Reports

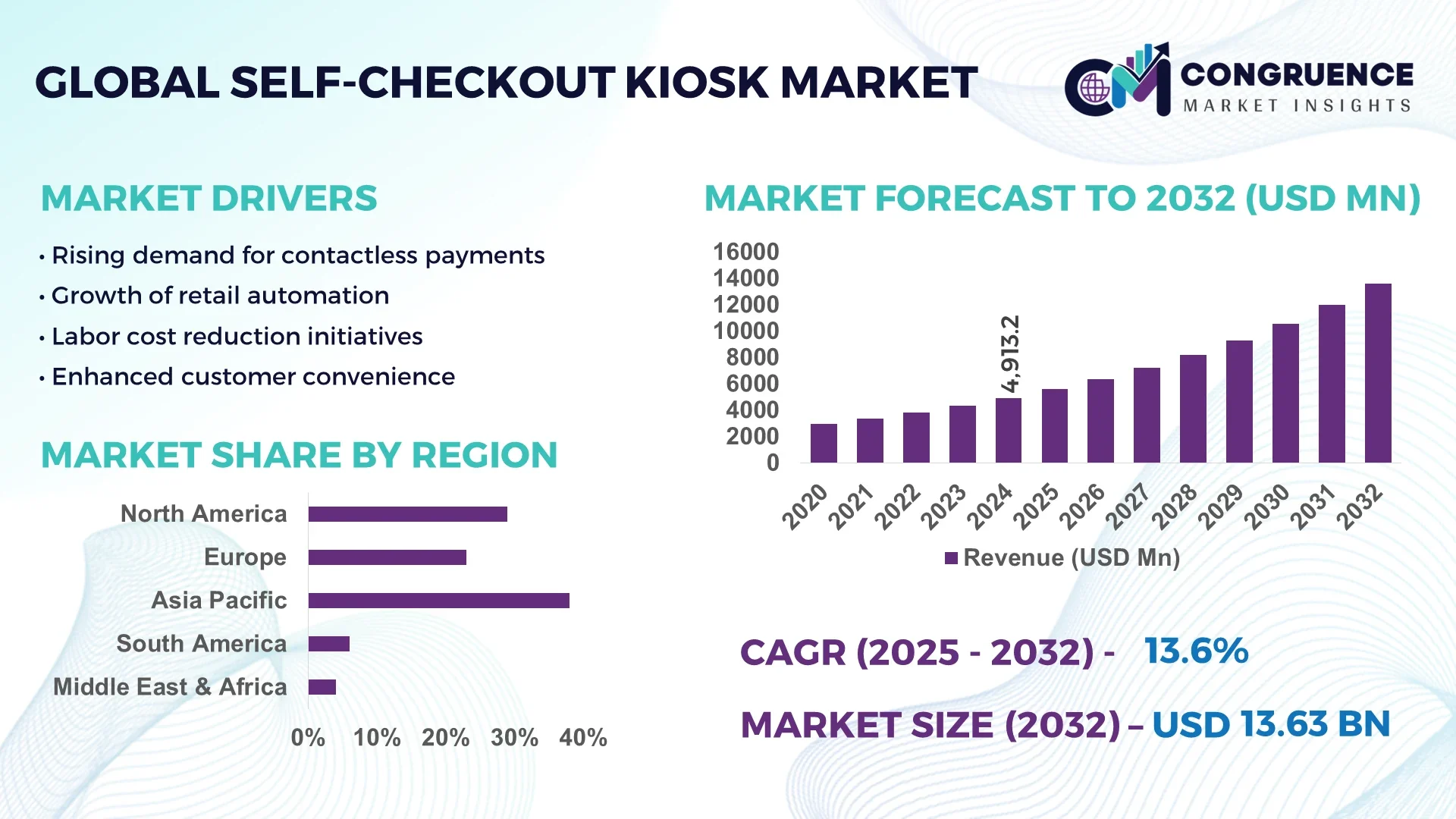

The Global Self-Checkout Kiosk Market was valued at USD 4,913.2 Million in 2024 and is anticipated to reach a value of USD 13,626.7 Million by 2032 expanding at a CAGR of 13.6% between 2025 and 2032.

In Japan, the Self-Checkout Kiosk Market demonstrates remarkable leadership: the country has significantly expanded its manufacturing capacity with multiple high-volume production facilities dedicated to kiosk assembly, supported by substantial investment from both public and private sectors. Japanese firms have deployed kiosks extensively across sectors such as convenience stores, airports, and rail stations, integrating advanced touchscreen interfaces, multilingual support, and ruggedized components to suit heavy traffic environments. Technology breakthroughs include integration of high-durability cash acceptance modules and remote monitoring systems designed to minimize downtime and simplify maintenance workflows.

The Self-Checkout Kiosk Market today is supported by a diverse array of industry applications and driving forces. The retail and grocery sectors remain foundational, accounting for the largest volume of deployments, while travel-related venues—such as airports, train stations, and hotels—have rapidly adopted kiosks to streamline check-in, payment, and service functions. Innovations include the introduction of modular plug-and-play hardware architectures, AI-powered error detection modules, and seamless mobile-to-kiosk handoff systems. Regulatory frameworks now mandate accessibility features—such as tactile buttons, adjustable screen heights, and audio-assist modes—enhancing usability and compliance globally. Environmental factors, including reductions in energy consumption via low-power display technologies and eco-friendly manufacturing materials, are gaining traction as companies seek sustainable deployments. Economic drivers include rising labor costs and demands for contact-light customer experience. Emerging trends include retrofittable retrofit AI units for legacy kiosk fleets, integration of loyalty-program interfaces at checkout points, and regional preferences—for instance, Latin American kiosks often include biometric PIN pads for enhanced security, while Southeast Asian units favor QR-code-based payments. The future outlook points toward convergence of self-checkout with mobile apps, digital wallets, and omni-channel loyalty systems, delivering a unified, highly efficient retail and service experience.

Artificial Intelligence is increasingly integral to the Self-Checkout Kiosk Market, delivering tangible improvements in operational performance, theft reduction, user guidance and decision-maker analytics. Modern AI-enhanced kiosks employ computer vision and machine learning to accurately recognize un-barcoded and visually similar items, minimizing the need for manual lookup and reducing error rates during scanning. At major retailers, AI-powered self-checkout systems now automatically detect un-scanned or mis-scanned items in real time, often alerting staff only when intervention is necessary—effectively reducing loss prevention interventions whilst maintaining seamless throughput.

Efficiency gains are measurable. For example, AI-driven kiosks utilizing computer vision have reduced transaction handling time by observing product movement rather than sequential barcode scanning, accelerating throughput especially in high-volume environments. AI systems also facilitate dynamic queue management: sensors powered by AI monitor kiosk usage, and automatically redirect customers to open lanes or deploy mobile checkout units as needed, balancing load and reducing wait times. Error correction improvements are notable—miss-scans or weight mismatches are detected and corrected with minimal interruption, enhancing reliability.

Employee roles have evolved concurrently. With AI‐empowered kiosks capable of self-error correction, about 80% of customers can resolve minor scanning mistakes when prompted, shifting staff from crisis management roles to service and guidance roles—improving workforce satisfaction and reducing conflict points.

Additionally, AI platforms in Self-Checkout Kiosk Market enable smart analytics: kiosks now capture anonymized behavioral data—such as item misplacement frequencies, peak traffic patterns, and common touchpoints—allowing operational teams to refine interface layouts, staff allocation, and maintenance schedules. Over time, these insights support predictive servicing, reducing kiosk downtime and ensuring consistent uptime.

In sum, AI’s role in the Self-Checkout Kiosk Market is no longer peripheral—it is a core driver of reliability, user experience, and operational intelligence, essential for strategic decision-makers aiming to modernize checkout infrastructure across industries.

“In early 2025, a US grocery chain expanded its deployment of AI-powered Mashgin self-checkout kiosks—which use computer vision to recognize multiple items instantly without barcode scanning—demonstrating nearly 100% accuracy and reducing transaction times to a median of just 18.7 seconds.”

The Self-Checkout Kiosk Market is characterized by intensifying digital transformation, evolving consumer preferences, and operational modernization. As retailers strive to deliver speed and autonomy, decision-makers invest in kiosk networks that unify payment, loyalty integration, and customer guidance—all while supporting evolving regulatory expectations. Technological modularization enables rapid deployment and easier scalability, while data-driven performance insights inform continuous optimization. Global differences persist: mature markets emphasize efficiency and integration, while emerging markets focus on mobile payment compatibility and cost-effective phasing out of staff-intensive checkout. Taken together, the market dynamics reflect a shift from standalone cashiers to intelligent, adaptive, and outcome-oriented checkout ecosystems, centered on reducing friction and elevating user satisfaction.

The rise in consumer preference for contactless and autonomous interaction has become a dominant driver within the Self-Checkout Kiosk Market. Surveys show that a significant majority of consumers—from younger demographics to time-constrained shoppers—favor self-checkout options over traditional staffed lanes due to greater speed and convenience. Retailers respond by expanding kiosk placement and functionality, integrating features like touchless payment, intuitive UI, and multilingual support. This shift not only aligns with elevated health and safety expectations but also enables retailers to reassign staff to higher-value tasks. The trend reinforces kiosks as a strategic asset in customer experience design, prompting investments in kiosk footprint and user assistance architecture.

A key restraint in the Self-Checkout Kiosk Market lies in integrating new kiosk technologies with existing legacy systems. Many organizations still operate older POS frameworks, making seamless integration of kiosk interfaces, loyalty platforms, and back-end inventory systems technically challenging. Incompatibility issues can lead to transaction errors, reporting discrepancies, and maintenance complexity. Additionally, retrofitting AI modules into older kiosks may require hardware upgrades, increasing upfront costs and system downtime. These technical and operational hurdles slow deployment speeds and extend project timelines, compelling decision-makers to invest in middleware or phased replacement strategies rather than immediate overhauls.

Emerging opportunities in the Self-Checkout Kiosk Market include increasing deployment outside traditional retail, particularly within sectors like healthcare and public transportation. Hospitals and clinics are piloting kiosks for patient check-in, wayfinding, and payment processing, enabling administrative task automation and reduced staff queues. Similarly, transit hubs—such as train stations and airports—are introducing self-checkout kiosks for ticketing, baggage check-in, and payment handling. These vertical expansions leverage the core kiosk platform while enhancing service delivery in complex, high-footfall environments. Adoption in such sectors positions kiosk technology as a universal interface for service commerce, not just retail.

A persistent challenge for the Self-Checkout Kiosk Market is the escalating cost associated with hardware lifecycle management, especially in high-traffic environments. Kiosks suffer wear on touchscreens, scanners, and payment modules, necessitating regular maintenance or replacements. Decision-makers face budgeting pressures for durable, vandal-resistant components and remote monitoring systems. These investments, while essential for uptime and user satisfaction, increase total cost of ownership. Delayed maintenance due to budgeting constraints can degrade customer experience and tarnish brand reputation—highlighting the need for strategic planning around durable hardware procurement, predictive servicing, and lifecycle cost management.

Modular & Prefabricated Hardware Adoption Accelerates: The Self-Checkout Kiosk Market is embracing modular construction design—prefabricated kiosk elements, such as standardized touchscreen modules and mounting frames, are assembled off-site using high-precision automated equipment. This approach reduces onsite labor demands and shortens deployment timelines. Demand for such precision components is increasing in regions such as Europe and North America, where operational speed and cost control are critical.

Retailers Prioritize AI-Augmented Theft Mitigation: Kiosks now integrate AI-enabled vision systems capable of detecting un-scanned items or visual mismatches in real time. These systems alert staff discretely, reducing shrink while preserving transaction speed. Deployment in high-traffic grocery and convenience segments has measurably improved loss prevention without degrading customer throughput.

Sustainability in Kiosk Design Gains Traction: Self-Checkout Kiosk Market participants are incorporating energy-efficient LED displays, recyclable composite plastics, and low-power standby modes as part of green product initiatives. Operationally, kiosks now utilize remote diagnostics to reduce service visits, cutting carbon footprint in maintenance logistics.

Cross-Channel Loyalty Integration at Checkout: Emerging Self-Checkout kiosks now feature embedded loyalty program interfaces, enabling real-time discount application, targeted offers, and mobile-to-kiosk handoffs. Customers can scan app codes or loyalty cards, instantly view personalized promotions, and complete transactions within the same interface—enhancing user engagement at the point of sale.

The Self-Checkout Kiosk Market demonstrates a diverse segmentation pattern shaped by product types, application areas, and end-user preferences. Variations in design, functionality, and deployment scale define the strategic choices made by decision-makers across industries. By type, the market includes cash-based kiosks, cashless kiosks, hybrid kiosks, and specialty models designed for niche use. Applications span retail, hospitality, transportation, healthcare, and entertainment sectors, each exhibiting distinct adoption trends. End-user insights further illustrate strong demand from large retail chains, quick-service restaurants, airports, and hospitals, alongside growing uptake in small businesses and local stores. The segmentation reveals that advanced technological integration, such as biometric authentication, AI-driven recognition, and omni-channel payment support, influences purchasing decisions across categories.

The Self-Checkout Kiosk Market by type consists of cash-based kiosks, cashless kiosks, hybrid kiosks, and specialized variants. Cash-based kiosks remain the most widely adopted, primarily due to their ability to handle traditional transactions in regions where cash continues to dominate consumer preferences. These kiosks integrate secure bill validators and coin dispensers, ensuring they can serve large customer bases with minimal friction. Cashless kiosks are gaining momentum as digital payment adoption accelerates globally, fueled by contactless card usage and mobile wallet penetration. This segment represents the fastest-growing category, particularly in developed economies where cash usage is declining. Hybrid kiosks, combining both cash and digital functionality, serve as transitional solutions in markets shifting gradually from cash to digital-first economies, offering versatility to operators. Specialty kiosks, tailored for applications such as ticketing, foodservice, or healthcare, hold niche importance by catering to unique sector-specific requirements. Collectively, these segments illustrate how consumer payment preferences and infrastructure readiness shape market direction.

The application landscape for the Self-Checkout Kiosk Market spans retail, hospitality, transportation, healthcare, and entertainment. Retail is the dominant application, driven by supermarkets, hypermarkets, and convenience stores that prioritize efficiency and reduced checkout times. The increasing deployment of kiosks across grocery chains reinforces this sector’s leadership position, as it addresses both customer satisfaction and workforce optimization. Hospitality is emerging as the fastest-growing application, with hotels and quick-service restaurants rapidly deploying kiosks for guest check-in, ordering, and payment functions. This growth is propelled by rising demand for faster service delivery and enhanced customer interaction. Transportation also plays a significant role, particularly in airports and train stations, where kiosks streamline ticketing and baggage processes. Healthcare adoption is steadily rising, with kiosks being used for patient registration and billing functions, helping hospitals reduce administrative bottlenecks. Entertainment venues, including cinemas and amusement parks, adopt kiosks to enhance ticketing efficiency. Each application highlights sector-specific demands influencing kiosk integration.

End-user segmentation within the Self-Checkout Kiosk Market highlights the prominence of large retail chains as the leading adopters. Supermarkets and hypermarkets dominate due to their high transaction volumes, extensive customer bases, and ongoing focus on operational efficiency. These organizations leverage self-checkout to optimize staffing levels and improve throughput during peak periods. Quick-service restaurants represent the fastest-growing end-user segment, as self-order and self-payment solutions help streamline operations and reduce wait times, particularly in urban areas with high customer turnover. Airports and transportation hubs follow closely, employing kiosks to manage growing passenger flows while improving service delivery. Hospitals and clinics are steadily integrating kiosks into patient-facing processes, enhancing check-in and payment efficiency. Smaller businesses, including local retailers and specialty stores, are beginning to adopt kiosks at a gradual pace, leveraging compact and cost-effective models tailored to their scale. Together, these end-user categories reveal an expanding adoption spectrum, underscoring the kiosk’s role as a versatile solution across industries.

Asia-Pacific accounted for the largest market share at 38% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2025 and 2032.

The Asia-Pacific region is strongly supported by advanced manufacturing hubs, increasing retail modernization, and rapid deployment across countries such as Japan, China, and India. North America, on the other hand, benefits from high digital payment adoption, widespread retail investment, and significant technological innovation in AI-driven kiosk solutions. Together, these regions set the tone for global expansion, shaping the strategic direction of the Self-Checkout Kiosk Market worldwide.

North America held approximately 29% market share in 2024, driven by the widespread adoption of kiosks across supermarkets, hypermarkets, and quick-service restaurants. The U.S. and Canada lead deployments, supported by strong retail digitization programs and early adoption of AI-enhanced systems. Government initiatives promoting cashless transactions and accessibility compliance standards have accelerated adoption across multiple industries. Technological trends, such as biometric authentication and cloud-based monitoring, are shaping future deployments. Large-scale investments in retail automation and the integration of loyalty-program interfaces further strengthen North America’s leadership in digital transformation of customer-facing systems.

Europe accounted for nearly 23% of global share in 2024, with Germany, the UK, and France being key adopters of self-checkout solutions. European markets emphasize sustainability initiatives, incorporating kiosks designed with recyclable materials and low-energy components. Regulatory bodies enforce stringent accessibility and data protection standards, shaping product designs to ensure compliance. Retailers across the region are also experimenting with advanced features such as multilingual interfaces and AI-based theft mitigation. Investments in digital payment ecosystems and cross-border e-commerce integration are enhancing kiosk deployment in both developed and emerging European markets.

Asia-Pacific dominated the Self-Checkout Kiosk Market in 2024 with the largest share of 38%, led by Japan, China, and India. Japan remains the technological hub, with extensive manufacturing capacity, advanced payment module innovations, and integration of ruggedized systems for heavy-use environments. China is rapidly expanding deployments across supermarkets and transportation hubs, supported by widespread mobile wallet adoption. India is emerging with strong investments in smart retail infrastructure and digital-first payment ecosystems. Regional tech hubs across Japan and South Korea continue to pioneer AI-driven kiosks, reinforcing Asia-Pacific’s role as both a production center and consumer market leader.

South America captured approximately 6% of the global market in 2024, with Brazil and Argentina at the forefront of adoption. Brazil’s growing retail infrastructure and modernization of shopping complexes are driving kiosk installations. Argentina is seeing rising demand within both transportation hubs and convenience store chains. Governments in the region are supporting digital payment adoption through incentives and favorable trade policies. Infrastructure developments, particularly in urban centers, are accelerating demand for kiosks designed to handle high traffic volumes. The market is steadily advancing with localized customization and competitive pricing strategies.

The Middle East & Africa represented around 4% of the global market in 2024, with the UAE and South Africa emerging as key growth contributors. Demand is rising in sectors such as oil & gas, retail, and construction, where modernization drives adoption of automation. The UAE leads in retail digitalization, supported by government smart city initiatives, while South Africa focuses on expanding retail and hospitality kiosks to meet rising consumer demand. Regional adoption of AI-driven payment verification and multilingual kiosks highlights the ongoing technological transformation. Trade partnerships and government investments in digital infrastructure further accelerate market growth.

Japan – 18% Market Share

High production capacity, advanced payment technology integration, and strong retail deployment across convenience stores and transportation hubs.

United States – 15% Market Share

Robust demand from supermarkets, hypermarkets, and quick-service restaurants supported by digital transformation and AI-driven retail automation.

The global Self-Checkout Kiosk Market is highly competitive, with over 35 active players operating across international and regional levels. Competition is characterized by rapid technological innovation, aggressive expansion into new retail segments, and strategic collaborations with payment technology providers. Leading companies maintain a strong market position by focusing on product differentiation through enhanced user interfaces, integration of AI-driven features, and mobile wallet compatibility. In recent years, the competitive environment has been shaped by mergers and acquisitions aimed at strengthening product portfolios and extending geographic reach. Partnerships between kiosk manufacturers and large retail chains have become increasingly common, ensuring widespread deployment across high-traffic environments. Moreover, investment in modular and customizable kiosk solutions is gaining momentum, enabling vendors to cater to both large enterprises and small retail outlets. Continuous innovation in biometric authentication, RFID integration, and cloud-based monitoring underscores the evolving nature of competition, while smaller players are capitalizing on niche applications such as hospitality and transportation.

NCR Corporation

Toshiba Global Commerce Solutions

Diebold Nixdorf, Incorporated

Fujitsu Limited

Pan-Oston

ECR Software Corporation (ECRS)

ITAB Shop Concept AB

Olea Kiosks Inc.

Pyramid Computer GmbH

HP Inc.

Digimarc Corporation

Mashgin, Inc.

The Self-Checkout Kiosk Market is undergoing a significant technological transformation, driven by digital innovation, automation, and evolving consumer preferences. Biometric authentication technologies such as fingerprint and facial recognition are becoming increasingly integrated to enhance security and reduce fraud. RFID tagging and scanning capabilities are streamlining product identification, minimizing human error, and accelerating checkout times. The adoption of AI-powered vision systems is enabling kiosks to automatically detect items without barcode scanning, which is particularly useful for fresh produce and untagged goods.

Mobile wallet integration, including NFC-based payments, is now a standard feature, meeting the growing demand for contactless transactions. Cloud connectivity is another key technological driver, allowing real-time monitoring, remote updates, and predictive maintenance. This not only improves system uptime but also enables retailers to gain insights into consumer behavior through advanced analytics. Voice-enabled interfaces and multilingual support are being deployed to improve accessibility and enhance user experience in diverse regions.

Emerging trends include the development of hybrid kiosks that combine cash and cashless functionalities, offering flexibility across markets where cash transactions remain dominant. Augmented reality (AR) and interactive digital displays are being piloted in some regions, aimed at engaging customers beyond transaction completion. Additionally, modular kiosk designs with customizable hardware configurations are empowering retailers to scale solutions according to store size and customer demand. Collectively, these advancements are positioning self-checkout kiosks as intelligent, adaptive, and customer-centric solutions for the global retail and service industries.

In January 2023, NCR Corporation expanded its self-checkout product line by introducing AI-enabled kiosks designed to improve item recognition accuracy. The new systems also integrate with loyalty programs, enhancing customer engagement and reducing transaction errors.

In June 2023, Diebold Nixdorf launched a next-generation self-checkout solution with modular hardware that allows retailers to customize payment configurations. This innovation supports cash, card, and mobile payments, aligning with diverse consumer preferences.

In February 2024, Toshiba Global Commerce Solutions unveiled its vision-based self-checkout technology that eliminates barcode scanning for produce and loose items. The system leverages AI image recognition to increase transaction speed and reduce shrinkage.

In May 2024, Fujitsu announced a strategic partnership with a major Asian retail chain to deploy hybrid self-checkout kiosks across 500 stores. The rollout focuses on cash and digital wallet compatibility, targeting both urban and semi-urban markets.

The Self-Checkout Kiosk Market Report provides a comprehensive analysis of the industry, covering multiple dimensions of the global landscape. The report examines the market through key segmentation parameters including type, application, and end-user, enabling stakeholders to understand performance across cash-based, cashless, hybrid, and specialty kiosks. Applications analyzed include retail, hospitality, transportation, healthcare, and entertainment, each representing distinct adoption patterns and consumer touchpoints. End-user categories such as large retail chains, quick-service restaurants, and transportation hubs are profiled to capture their influence on demand dynamics.

Geographically, the report spans all major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—highlighting both mature and emerging markets. Regional insights emphasize adoption drivers such as digital payment ecosystems, regulatory compliance requirements, and infrastructure development. The report also addresses technology adoption trends, including AI, biometrics, RFID, and cloud-based systems, providing a forward-looking view of innovation shaping the industry.

Additionally, the scope extends to competitive analysis, profiling the strategies of leading companies and highlighting recent developments that influence market positioning. It also explores niche segments and emerging opportunities in underpenetrated industries such as healthcare and entertainment. By offering quantitative and qualitative insights into market dynamics, segmentation, regional trends, and technology outlooks, the report serves as a strategic resource for decision-makers, investors, and industry professionals seeking to evaluate growth opportunities in the Self-Checkout Kiosk Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,913.2 Million |

| Market Revenue (2032) | USD 13,626.7 Million |

| CAGR (2025–2032) | 13.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | NCR Corporation, Toshiba Global Commerce Solutions, Diebold Nixdorf Incorporated, Fujitsu Limited, Pan-Oston, ECR Software Corporation (ECRS), ITAB Shop Concept AB, Olea Kiosks Inc., Pyramid Computer GmbH, HP Inc., Digimarc Corporation, Mashgin Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |