Reports

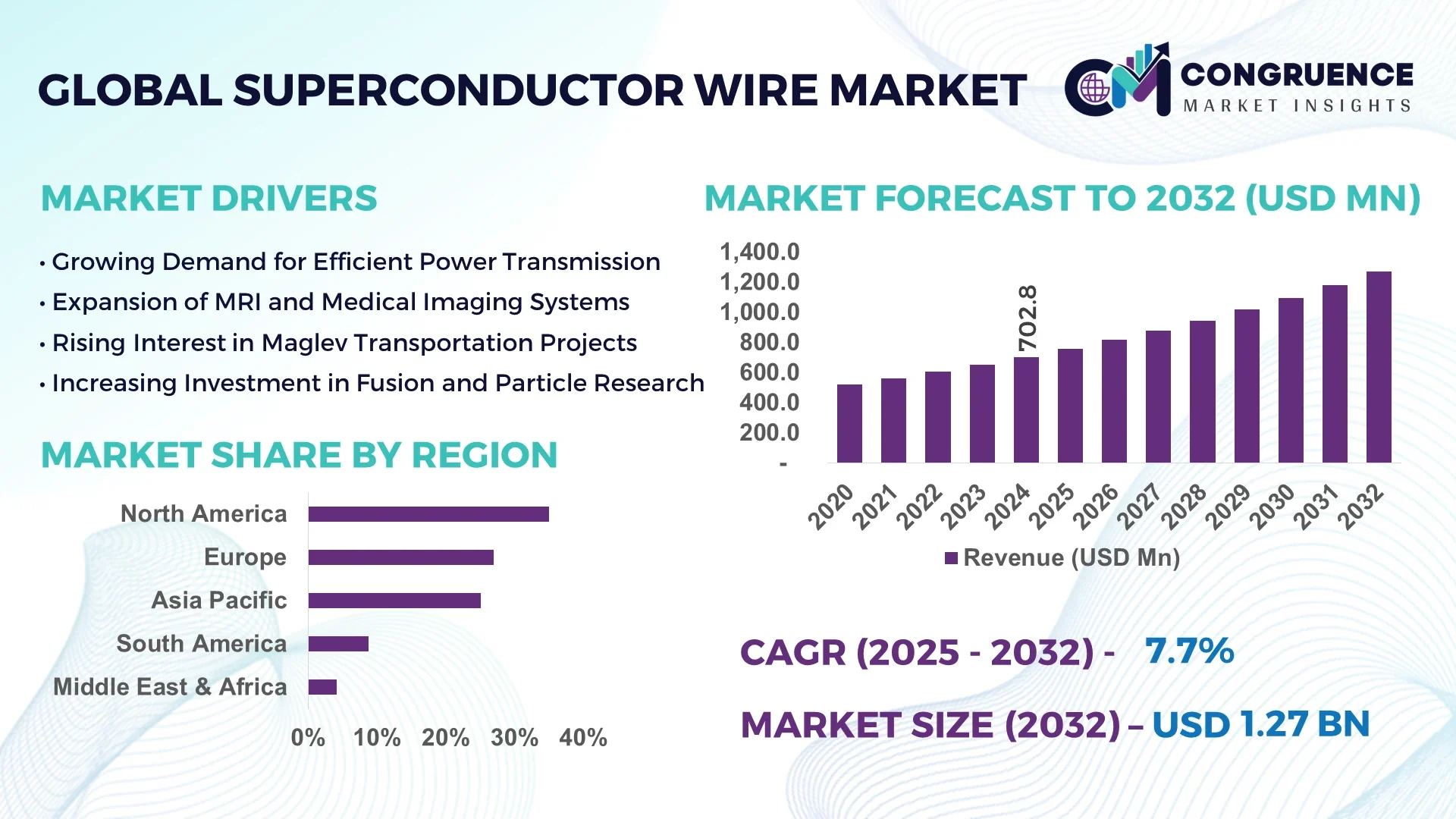

The Global Superconductor Wire Market was valued at USD 702.8 Million in 2024 and is anticipated to reach a value of USD 1272.2 Million by 2032, expanding at a CAGR of 7.7% between 2025 and 2032.

The United States is a dominant player in the Superconductor Wire Market, driven by substantial investments in research and development, especially in the energy and medical sectors. The growing demand for advanced materials in these fields has further amplified the need for superconducting materials and wires in the region.

The Superconductor Wire Market has seen significant advancements over the past few years, particularly due to the increasing adoption of high-temperature superconductors (HTS). These wires are used in power applications such as energy transmission, magnetic resonance imaging (MRI) systems, and particle accelerators. The shift from low-temperature superconductors (LTS) to HTS technology has resulted in a surge of investments from both private and government sectors. Furthermore, the development of innovative techniques to reduce production costs and improve the efficiency of these wires is driving the market forward. As global power consumption increases, superconducting wire technologies are gaining traction for their potential to reduce energy loss in transmission lines, making them increasingly important for future grid networks. This market is also benefiting from the rising demand for medical applications, such as MRI and other diagnostic equipment, where superconducting wires are essential for producing strong magnetic fields.

Artificial Intelligence (AI) is rapidly transforming the Superconductor Wire Market, influencing both the development and optimization of superconductor wire manufacturing processes. AI technologies are being integrated into the design and production stages of superconductor wire to enhance efficiency, reduce costs, and improve material properties. Through machine learning algorithms and data analytics, manufacturers are now able to predict material behaviors, optimize wire compositions, and develop more efficient production methods. AI is especially critical in the discovery of new superconducting materials that can operate at higher temperatures, a key factor driving the market's growth.

Additionally, AI-powered simulations help in testing the performance of superconducting wires before physical prototypes are created, reducing the need for expensive trial-and-error processes. The precision of AI models is helping to push the boundaries of wire capacity and performance, allowing for more energy-efficient systems. AI is also being utilized to monitor the quality control of wires during the manufacturing process, detecting inconsistencies in real-time, which significantly reduces defects and production downtime. These advances are making superconducting wires more accessible and cost-effective, driving adoption in various industries including power transmission, medical technology, and transportation systems, where superconductivity can lead to significant improvements in performance and energy efficiency.

"In 2024, a leading research institute announced the development of AI-based algorithms designed to optimize the properties of high-temperature superconducting wires, making them more suitable for use in energy grids."

The Superconductor Wire Market is being significantly influenced by various dynamics that are shaping its growth. These dynamics are primarily driven by technological advancements, the expanding demand for high-performance energy solutions, and the increasing applications in medical technology. As the need for more efficient energy transmission grows globally, superconducting wires are emerging as a promising solution due to their minimal energy loss. Additionally, advancements in manufacturing processes, such as the development of high-temperature superconductors, are allowing for a broader range of applications, from power grids to MRI systems. The market is also benefiting from government policies and incentives promoting the use of energy-efficient technologies.

Superconducting wires play a crucial and increasingly strategic role in modern energy transmission systems, as they significantly reduce power losses that typically occur during the transportation of electricity over long distances. The growing global demand for energy-efficient, high-performance power grids is a major driver behind the increasing adoption of superconducting wire technologies. Traditional power grids often suffer from substantial transmission losses due to resistance in conventional conductors, making superconducting wires a highly viable and attractive alternative for enhancing grid efficiency and reliability. As more countries prioritize upgrading their aging energy infrastructure, several have launched pilot projects and national initiatives to integrate superconducting cables into their existing energy networks. The pressing need for efficient electricity delivery in densely populated urban centers and across expansive geographic regions further amplifies the demand. Moreover, in the context of global climate goals and the ongoing energy transition, governments and regulatory bodies are acknowledging the transformative potential of these technologies and are offering financial, policy, and research support to accelerate their deployment.

Despite the clear technological and environmental advantages, the high production and installation costs associated with superconducting wires remain a considerable restraint limiting wider market adoption. The materials required for manufacturing superconducting wires such as yttrium, bismuth, and other rare-earth elements are both costly and subject to fluctuating availability. Additionally, the intricate and highly specialized production processes, which often involve complex layering and cooling systems, drive up overall manufacturing expenses. Installation costs can also be prohibitive, especially when integrating superconducting systems into existing infrastructure not originally designed for such technologies. The required cryogenic support systems further add to operational and maintenance costs. While long-term benefits in efficiency and performance are substantial, the significant upfront capital investments needed to implement superconducting wire systems can deter utilities and industrial users from adopting them on a large scale. The current lack of industry-wide standardization in production and implementation practices adds another layer of complexity and cost, creating barriers to scalability and broader commercial viability.

As the global energy landscape rapidly shifts toward sustainable and renewable sources such as wind, solar, and hydroelectric power, a substantial opportunity is emerging for superconducting wires to play a pivotal role in enhancing the overall efficiency, capacity, and reliability of these systems. Superconductors are particularly valuable in the context of renewable energy because they enable virtually lossless energy transmission and offer improved energy storage capabilities, both of which are critical for the stability and scalability of renewable networks. By integrating superconducting materials into solar and wind farms, energy providers can facilitate long-distance transmission of clean power with minimal energy loss, addressing one of the key technical limitations of renewables. This is especially important for transmitting electricity generated in remote areas, such as offshore wind farms, to urban consumption centers. Furthermore, as national governments and international organizations intensify their support for decarbonization through policy initiatives and funding programs, the role of superconducting technologies in enabling next-generation, resilient energy systems becomes even more significant, positioning the market for robust growth.

One of the most pressing challenges facing the superconductor wire market is the limited availability of essential raw materials, particularly rare-earth elements and other specialized compounds critical to the production of high-performance superconductors. These materials are not only scarce but also geographically concentrated in a few regions, making the supply chain vulnerable to geopolitical tensions, trade restrictions, and environmental regulations. The price volatility and uncertain availability of these inputs can significantly affect production planning and overall cost structures for manufacturers. Moreover, the extraction, processing, and refinement of these materials often involve environmentally damaging practices and raise ethical concerns related to labor conditions and ecological degradation. These issues can negatively influence public perception and limit adoption, especially in regions with stringent environmental compliance standards. Addressing this challenge will require the development of alternative materials, improved recycling processes, and a more resilient global supply chain to ensure the long-term sustainability, affordability, and scalability of superconducting wire technologies.

• Technological Advancements in Superconducting Materials: The demand for high-performance superconducting wires has increased due to the development of new materials that allow superconductors to operate at higher temperatures. Innovations in high-temperature superconductors (HTS) have expanded the potential for these wires in practical applications, particularly in power grids and transportation systems. As research continues, improvements in material properties are allowing superconducting wires to be more widely used in energy-efficient solutions, reducing transmission losses in power systems.

• Increased Adoption in Medical Imaging and Diagnostics: Superconducting wires are increasingly being used in medical imaging equipment, such as MRI machines, due to their ability to generate strong magnetic fields with minimal energy loss. This trend is expanding in both developed and emerging markets, where the demand for advanced healthcare technologies is rising. The market for superconducting wires in medical applications is expected to continue growing as hospitals and diagnostic centers adopt more efficient and powerful imaging technologies, improving patient care.

• Integration into Smart Grids and Renewable Energy Networks: With the global shift towards sustainable energy, superconducting wires are being integrated into smart grids and renewable energy networks. These wires help to efficiently transmit electricity generated by renewable sources, such as solar and wind, over long distances with minimal energy loss. This trend is particularly significant in countries looking to transition to greener energy solutions, supporting the growth of superconducting wire technologies in the energy sector.

• Government Support and Investment in Energy Efficiency: Governments around the world are investing in energy-efficient technologies, including superconducting wires, as part of their efforts to reduce greenhouse gas emissions and improve energy infrastructure. National and international initiatives are providing funding for research and development in superconducting wire technologies, further driving innovation and commercial adoption. This trend is particularly evident in countries with aggressive renewable energy targets, where superconductors are being used to improve grid efficiency and enable the large-scale deployment of clean energy solutions.

The Superconductor Wire Market is segmented by type, application, and end-user insights. In terms of type, the market is divided into high-temperature superconductors (HTS) and low-temperature superconductors (LTS), with HTS being the fastest-growing segment due to their higher operational efficiency. For applications, the market includes power transmission, medical devices, and transportation, among others, with power transmission leading in terms of demand, driven by the need for efficient grid systems. The end-user insights segment includes industries such as energy, healthcare, and transportation, with the energy sector dominating, owing to the push for energy-efficient technologies. Each segment has distinct dynamics, but overall, the shift toward renewable energy and advanced medical technologies is fueling growth across all categories.

The Superconductor Wire Market is primarily segmented into high-temperature superconductors (HTS) and low-temperature superconductors (LTS). HTS wires are the fastest-growing segment due to their ability to operate at higher temperatures, reducing the need for costly and complex cooling systems. This makes HTS wires ideal for large-scale applications such as power grids, MRI machines, and maglev trains. The growth of renewable energy infrastructure, along with the demand for energy-efficient transmission solutions, is further driving the adoption of HTS wires. LTS wires, while still in demand for niche applications such as particle accelerators and medical equipment, are growing at a slower pace due to their reliance on expensive liquid cooling systems. HTS wires' ability to operate at higher temperatures with lower operational costs is expected to keep them as the dominant segment moving forward.

The Superconductor Wire Market is widely used across several key applications, including power transmission, medical devices, transportation, research, and electronics. Power transmission is the leading application segment, driven by the global push for more efficient energy grids and reducing energy losses. Superconducting wires offer an efficient solution to long-distance energy transmission, making them a critical component in modern power systems. The medical devices segment, especially MRI machines, is also significant, as superconducting wires are essential for generating strong magnetic fields used in medical imaging. Transportation, particularly in maglev trains, is the fastest-growing application, driven by advancements in high-speed trains and the increasing adoption of sustainable transport solutions. The research segment remains strong due to the use of superconducting wires in particle accelerators and experimental physics.

The Superconductor Wire Market serves multiple end-user industries, with the energy sector being the largest due to the increasing demand for efficient transmission and distribution systems. Superconducting wires are being integrated into power grids to reduce energy losses and improve the performance of electrical systems. The healthcare sector, driven by the need for advanced medical imaging technologies such as MRI, is another key end-user of superconducting wires. This sector is growing steadily as hospitals and diagnostic centers upgrade to more efficient equipment. The transportation sector is the fastest-growing end-user category, primarily due to the expanding use of superconducting wires in maglev trains, which are seen as the future of high-speed and energy-efficient transport. Other end-user industries, such as electronics and research, are also contributing to the market’s growth, though they represent smaller segments in comparison.

North America accounted for the largest market share at 35% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.5% between 2025 and 2032.

North America’s dominant position is largely driven by significant investments in energy infrastructure and medical technologies, while Asia-Pacific’s growth is propelled by the region's expanding industrial sectors and technological advancements. As demand for energy-efficient solutions continues to rise, countries in Asia-Pacific are increasingly adopting superconducting wire technologies in power transmission, transportation, and research applications. This dynamic growth in Asia-Pacific is set to surpass North America in the coming years, further shifting the global market landscape.

Powering the Future with Superconducting Innovation

North America remains the leading market for superconductor wires, contributing a substantial share due to its well-established industries in healthcare, energy, and transportation. The adoption of superconducting materials in medical imaging systems like MRI machines is robust, with hospitals and healthcare facilities upgrading to advanced technologies. In energy, the U.S. and Canada are investing in modernizing the electrical grid with high-efficiency superconducting cables. Furthermore, North America's advancements in renewable energy projects have accelerated the demand for superconducting wires in energy storage systems and power distribution, strengthening the region’s market position.

Leading the Charge in Sustainable Energy Solutions

Europe's superconductor wire market is witnessing steady growth, driven by increasing adoption in healthcare and energy sectors. Countries like Germany, France, and the UK are investing in smart grid technologies that incorporate superconducting wires to enhance energy efficiency. The healthcare industry in Europe is also expanding its use of MRI machines and other advanced diagnostic equipment, propelling the demand for superconducting wires. Furthermore, the European Union's commitment to sustainability and energy transition programs is further stimulating the growth of superconducting wires in power transmission, especially as the region seeks to reduce carbon emissions.

Accelerating Growth through Technological Advancements

Asia-Pacific is experiencing the fastest growth in the superconductor wire market, spurred by significant investments in infrastructure, renewable energy, and industrial applications. China and Japan are major players, focusing on large-scale power grids and high-speed maglev trains. The growing adoption of superconducting materials in industries such as transportation, healthcare, and energy is propelling the demand for superconductor wires. Furthermore, countries like South Korea and India are rapidly advancing their energy grids, which creates lucrative opportunities for superconductor wire technologies, boosting market dynamics in the region.

Emerging Potential Backed by Energy and Healthcare Developments

In South America, the superconductor wire market is relatively smaller but shows signs of gradual growth, driven by developments in energy and healthcare sectors. Brazil is leading the market, especially in research and development initiatives surrounding superconducting technology for power transmission and storage. The region’s focus on enhancing healthcare infrastructure also supports the demand for superconducting wires in medical imaging. As South American countries explore renewable energy options and develop more sustainable infrastructure, the use of superconducting wires is expected to expand, albeit at a slower pace compared to other regions.

Early Adoption Driven by Infrastructure Modernization and Energy Efficiency

The Middle East & Africa superconductor wire market is in the early stages of adoption, with key growth drivers being the energy sector and the push towards modernization in infrastructure. The UAE and Saudi Arabia are investing in renewable energy projects, and superconducting wires are gaining attention due to their ability to efficiently transmit energy over long distances with minimal loss. Additionally, the increasing demand for healthcare advancements in the region is fueling the use of superconducting materials in MRI and other diagnostic equipment. Despite the smaller market size, the Middle East & Africa region is gradually adopting these technologies.

United States – holds the largest share at 20% due to extensive investments in energy infrastructure and medical technologies, particularly MRI and power grid upgrades.

China – holds a significant market share at 18%, driven by the rapid expansion of renewable energy projects and the adoption of superconducting wires in power transmission and transportation systems.

The superconductor wire market is highly competitive, with several key players dominating the landscape. Leading companies are focused on innovations, collaborations, and strategic mergers to strengthen their market position. The market is characterized by ongoing technological advancements and the development of high-performance superconducting materials. Major players are investing heavily in R&D to offer superior products that cater to the growing demand for energy-efficient solutions across industries like healthcare, transportation, and power distribution. As new applications for superconducting wires emerge, companies are aiming to stay ahead of the competition through the development of advanced technologies, such as high-temperature superconductors. Strategic partnerships and investments in regional markets, particularly in the Asia-Pacific and North American regions, are key factors driving competition. Companies are also focusing on expanding their manufacturing capabilities to meet increasing demand, especially in sectors like renewable energy, where the need for efficient transmission and storage solutions is growing rapidly.

American Superconductor Corporation

Superconductor Technologies Inc.

Sumitomo Electric Industries

Fujikura Ltd.

Bruker Corporation

Southwire Company LLC

Showa Denko Materials Co., Ltd.

Oxford Instruments

Siemens AG

Technology plays a pivotal role in shaping the future of the superconductor wire market. Advancements in high-temperature superconductors (HTS) have revolutionized the industry by allowing for more efficient and cost-effective solutions in power transmission, transportation, and healthcare. HTS wires, which operate at higher temperatures compared to traditional superconductors, are being increasingly adopted in the power sector to improve the efficiency of electrical grids, reduce transmission losses, and integrate renewable energy sources. The development of second-generation (2G) HTS wires has also contributed to significant advancements in performance, with these wires offering better flexibility, higher critical current density, and a more manageable production process.

Moreover, innovations in cryogenic technologies are enhancing the performance of superconductor wires, making them more reliable and viable for large-scale applications. In healthcare, superconducting wires are used in MRI machines and particle accelerators, where their high conductivity and ability to operate at low temperatures are indispensable. As demand for sustainable and energy-efficient technologies rises, the ongoing technological advancements in superconducting wire manufacturing will continue to play a critical role in meeting global energy and healthcare demands.

In June 2023, AMSC secured a $200 million contract to supply high-temperature superconductor (HTS) wires for a large-scale power grid modernization project in the U.S.

In September 2023, Bruker Corporation announced the completion of its new superconductor wire manufacturing facility in Germany, increasing its production capacity by 30%.

In February 2024, Fujikura partnered with a leading European research institute to develop next-generation superconducting materials for fusion energy applications, with an initial funding of €50 million.

In October 2023, Sumitomo Electric unveiled its new high-performance superconducting cable system, which achieved a record-breaking current capacity of 5,000 amperes in testing.

The scope of the Superconductor Wire Market report includes a thorough analysis of the key segments, including types, applications, and end-users across various regions. It outlines the current market landscape and identifies factors that influence the growth trajectory of superconductor wire technologies. The report covers the market’s technological advancements, examining the impact of high-temperature superconductors (HTS) and their growing demand for energy applications like power grids and electric vehicles.

A detailed regional analysis highlights the market's performance in North America, Europe, Asia-Pacific, and other key regions, with particular focus on the United States and China, which are expected to lead the market due to large-scale adoption of superconducting technologies in power transmission and energy storage solutions.

The report provides a competitive overview of leading players in the superconductor wire market, offering insights into their business strategies, product launches, and partnerships. Moreover, the report includes a forecast of future trends, driven by growing investments in research and development aimed at improving the performance and efficiency of superconducting wires.

It also evaluates opportunities and challenges associated with the market, emphasizing innovations such as superconducting cables, fusion energy, and quantum computing, which are expected to revolutionize the industry. The comprehensive nature of this report makes it an essential tool for stakeholders aiming to navigate the evolving superconductor wire market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 702.8 Million |

|

Market Revenue in 2032 |

USD 1,272.2 Million |

|

CAGR (2025 - 2032) |

7.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

American Superconductor Corporation, Superconductor Technologies Inc., Sumitomo Electric Industries, Fujikura Ltd., Bruker Corporation, Southwire Company LLC, Showa Denko Materials Co., Ltd., Oxford Instruments, Siemens AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |