Reports

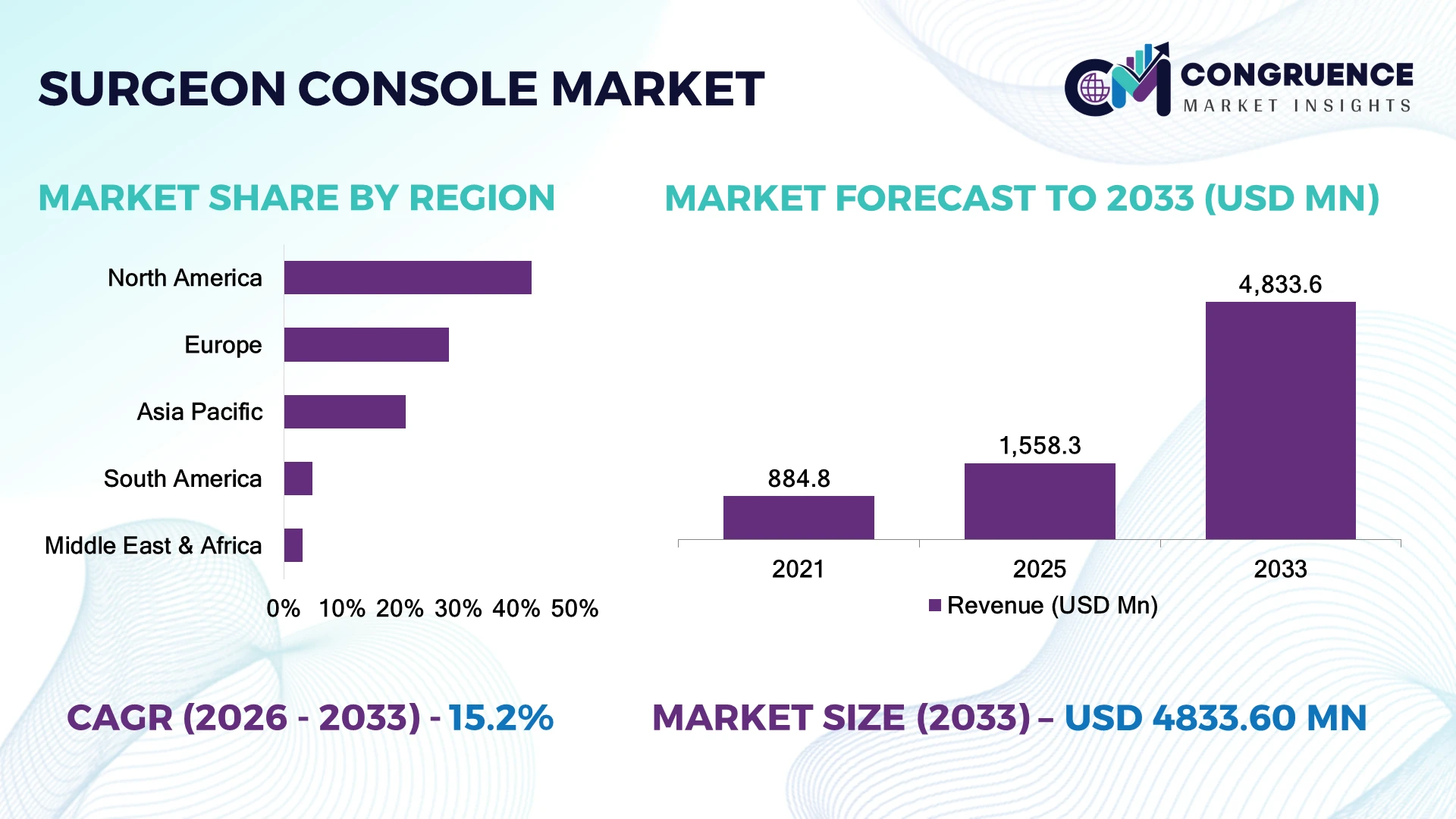

The Global Surgeon Console Market was valued at USD 1,558.3 Million in 2025 and is anticipated to reach a value of USD 4,833.6 Million by 2033 expanding at a CAGR of 15.2% between 2026 and 2033. Rising robotic-assisted surgical procedures, expanding hospital investments in digital operating rooms, and increasing regulatory approvals for next-generation surgical robotics are accelerating surgeon console adoption.

The United States leads the global market with approximately 46% share, supported by over 1,900 robotic surgery installations, strong investment in tertiary healthcare infrastructure, and widespread adoption across urology, gynecology, and general surgery. Compared with Japan, where robotic-assisted procedures represent nearly 18% of minimally invasive surgeries, the United States exceeds 39%, reinforced by healthcare modernization initiatives despite continued global medical device supply-chain realignment.

Healthcare providers investing in AI-enabled, ergonomically advanced surgeon consoles with scalable robotic platforms will secure stronger procedural efficiency and long-term clinical competitiveness.

Market Size & Growth: USD 1,558.3 Million (2025) to USD 4,833.6 Million (2033), CAGR 15.2%, driven by robotic surgery expansion.

Top Growth Drivers: Robotic procedures +24%, hospital automation +18%, minimally invasive surgeries +21%.

Short-Term Forecast: By 2028, console workflow efficiency improves 17% through AI-assisted visualization.

Emerging Technologies: AI guidance, 3D visualization, digital twin planning improve surgical precision.

Regional Leaders: North America leads; Europe and Asia-Pacific accelerate through hospital modernization and robotics investment.

Consumer/End-User Trends: Nearly 63% of tertiary hospitals prioritize robotic surgery platform expansion.

Pilot/Case Example: 2025 digital operating room deployment reduced average procedure setup time by 19%.

Competitive Landscape: Leading vendors control approximately 68% share through integrated robotic ecosystems.

Regulatory & ESG Impact: Digital operating room initiatives reduce disposable instrument waste by nearly 12%.

Investment & Funding: Hospital robotic infrastructure investment exceeds USD 2.5 billion globally, supporting expansion.

Innovation & Future Outlook: AI-assisted decision support and haptic feedback redefine advanced robotic surgery platforms.

The Surgeon Console Market is evolving through AI-assisted visualization, haptic feedback systems, and cloud-enabled surgical workflow integration. Demand is strongest across tertiary hospitals, ambulatory surgical centers, and academic medical institutions. Nearly 44% of new robotic surgery procurements prioritize advanced console ergonomics and intelligent imaging, while healthcare supply-chain localization is improving equipment availability, setting the foundation for the strategic outlook below.

Surgeon consoles have become a strategic investment category as healthcare providers compete to expand robotic-assisted surgery capacity, improve surgical precision, and increase operating room productivity. Digital operating room modernization, strengthened medical device regulations, and growing adoption of image-guided procedures are reshaping procurement priorities. Hospitals increasingly evaluate complete robotic ecosystems rather than standalone surgical equipment, creating stronger demand for integrated surgeon console platforms.

Modern AI-assisted consoles improve workflow efficiency by approximately 22% compared with conventional robotic interfaces while reducing surgeon fatigue through ergonomic controls and enhanced visualization. North America leads in installed robotic surgery infrastructure, whereas Asia-Pacific records faster deployment through hospital expansion and domestic medical technology manufacturing. More than 58% of newly commissioned robotic operating rooms now include advanced digital visualization and real-time surgical analytics.

Healthcare providers increasingly deploy surgeon consoles alongside integrated imaging, navigation, and robotic instrumentation platforms. Manufacturers are expanding partnerships with hospitals, investing in software upgrades, and strengthening surgeon training programs to improve utilization rates. Organizations that combine intelligent console technology, scalable robotic platforms, and clinical workflow optimization will establish sustainable competitive advantages as robotic surgery continues transforming modern healthcare delivery.

Expanding robotic-assisted surgical programs across tertiary hospitals and specialty care centers remain the primary driver for surgeon console adoption. Nearly 64% of newly commissioned robotic operating rooms now incorporate next-generation surgeon consoles with integrated 3D visualization, while AI-assisted workflow optimization improves procedural efficiency by approximately 21% and reduces console transition time by nearly 17%. The United States continues strengthening reimbursement support for minimally invasive robotic procedures, encouraging hospitals to modernize surgical infrastructure. This shift improves operating room utilization and clinical precision. Manufacturers are responding through AI-enabled console development, ergonomic interface innovation, strategic hospital partnerships, and investment in modular robotic platforms that support multiple surgical specialties, creating long-term competitive differentiation through scalable digital surgery ecosystems.

Surgeon console deployment remains constrained by substantial capital expenditure, maintenance costs, and specialized training requirements. Initial robotic surgery platform investments account for nearly 72% of total procurement expenditure, while annual maintenance contracts increase lifecycle operating costs by approximately 14%. India and several emerging healthcare markets continue facing budget limitations that delay widespread robotic surgery adoption despite growing clinical demand. These financial barriers restrict deployment across mid-sized hospitals and independent surgical centers while extending procurement cycles. Medical technology providers are mitigating these constraints through leasing models, local manufacturing initiatives, long-term service agreements, and shared robotic surgery programs that reduce acquisition risk while improving equipment affordability and operational scalability.

Artificial intelligence, digital visualization, and cloud-connected surgical analytics are creating significant opportunities for next-generation surgeon consoles. Around 58% of leading hospitals plan to integrate AI-assisted intraoperative guidance into robotic surgery workflows, while intelligent decision-support systems improve surgical planning efficiency by approximately 24%. South Korea continues expanding investment in smart hospital infrastructure and advanced medical robotics, accelerating demand for intelligent surgical platforms. Technology developers are strengthening software ecosystems, expanding R&D partnerships with healthcare institutions, and integrating real-time data analytics into surgeon consoles. A particularly valuable opportunity lies in interoperable console architectures capable of supporting multiple robotic systems, reducing infrastructure costs while improving long-term clinical flexibility.

Successful deployment increasingly depends on integrating surgeon consoles with imaging systems, robotic instruments, hospital information systems, and cybersecurity frameworks. Approximately 47% of healthcare providers continue operating mixed-generation surgical equipment, while interoperability challenges extend implementation timelines by nearly 19%. Germany's expansion of digitally integrated operating rooms highlights the need for standardized communication across robotic platforms and hospital infrastructure. These complexities directly influence system utilization, training efficiency, and long-term technology sustainability. Manufacturers must invest in standardized software interfaces, advanced cybersecurity, simulation-based surgeon education, and collaborative partnerships with hospitals to ensure consistent deployment quality and maximize clinical productivity across diverse healthcare environments.

AI-Assisted Surgical Guidance AI-powered visualization and workflow assistance are becoming standard features, with approximately 56% of newly installed robotic systems supporting intelligent intraoperative guidance. Automated workflow optimization reduces procedure preparation time by nearly 18%, improving operating room utilization. Manufacturers are expanding software capabilities and collaborating with healthcare providers to strengthen clinical decision support as hospitals accelerate digital operating room modernization.

Enhanced Console Ergonomics Advanced ergonomic console designs are reducing surgeon fatigue while improving procedural precision. Adjustable interfaces and immersive 3D visualization increase surgeon comfort by approximately 27% and improve console operating efficiency by nearly 16%. Healthcare providers increasingly prioritize clinician wellness alongside productivity, encouraging manufacturers to redesign operator interfaces and integrate personalized control configurations into premium robotic platforms.

Remote Training Ecosystems Digital simulation platforms and cloud-connected surgical education are transforming workforce development. Nearly 43% of robotic surgery training programs now incorporate virtual simulation, reducing hands-on onboarding time by approximately 22%. Hospitals are responding to skilled workforce shortages through collaborative training partnerships, enabling faster adoption of advanced surgeon consoles while maintaining procedural consistency across expanding robotic surgery programs.

Multi-Specialty Platform Expansion Hospitals increasingly deploy surgeon consoles supporting multiple clinical specialties instead of dedicated single-procedure systems. Shared robotic infrastructure improves equipment utilization by approximately 25% while lowering idle operating capacity by nearly 15%. Vendors are strengthening modular platform architectures, expanding compatible surgical instruments, and integrating software upgrades that extend system functionality without requiring complete hardware replacement.

Multi-specialty surgeon consoles accounted for approximately 61% of the market in 2025 owing to their ability to support multiple robotic procedures across urology, gynecology, general surgery, thoracic surgery, and colorectal surgery through a unified platform. Healthcare providers favor these systems because they maximize operating room utilization, improve return on capital investment, and simplify surgeon training across departments. Integrated 3D visualization, AI-assisted workflow optimization, and modular software upgrades further strengthen adoption. Manufacturers continue expanding compatibility with additional robotic instruments while investing in ergonomic console design and advanced visualization technologies to enhance clinical productivity.

Single-specialty surgeon consoles represent the fastest-growing segment, driven by increasing demand for highly optimized robotic systems in orthopedic, neurosurgical, cardiovascular, and ophthalmic procedures. Deployment within specialty hospitals has increased by approximately 18%, while procedure-specific optimization improves workflow efficiency by nearly 16%. Vendors are expanding specialty-focused software, clinical collaborations, and precision instrument portfolios, strengthening differentiation while enabling hospitals to deploy application-specific robotic surgery programs alongside versatile multi-specialty platforms.

Healthcare technology assessments published during 2025 indicate that hospitals increasingly prioritize modular robotic console platforms capable of supporting multiple specialties, reinforcing long-term utilization and infrastructure scalability.

General surgery represented approximately 34% of the surgeon console market in 2025 due to its broad procedural volume and expanding adoption of minimally invasive robotic techniques. Robotic platforms are widely deployed for colorectal, bariatric, abdominal, and gastrointestinal procedures where enhanced dexterity, precision, and visualization improve surgical outcomes. Urology and gynecology remain mature application segments with consistently high robotic utilization, while thoracic surgery continues benefiting from advanced imaging and improved instrument articulation. Manufacturers are enhancing application-specific software, surgeon education programs, and digital workflow integration to support broader procedural adoption.

Orthopedic surgery is emerging as the fastest-growing application segment as robotic navigation, AI-assisted planning, and real-time imaging become standard for joint reconstruction and musculoskeletal procedures. Adoption across orthopedic centers has increased by approximately 20%, while robotic guidance improves implant positioning accuracy by nearly 17%. Companies continue investing in navigation software, imaging integration, and procedure-specific robotic workflows, expanding robotic surgery beyond traditional soft-tissue applications and strengthening long-term platform utilization.

Industry findings released during 2025 show that robotic-assisted general surgery continues recording the largest annual procedure volume among hospital robotic surgery programs, supporting continued investment in advanced surgeon console technologies.

Hospitals accounted for approximately 76% of the surgeon console market in 2025 owing to large procedural volumes, integrated surgical infrastructure, and the financial capacity to invest in comprehensive robotic surgery platforms. Academic medical centers and tertiary hospitals remain primary adopters because they perform high-complexity procedures across multiple specialties while maintaining dedicated robotic surgery teams. Ambulatory Surgical Centers are the fastest-growing end-user segment, supported by increasing outpatient robotic procedures and workflow optimization. Specialty clinics continue expanding robotic capabilities for focused clinical applications. Manufacturers target these buyers through flexible financing, clinical partnerships, customized service contracts, and integrated training ecosystems that strengthen long-term equipment utilization.

Demand from Ambulatory Surgical Centers has grown by approximately 21%, while hospitals continue improving robotic operating room utilization by nearly 18% through multi-specialty scheduling and digital workflow integration. Vendors are expanding cloud-enabled service platforms, predictive maintenance capabilities, and modular console upgrades that support operational scalability across diverse healthcare environments. Investment priorities increasingly favor interoperable systems capable of supporting future software enhancements without replacing installed hardware.

Healthcare technology surveys released during 2025 indicate that large hospitals continue performing the overwhelming majority of robotic-assisted surgical procedures, while outpatient robotic surgery programs are expanding rapidly through specialized ambulatory surgical centers.

North America accounted for the largest market share at 42.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.1% between 2026 and 2033.

Advanced Robotic Surgery Infrastructure Strengthens Clinical Leadership

North America remains the leading regional market due to extensive robotic surgery deployment across tertiary hospitals, continuous capital investment, and widespread integration of digital operating rooms. The region contributed approximately 42.6% of global demand in 2025, supported by mature reimbursement frameworks and rapid adoption of AI-assisted surgical platforms. More than 72% of high-volume academic hospitals have established dedicated robotic surgery programs, while multi-specialty console utilization continues expanding. Medical device companies are strengthening surgeon training centers, expanding software-enabled service platforms, and investing in next-generation console ergonomics. Hospital partnerships and integrated digital workflow deployments continue improving operating room productivity while supporting broader adoption across outpatient surgical facilities.

United States Market Outlook: The United States leads the regional market through its extensive installed robotic surgery base, advanced medical technology ecosystem, and continuous investment in minimally invasive procedures. Approximately 78% of robotic-assisted surgeries within North America are performed in the country, supported by strong clinical research activity, experienced robotic surgeons, and ongoing adoption across community hospitals. Expansion of ambulatory robotic surgery, AI-assisted surgical planning, and hospital modernization initiatives continues reinforcing national leadership while accelerating procurement of next-generation surgeon consoles.

Clinical Standardization Accelerates Robotic Surgery Expansion

Europe continues expanding robotic surgery through hospital modernization, standardized clinical protocols, and increasing adoption of minimally invasive procedures across public healthcare systems. The region accounted for approximately 28.4% of global demand in 2025, supported by rising investments in surgical robotics and cross-border clinical collaborations. Nearly 61% of newly commissioned robotic operating suites now incorporate integrated digital visualization and surgeon console technologies. Manufacturers continue strengthening regional distribution, clinical education partnerships, and service capabilities while improving interoperability between robotic systems and hospital information platforms.

Germany Market Outlook: Germany represents the largest European market owing to its advanced hospital infrastructure, strong medical device manufacturing capabilities, and rapid adoption of robotic-assisted surgery within university hospitals. Robotic surgical installations across major clinical centers continue increasing, with procedure volumes rising by approximately 16% over recent deployment cycles. Continuous investment in precision surgery, clinician training, and digital healthcare infrastructure positions Germany as the primary innovation hub for advanced surgeon console adoption.

Healthcare Capacity Expansion Fuels Large-Scale Deployment

Asia-Pacific is emerging as the fastest-growing regional market as governments expand advanced surgical infrastructure, increase healthcare investment, and strengthen domestic medical technology manufacturing. The region represented approximately 20.9% of global demand in 2025 while recording rapid deployment across metropolitan hospitals. Installation of robotic surgery platforms has increased by nearly 24% across leading healthcare institutions, supported by modernization initiatives and growing procedural volumes. International manufacturers continue expanding regional production, distribution partnerships, and localized surgeon training programs to improve market penetration and reduce deployment timelines.

China Market Outlook: China leads regional expansion through substantial healthcare infrastructure investment, rapidly growing robotic surgery adoption, and strengthening domestic medical device manufacturing. Large tertiary hospitals continue expanding robotic operating rooms, while local technology developers increasingly collaborate with healthcare providers to commercialize next-generation surgical platforms. Robotic surgical procedure capacity has increased by approximately 22% across major urban hospitals, reinforcing China's strategic importance for future surgeon console deployment and manufacturing scale.

Private Healthcare Investment Supports Robotic Adoption

South America is witnessing gradual expansion of surgeon console deployment as private hospital groups prioritize minimally invasive surgery and advanced operating room modernization. The region accounted for approximately 4.9% of global demand in 2025, with adoption concentrated in large metropolitan healthcare networks. Robotic surgical procedures have increased by nearly 15% across premium healthcare providers, although infrastructure availability and equipment financing continue limiting broader implementation. Manufacturers are responding through distributor partnerships, surgeon education initiatives, and flexible financing models that improve accessibility while supporting long-term market development.

Brazil Market Outlook: Brazil remains the region's largest market due to its expanding private healthcare sector, advanced hospital networks, and growing investment in robotic-assisted surgery. Leading hospitals continue increasing robotic procedure capacity while strengthening surgeon certification programs and multidisciplinary robotic surgery centers. Hospital investment in advanced surgical technologies has increased by approximately 17%, positioning Brazil as the principal growth engine for surgeon console deployment across South America.

Healthcare Modernization Drives Premium Technology Adoption

The Middle East & Africa market is advancing through strategic healthcare modernization, specialty hospital expansion, and government-backed investment in advanced surgical technologies. The region represented approximately 3.2% of global demand in 2025, with deployment concentrated in high-capacity healthcare systems. Investment in digitally integrated operating rooms has increased by nearly 19%, enabling wider implementation of robotic-assisted surgery across flagship medical institutions. International manufacturers continue strengthening regional service networks, clinical partnerships, and physician training programs to accelerate adoption while supporting long-term infrastructure development.

Saudi Arabia Market Outlook: Saudi Arabia leads regional deployment through large-scale healthcare transformation initiatives, construction of advanced medical facilities, and increasing investment in robotic surgery capabilities. Major referral hospitals continue integrating sophisticated surgeon consoles with digital operating room infrastructure while expanding specialist training programs. Robotic-assisted surgical capacity has grown by approximately 18% across leading healthcare institutions, strengthening the country's position as the primary regional market for next-generation surgical robotics.

The surgeon console market is led by Intuitive Surgical, while Medtronic, CMR Surgical, Johnson & Johnson MedTech, and SS Innovations compete through differentiated robotic platforms, regional expansion, and workflow innovation. The top five participants collectively control approximately 86% of global market activity, reflecting high technological concentration. Competition centers on console ergonomics, imaging precision, AI-assisted navigation, instrument dexterity, and service ecosystems, with advanced platforms improving surgical workflow efficiency by nearly 28% and reducing console setup time by approximately 18%. Global leaders compete against emerging innovators through hospital partnerships, surgeon training networks, software upgrades, and vertical integration spanning instruments, visualization, and digital services. The competitive landscape is shifting toward intelligent consoles with real-time analytics, force feedback, and cloud-enabled performance monitoring rather than hardware alone. High regulatory requirements, clinical validation, surgeon training, and installed-base loyalty remain significant entry barriers. Winning requires integrated robotic ecosystems, continuous software innovation, strong clinical evidence, and scalable post-installation service capabilities.

Intuitive Surgical

Medtronic

Johnson & Johnson MedTech

CMR Surgical

SS Innovations International

Asensus Surgical

Moon Surgical

Distalmotion

Medicaroid Corporation

MicroPort MedBot

Ronovo Surgical

Virtual Incision Corporation

Surgeon consoles are rapidly evolving from mechanical control interfaces into intelligent surgical command platforms integrating AI-assisted visualization, force feedback, advanced ergonomics, and real-time analytics. Approximately 68% of newly installed robotic surgery systems now incorporate AI-supported image enhancement or workflow assistance, while force-feedback technologies improve tissue handling precision by nearly 24%. Cloud-connected software updates and digital procedure analytics are strengthening operational efficiency and reducing maintenance complexity across high-volume surgical centers.

Next-generation consoles outperform conventional systems through high-performance processors, immersive 3D visualization, digital workflow integration, and adaptive instrument control. Compared with legacy platforms, modern AI-enabled consoles reduce surgeon workflow interruptions by approximately 31% while improving procedural efficiency by nearly 22%. Adoption of digital training simulators has exceeded 57% among leading academic hospitals, providing measurable improvements in surgeon proficiency and shorter learning curves. Technology leaders with integrated robotics ecosystems benefit most through recurring software upgrades, analytics services, and expanded clinical capabilities.

Between 2026 and 2028, intelligent automation, augmented reality guidance, digital twins, and predictive maintenance will reshape competitive positioning. More than 46% of hospitals evaluating robotic surgery upgrades are prioritizing software-expandable consoles over fixed-function hardware. Vendors investing in interoperable platforms, cybersecurity, remote collaboration, and AI-assisted decision support will strengthen long-term differentiation while reducing operating costs and accelerating global deployment across complex surgical specialties.

March 2024 Intuitive Surgical received U.S. FDA clearance for the da Vinci 5 robotic surgical system featuring more than 150 platform enhancements and first-of-its-kind force feedback technology, strengthening next-generation surgeon console capabilities and hospital adoption. Source: Intuitive Surgical

July 2025 Intuitive Surgical secured CE Mark approval for the da Vinci 5 across Europe after supporting more than 410,000 European robotic procedures during 2024, significantly expanding commercial deployment opportunities for advanced surgeon consoles. Source: Intuitive Surgical Investor Relations

May 2026 Intuitive Surgical introduced over 100 software and usability enhancements for da Vinci 5, including telepresence improvements and secure mobile console login, reinforcing surgeon productivity, remote collaboration, and digital operating room integration. Source: Intuitive Surgical News

July 2024 Intuitive Surgical reported accelerated market rollout of da Vinci 5 following strong surgeon adoption, with improved ergonomics and visualization driving faster-than-expected customer acceptance and reinforcing competitive leadership. Source: MedTech Dive.

This report delivers comprehensive analysis of the surgeon console market across console type, surgical specialty, end-user, and major geographic regions. It evaluates adoption patterns across hospitals, ambulatory surgical centers, and academic institutions while examining robotic surgery integration, AI-assisted visualization, force-feedback systems, digital operating rooms, simulation technologies, and cloud-enabled surgical platforms. The study also assesses deployment trends, procurement strategies, platform interoperability, and evolving technology priorities influencing purchasing decisions.

The report profiles leading manufacturers, covering approximately 85% of established commercial activity while analyzing competitive positioning, product innovation, regional deployment intensity, and partnership strategies. Strategic insights support investment planning, product development, market entry, expansion priorities, and competitive benchmarking between 2026 and 2033 through detailed assessment of technology evolution, clinical adoption, regulatory developments, and emerging opportunities across established and rapidly expanding robotic surgery markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,558.3 Million |

|

Market Revenue in 2033 |

USD 4,833.6 Million |

|

CAGR (2026 - 2033) |

15.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Intuitive Surgical, Medtronic, Johnson & Johnson MedTech, CMR Surgical, SS Innovations International, Asensus Surgical, Moon Surgical, Distalmotion, Medicaroid Corporation, MicroPort MedBot, Ronovo Surgical, Virtual Incision Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |