Indian Nursing Council supported the launch of India’s second national reference simulation centre at BVV Sangha’s Sajjalashree Institute of Nursing Sciences in Bagalkot. The 22,000-square-foot facility includes advanced simulation suites, virtual reality units, and high-fidelity mannequins to strengthen surgical and clinical training capabilities. Source: industry news report

The Surgical Simulation Market Report provides a structured assessment of technologies, applications, and institutional adoption patterns shaping the global simulation-based surgical training ecosystem. The scope includes comprehensive analysis across hardware platforms, software-driven simulation systems, and integrated training environments designed for medical education, professional skill development, and procedural validation. The report evaluates simulation technologies such as virtual reality, augmented reality, mixed reality platforms, haptic-enabled simulators, AI-supported learning systems, and high-fidelity patient mannequins that replicate real surgical conditions. Market segmentation within the report examines multiple product categories including laparoscopic surgery simulators, robotic surgery training systems, endovascular simulation platforms, orthopedic and neurosurgical training modules, and multidisciplinary procedural simulators. It also explores simulation delivery formats such as on-premise simulation labs, academic training centers, hospital-based education programs, and cloud-connected digital simulation platforms. Analysis includes integration of data analytics, performance tracking systems, and competency-based training models used by healthcare institutions to standardize surgical education.

Geographic coverage spans major healthcare innovation regions including North America, Europe, Asia-Pacific, the Middle East, Latin America, and emerging healthcare markets where medical training infrastructure is expanding. The report reviews adoption patterns across more than 40 countries, highlighting investments in simulation centers, technology partnerships, and institutional training programs supporting surgeons, residents, nurses, and emergency care professionals. Industry focus areas include academic medical institutions, teaching hospitals, surgical training institutes, defense medical training facilities, and private healthcare networks. The report also considers niche and emerging segments such as AI-driven virtual patients, digital twin-based surgical rehearsal systems, remote collaborative simulation environments, and data-centric training analytics platforms. Overall, the scope emphasizes technology innovation, training scalability, and the role of simulation in improving procedural competency, patient safety, and healthcare workforce preparedness across diverse healthcare systems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

CAE Healthcare, Surgical Science Sweden AB, Mentice, VirtaMed, Simulab Corporation, 3D Systems Healthcare, Gaumard Scientific, Intelligent Ultrasound Group, Kyoto Kagaku Co., Ltd., Limbs & Things, Inovus Medical , Surgical Theater , FundamentalVR |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |