Reports

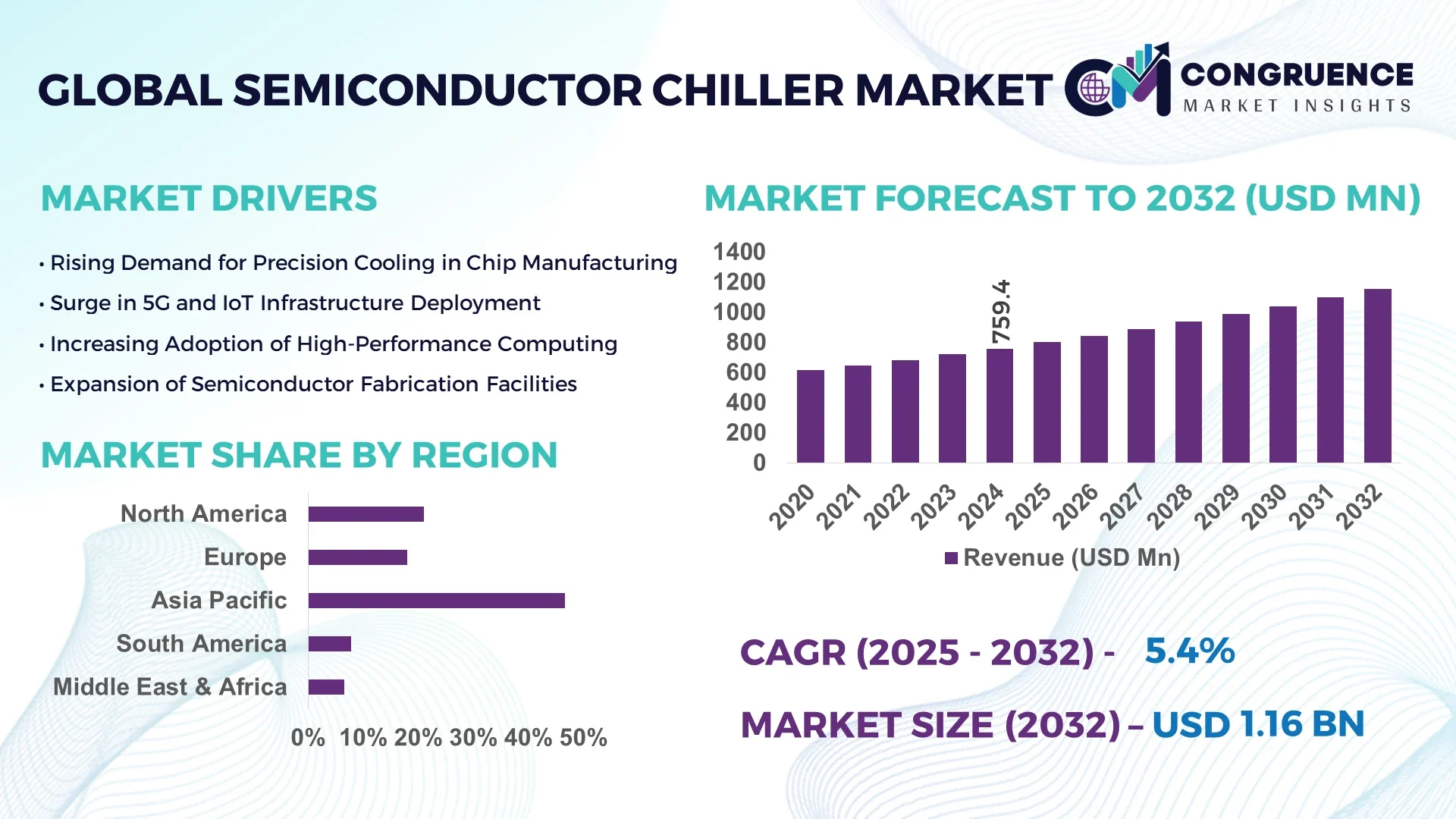

The Global Semiconductor Chiller Market was valued at USD 759.42 Million in 2024 and is anticipated to reach a value of USD 1156.66 Million by 2032 expanding at a CAGR of 5.4% between 2025 and 2032.

In the United States, robust investments in advanced semiconductor fabrication facilities have significantly elevated demand for high-precision chillers, particularly in states like Texas and Arizona. These regions benefit from dedicated industrial parks and government-backed semiconductor incentive programs, contributing to elevated production capabilities and widespread use of liquid cooling technologies in cleanroom environments.

The Semiconductor Chiller Market plays a vital role in ensuring stable thermal management in high-performance semiconductor manufacturing, lithography, and etching processes. Across sectors such as integrated circuit production, wafer testing, and photonics, precision chillers have become indispensable due to their ability to maintain strict temperature tolerances. Technological advancements, including the integration of digital monitoring systems and eco-friendly refrigerants, are significantly improving energy efficiency and operational control. Additionally, the adoption of modular and scalable chiller systems tailored for varying fab sizes is becoming increasingly common. Regulatory shifts, especially those promoting environmentally sustainable refrigerants, are also influencing design innovations. Regionally, the Asia-Pacific market—led by Taiwan, South Korea, and China—exhibits rapid adoption due to expanding fab infrastructure and strong export dynamics. Meanwhile, the rise of compact chillers for specialized micro-fabrication and the demand for ultra-low vibration cooling solutions signal the evolution of the market’s growth trajectory.

Artificial Intelligence is ushering in a new era of operational intelligence and automation in the Semiconductor Chiller Market. By embedding AI-powered predictive analytics into cooling systems, manufacturers can now detect potential system anomalies before they result in operational downtime. Smart chillers utilize machine learning algorithms to analyze temperature fluctuation patterns, adjusting coolant flow and compressor output in real time to achieve optimal thermal stability with minimal energy consumption. This not only increases system longevity but also contributes to significant reductions in total cost of ownership.

In semiconductor fabs where even a single degree of deviation can compromise chip integrity, AI-enabled chiller systems offer unmatched precision. These systems automatically adapt to process changes and environmental conditions, reducing the need for manual intervention. Furthermore, AI integration supports real-time diagnostics, remote system management, and self-regulating maintenance schedules—features that are crucial for uninterrupted operations in high-throughput manufacturing environments.

Across the Semiconductor Chiller Market, companies are also integrating AI into Building Management Systems (BMS), enabling centralized control of multiple thermal systems for improved synchronization and efficiency. Additionally, AI is helping optimize load balancing across multiple chillers, resulting in up to 18% improvement in energy efficiency across semiconductor fabrication facilities. This digital transformation not only enhances equipment performance but also aligns with broader ESG goals by reducing carbon footprints and enabling more transparent energy reporting. As AI technologies mature, their role in driving innovation and competitiveness within the Semiconductor Chiller Market will only grow more integral.

“In early 2025, a leading semiconductor fab in South Korea implemented an AI-enhanced chiller monitoring platform that reduced equipment downtime by 23% and improved coolant utilization efficiency by 17%, thanks to real-time machine learning analysis of thermal load variations across multiple production zones.”

The need for precision cooling in modern semiconductor fabs is a major growth driver for the Semiconductor Chiller Market. With the global push for advanced chip production used in AI, quantum computing, and high-speed telecommunications, the thermal management demands have intensified. Manufacturers are installing advanced EUV lithography and plasma etching machines that require exact temperature control down to ±0.1°C. This has led to rising adoption of semiconductor chillers equipped with dynamic temperature modulation, micro-channel heat exchangers, and noise-reduction features. For instance, the growing presence of 300mm wafer fabs necessitates chillers with higher load capacities and fail-safe redundancy to ensure 24/7 uninterrupted operations. These factors are pushing OEMs and fabs to prioritize smart, efficient thermal control systems, driving sustained market expansion.

One significant restraint in the Semiconductor Chiller Market is the high upfront investment required for acquiring and integrating precision chillers. These systems often involve complex installations with custom control units, specialized piping, and advanced sensors, contributing to elevated capital expenditures. Additionally, ongoing maintenance—including calibration, fluid replacement, and filter checks—adds to the operational burden, especially for fabs operating multiple units. The need for skilled personnel to manage these systems further raises operational costs. Smaller semiconductor players, particularly those in developing regions, often find it difficult to justify the total cost of ownership for advanced chillers, hindering broader adoption. This financial barrier may slow deployment in cost-sensitive environments.

The Semiconductor Chiller Market is witnessing substantial opportunities due to increased capital flows into semiconductor infrastructure in emerging economies. Countries such as Vietnam, India, and Malaysia are launching ambitious fab development initiatives, supported by government-backed semiconductor manufacturing incentives. As new fabrication plants emerge, demand for localized and adaptable thermal management solutions is increasing. These markets offer lucrative opportunities for chiller manufacturers to introduce energy-efficient, mid-range cooling systems tailored to regional needs. Moreover, the growth of packaging, testing, and foundry operations in these regions is fostering additional demand for both centralized and decentralized chiller units. Vendors capable of offering integrated, cost-effective, and scalable solutions are well-positioned to capture market share in these high-growth areas.

A key challenge facing the Semiconductor Chiller Market is adapting to evolving environmental regulations concerning refrigerants and greenhouse gas emissions. International protocols, including those limiting the use of hydrofluorocarbons (HFCs), require manufacturers to redesign systems using low-global-warming-potential (GWP) alternatives. However, the transition to next-generation refrigerants involves reengineering system components, upgrading compressor technology, and ensuring compliance with safety standards—all of which increase design complexity and cost. Additionally, many fabs are located in jurisdictions with overlapping regulatory frameworks, complicating global standardization. These pressures place considerable compliance and R&D burdens on chiller manufacturers, potentially delaying product rollouts and impacting operational flexibility.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction practices is accelerating demand for compact and scalable semiconductor chillers. In high-cost labor regions such as Western Europe and the U.S., modular fab units equipped with pre-installed thermal control systems reduce construction time by up to 30%. These prefabricated systems enable quick deployment of fabs and minimize onsite customization, resulting in growing interest in plug-and-play chiller units that are easy to integrate within modular setups.

• Integration of IoT and Predictive Maintenance Features: IoT-enabled chillers with real-time diagnostics and self-regulating components are gaining widespread traction. Leading manufacturers now offer chillers embedded with smart sensors that allow for condition-based maintenance and operational status reporting. Over 40% of newly commissioned semiconductor fabs in Asia-Pacific have already adopted predictive maintenance-enabled chillers to reduce unplanned downtime and ensure uninterrupted wafer fabrication cycles. This trend is significantly optimizing energy use and extending equipment lifecycle.

• Shift Toward Low-GWP and Eco-Friendly Refrigerants: Environmental regulations are catalyzing a strong push toward refrigerants with low global warming potential (GWP). Chiller manufacturers are transitioning from traditional HFCs to advanced alternatives such as R-1234yf and R-513A. In Japan and South Korea, more than 50% of new chillers deployed in 2024 now operate on low-GWP refrigerants, complying with aggressive environmental mandates. This shift is redefining design priorities for OEMs and promoting sustainable product portfolios.

• Increasing Customization for Niche Semiconductor Applications: As niche sectors such as MEMS and compound semiconductors grow, the need for application-specific chillers is rising. For example, fabs focusing on GaN and SiC wafers require chillers with tighter temperature control and resistance to magnetic interference. Manufacturers are now offering highly customizable chiller solutions with enhanced vibration isolation and thermal zoning features. This trend is expanding the product mix and encouraging the development of tailored solutions for specialized chip fabrication processes.

The Semiconductor Chiller Market is segmented based on type, application, and end-user verticals. Each of these segments plays a vital role in shaping the demand and innovation landscape of thermal management in semiconductor manufacturing. Type segmentation includes various cooling technologies such as air-cooled, water-cooled, and dual cooling systems, each serving specific fab requirements. Application-wise, chillers are used in etching, lithography, wafer cleaning, and other high-heat generating processes that demand thermal precision. Meanwhile, end-user segmentation comprises integrated device manufacturers (IDMs), foundries, outsourced semiconductor assembly and test (OSAT) providers, and research institutions. A detailed understanding of these segments helps identify growth pockets and competitive advantages in global markets.

Air-cooled chillers represent the leading type in the Semiconductor Chiller Market, largely due to their ease of installation and lower maintenance needs. These systems are particularly favored in regions with moderate climates where outdoor heat rejection is viable. Their rising deployment in mid-sized fabs contributes to their widespread adoption. Water-cooled chillers, although requiring more infrastructure, are the fastest-growing type, driven by their superior energy efficiency and ability to handle high thermal loads, especially in mega fabs operating 24/7. Dual-cooling systems are also gaining attention in flexible fabs that switch between processes requiring varied thermal conditions. Portable and compact chillers serve niche functions, such as R&D labs or pilot lines, and contribute to the market by fulfilling low-capacity yet precision-sensitive requirements. The overall type segmentation is evolving rapidly with the emergence of hybrid designs that combine the benefits of traditional and modern thermal control technologies.

Lithography emerges as the leading application for chillers in the Semiconductor Chiller Market due to its reliance on stable, vibration-free cooling environments. EUV lithography, in particular, demands precise temperature control to ensure imaging accuracy, making high-performance chillers a core component of the process. The fastest-growing application segment is etching, driven by the development of advanced node chips where precise temperature regulation is essential to maintaining pattern integrity. Wafer cleaning also contributes significantly to market demand, with miniaturization trends requiring enhanced contamination control supported by consistent thermal environments. Backend processes such as dicing and packaging are increasingly incorporating dedicated chiller units to maintain thermal consistency during precision operations. As chip architectures grow more complex, every stage of production—both front-end and back-end—relies heavily on optimized cooling, deepening the market's integration across diverse fabrication processes.

Integrated Device Manufacturers (IDMs) are the leading end-user segment in the Semiconductor Chiller Market due to their vertical integration and investment in cutting-edge fabs. These players prioritize in-house production capabilities and require large-scale thermal solutions capable of operating continuously with minimal deviations. Foundries represent the fastest-growing end-user segment, particularly in Asia-Pacific, as fabless design companies outsource chip production, fueling demand for scalable and energy-efficient chillers. Outsourced Semiconductor Assembly and Test (OSAT) providers also play a notable role, especially in the backend stages where temperature control is vital during bonding and packaging. Research institutions and universities are emerging users, deploying compact chillers in experimental cleanroom environments for prototype development and process validation. These diverse end-user profiles highlight the expanding relevance of precision cooling across both industrial and institutional semiconductor ecosystems.

Asia-Pacific accounted for the largest market share at 46.7% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

Asia-Pacific continues to dominate the Semiconductor Chiller Market, driven by robust semiconductor manufacturing activities across China, Taiwan, South Korea, and Japan. High-volume chip production, substantial investment in wafer fabs, and rapid technological integration have made the region a powerhouse in thermal management infrastructure. Government support for cleanroom expansion and green refrigerant adoption is also fostering growth. Meanwhile, North America is witnessing accelerated adoption of advanced cooling technologies in high-performance chip manufacturing, especially across the U.S. and Canada. With expanding foundry capacity, rising demand for AI-based chipsets, and supportive policy reforms, the region is positioning itself as a key growth hub in the global Semiconductor Chiller Market.

Advanced Thermal Solutions Transforming Cleanroom Efficiency

North America accounted for a 21.5% share of the Semiconductor Chiller Market in 2024, led by the U.S. with its expansive semiconductor fabrication footprint and investment in cleanroom innovation. High demand from industries such as aerospace, defense, and automotive electronics is significantly driving adoption. Federal initiatives like the CHIPS Act are fueling investment in advanced fabrication facilities, requiring state-of-the-art temperature regulation systems. Technological innovations, including smart chillers with IoT integration and AI-based predictive diagnostics, are reshaping thermal control processes. The focus on digitized, energy-efficient manufacturing environments is pushing the market toward scalable and modular chiller designs tailored for next-gen semiconductor plants.

Sustainable Cooling Technologies Gaining Ground in Chip Manufacturing

Europe held approximately 17.9% of the Semiconductor Chiller Market in 2024, with Germany, the UK, and France serving as the primary demand centers. These countries are emphasizing sustainable semiconductor manufacturing practices, supported by strong environmental regulations from agencies such as the European Chemicals Agency (ECHA). Germany, in particular, is advancing high-performance chip design for the automotive sector, driving precision cooling needs. The region is rapidly integrating low-GWP refrigerants and energy-efficient chiller systems as part of its green transition. Moreover, digital transformation initiatives across fab infrastructure are encouraging the adoption of AI-powered chillers and real-time diagnostics for fault-tolerant chip production.

Rapid Fab Expansion and Smart Chiller Demand Dominating Growth Landscape

With over 46.7% market share in 2024, Asia-Pacific leads the Semiconductor Chiller Market globally. China, Japan, Taiwan, and South Korea are the top consumers, each housing several mega fabs dedicated to advanced node chip production. These nations are investing in clean, automated fabs, boosting demand for highly accurate thermal control systems. Japan and South Korea are particularly focused on adopting low-emission cooling solutions in response to regional climate goals. Concurrently, innovation hubs across India and Southeast Asia are fostering growth through increased electronics exports and R&D investment. Smart chiller technology adoption is high, driven by the need to reduce energy costs and meet regulatory benchmarks in high-output fabs.

Growing Industrial Base and Cleanroom Infrastructure Boosting Demand

Brazil and Argentina represent the largest contributors to the Semiconductor Chiller Market in South America. In 2024, the region held a modest 4.8% share, though strategic infrastructure improvements and governmental trade incentives are fostering upward momentum. Brazil’s development of semiconductor assembly lines and investments in electronics exports are triggering demand for advanced thermal control systems. Argentina is witnessing a growing emphasis on energy-efficient systems across its industrial parks, influencing chiller purchases. Incentive programs that support digital and cleanroom infrastructure have led to an uptick in fab capacity expansions. Additionally, renewable energy integration into fab utilities is spurring demand for sustainable chiller technologies.

Digital Modernization and Industrial Investments Driving Chiller Demand

Middle East & Africa contributed 3.6% to the global Semiconductor Chiller Market in 2024. Countries such as the UAE and South Africa are emerging as growth hotspots due to rising investments in digital infrastructure and electronics manufacturing. The UAE's technology parks are witnessing increased deployment of cleanroom environments, fueling precision cooling needs. Growth in the regional oil & gas sector’s electronics control systems also supports market demand. Governments are encouraging localized semiconductor value chains through policy frameworks and trade pacts, which, in turn, are enhancing investment in temperature control technologies. Technological modernization, especially integration with smart energy grids, is further shaping the chiller market landscape in the region.

China – 27.3% market share

High chip production capacity and strong end-user demand from electronics and telecom sectors drive dominance in the Semiconductor Chiller Market.

United States – 18.2% market share

Significant investment in fabrication plants and advanced semiconductor technologies propels demand for next-gen chiller systems.

The Semiconductor Chiller Market is characterized by intense competition, with more than 40 prominent companies actively operating across various global regions. These players are strategically positioned across North America, Asia-Pacific, and Europe, offering differentiated chiller solutions tailored for diverse semiconductor fabrication environments. Innovation remains a cornerstone of the competitive landscape, with leading firms investing heavily in smart cooling systems, eco-friendly refrigerants, and digitally integrated control modules.

Strategic partnerships are increasingly shaping the market dynamics, as companies collaborate with chip manufacturers, fab equipment vendors, and automation providers to enhance operational compatibility. Mergers and acquisitions are also accelerating, particularly in Asia-Pacific and Europe, where firms aim to expand their technological portfolios and regional footprints. Product innovation trends include the development of modular and scalable chillers, IoT-enabled diagnostic systems, and low-noise cooling units for precision electronics manufacturing. Competitors are also leveraging advanced analytics and AI-powered software to improve predictive maintenance and reduce operational downtime, further intensifying the race for market leadership in the global Semiconductor Chiller Market.

Daikin Industries, Ltd.

Thermo Fisher Scientific Inc.

KKT Chillers

BV Thermal Systems

Laird Thermal Systems

RIEDEL Kooling GmbH

Glen Dimplex Group

Motivair Corporation

Filtrine Manufacturing Company

SMC Corporation

The Semiconductor Chiller Market is undergoing a major technological transformation, propelled by advancements in precision cooling, digital monitoring, and eco-efficient refrigeration. One of the most significant innovations is the integration of intelligent control systems that enable real-time temperature management using predictive analytics and machine learning. These systems can adapt chiller performance dynamically to fluctuations in fab operations, improving system efficiency by up to 18% while minimizing downtime. IoT-enabled chillers are also gaining ground, especially in cleanroom environments requiring strict process control. These systems provide remote diagnostics, live performance tracking, and automated alerts, allowing fab operators to conduct predictive maintenance and reduce operational risks. Additionally, variable-speed compressor technology is being widely adopted, enabling fine-tuned energy consumption and ensuring better thermal stability in sensitive semiconductor production zones.

In response to environmental regulations, low-global-warming-potential (low-GWP) refrigerants such as R-1234yf and R-513A are increasingly replacing traditional HFCs in newly launched systems. This shift is driving manufacturers to design green chillers with reduced emissions and higher energy efficiency, aligning with global sustainability goals. Furthermore, modular and scalable chiller designs are emerging to support fab expansion projects without interrupting operations. These designs are ideal for high-density installations and can be easily reconfigured to match production scale. Such technology evolution is setting new benchmarks in thermal precision and cost-effective semiconductor manufacturing infrastructure.

• In March 2024, SMC Corporation launched its next-generation HRS-R Series recirculating chillers, designed specifically for semiconductor equipment. The new units offer 23% higher cooling capacity and improved flow rate precision, catering to the increasing demand for stability in high-performance chip production lines.

• In November 2023, Daikin Industries unveiled an industrial chiller system incorporating R-1234ze(E), a next-gen low-GWP refrigerant. The unit demonstrated a 30% reduction in greenhouse gas emissions while maintaining the thermal stability needed for photolithography and wafer etching processes.

• In January 2024, Glen Dimplex Thermal Solutions partnered with a leading semiconductor fab in Europe to pilot AI-integrated chillers. Early trials showed a 14% boost in operational uptime and a 21% reduction in energy use through real-time adaptive temperature control algorithms.

• In July 2023, KKT Chillers expanded its manufacturing plant in Germany, increasing production output capacity by 35%. The expansion aimed to meet rising demand for custom-engineered chillers tailored for advanced semiconductor nodes and cleanroom installations across Europe and Asia.

The Semiconductor Chiller Market Report provides an in-depth analysis of the global landscape, covering a comprehensive range of industry components including product types, application domains, end-user sectors, and regional trends. The report examines key segments such as air-cooled chillers, water-cooled chillers, and recirculating chillers, with detailed attention to their role in semiconductor manufacturing processes like wafer fabrication, photolithography, etching, and deposition. Special focus is given to the increasing integration of precision cooling technologies designed for high-performance and compact semiconductor equipment. From an application perspective, the report assesses demand across fabs, research labs, and semiconductor testing facilities. It highlights the growing relevance of chiller systems in maintaining cleanroom conditions, stabilizing thermal profiles in micro-scale processing, and supporting temperature-sensitive processes in advanced chip production.

Geographically, the study covers five primary regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report identifies strategic developments, industrial adoption rates, and technology-driven expansion across key countries like the U.S., China, Japan, Germany, and South Korea. Additionally, the report outlines current and emerging technologies reshaping the market, such as IoT-enabled smart chillers, energy-efficient refrigerants, and modular chiller systems. It also touches on niche trends including compact cooling systems for edge semiconductor devices and AI-assisted chiller optimization platforms. The report serves as a strategic guide for stakeholders navigating the evolving semiconductor thermal management landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 759.42 Million |

|

Market Revenue in 2032 |

USD 1156.66 Million |

|

CAGR (2025 - 2032) |

5.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End‑User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Samsung Electronics Co., Ltd., Apple Inc., Sony Corporation, LG Electronics Inc., Panasonic Corporation, Xiaomi Corporation, HP Inc., Dell Technologies Inc., Lenovo Group Ltd., TCL Technology Group Corporation, ASUSTeK Computer Inc., Acer Inc., Huawei Technologies Co., Ltd., Sharp Corporation, Vivo Communication Technology Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |