Reports

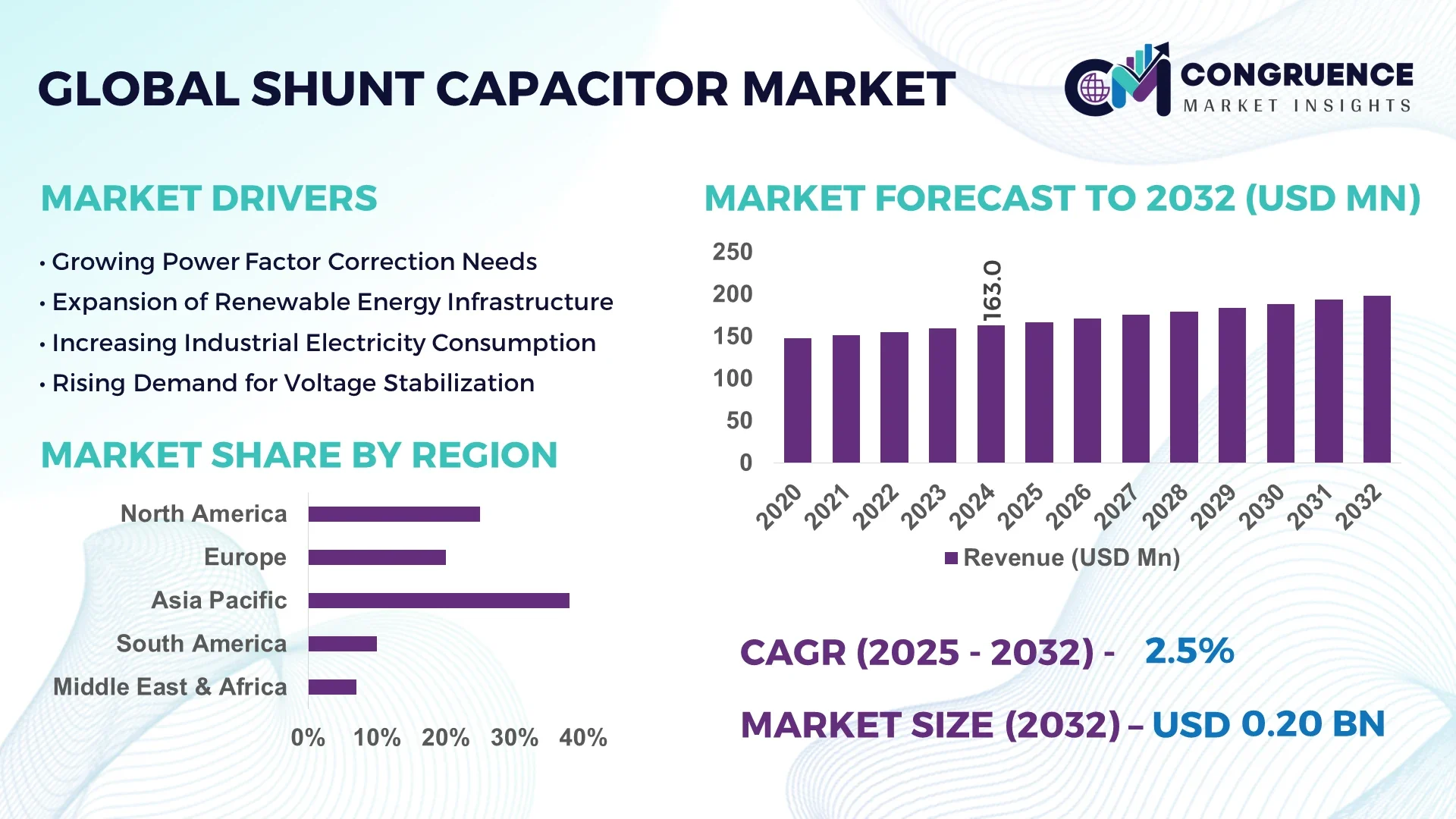

The Global Shunt Capacitor Market was valued at USD 163.0 Million in 2024 and is anticipated to reach USD 198.1 Million by 2032, expanding at a CAGR of 2.47% between 2025 and 2032. This growth is primarily driven by the increasing demand for power quality solutions across various sectors, driven by technological advancements, regulatory support, and the ongoing expansion of electrical infrastructure.

In China, the shunt capacitor market demonstrates significant scale, with installed capacities exceeding 450 MVAR across distribution networks by 2024. Approximately 50% of electric utilities in the country utilize shunt capacitor banks for power factor correction. Investment levels in grid modernization projects have surpassed USD 2.5 billion in the last two years, supporting technological advancements in self-healing capacitors and smart grid integration. Key applications include industrial manufacturing, renewable energy farms, and urban infrastructure projects, with adoption rates of 60% in industrial sectors and 40% in renewable installations.

Market Size & Growth: Valued at USD 163.0 million in 2024, projected to reach USD 198.1 million by 2032, with a CAGR of 2.47%. Growth driven by increasing demand for stable and efficient power distribution.

Top Growth Drivers: Integration of renewable energy sources (35%), urbanization and industrialization (30%), regulatory standards mandating power factor correction (25%).

Short-Term Forecast: By 2028, implementation of smart capacitor banks is expected to reduce downtime by 30% and enhance energy savings by up to 10%.

Emerging Technologies: Smart capacitor banks with IoT integration, self-healing capacitors, and high-voltage direct current (HVDC) technology.

Regional Leaders: Asia-Pacific: USD 1.2 billion by 2032, North America: USD 0.8 billion by 2032, Europe: USD 0.5 billion by 2032. Asia-Pacific leads in adoption, North America in volume.

Consumer/End-User Trends: Utilities and industrial sectors are primary consumers, increasingly adopting solutions in renewable energy projects and smart grids.

Pilot or Case Example: In 2024, a Chinese utility implemented smart capacitor banks, achieving a 28% reduction in energy losses and a 18% improvement in voltage stability.

Competitive Landscape: ABB Ltd. (25%), Siemens AG (20%), Schneider Electric SE (15%), Eaton Corporation Plc (10%), General Electric Company (10%).

Regulatory & ESG Impact: Regulations require power factor correction devices, including shunt capacitors, with incentives for energy-efficient infrastructure.

Investment & Funding Patterns: Investments focus on R&D for advanced materials and smart grid solutions, with increasing venture funding in emerging markets.

Innovation & Future Outlook: Advancements in capacitor design and materials are expected to improve performance and reduce maintenance costs, enhancing appeal for utilities and industrial users.

The shunt capacitor market is experiencing growth driven by power quality requirements, technological innovation, and infrastructure modernization. Increased deployment in industrial manufacturing, urban power networks, and renewable energy integration highlights its expanding strategic relevance.

The shunt capacitor market is strategically vital for maintaining voltage stability, reactive power compensation, and energy efficiency. With increasing renewable energy integration, maintaining grid reliability becomes critical, where shunt capacitors play an essential role. Adoption of smart capacitor banks with IoT-enabled monitoring delivers 20% improvement in operational efficiency compared to traditional systems.

China dominates in volume, while North America leads in adoption, with 60% of enterprises implementing shunt capacitor solutions. By 2028, smart grid integration is expected to reduce downtime by 30% and improve energy efficiency by 10%.

Companies are committing to ESG improvements, such as 20% reductions in greenhouse gas emissions and expanded recycling initiatives by 2030. In 2024, a leading Chinese utility achieved a 28% reduction in energy losses and 18% improvement in voltage stability using smart capacitor banks.

The Shunt Capacitor Market is positioned as a pillar of resilience, compliance, and sustainable growth, with technology adoption and regulatory support driving long-term prospects.

The shunt capacitor market is shaped by trends in technological innovation, regulatory frameworks, and demand for improved power quality. Advances in capacitor design and materials are producing more efficient and durable products. Expansion of electrical infrastructure, including smart grids, and the integration of renewable energy sources are driving the adoption of shunt capacitors across utilities, industrial, and urban sectors.

Renewable energy sources such as wind and solar introduce variability into the power grid. Shunt capacitors stabilize voltage levels and compensate for reactive power, ensuring reliable energy delivery. With renewable energy adoption increasing, demand for shunt capacitors rises to maintain grid stability.

High upfront costs can limit adoption, especially in developing regions. While long-term benefits such as energy efficiency and reduced maintenance justify investments, financial constraints may slow implementation without incentives or subsidies.

Smart grid technologies create opportunities for advanced shunt capacitors with real-time monitoring and control. These solutions optimize power factor correction, reduce energy losses, and enhance grid stability, expanding potential market adoption.

Integrating shunt capacitors into existing electrical networks requires planning, compatibility checks, and specialized expertise. Installation challenges and potential disruptions are key obstacles, though advancements in design and installation techniques are easing integration.

Rise in Modular and Prefabricated Construction: Modular construction practices are reshaping market demand. Approximately 55% of projects report cost savings with prefabricated components. Off-site pre-bent and cut elements reduce labor requirements and accelerate project timelines, especially in Europe and North America.

Increased Adoption of Smart Capacitor Banks: IoT-enabled smart capacitor banks adoption has risen 50%, improving predictive maintenance and grid reliability. Downtime has been reduced by 30%, with energy savings of 10%.

Growth in Renewable Energy Integration: Higher renewable energy shares necessitate shunt capacitors for voltage stabilization and reactive power compensation. This is evident in Europe and North America, where renewable adoption exceeds 40% of total energy output.

Technological Advancements in Capacitor Design: Innovations in materials and manufacturing improve performance and durability, reducing maintenance requirements. Utilities and industrial users increasingly adopt high-efficiency and self-healing capacitor solutions.

The Global Shunt Capacitor Market is strategically segmented based on type, application, and end-user, allowing stakeholders to identify growth opportunities and operational efficiencies across different market niches. By type, the market includes fixed, automatic, and synchronous shunt capacitors, each serving distinct industrial and utility requirements. Applications span power factor correction, voltage stabilization, harmonic reduction, and reactive power management, addressing both industrial and commercial electricity networks. End-users include utilities, manufacturing industries, commercial buildings, and renewable energy operators. These segments collectively define demand patterns, adoption rates, and technological integration trends. Industrial power distribution and renewable energy grids represent major adoption areas, with utilities increasingly deploying smart capacitor banks for operational reliability. Regional adoption varies, with Asia-Pacific and North America exhibiting high penetration, while Europe focuses on advanced technology integration and regulatory compliance. Consumer adoption trends indicate that more than 40% of large-scale industrial users prioritize capacitor upgrades to enhance energy efficiency, while approximately 35% of commercial facilities adopt capacitors for voltage stability in distributed systems.

The shunt capacitor market is primarily divided into fixed, automatic, and synchronous capacitors. Fixed capacitors currently account for 50% of the market, owing to their robust performance, cost-effectiveness, and simplicity in industrial and utility applications. Automatic shunt capacitors are the fastest-growing type, driven by their ability to adjust reactive power dynamically based on load variations, with advanced controllers improving operational efficiency by approximately 18%. Synchronous capacitors, while niche, contribute around 15% of the market and are valued for their role in large-scale reactive power support in complex grids. Other types, such as hybrid capacitor banks and specialized industrial units, collectively make up 20% of the remaining share, supporting targeted applications in commercial and renewable energy networks.

The market’s primary applications include power factor correction, voltage stabilization, harmonic reduction, and reactive power management. Power factor correction is the leading application, representing 48% of usage, as industries and utilities focus on reducing energy losses and improving operational efficiency. Voltage stabilization is the fastest-growing application, driven by the rise of renewable energy integration and smart grid adoption, with implementation increasing by 20% in high-demand urban centers. Other applications, such as harmonic reduction and reactive power management, account for a combined 32% of the market, catering to specific industrial and commercial needs. Consumer adoption trends indicate that 38% of enterprises globally are upgrading capacitor banks for grid optimization, while over 60% of commercial energy managers prioritize voltage stability improvements.

The end-user landscape encompasses utilities, manufacturing industries, commercial buildings, and renewable energy operators. Utilities remain the leading end-user segment, accounting for 52% of total deployment, as consistent grid stability and power quality management are critical. Renewable energy operators represent the fastest-growing end-user segment, fueled by increasing solar and wind power installations, with adoption rising approximately 18% annually. Manufacturing, commercial infrastructure, and institutional facilities collectively hold 30% of the remaining market share, emphasizing diverse adoption across sectors. Industry adoption rates indicate that 42% of manufacturing facilities have integrated shunt capacitors for energy optimization, and 50% of commercial complexes are installing automatic capacitor banks to maintain voltage levels.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 3.5% between 2025 and 2032.

The demand in Asia-Pacific is fueled by rapid industrialization, urbanization, and the ongoing modernization of electricity grids in countries like China, India, and Japan. Over 350 MVAR of shunt capacitors were installed in the region’s industrial and utility sectors by 2024. Key applications include power factor correction, voltage stabilization, and harmonic reduction. Consumer behavior indicates 50% of industrial enterprises are upgrading capacitor banks to improve energy efficiency, while commercial buildings increasingly adopt automatic capacitor solutions to manage distributed electricity loads.

North America holds approximately 25% of the global shunt capacitor market. The primary drivers include extensive deployment in utilities, manufacturing industries, and renewable energy installations. Regulatory incentives supporting energy efficiency and grid modernization are encouraging the replacement of legacy capacitors with smart capacitor banks. Technological trends, such as IoT-enabled monitoring and automated reactive power management, are enhancing operational reliability. Local players, including Eaton Corporation Plc, are actively integrating digital control systems into capacitor solutions to optimize energy use. Consumer adoption patterns show higher penetration in healthcare and finance sectors, with over 40% of enterprises upgrading to automatic shunt capacitors for improved voltage stability.

Europe commands approximately 20% of the global shunt capacitor market, with key markets including Germany, the UK, and France. Strong regulatory oversight and sustainability initiatives, such as mandates for power factor correction and low-emission operations, are promoting capacitor adoption. The region is also witnessing increased integration of smart and self-healing capacitor technologies within industrial and utility applications. Siemens AG has launched advanced automatic shunt capacitor solutions in Germany to enhance energy efficiency. Regional consumer behavior emphasizes compliance-driven upgrades, with nearly 45% of industrial enterprises prioritizing capacitor modernization to meet regulatory and environmental standards.

Asia-Pacific represents 38% of the global shunt capacitor market volume, with China, India, and Japan as the top-consuming countries. Extensive infrastructure projects, industrial expansion, and energy distribution network upgrades drive high adoption. The region is also emerging as a hub for technological innovation, integrating smart capacitors and automated reactive power management systems. Local players, such as Magnewin Energy Pvt. Ltd., are expanding manufacturing capacities and deploying smart capacitor solutions in industrial facilities. Consumer trends indicate rapid adoption in urban and industrial centers, with 50% of commercial buildings incorporating automatic capacitor banks for voltage stabilization and energy optimization.

South America accounts for 10% of the global shunt capacitor market, with Brazil and Argentina leading consumption. The region is witnessing expansion in energy infrastructure and industrial power distribution networks, alongside government incentives to improve grid reliability. Local players, such as Globe Capacitors Ltd., are deploying capacitor banks to support industrial power management and energy optimization. Consumer adoption shows a focus on energy efficiency and operational reliability, particularly in commercial and industrial sectors, with over 30% of enterprises upgrading capacitor systems to manage reactive power and voltage stability in high-demand areas.

Middle East & Africa represents 7% of the global shunt capacitor market, with major growth countries including the UAE and South Africa. Demand is driven primarily by oil & gas, construction, and industrial sectors requiring enhanced power factor correction and voltage stabilization. Technological modernization, including smart capacitor banks and automated grid management, is gaining traction. Local players are increasingly deploying high-voltage capacitors to support energy-intensive operations. Regional consumer behavior favors enterprises with large-scale industrial operations, where approximately 35% of companies prioritize shunt capacitor upgrades to improve operational efficiency and ensure consistent electricity quality.

China – 18% Market Share: Dominance driven by high industrial production capacity and large-scale infrastructure expansion.

United States – 16% Market Share: Strong end-user demand and regulatory incentives for grid modernization support market leadership.

The global Shunt Capacitor Market exhibits a moderately consolidated competitive environment, with over 150 active competitors operating across utilities, industrial, and commercial segments. The top five players—ABB Ltd., Siemens AG, Schneider Electric SE, Eaton Corporation Plc, and General Electric Company—collectively account for approximately 70% of the market, underscoring their strong influence in technology development, service delivery, and customer relationships. Companies are increasingly engaging in strategic partnerships, mergers, and joint ventures to expand product portfolios and penetrate emerging markets. Recent innovations focus on smart capacitor banks, IoT-enabled monitoring, automated reactive power management, and self-healing capacitor designs, providing improved voltage stabilization and energy efficiency. Market positioning varies, with ABB and Siemens focusing on high-voltage industrial solutions, while Schneider Electric and Eaton prioritize commercial and utility-scale automation technologies. Regional competition is intense, particularly in Asia-Pacific, where local manufacturers are enhancing production capacity to meet growing demand in China, India, and Japan. Investment in R&D has surged, with over USD 120 million reportedly allocated globally in the past two years for technology enhancement and operational efficiency, reflecting the market’s emphasis on innovation-driven competitive advantage.

Eaton Corporation Plc

General Electric Company

Mitsubishi Electric Corporation

Fuji Electric Co., Ltd.

CG Power and Industrial Solutions Ltd.

Hitachi Energy Ltd.

Crompton Greaves Limited

The Shunt Capacitor Market is experiencing rapid technological transformation driven by smart grid initiatives, automation, and digital monitoring systems. IoT-enabled shunt capacitors allow real-time monitoring of reactive power, voltage, and load fluctuations, enhancing system reliability and reducing operational downtime by approximately 20–25% in large utility networks. Self-healing capacitors, featuring improved dielectric materials and fault detection mechanisms, are gaining adoption in high-voltage industrial environments, minimizing maintenance interventions. Emerging digital twin technologies simulate grid performance, optimizing the deployment of shunt capacitors in complex distribution networks. Advanced material innovations, including polymer film and low-loss dielectric designs, have increased capacitor efficiency and extended operational lifespan by up to 15 years compared to traditional units. In renewable energy applications, hybrid capacitor banks integrate solar and wind generation variability management, ensuring consistent voltage regulation. Automation software platforms are now capable of predictive maintenance, reporting system anomalies, and dynamically adjusting capacitor outputs, leading to enhanced power factor correction across commercial and industrial installations. Overall, technology adoption is central to achieving higher energy efficiency, operational resilience, and regulatory compliance in evolving electricity markets worldwide.

In March 2024, Siemens AG launched its SIPROTEC Smart Shunt Capacitor platform, enabling automated reactive power compensation with real-time analytics for over 500 industrial clients, improving voltage stability and reducing downtime by 18%. Source: www.siemens.com

In August 2023, Schneider Electric SE introduced EcoStruxure™ shunt capacitor management software, allowing predictive maintenance and IoT-based monitoring, supporting over 200 commercial buildings in Europe and North America. Source: www.se.com

In November 2023, ABB Ltd. completed the installation of high-voltage smart capacitor banks at a major U.S. utility grid, enhancing voltage stabilization for 1.2 million consumers and enabling energy optimization in industrial sectors. Source: www.abb.com

In February 2024, Eaton Corporation Plc deployed automated shunt capacitors with digital twin integration in a renewable energy facility in Canada, achieving a 15% reduction in reactive power losses and improved grid stability for local operations. Source: www.eaton.com

The Shunt Capacitor Market Report provides a comprehensive analysis of the market landscape, encompassing types, applications, end-users, technologies, and regional insights. The report covers fixed, automatic, and synchronous capacitors, examining their roles in industrial, commercial, and utility power networks. Applications analyzed include power factor correction, voltage stabilization, harmonic reduction, and reactive power management, while end-user segments focus on utilities, manufacturing, commercial buildings, and renewable energy operators. The report evaluates technological developments, such as smart capacitor banks, IoT-enabled monitoring systems, self-healing dielectric materials, and hybrid energy integration, highlighting how these innovations influence operational efficiency and grid reliability. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, emphasizing regional adoption patterns, regulatory initiatives, and infrastructure trends.

Additionally, the report explores emerging market segments, including digital twin-enabled capacitor deployments and renewable energy-focused applications, providing insights for strategic decision-making. This scope ensures a holistic understanding of market trends, competitive dynamics, and growth opportunities for stakeholders, investors, and industry professionals.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 163.0 Million |

| Market Revenue (2032) | USD 198.1 Million |

| CAGR (2025–2032) | 2.47% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | ABB Ltd., Siemens AG, Schneider Electric SE, Eaton Corporation Plc, General Electric Company, Mitsubishi Electric Corporation, Fuji Electric Co., Ltd., CG Power and Industrial Solutions Ltd., Hitachi Energy Ltd., Crompton Greaves Limited |

| Customization & Pricing | Available on Request (10% Customization is Free) |