Reports

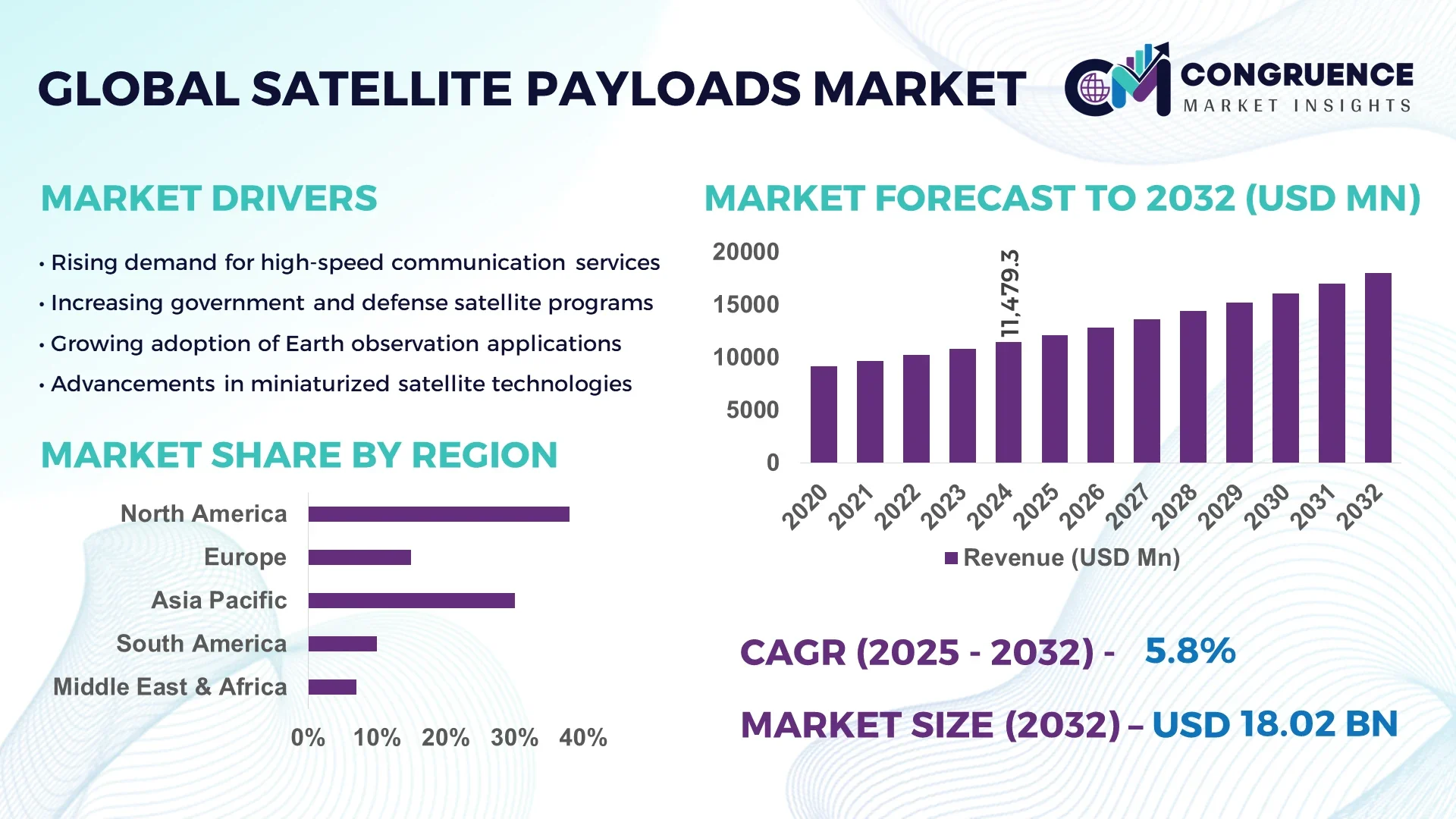

The Global Satellite Payloads Market was valued at USD 11479.3 Million in 2024 and is anticipated to reach a value of USD 18021.9 Million by 2032 expanding at a CAGR of 5.8% between 2025 and 2032.

The United States demonstrates formidable production capacity and investment levels in satellite payload technologies, with robust infrastructure supporting high-throughput communication, precision imaging, and scientific payload development. Its capabilities are further strengthened by continuous funding for research and development in advanced optical systems and miniaturized sensors, alongside deployment in key sectors such as defense, remote sensing, and telecommunications.

Key industry sectors in the Satellite Payloads Market include communication payloads, imaging payloads, navigation systems, scientific experimentation instruments, and technology demonstration modules. Communication payloads remain predominant, while software-defined and modular payloads are experiencing fast growth with demand driven by the need for flexible, reconfigurable, and cost-efficient platforms. Low Earth Orbit (LEO) systems continue to dominate deployment, benefiting from rapid advancements in small satellite constellations and mega-network projects. Regulatory drivers such as spectrum allocation and space debris management influence payload design, while economic incentives, including rising demand for broadband and Earth observation services, support expansion. Regions like Asia-Pacific, particularly driven by India, China, and Japan, are witnessing accelerated adoption. Emerging trends include hyperspectral imaging, agile beamforming, modular reconfigurable payloads, and advanced environmental sensing, underpinned by innovations in AI integration and sustainable satellite design.

AI is fundamentally transforming the Satellite Payloads Market by embedding real-time autonomy, advanced analytics, and intelligent processing directly onboard satellite systems. In communication payloads, AI enables adaptive beamforming, interference detection, and spectrum management, dramatically enhancing signal quality and throughput. On Earth-observation missions, AI-powered data filtering, compression, and onboard analytics reduce reliance on ground transmission and deliver faster actionable insights. Predictive maintenance algorithms proactively address hardware anomalies, optimizing payload uptime and extending operational life. AI-driven design and simulation tools help engineers optimize payload weight, functionality, and resilience, shortening development cycles and reducing costs. In constellation operations, autonomous scheduling, routing, and coordination improve efficiency and mission responsiveness across large satellite fleets. Across commercial, defense, and scientific applications, the integration of AI is driving measurable improvements in speed, performance, and adaptability, signaling a major transformation of the Satellite Payloads Market.

"2024 witnessed the successful demonstration of Dynamic Targeting technology aboard an AI-enabled satellite that autonomously analyzed cloud cover in under 90 seconds while orbiting at high velocity, allowing immediate adjustments for capturing clear imagery and eliminating unnecessary data collection."

The Satellite Payloads Market is experiencing steady transformation driven by advancements in modular designs, miniaturization, and enhanced data processing capabilities. Shifts in global communication needs, expanding Earth observation applications, and defense modernization programs are key forces shaping demand. The adoption of Low Earth Orbit constellations is boosting payload integration, with flexible and reconfigurable payloads enabling real-time adjustments and greater mission versatility. Government funding, private investments, and rising collaboration between aerospace companies and technology providers are strengthening the competitive landscape. Additionally, the growing use of AI-enabled payloads, hyperspectral imaging, and environmentally sustainable designs reflects a clear trajectory toward smarter, more adaptive, and resilient satellite payload solutions.

The growing reliance on satellite-based communication and imaging services is a significant driver for the Satellite Payloads Market. Rising global demand for high-speed internet, especially in underserved and remote regions, is accelerating the deployment of communication payloads with advanced transponders and high-throughput capabilities. Earth observation payloads are increasingly utilized for precision agriculture, urban planning, disaster management, and climate monitoring, delivering valuable insights across industries. The surge in Low Earth Orbit satellite networks further boosts payload demand, as operators require compact yet powerful systems capable of supporting broadband, imaging, and surveillance functions. These evolving requirements underscore the importance of adaptable payloads that deliver both performance and cost-efficiency in diverse operational environments.

Despite the strong outlook, the Satellite Payloads Market faces significant restraints associated with high development costs and regulatory complexities. Designing payloads that meet advanced performance criteria requires sophisticated materials, extensive testing, and precision engineering, all of which elevate costs and extend project timelines. Furthermore, international regulatory frameworks governing frequency allocation, spectrum rights, and orbital slot coordination add to compliance burdens, limiting flexibility for operators. Smaller enterprises face entry barriers due to both the financial requirements and the stringent approval processes. These factors collectively slow down market penetration for new entrants and increase pressure on established players to maintain technological and regulatory readiness.

The transition toward AI-powered and software-defined payloads presents a major opportunity for the Satellite Payloads Market. AI integration allows satellites to process data in orbit, adapt to changing mission requirements, and reduce reliance on ground infrastructure, enabling faster and more efficient service delivery. Software-defined payloads bring flexibility by reprogramming frequency bands, beam coverage, and signal processing mid-mission, extending the functional lifespan of satellites. With the increasing demand for real-time decision-making, defense and commercial sectors are prioritizing investment in these next-generation payloads. This trend not only expands market scope but also fosters innovation in payload design, creating lucrative opportunities for technology providers and satellite manufacturers.

A critical challenge in the Satellite Payloads Market is the growing issue of orbital congestion and long-term sustainability. The rapid deployment of thousands of satellites in Low Earth Orbit raises concerns about collision risks, debris accumulation, and long-term operational safety. Payload developers must design systems that are not only lightweight and efficient but also aligned with sustainability measures such as debris mitigation technologies and end-of-life disposal strategies. Compliance with emerging international space sustainability guidelines further increases design complexity and operational costs. As satellite constellations expand, ensuring payload durability, safe disposal, and resilience against debris impacts remains a pressing challenge that influences both industry practices and policy frameworks.

• Expansion of Software-Defined Payloads: Software-defined payloads are rapidly gaining traction as operators prioritize flexibility and reconfigurability. Unlike traditional payloads with fixed functions, these systems can be reprogrammed mid-mission, allowing operators to adjust frequency bands, beam coverage, and mission parameters in real time. This adaptability extends the operational lifespan of satellites while reducing costs associated with building and launching new units. Adoption is particularly strong in communication satellites, where demand for bandwidth and coverage changes frequently, necessitating highly agile payload systems.

• Growth of Hyperspectral Imaging Payloads: Hyperspectral imaging is emerging as a powerful trend in the Satellite Payloads Market, with applications spanning defense, agriculture, mineral exploration, and disaster management. Payloads equipped with hyperspectral sensors can capture data across hundreds of spectral bands, offering unparalleled accuracy in identifying materials and monitoring environmental changes. Recent innovations in miniaturization have enabled the integration of these complex sensors into smaller satellites, broadening access and cutting deployment costs. Demand is rising in Asia-Pacific, where governments are investing heavily in precision agriculture and climate monitoring solutions.

• Increased Deployment of Low Earth Orbit Constellations: The proliferation of LEO satellite constellations is reshaping payload demand, creating the need for compact, lightweight, and energy-efficient payloads capable of supporting global broadband networks. With thousands of satellites projected to be launched annually, payload designs are evolving toward modularity and reduced production costs. These constellations demand high-throughput communication and data processing payloads that can function seamlessly in large-scale networks. This trend is driving partnerships between aerospace manufacturers and technology firms to meet stringent requirements for rapid deployment and operational resilience.

• Integration of AI and Machine Learning in Payloads: AI and machine learning integration has become a defining trend, enabling payloads to analyze data, make autonomous decisions, and optimize resources in orbit. These smart payloads reduce the need for constant ground communication and enable real-time insights for applications such as surveillance, environmental monitoring, and communication management. AI-enabled predictive maintenance further enhances payload reliability by identifying anomalies before they escalate. As industries and governments push for faster, more efficient data services, AI-powered payloads are becoming essential to delivering performance and operational adaptability.

The Satellite Payloads Market is segmented by type, application, and end-user, reflecting diverse technological and operational requirements. By type, communication payloads dominate due to their indispensable role in global connectivity, while software-defined and imaging payloads are witnessing accelerated adoption driven by technological innovation. Applications span communication, Earth observation, navigation, scientific research, and technology demonstration, with communication holding the leading share and Earth observation expanding rapidly. End-users include commercial enterprises, government organizations, defense agencies, and research institutions, each with unique requirements ranging from broadband delivery to security surveillance. Increasing investments across all segments highlight a dynamic market environment shaped by evolving demands, rapid technological integration, and cross-sector collaboration.

Communication payloads represent the leading type, owing to their critical role in enabling satellite-based broadband, television broadcasting, and defense communication systems. These payloads incorporate advanced transponders and high-throughput modules, supporting the growing demand for faster, more reliable global connectivity. Software-defined payloads are the fastest-growing segment, as they allow reprogramming of functions in orbit, providing unmatched flexibility for operators facing shifting mission needs. Imaging payloads also hold significant relevance, particularly with the adoption of hyperspectral and multispectral sensors in agriculture, defense, and climate monitoring. Navigation payloads continue to serve a foundational role in supporting global positioning and geolocation services across industries. Scientific and technology demonstration payloads, though niche, provide essential platforms for testing emerging innovations and advancing space exploration objectives. Collectively, these diverse payload types illustrate the broadening technological base of the market, with adaptability and miniaturization emerging as key design priorities.

Communication applications dominate the Satellite Payloads Market, reflecting the accelerating demand for high-capacity broadband and secure communication systems. The expansion of global internet connectivity initiatives and the deployment of large constellations underscore the central role of communication payloads. Earth observation is the fastest-growing application, propelled by increasing needs in climate monitoring, disaster management, precision agriculture, and urban development. Imaging payloads integrated into small and mid-sized satellites have made Earth observation more accessible and cost-efficient. Navigation applications remain integral to transportation, logistics, and defense operations, ensuring continuity in positioning and timing services. Scientific research and experimentation applications, though relatively smaller, support critical missions in space exploration, environmental studies, and astronomy. Technology demonstration applications provide testing grounds for innovative payloads, accelerating the development of future-ready systems. These application areas highlight the diverse and evolving utility of satellite payloads across industries, each reinforcing the market’s trajectory toward advanced, multi-functional satellite ecosystems.

Government and defense agencies represent the leading end-user segment in the Satellite Payloads Market due to their reliance on secure communication, surveillance, and reconnaissance capabilities. Strategic investments in national security and intelligence gathering sustain their dominant position. The commercial sector is the fastest-growing end-user, supported by surging demand for broadband services, direct-to-home broadcasting, and enterprise-level data solutions. With increasing privatization of space activities, commercial operators are playing a pivotal role in driving innovation and scaling satellite deployments. Research institutions and universities also contribute significantly by leveraging payloads for scientific exploration, climate studies, and technology testing. Emerging space startups further diversify the end-user base, introducing innovative, cost-effective payload solutions. Collectively, these end-user segments reflect a dynamic ecosystem where public and private stakeholders are equally crucial, with commercial enterprises accelerating growth and governments ensuring mission-critical capabilities that anchor long-term market stability.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

North America continues to benefit from advanced aerospace infrastructure, strong private investments, and government-funded satellite programs. Meanwhile, Asia-Pacific is witnessing rapid adoption, fueled by increasing satellite deployments in China, India, and Japan. Europe maintains a significant share, supported by sustainability policies and technological innovation in communication payloads. South America and the Middle East & Africa are smaller but emerging markets, with strong momentum driven by defense, energy, and telecommunication requirements. Collectively, these regional dynamics highlight the diverse growth patterns shaping the global Satellite Payloads Market.

High-Throughput Connectivity and Defense Modernization Driving Payload Demand

North America accounted for nearly 38% of the global Satellite Payloads Market in 2024, underpinned by extensive deployment of high-throughput communication payloads and cutting-edge defense applications. Industries such as telecommunications, space exploration, and military intelligence dominate regional demand. Government initiatives supporting broadband expansion in rural areas and the modernization of defense systems further enhance payload deployment. Technological advancements, including AI-integrated payloads and software-defined modules, are being adopted at scale to improve flexibility and data management. Regulatory frameworks encouraging orbital sustainability and spectrum efficiency also guide market direction, strengthening the region’s leadership in next-generation satellite payload innovations.

Advancing Sustainable Payload Solutions with Emerging Space Technologies

Europe held approximately 27% of the global Satellite Payloads Market in 2024, led by major economies including Germany, the UK, and France. Strong regional focus on climate monitoring, secure communication, and Earth observation drives significant payload demand. The European Space Agency and national regulatory authorities are pushing for sustainability through debris mitigation initiatives and green propulsion systems, influencing payload design. The adoption of hyperspectral imaging payloads is gaining traction, particularly in environmental and agricultural monitoring. Technological advancements in modular and reconfigurable payloads highlight Europe’s strategy of aligning innovation with sustainable development, ensuring steady integration of next-generation systems across industries.

Expanding Satellite Constellations and Manufacturing Innovation Accelerating Growth

Asia-Pacific ranked as the fastest-growing regional contributor to the Satellite Payloads Market in 2024, accounting for close to 22% of global share. Countries including China, India, and Japan are at the forefront, with large-scale government-funded satellite programs and private-sector innovation hubs. Manufacturing clusters in China and India are expanding rapidly, enabling cost-effective production of payloads tailored to broadband and Earth observation requirements. Japan’s advancements in scientific payloads and deep-space exploration further broaden the regional scope. The strong push for high-speed internet access and growing investments in regional navigation systems demonstrate the rising significance of Asia-Pacific as a global innovation hub for satellite payload development.

Government Incentives and Telecom Expansion Supporting Payload Adoption

South America contributed nearly 6% of the global Satellite Payloads Market in 2024, with Brazil and Argentina emerging as primary demand centers. Brazil leads the region through investments in space exploration and telecommunication services, while Argentina’s contributions stem from defense and remote sensing initiatives. The market benefits from regional government incentives aimed at strengthening satellite infrastructure to expand broadband connectivity across underserved regions. Satellite payload deployment is also rising in energy and agriculture monitoring, where precision solutions support sustainable resource management. Trade policies encouraging collaboration with global aerospace firms are reinforcing South America’s role as an expanding market for payload technologies.

Energy Sector Expansion and Digital Transformation Fueling Demand

The Middle East & Africa accounted for around 7% of the Satellite Payloads Market in 2024, with the UAE and South Africa being the largest contributors. Payload adoption in the region is driven by demand for oil and gas exploration support, defense modernization, and construction monitoring. The UAE’s investments in advanced payload-equipped satellites for communication and navigation highlight the region’s growing technological focus. South Africa contributes through research-focused payloads in climate and environmental observation. Local regulations supporting satellite development and cross-border trade partnerships with international players are accelerating modernization, positioning the region as an emerging hub for satellite payload deployment.

United States: 32% market share | Leadership driven by advanced aerospace infrastructure, strong defense spending, and high production capacity in communication payloads.

China: 18% market share | Dominance supported by large-scale government programs, rapid satellite manufacturing growth, and expanding broadband satellite constellations.

The Satellite Payloads Market is characterized by a highly competitive environment with more than 40 active global players operating across communication, imaging, navigation, and scientific payload domains. The market is shaped by a mix of established aerospace manufacturers, defense contractors, and specialized technology firms competing on innovation, performance, and scalability. Companies are increasingly focusing on modular and software-defined payloads to meet rising demand for flexibility and reconfigurability. Strategic initiatives such as joint ventures, long-term government contracts, and partnerships with private satellite operators are central to maintaining competitive positioning. Recent trends include the integration of AI-driven payloads, deployment of lightweight miniaturized modules, and the use of additive manufacturing for faster, cost-effective production. Mergers and acquisitions are consolidating capabilities in advanced payload design and integration, while regional expansion strategies are enabling firms to capture emerging markets. Competitive intensity is further amplified by strong R&D pipelines, with firms prioritizing hyperspectral imaging, adaptive beamforming, and next-generation environmental monitoring payloads to secure technological leadership in this evolving market.

Airbus Defence and Space

Lockheed Martin Corporation

Northrop Grumman Corporation

Thales Alenia Space

Boeing Defense, Space & Security

OHB SE

L3Harris Technologies

Mitsubishi Electric Corporation

Honeywell International Inc.

Raytheon Technologies Corporation

The Satellite Payloads Market is undergoing significant technological evolution, with multiple advancements shaping performance, efficiency, and functionality. Software-defined payloads are one of the most transformative innovations, enabling satellites to dynamically reconfigure frequency bands, adjust beam coverage, and adapt to new mission requirements without the need for hardware replacement. This flexibility significantly reduces long-term costs and enhances operational lifespan. Miniaturization is another major trend, with payloads being designed to deliver high performance while reducing weight and power consumption. These compact payloads are particularly suited for small satellites and large Low Earth Orbit constellations, which require scalable and cost-effective deployment.

Hyperspectral and multispectral imaging payloads are gaining momentum in environmental monitoring, defense surveillance, and precision agriculture, offering the ability to capture hundreds of spectral bands for detailed analysis. Advances in on-board processing technologies, powered by artificial intelligence and edge computing, are enabling satellites to analyze and filter massive volumes of data in orbit, significantly lowering transmission requirements and improving response times for end-users. Additive manufacturing techniques are increasingly applied to payload components, reducing production timelines while enabling complex geometries that enhance performance. Additionally, innovations in thermal management, radiation shielding, and lightweight composite materials are improving durability and efficiency under harsh orbital conditions. Collectively, these technological advancements are positioning satellite payloads as smarter, more adaptable, and more resilient systems, aligning with the growing demand for agile and sustainable space solutions.

• In February 2023, Airbus successfully tested its software-defined payload technology on a communication satellite, allowing real-time reconfiguration of frequency and coverage areas to improve flexibility for operators serving multiple regions.

• In September 2023, Northrop Grumman launched an advanced hyperspectral imaging payload designed for defense and Earth observation missions, integrating miniaturized sensors capable of capturing over 300 spectral bands with improved resolution and efficiency.

• In April 2024, Lockheed Martin introduced an AI-enabled payload management system that performs onboard data analysis and predictive maintenance, reducing ground control reliance and extending satellite operational lifespan in geostationary orbit.

• In October 2024, Thales Alenia Space deployed a next-generation modular payload platform, capable of supporting multiple communication and imaging functions simultaneously, offering operators reduced integration costs and enhanced mission flexibility.

The scope of the Satellite Payloads Market Report encompasses a comprehensive analysis of technologies, applications, and geographic regions that collectively define the industry landscape. The report covers all major payload types, including communication, imaging, navigation, scientific, and technology demonstration payloads, with special emphasis on emerging categories such as software-defined and hyperspectral imaging payloads. Each type is assessed in terms of its operational role, technological innovation, and adoption across industries such as telecommunications, defense, climate monitoring, and scientific exploration.

Geographically, the report provides detailed coverage of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing demand patterns, infrastructure readiness, and regional innovation hubs. The application scope includes communication networks, Earth observation, navigation services, and scientific missions, offering insights into both leading and fast-growing segments. End-user analysis spans government agencies, defense organizations, commercial operators, and research institutions, highlighting unique drivers influencing procurement and adoption.

The report also focuses on technological advancements such as AI integration, additive manufacturing, and modular payload architectures, which are reshaping the industry. It explores competitive dynamics, recent developments, and sustainability initiatives that are increasingly influencing payload design and deployment. Additionally, niche segments such as small satellite payloads and next-generation constellation systems are included, reflecting the broadening scope of opportunities available to stakeholders. This structured approach ensures that decision-makers gain a holistic understanding of the global Satellite Payloads Market and its evolving trajectory.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 11479.3 Million |

|

Market Revenue in 2032 |

USD 18021.9 Million |

|

CAGR (2025 - 2032) |

5.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Airbus Defence and Space, Lockheed Martin Corporation, Northrop Grumman Corporation, Thales Alenia Space, Boeing Defense, Space & Security, OHB SE, L3Harris Technologies, Mitsubishi Electric Corporation, Honeywell International Inc., Raytheon Technologies Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |