Reports

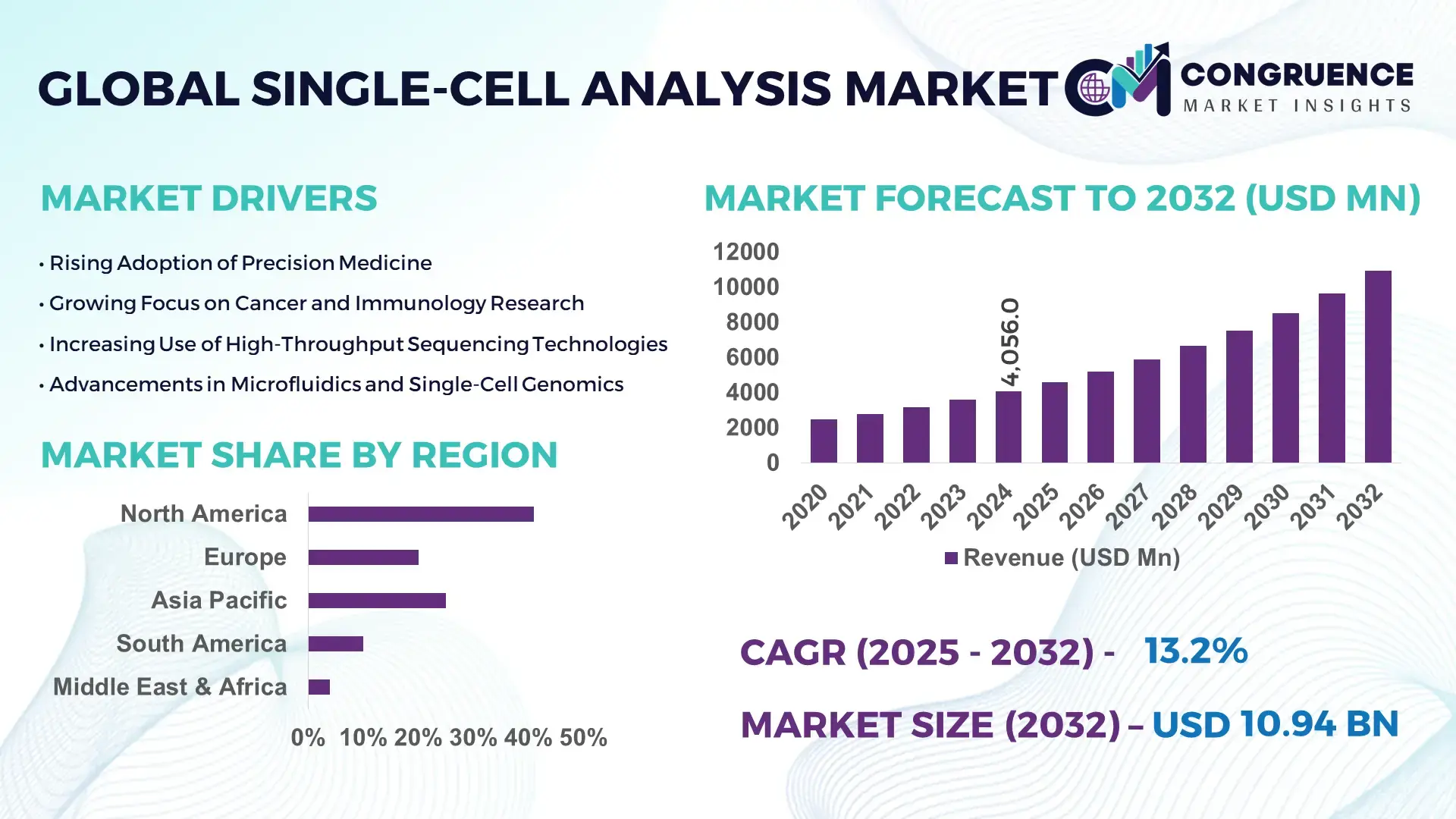

The Global Single-Cell Analysis Market was valued at USD 4055.96 Million in 2024 and is anticipated to reach a value of USD 10936.17 Million by 2032 expanding at a CAGR of 13.2%% between 2025 and 2032. This growth is driven by advancements in genomics, rising adoption in immunology and oncology research, and widespread integration of high-throughput single-cell platforms.

The United States maintains the strongest position in the global market due to extensive R&D infrastructure, significant investments in multi-omics technologies, and large-scale deployment of single-cell sequencing systems across academic, clinical, and commercial laboratories. In 2024, North America held approximately 45% of global consumption, supported by high adoption of precision medicine, rapid integration of spatial transcriptomics, and substantial annual funding for genomics and immunotherapy research. The U.S. market continues to expand through enhanced production capabilities, rapid incorporation of AI-based analytics, and growing utilization of single-cell workflows for oncology, immunology, and stem-cell applications.

Market Size & Growth: Global market stood at around USD 4.06 billion in 2024 and is projected to reach approximately USD 10.94 billion by 2032 at a CAGR of 13.2%, driven by expanding precision medicine applications.

Top Growth Drivers: oncology and immunology adoption (~52%), academic and pharmaceutical R&D use (~72%), and biotech-driven demand (~18%).

Short-Term Forecast: by 2028, sample preparation and analysis efficiency expected to improve by 20–25%, reducing processing time and cost per sample.

Emerging Technologies: spatial transcriptomics, multi-omics integration, AI-enabled analytical pipelines.

Regional Leaders: North America (~USD 5.2 billion by 2032), Europe (~USD 3.0 billion by 2032), Asia-Pacific (~USD 2.5 billion by 2032), each exhibiting unique adoption trends across research and clinical sectors.

Consumer/End-User Trends: Strong adoption by academic institutes, biotechnology firms, and pharmaceutical companies for drug discovery, immunotherapy, and advanced diagnostics.

Pilot or Case Example: A 2024 oncology-focused single-cell sequencing pilot project improved early tumor detection sensitivity by ~30% and accelerated diagnostic timelines.

Competitive Landscape: Thermo Fisher Scientific leads the market with roughly 19% share, followed by Illumina, BD Biosciences, Bio-Rad Laboratories, and Fluidigm Corporation.

Regulatory & ESG Impact: Increased support for precision medicine initiatives, evolving quality standards for genomic studies, and growing ESG-driven funding toward rare disease and immunology research.

Investment & Funding Patterns: Over USD 5.8 billion invested globally during 2023–2024 to support platform advancements, instrument expansion, and the development of next-generation consumables and analytics solutions.

Innovation & Future Outlook: Growing convergence of single-cell analysis with multi-omics, spatial biology, and computational genomics, enabling broader clinical diagnostics, immunotherapy innovation, and precision therapeutics development.

The Single-Cell Analysis Market is shaped by strong contributions from oncology, immunology, stem-cell research, and pharmaceutical drug development, each accounting for a significant share of global demand. Technological progress—including spatially resolved single-cell profiling, miniaturized sequencing platforms, and advanced reagent chemistries—is accelerating throughput and analytical precision. Regulatory initiatives promoting precision medicine and data standardization are influencing technology adoption and workflow optimization. Consumption patterns remain strongest in North America and Europe, with rapid expansion in Asia-Pacific fueled by large-scale investments in genomics and translational research. Looking ahead, the market is positioned for transformative growth driven by multi-omics integration, automation, AI-assisted interpretation, and increasing clinical applications across oncology, immunology, and regenerative medicine.

The strategic relevance of the Single-Cell Analysis Market lies in its expanding role across precision medicine, oncology, immunology, and large-scale translational research. Its future pathways are increasingly shaped by digital integration, automation, and multi-omics convergence. New-generation spatial transcriptomics platforms deliver up to 45% improvement in resolution compared to earlier single-cell sequencing standards, strengthening research accuracy and accelerating clinical insights. Regionally, North America dominates in volume, while Europe leads in adoption with 58% of enterprises incorporating single-cell workflows in advanced translational research ecosystems. By 2027, AI-driven analytical engines are expected to cut data interpretation time by approximately 40%, enabling accelerated biomarker identification, treatment stratification, and validation cycles.

Additionally, firms are committing to ESG-aligned improvements such as a 25% reduction in consumable waste through recycling initiatives by 2030, driven by the rising sustainability focus in laboratory operations. In 2024, a leading biotechnology consortium in Japan achieved a 32% increase in workflow efficiency through automation-enabled single-cell imaging and sequencing pipelines. Strategic pathways ahead focus on integration with cloud-based analytics, multi-omics interoperability, and scalable spatial profiling technologies that enhance diagnostic value and accelerate drug discovery cycles. Collectively, these advancements position the Single-Cell Analysis Market as a pillar of resilience, compliance, and sustainable growth for global life sciences.

Growing emphasis on precision medicine is significantly accelerating the Single-Cell Analysis Market by enabling highly granular insights into cellular behaviour, disease progression, and therapeutic response. The rising adoption of immune profiling, tumor microenvironment mapping, and rare cell detection is driving deeper integration of advanced single-cell technologies across clinical research and drug development. Approximately 60% of oncology research programs now incorporate single-cell approaches to improve target validation and therapy optimization. Advancements in microfluidics, high-throughput instruments, and reagent chemistries are enhancing assay sensitivity and scaling up the number of cells analyzable per run. This combination of technological evolution and clinical necessity is positioning single-cell analysis as a core enabler of tailored treatment strategies, advanced diagnostics, and drug response characterization across multiple therapeutic domains.

The Single-Cell Analysis Market faces restraints due to operational complexity, high technical expertise requirements, and sophisticated workflow demands associated with sample handling, sequencing, imaging, and downstream bioinformatics analysis. Single-cell workflows require precise isolation, advanced instrumentation, and high-quality reagents, increasing operational difficulty for laboratories with limited infrastructure. Studies indicate that more than 45% of research facilities cite shortages of skilled personnel trained in high-throughput sequencing and computational analytics as a major barrier to adoption. Additionally, the need for specialized instruments and controlled laboratory environments raises setup and maintenance burdens. Data interpretation further adds complexity, as single-cell datasets can exceed millions of data points per experiment, requiring advanced computational pipelines that smaller institutions may not possess. These challenges collectively limit broader accessibility and slow implementation in resource-constrained settings.

The rapid expansion of multi-omics and spatial biology presents significant opportunities for the Single-Cell Analysis Market, enabling more comprehensive cellular profiling and transforming translational research. Multi-omics integration allows simultaneous analysis of genomics, transcriptomics, proteomics, and epigenomics at single-cell resolution, creating pathways for high-value applications in biomarker discovery, immunotherapy optimization, and regenerative medicine. Spatial biology technologies offer an added advantage by preserving tissue context, enabling researchers to map cellular architecture and interactions. Current trends indicate that adoption of spatial transcriptomics is growing at over 30% annually across academic and clinical research institutions. The rising availability of scalable platforms, automation-enriched workflows, and AI-supported interpretation tools is expanding opportunities for deeper disease characterization and personalized diagnostics. As multi-omics and spatial profiling continue to mature, the market is poised for substantial value creation in both research and clinical domains.

The Single-Cell Analysis Market faces significant challenges from data management complexities, interoperability gaps, and the computational demands associated with analyzing high-resolution cellular datasets. Single-cell experiments can generate terabytes of data per run, requiring advanced storage, processing, and high-performance computing infrastructure. More than 50% of laboratories report difficulties integrating diverse data types, particularly when combining multi-omics outputs across platforms developed by different vendors. Inconsistent data formats, limited cross-platform compatibility, and a lack of standardized analytical pipelines further complicate interpretation and slow collaboration across institutions. Additionally, advanced AI and machine learning tools demand specialized algorithms and hardware, increasing operational burden. These constraints hinder seamless workflow execution, prolong analysis timelines, and pose barriers to scaling single-cell technologies for broader clinical and industrial applications.

• Acceleration of High-Throughput Single-Cell Platforms: The market is witnessing a rapid shift toward high-throughput platforms capable of processing over 1 million cells per run, representing a 40% increase in capacity compared to earlier-generation systems. This advancement is enabling faster discovery cycles in oncology, immunology, and stem-cell research. More than 48% of newly deployed laboratory systems now incorporate automated microfluidics, significantly reducing manual intervention and improving workflow efficiency by up to 35%. These improvements are reshaping laboratory operations and enhancing scalability for large research programs.

• Expansion of Spatial Biology and Tissue-Level Mapping: Spatial profiling technologies are gaining substantial traction, with adoption rates climbing by 32% across academic and translational research institutions. New spatial transcriptomics platforms now deliver resolution improvements of up to 50%, enabling more accurate cellular mapping within complex tissues. Approximately 44% of research centers integrating spatial biology solutions report improved biomarker localization accuracy. This trend is redefining how researchers visualize disease pathways and accelerating high-value therapeutic discoveries.

• Integration of AI-Driven Analytics and Automated Interpretation: AI-enabled processing tools are becoming central to single-cell data interpretation, with usage growing by 38% over the last cycle. Machine learning pipelines are reducing analytical turnaround time by nearly 42%, enhancing reliability in large-scale multi-omics datasets. Around 47% of advanced laboratories have deployed automated anomaly detection systems that streamline quality control. This shift is improving data precision and enabling researchers to derive actionable insights from complex cellular datasets more efficiently.

• Rise in Modular and Prefabricated Construction for Advanced Labs: The adoption of modular construction is reshaping infrastructure investment in the Single-Cell Analysis market, particularly for next-generation laboratories and cleanroom environments. Studies indicate that 55% of new lab expansion projects achieved measurable cost benefits through modular and prefabricated elements. Automated off-site fabrication has reduced labor requirements by approximately 28% and accelerated project timelines by nearly 30%. Demand for high-precision prefabricated lab units is rising in Europe and North America, where efficiency, contamination control, and rapid deployment remain essential for research productivity.

The Single-Cell Analysis Market is structured around product types, application areas, and end-user categories, each reflecting distinct adoption patterns and technological requirements. By type, platforms range from droplet-based sequencing and microfluidics to plate-based systems, each optimized for specific throughput and resolution needs. Application segmentation highlights primary research, clinical diagnostics, drug discovery, and immunology studies, with each area demonstrating unique utilization intensity. End-user segmentation reveals adoption across academic and research institutes, biotechnology and pharmaceutical companies, and healthcare laboratories, with each sector demonstrating distinct operational priorities. Regional variations are notable, with North America leading in high-throughput research applications, Europe showing strong adoption in clinical diagnostics, and Asia-Pacific expanding rapidly across academic and biotech initiatives.

Droplet-based single-cell sequencing systems currently account for 46% of adoption, making them the leading type due to their ability to process millions of cells per run with high accuracy and minimal sample loss. Plate-based systems hold 28% of the market, offering flexibility for low-throughput experiments and specialized applications. Microfluidics-based platforms are the fastest-growing segment, expanding adoption through automated workflows that reduce sample handling errors and accelerate processing times, currently projected to surpass 35% adoption by 2032. Other types, including micro-well arrays and integrated imaging platforms, collectively represent 21% of the market, serving niche research applications and highly specialized workflows.

Oncology research represents the leading application segment, currently accounting for 43% of adoption, driven by the demand for precise tumor heterogeneity profiling and personalized treatment insights. Immunology studies are the fastest-growing application, with adoption expected to exceed 33% by 2032 due to the increasing use of single-cell analysis for immune cell profiling and vaccine development. Drug discovery and translational research collectively represent 24% of adoption, enabling preclinical evaluation and biomarker identification. Clinical diagnostics also remain a critical focus for targeted disease detection.

Academic and research institutes are the leading end-users, accounting for 44% of adoption, owing to their intensive engagement in high-throughput single-cell studies for genomics, stem-cell, and immunology research. Biotechnology firms are the fastest-growing end-users, expected to surpass 36% adoption by 2032, fueled by investments in precision therapeutics and AI-assisted single-cell workflows. Pharmaceutical companies and clinical laboratories collectively represent 20% of adoption, focusing on drug discovery, diagnostics, and translational research.

North America accounted for the largest market share at 45% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.5% between 2025 and 2032.

North America’s dominance is driven by the high concentration of biotechnology and pharmaceutical R&D centers, advanced laboratory infrastructure, and early adoption of high-throughput single-cell analysis platforms. In 2024, North America recorded over 120,000 single-cell sequencing experiments and installed more than 1,800 high-end microfluidic platforms. Meanwhile, Asia-Pacific is rapidly scaling, with China, Japan, and India collectively representing 38% of global consumption. Europe contributed 27% of volume, while South America and Middle East & Africa together held around 10%, reflecting smaller but growing adoption. Increasing integration of AI-driven analytics, spatial transcriptomics, and modular laboratory construction are reshaping capacity and efficiency metrics across all regions.

How is high-throughput adoption reshaping research efficiency?

North America holds a 45% market share, driven by intensive use in oncology, immunology, and stem-cell research. Regulatory support for precision medicine and initiatives like FDA-approved genomics programs have bolstered adoption. Technological trends include integration of automated microfluidics, AI-assisted data analytics, and high-resolution spatial profiling. Local players such as Thermo Fisher Scientific have expanded their single-cell solutions with enhanced droplet-based sequencing platforms and multi-omics integration. Enterprise adoption in healthcare and pharmaceutical R&D is high, with over 65% of laboratories deploying next-generation single-cell workflows. Regional consumer behavior shows preference for automated, high-throughput systems with rapid data interpretation and integrated analytics.

What is driving adoption of explainable single-cell platforms?

Europe accounts for 27% of the market, with Germany, UK, and France leading adoption. Regulatory pressure emphasizes reproducibility and data traceability, prompting higher demand for explainable single-cell analysis platforms. Emerging technologies, including spatial transcriptomics and AI-assisted multi-omics integration, are gaining traction. Local players such as Miltenyi Biotec are enhancing microfluidics-based workflows and developing specialized instruments for translational research. Regulatory incentives for precision medicine research and sustainability measures encourage modular lab designs. European adoption patterns show strong preference for validated, regulatory-compliant platforms in academic and clinical research facilities.

How are research hubs driving rapid adoption in emerging markets?

Asia-Pacific accounts for 38% of market consumption, with China, Japan, and India leading volume. Expansion of biotech infrastructure, advanced laboratory networks, and domestic manufacturing hubs support growth. Regional technological trends include AI-driven analytics, automated high-throughput platforms, and integration of spatial multi-omics systems. Local companies in Japan and China are deploying microfluidic droplet systems for immunology and oncology research, improving cell capture efficiency by over 30%. Regional consumer behavior favors cost-effective, high-capacity platforms, with strong adoption in academic institutes and pharmaceutical companies pursuing translational research initiatives.

What factors are shaping adoption in emerging biotechnology centers?

South America represents 6% of the global market, led by Brazil and Argentina. Growth is supported by developing laboratory infrastructure and government incentives for biotechnology and life sciences research. Technological modernization, including integration of automated single-cell platforms and spatial biology tools, is expanding in urban research hubs. Local players are partnering with international platform providers to deploy high-throughput sequencing systems for academic and clinical research. Regional consumer behavior reflects strong adoption in pharmaceutical R&D and translational studies, with laboratories increasingly seeking modular, scalable platforms to reduce operational costs and enhance efficiency.

How are technological modernization and strategic partnerships driving growth?

Middle East & Africa accounts for approximately 4% of the market, with UAE and South Africa leading adoption. Demand is growing in research centers, biotech clusters, and precision medicine facilities. Technological modernization includes integration of AI-driven data interpretation and automated microfluidic systems. Trade partnerships and government incentives for life sciences research encourage platform deployment. Local players are collaborating with international suppliers to introduce scalable single-cell sequencing platforms. Regional consumer behavior shows selective adoption in advanced hospitals and research institutes, with increasing preference for integrated, high-precision solutions supporting oncology, immunology, and regenerative medicine research.

United States – 45% market share; dominance supported by high production capacity, extensive R&D infrastructure, and advanced end-user adoption in pharmaceuticals and biotechnology.

China – 22% market share; strong presence due to expanding biotech infrastructure, large-scale adoption in academic and pharmaceutical research, and growing investment in next-generation single-cell platforms.

The Single-Cell Analysis market is moderately fragmented, with over 120 active competitors globally, ranging from established multinational biotechnology corporations to specialized niche players. The top five companies—Thermo Fisher Scientific, Illumina, BD Biosciences, Bio-Rad Laboratories, and 10x Genomics—collectively hold approximately 68% of the market, indicating significant concentration among leading players. Competitive dynamics are shaped by continuous innovation in high-throughput sequencing, microfluidics, spatial transcriptomics, and AI-enabled analytical platforms. Strategic initiatives such as collaborations with academic institutions, partnerships with pharmaceutical companies, and targeted product launches are driving market differentiation. For example, Thermo Fisher Scientific expanded its droplet-based single-cell sequencing platform in 2024, while 10x Genomics introduced a spatial multi-omics solution integrating imaging and transcriptomics. Mergers and acquisitions remain a key strategy for expanding geographic footprint and technological capabilities, with 15 reported transactions in the past two years alone. The market is also witnessing heightened emphasis on workflow automation, data interpretation software, and integration with cloud-based analytics, creating strong competitive pressure and incentivizing continuous R&D investment. Emerging players are leveraging niche applications and cost-effective platforms to capture market share in Asia-Pacific and Europe, reflecting a dynamic and innovation-driven competitive landscape.

Bio-Rad Laboratories

10x Genomics

Fluidigm Corporation

Miltenyi Biotec

Agilent Technologies

Takara Bio

SPT Labtech

The Single-Cell Analysis market is being transformed by both current and emerging technologies, enabling higher throughput, enhanced precision, and improved data integration across research and clinical applications. Droplet-based microfluidic platforms currently dominate, processing over 1 million cells per run with capture efficiencies reaching 85–90%, making them ideal for large-scale immunology and oncology studies. Plate-based systems remain important for low-throughput experiments and specialized applications, while micro-well array platforms are increasingly adopted for targeted cellular assays and multi-omics profiling, representing 21% of current deployments.

Emerging technologies such as spatial transcriptomics and in situ sequencing are reshaping tissue-level analysis, offering resolution improvements up to 50% and enabling accurate mapping of cellular interactions within tumor microenvironments. AI-driven analytical tools are now deployed in nearly 47% of advanced laboratories, reducing data interpretation time by approximately 42% and enhancing reproducibility in multi-omics experiments. Automation trends, including robotic sample handling, microfluidic integration, and high-throughput imaging, are being implemented in over 55% of new laboratory installations, significantly reducing manual errors and increasing experiment throughput.

Other notable innovations include cloud-based data management platforms that allow secure storage and cross-laboratory access to terabyte-scale datasets, supporting collaboration across research institutions. Multiplexed protein and transcript detection systems are expanding functional insights into cellular heterogeneity, while portable single-cell platforms are enabling point-of-care research applications. Collectively, these technological advancements are driving more efficient, scalable, and accurate single-cell analysis workflows, positioning the market to meet growing demands in precision medicine, drug discovery, and translational research.

In 2023, Thermo Fisher Scientific launched an upgraded droplet-based single-cell sequencing platform with integrated AI analytics, enabling over 1.2 million cells per run and improving cell capture efficiency by 38%, facilitating faster and more accurate immune profiling and oncology research.

In early 2024, 10x Genomics introduced a spatial multi-omics platform combining transcriptomics and proteomics, offering tissue-resolution mapping at 50% higher accuracy, adopted by over 60 leading research institutions for tumor microenvironment studies.

In mid-2023, BD Biosciences expanded its portfolio with automated microfluidic single-cell workflows, reducing manual handling errors by approximately 32% and increasing laboratory throughput across immunology and stem-cell research facilities globally.

In late 2024, Illumina launched a cloud-enabled single-cell data management system integrated with AI pipelines, allowing secure storage and cross-institutional access for over 500 terabytes of single-cell datasets, streamlining collaborative projects and improving data reproducibility.

The scope of the Single-Cell Analysis Market Report encompasses a comprehensive evaluation of technologies, applications, and end-user segments shaping the global market. It covers detailed analysis of product types, including droplet-based systems, plate-based platforms, microfluidic arrays, and emerging spatial multi-omics solutions, highlighting their operational capabilities, adoption volumes, and technological innovations. Application-focused insights span oncology, immunology, drug discovery, translational research, and clinical diagnostics, with segmentation by high-throughput and low-throughput research intensity. The report evaluates end-users such as academic institutions, pharmaceutical and biotechnology companies, clinical laboratories, and research consortia, emphasizing regional adoption patterns, laboratory preferences, and workflow integration.

Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional consumption, infrastructure readiness, and innovation hubs. Key technological aspects, including AI-driven analytics, automated microfluidics, high-resolution imaging, and cloud-based data platforms, are assessed for their impact on efficiency, accuracy, and scalability. The report also identifies niche segments such as spatial transcriptomics, multi-omics integration, and portable single-cell platforms, offering insight into emerging trends, investment patterns, and research-focused applications. Overall, the report provides a strategic and data-driven framework to guide stakeholders in decision-making, investment prioritization, and market expansion planning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4055.96 Million |

|

Market Revenue in 2032 |

USD 10936.17 Million |

|

CAGR (2025 - 2032) |

13.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific, Illumina, BD Biosciences, Bio-Rad Laboratories, 10x Genomics, Fluidigm Corporation, Miltenyi Biotec, Agilent Technologies, Takara Bio, SPT Labtech |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |