Reports

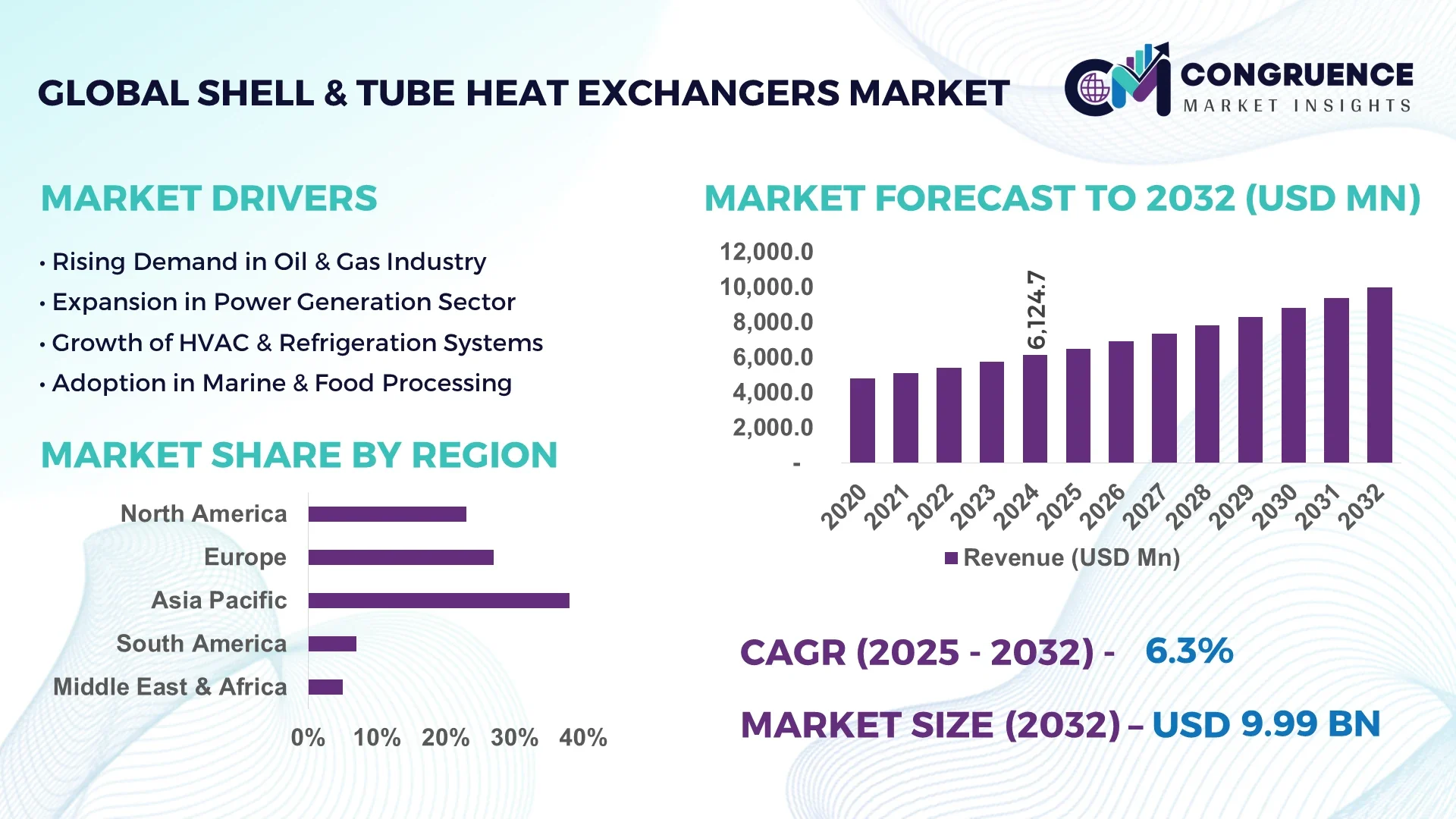

The Global Shell & Tube Heat Exchangers Market was valued at USD 6124.7 Million in 2024 and is anticipated to reach a value of USD 9985.1 Million by 2032 expanding at a CAGR of 6.3% between 2025 and 2032.

In China, production capacity has surged with the commissioning of several large-scale fabrication facilities capable of manufacturing over 10,000 units annually. Investment levels have accelerated in advanced welding technologies and CNC machining lines to support high-volume fabrication. Key industry applications in China span petrochemical refining, power generation, and HVAC infrastructure. Moreover, Chinese manufacturers are increasingly integrating automated nondestructive testing and high-precision tube-to-tubesheet expansion systems, reinforcing technological leadership in shell & tube heat exchanger fabrication.

The Shell & Tube Heat Exchangers Market is driven by diverse industrial sectors including chemical processing, oil & gas refining, power generation, HVAC and refrigeration, food & beverage, and pulp & paper industries. In chemical and petrochemical plants, exchangers are indispensable for distillation, reaction cooling, and condensation operations under high pressure and temperature. Recent product innovations include titanium-clad tubes for enhanced corrosion resistance, compact multi-pass designs for reduced footprint in urban HVAC systems, and integrated waste heat recovery units. Regulatory and environmental drivers such as energy efficiency mandates and tightening emissions standards are spurring demand globally, particularly in regions implementing decarbonization policies. Regional consumption patterns show robust growth in Asia Pacific driven by new heavy industrial projects, while Europe emphasizes retrofitting energy-efficient systems in existing infrastructure. Emerging trends include digital integration through condition-based monitoring and modular exchanger assemblies for rapid deployment and scalability. The future outlook points to continued innovation in materials, digital diagnostics, and flexibility to meet evolving industrial needs.

The use of artificial intelligence is reshaping the Shell & Tube Heat Exchangers Market by enabling advanced operational efficiency, predictive maintenance, and optimization of thermal performance. AI-driven models are now being embedded in exchanger control systems to continuously assess parameters such as tube fouling, thermal gradients, and vibration, allowing for dynamic adjustment of flow rates and temperature differentials. Operational performance has improved through the deployment of data analytics platforms that track inlet and outlet temperature, pressure variances, and fouling accumulation, enabling technicians to preempt maintenance requirements and reduce unplanned downtime. In some industrial refineries, AI algorithms have shortened cycle-cleanout durations by up to 20 %, significantly improving throughput. AI-powered fault detection systems now analyze real-time sensor streams to identify emerging anomalies—such as leak onset or heat transfer degradation—prompting targeted interventions that avoid extended outages. The Shell & Tube Heat Exchangers Market benefits from these digital enhancements by lowering maintenance costs, extending service intervals, and increasing overall process reliability. Advanced AI tools also support lifecycle planning: by simulating thermal and mechanical stresses digitally, operators can forecast maintenance needs and plan exchanger replacements before failures occur. These capabilities are increasingly expected by industry decision-makers as part of integrated plant automation strategies, reinforcing AI’s role as a catalyst for smarter operations in the Shell & Tube Heat Exchangers Market.

“Estimation of heat transfer coefficient in heat exchangers from closed-loop data using neural networks” developed in 2025 demonstrated that a neural-network architecture (Per-PINN) could accurately model the time-varying heat transfer coefficient U(t) from operational data, enhancing fouling estimation and enabling proactive maintenance scheduling.

The Shell & Tube Heat Exchangers Market is characterized by continuous technological enhancements, evolving industrial demands, and stringent regulatory expectations. Key trends include increasing preferences for corrosion-resistant materials such as titanium and nickel alloys, and integration of digital sensors for real-time performance monitoring. Demand from chemical processing and power generation facilities remains strong, driven by reliable high-temperature and high-pressure thermal management needs. Growth is also supported by urban expansion stimulating HVAC infrastructure projects, and evolving environmental standards pushing for lower emissions and higher energy efficiency. Emerging interest in modular exchanger designs allows manufacturers to offer scalable solutions for rapid deployment. Decisions are influenced by lifecycle cost analysis and total cost of ownership considerations. Regulatory pressures, particularly around energy efficiency and emissions, have reinforced the demand for exchangers that optimize thermal performance and reduce waste heat. All these dynamics influence capital equipment planning, retrofit decision cycles, and partnership models among fabricators and end-users in the Shell & Tube Heat Exchangers Market.

Rapid construction of petrochemical and refining facilities in Asia Pacific—especially in China and India—is driving increased deployment of shell & tube heat exchangers. The need for robust thermal systems for distillation, condensation, and reaction cooling is rising. Advanced fabrication plants in the region are ramping up production, deploying automated welding lines and material handling systems to support high throughput. This expansion is compelling chemical and petrochemical operators to invest in heavy-duty exchangers designed to withstand corrosive media and fluctuating thermal loads—directly benefiting the Shell & Tube Heat Exchangers Market with significant demand growth in fabricator order books.

Stainless steel, titanium, and exotic alloy prices have increased, raising manufacturing costs of shell & tube exchangers. Furthermore, maintenance operations—particularly cleaning and plugging to manage fouling—require specialized equipment and extended downtime periods. As a result, operators face heightened capex and opex burdens. These cost pressures can delay replacement cycles and lead some buyers to consider refurbished equipment or alternative technologies, constraining the overall Shell & Tube Heat Exchangers Market uptake in cost-sensitive segments.

Digital twin adoption offers an opportunity for enhanced monitoring and lifecycle management of shell & tube units. By simulating thermal performance and fouling over time, operators can optimize inspection schedules and reduce unplanned shutdowns. Modular exchanger units—pre-engineered and skid-mounted—also offer rapid installation and commissioning, particularly valuable in offshore and remote industrial sites. These modular solutions can reduce on-site labour by up to 30 % and accelerate project timelines, presenting significant potential for growth in the Shell & Tube Heat Exchangers Market.

Complex regulatory requirements around pressure vessel codes, material certifications, and environmental standards present challenges to exchanger suppliers. Complying with regional codes—such as PED in Europe, ASME in North America, and national equivalents in Asia—requires extensive documentation, testing, and quality assurance processes. Shipment of customized units across borders often faces delays due to certification mismatches. These regulatory hurdles increase lead times and compliance costs, complicating international trade and project planning within the Shell & Tube Heat Exchangers Market.

Modular fabrication and pre-assembled exchanger units: Manufacturers are delivering factory-integrated shell & tube units with plug-and-play plumbing connections. These modular systems reduce field installation labour by approximately 25 % and shorten commissioning cycles for industrial plants.

Advanced corrosion-resistant alloy adoption: Growing use of titanium-clad, nickel-alloy, and duplex stainless steel tube bundles is extending exchanger service life by up to 40 % in corrosive chemical and desalination environments.

Smart monitoring retrofits: Retrofitting legacy shell & tube units with sensor arrays for temperature, pressure, and vibration has allowed operators to cut unscheduled maintenance incidents by nearly 30 %, improving operational uptime.

Waste heat recovery integration: Incorporating additional exchanger stages to capture and reuse waste heat within industrial processes (e.g., capturing boiler flue heat for pre-heating feed water) has led to energy savings of up to 15 % for power and manufacturing facilities.

The Shell & Tube Heat Exchangers Market segmentation includes product types—such as one-pass, two-pass, U-tube, floating head models—applications spanning chemical, petrochemical, power generation, HVAC, marine, and food-grade processing, and end-user categories encompassing refineries, utilities, HVAC contractors, and food & beverage processors. Each segment presents strategic relevance: types vary by thermal performance and maintenance needs; applications define design complexity and material choice; end-users determine volume, customization needs, and service models. Decision-makers and analysts leverage segmentation insights to tailor product offerings, service frameworks, and manufacturing investment strategies.

Among available shell & tube exchanger types, floating head designs lead due to their flexibility for tube bundle removal and effective cleaning in high-fouling chemical environments. U-tube models are the fastest-growing because their simple construction and ability to handle thermal expansion without complicated sealing make them ideal for high-temperature cycles. One-pass and two-pass variants continue to serve niche requirements—one-pass for straightforward heat transfer with low pressure drop, and two-pass for higher heat recovery in compact footprints.

Chemical and petrochemical applications lead demand for shell & tube exchangers, driven by intensive use in distillation, reaction cooling, and condensers, particularly under high pressures and corrosive conditions. The fastest-growing application is HVAC & refrigeration—for urban infrastructure, district heating, and data centre cooling—due to increasing energy efficiency mandates. Oil & gas, power, and marine applications contribute modestly, supporting complex cooling, pre-heating, or waste heat systems.

Refineries and chemical processors represent the leading end-users, given their reliance on reliable thermal management for core operations. The fastest-growing end-user segment is building services contractors in commercial and institutional HVAC projects, responding to urbanization and low-carbon building codes. Utilities, marine operators, and food & beverage producers also participate, often under retrofit or modernization initiatives toward improved energy performance.

Asia-Pacific accounted for the largest market share at 38% in 2024 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

The Shell & Tube Heat Exchangers Market exhibits strong regional diversity, with Asia-Pacific maintaining leadership due to its vast manufacturing capacity, industrial expansion, and high energy demand. Europe and North America remain critical hubs for technology adoption and regulatory-driven upgrades, while South America and Middle East & Africa are emerging as vibrant markets supported by oil & gas projects, infrastructure development, and government-backed energy initiatives. Regional differences in regulatory environments, materials adoption, and industry verticals create unique opportunities for stakeholders to tailor strategies and leverage growth potential across global markets.

Advanced Fabrication Driving Industrial Cooling Solutions

North America accounted for approximately 23% of the Shell & Tube Heat Exchangers Market in 2024, supported by a robust base of chemical, oil & gas, and power generation industries. Demand is reinforced by the shale gas boom, which continues to require efficient thermal systems for refining and petrochemical plants. Regulatory agencies have enforced stricter efficiency and emissions standards, compelling manufacturers to upgrade exchanger designs. Technological advancements, including AI-based predictive maintenance and IoT-enabled monitoring, are gaining traction across industrial facilities. Digital twin simulations are also being deployed for lifecycle optimization. Government initiatives supporting decarbonization and industrial modernization further strengthen the adoption of advanced exchangers across the region.

Sustainability and Innovation Reshaping Energy Systems

Europe held around 27% of the Shell & Tube Heat Exchangers Market in 2024, driven by key economies including Germany, the UK, and France. Regulatory bodies such as the European Commission enforce strict environmental standards that encourage adoption of energy-efficient and low-emission thermal systems. Sustainability initiatives such as the EU Green Deal continue to accelerate retrofitting projects. Countries like Germany are investing heavily in renewable energy infrastructure, while France and the UK lead in district heating applications. Advanced technologies, including corrosion-resistant alloys and modular exchangers, are being integrated into industrial systems to align with long-term carbon neutrality targets.

Industrial Expansion and Energy Infrastructure Boost Demand

Asia-Pacific accounted for the largest share at 38% of the Shell & Tube Heat Exchangers Market in 2024, with China, India, and Japan as the top-consuming nations. The region’s demand is primarily fueled by large-scale chemical plants, oil refineries, and extensive power generation infrastructure. China dominates with high-volume fabrication capacity, while India is rapidly expanding petrochemical and industrial processing facilities. Japan continues to advance in precision engineering and corrosion-resistant material applications. Regional technology hubs are focusing on AI-enabled condition monitoring and modular assembly techniques, ensuring Asia-Pacific remains the most dynamic region for innovation and industrial application growth.

Energy Diversification Supporting Thermal Equipment Demand

South America represented nearly 7% of the Shell & Tube Heat Exchangers Market in 2024, with Brazil and Argentina leading consumption. Brazil’s oil refining capacity and renewable energy investments contribute significantly to regional adoption. Argentina’s chemical and agricultural processing industries further support steady demand. Infrastructure modernization projects, especially in power generation and industrial processing, are spurring market penetration. Governments in the region are promoting trade incentives and encouraging localized production to strengthen supply chains. The adoption of advanced alloy exchangers and modular systems is gradually increasing in response to regional climatic and operational challenges.

Oil & Gas Strength Meets Modernization Initiatives

The Middle East & Africa accounted for about 5% of the Shell & Tube Heat Exchangers Market in 2024, yet it is projected to record the fastest expansion through 2032. Countries like UAE and Saudi Arabia remain major demand centers due to ongoing oil & gas exploration, refining expansions, and large-scale industrial projects. South Africa is emerging as a hub for power generation and mining sector applications. Regional modernization trends emphasize digital monitoring tools, robust corrosion-resistant materials, and modular exchangers for rapid deployment. Trade partnerships with global equipment suppliers and new local fabrication facilities are accelerating adoption across the region.

China – 24% market share: High-volume production capacity and strong industrial demand from petrochemical and power generation sectors.

Germany – 12% market share: Advanced engineering expertise, strong focus on sustainable energy infrastructure, and stringent regulatory standards driving adoption.

The Shell & Tube Heat Exchangers Market is highly competitive, with over 60 active global and regional players delivering diverse product portfolios. Established manufacturers dominate with advanced engineering capabilities, while smaller firms compete through customization and cost optimization. Competition is shaped by strategic initiatives such as mergers, cross-border partnerships, and investments in modular exchanger fabrication. Technological innovation—including the integration of digital twins, smart monitoring systems, and corrosion-resistant alloys—plays a decisive role in market positioning. Leading companies are focusing on expanding global footprints by establishing fabrication hubs in Asia and the Middle East to shorten lead times. In addition, competition is intensifying in aftermarket services, where predictive maintenance and lifecycle management solutions are becoming essential differentiators. This evolving landscape underscores the shift toward innovation-driven strategies as companies position themselves to capture long-term growth in the Shell & Tube Heat Exchangers Market.

Alfa Laval AB

Kelvion Holding GmbH

Xylem Inc.

HRS Heat Exchangers Ltd.

API Heat Transfer Inc.

Danfoss A/S

Chart Industries Inc.

Hisaka Works Ltd.

Funke Wärmeaustauscher Apparatebau GmbH

Koch Heat Transfer Company LP

Technological advancements are reshaping the Shell & Tube Heat Exchangers Market, with innovations in materials, design, and digital integration driving performance improvements. Advanced alloys such as titanium, duplex stainless steel, and nickel-based composites are being deployed to extend service life in corrosive environments, achieving up to 40% longer operational durability. Computational fluid dynamics (CFD) modeling is increasingly used during design stages to optimize flow distribution and thermal efficiency, reducing pressure drop by up to 15%. Digital technologies are transforming lifecycle management, with IoT sensors enabling real-time monitoring of fouling, vibration, and tube wall thickness. Predictive analytics supported by AI algorithms helps forecast maintenance schedules, reducing unplanned downtime by approximately 25%.

Modular exchanger technologies are gaining traction, allowing for pre-fabricated, skid-mounted solutions that cut installation times by 30% and provide scalability for industrial projects. Integration of waste heat recovery systems within exchangers supports industrial decarbonization by capturing and reusing heat that would otherwise be lost. Additive manufacturing is also entering the market, enabling production of complex geometries and high-efficiency tube configurations that were previously impractical. These combined innovations reflect a shift toward smarter, longer-lasting, and more energy-efficient systems, reinforcing technology as a core competitive advantage in the Shell & Tube Heat Exchangers Market.

In March 2023, Alfa Laval introduced a titanium-clad shell & tube exchanger line designed for offshore oil & gas platforms, extending service life by 35% under highly corrosive marine conditions.

In July 2023, Kelvion launched a modular floating head exchanger system for chemical plants, cutting maintenance downtime by nearly 20% through easy tube bundle replacement.

In February 2024, API Heat Transfer unveiled a digitally monitored shell & tube exchanger equipped with AI-based fouling detection sensors, improving operational uptime in refining applications.

In May 2024, Hisaka Works Ltd. expanded its production facility in Japan to manufacture high-capacity shell & tube units, adding capacity for over 2,500 units annually.

The Shell & Tube Heat Exchangers Market Report provides comprehensive insights into industry dynamics, covering product types, applications, and end-user industries across all major regions. It analyzes demand patterns from petrochemicals, power generation, HVAC, food & beverage, marine, and pulp & paper sectors. The report evaluates segmentation by exchanger type—including floating head, U-tube, fixed tube sheet, and multi-pass designs—highlighting their respective advantages, use cases, and adoption trends. Regional coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, outlining demand patterns and unique regulatory and industrial influences shaping growth.

The scope further includes analysis of technological innovations such as corrosion-resistant alloys, AI-based predictive maintenance, modular construction, and additive manufacturing. Special focus is given to energy efficiency initiatives, integration of waste heat recovery systems, and digital twin deployment for lifecycle management. The report also outlines competitive strategies of leading manufacturers, identifying how companies are leveraging global expansion, partnerships, and aftermarket services to strengthen positioning. By providing detailed coverage of both established and emerging segments, the Shell & Tube Heat Exchangers Market Report offers decision-makers actionable insights for investment, product development, and long-term strategic planning across a rapidly evolving industrial landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 6124.7 Million |

|

Market Revenue in 2032 |

USD 9985.1 Million |

|

CAGR (2025 - 2032) |

6.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Alfa Laval AB, Kelvion Holding GmbH, Xylem Inc., HRS Heat Exchangers Ltd., API Heat Transfer Inc., Danfoss A/S, Chart Industries Inc., Hisaka Works Ltd., Funke Wärmeaustauscher Apparatebau GmbH, Koch Heat Transfer Company LP |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |