Reports

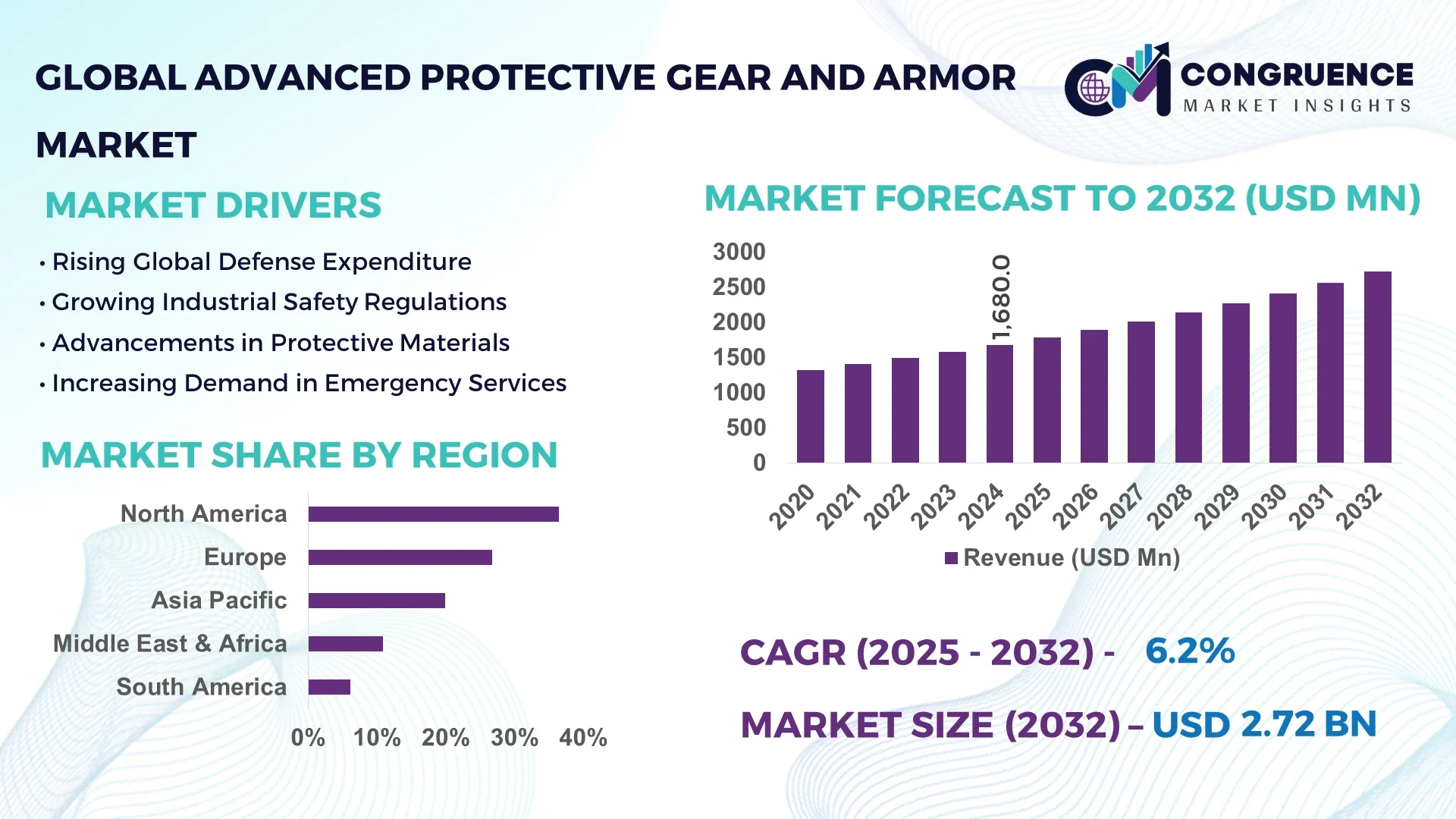

The Global Advanced Protective Gear and Armor Market was valued at USD 1,680.0 Million in 2024 and is anticipated to reach a value of USD 2,718.4 Million by 2032 expanding at a CAGR of 6.2% between 2025 and 2032. The growth is primarily driven by increasing demand for advanced defense solutions, industrial safety gear, and next-generation materials enhancing protective performance.

The United States leads the global Advanced Protective Gear and Armor Market with a robust defense manufacturing ecosystem supported by over 250 defense contractors and strong federal investment in military modernization. The country’s annual defense R&D expenditure surpassed USD 140 billion in 2024, contributing to major technological breakthroughs such as nanocomposite fibers and lightweight ballistic protection. Advanced protective gear is widely utilized across defense, law enforcement, firefighting, and aerospace sectors, with over 70% of U.S. law enforcement agencies adopting integrated body armor systems. Continuous innovation in aramid fibers and high-strength ceramics has enabled a 20% weight reduction and 30% performance enhancement in ballistic applications.

Market Size & Growth: Valued at USD 1.68 Billion in 2024, projected to reach USD 2.72 Billion by 2032, expanding at a CAGR of 6.2%. Growth is driven by rising demand for military-grade and industrial protective materials.

Top Growth Drivers: Increasing defense adoption (up 25%), technological innovation in composite materials (efficiency gain 18%), and industrial safety regulation compliance (implementation rate 32%).

Short-Term Forecast: By 2028, improved material durability and smart sensor integration expected to enhance user protection efficiency by 22%.

Emerging Technologies: Development of smart textiles, nanofiber-based armor, and AI-enabled body temperature monitoring systems.

Regional Leaders: North America (USD 1.2 Billion by 2032) leads in defense innovation; Europe (USD 780 Million) excels in industrial safety gear; Asia Pacific (USD 640 Million) demonstrates rapid adoption across manufacturing sectors.

Consumer/End-User Trends: High adoption among defense forces, firefighting units, and oil & gas industries emphasizing durability and mobility.

Pilot or Case Example: In 2024, the U.S. Army’s “Integrated Soldier Protection Program” achieved a 28% reduction in armor weight while improving impact resistance by 35%.

Competitive Landscape: 3M Company leads with an estimated 14% share, followed by DuPont, Teijin Limited, Honeywell International, and DSM.

Regulatory & ESG Impact: Compliance with ISO 11612 and REACH standards drives sustainable material innovation and 15% reduction in non-recyclable components by 2030.

Investment & Funding Patterns: Over USD 3.5 Billion invested globally in R&D and defense modernization programs targeting advanced material sciences.

Innovation & Future Outlook: Integration of AI-based monitoring, IoT-enabled safety wearables, and graphene-infused fabrics expected to redefine user safety and efficiency.

Advanced Protective Gear and Armor Market growth is supported by rising defense budgets, increasing industrial safety mandates, and advancements in fiber-reinforced composites. Innovations in nanomaterials, ergonomic design, and connected safety systems are enhancing protective performance across critical sectors such as military, aerospace, and industrial operations, positioning the market for strong, sustainable expansion through 2032.

The Advanced Protective Gear and Armor Market holds strategic relevance as a key enabler of global safety, defense readiness, and industrial protection. The industry is undergoing a transformation driven by technological convergence between material science and digital intelligence. For instance, graphene-reinforced composites deliver 35% higher tensile strength compared to traditional Kevlar-based armor. North America dominates in production volume, while Europe leads in adoption with 62% of enterprises integrating advanced body protection technologies.

By 2028, AI-driven predictive maintenance and IoT-enabled monitoring systems are expected to reduce operational downtime by 27%, improving protection reliability in defense and industrial applications. Firms are committing to ESG metrics such as a 20% reduction in hazardous material usage and a 25% increase in recyclability of protective gear by 2030. In 2024, Japan’s Defense Technology Agency achieved a 40% improvement in heat resistance through nanofiber layering initiatives.

Strategically, manufacturers are adopting circular production models and lean manufacturing to enhance resilience and cost-efficiency. The synergy between defense modernization, workplace safety compliance, and sustainable material innovation positions the Advanced Protective Gear and Armor Market as a pillar of resilience, compliance, and sustainable growth through 2032 and beyond.

The Advanced Protective Gear and Armor Market is characterized by rapid technological progress, increasing defense spending, and stringent safety mandates across multiple industries. Growing investment in nanotechnology and smart fabrics has redefined material performance standards. Demand is also being shaped by workforce safety regulations in oil & gas, mining, and construction industries. Advancements in lightweight composites, ergonomic designs, and digital integration are enabling higher adoption across both military and civilian sectors, driving consistent innovation and competitive intensity within the market.

Continuous advancements in material science—such as aramid fibers, ultra-high molecular weight polyethylene (UHMWPE), and nanocomposite coatings—are significantly improving durability, flexibility, and heat resistance of protective gear. Smart textiles embedded with biosensors allow real-time monitoring of temperature, pressure, and body movements, enhancing situational awareness for defense and emergency responders. The global production of high-performance protective fibers increased by over 18% in 2024, indicating rapid scaling of technological adoption.

The high cost of specialized materials, combined with complex supply chains for advanced polymers and ceramics, remains a critical restraint. Manufacturing high-grade armor requires specialized equipment and precision engineering, driving up operational expenses. In 2024, material procurement and energy costs accounted for over 45% of total production expenditure. Moreover, limited global suppliers of ballistic-grade fibers create price volatility and procurement delays, hindering small and mid-sized manufacturers from achieving scale efficiency.

The integration of smart sensors, AI analytics, and IoT-enabled features in protective gear presents significant opportunities. Smart armor systems can monitor vital signs, detect environmental hazards, and transmit real-time data to command centers. With wearable technology adoption in industrial and defense applications projected to rise by 30% by 2028, companies investing in intelligent protective systems are well-positioned to capitalize on growing demand for connected safety solutions.

Recycling advanced composite and polymer-based armor materials poses a significant challenge due to their complex chemical composition. Disposal of outdated or damaged protective gear generates environmental concerns, as less than 25% of used armor materials are currently recyclable. Increasing environmental compliance regulations in Europe and North America are compelling manufacturers to develop eco-friendly substitutes and adopt closed-loop recycling processes—necessitating high R&D costs and longer product development cycles.

Adoption of Smart Sensor-Integrated Armor Systems: Over 40% of defense and industrial organizations have begun adopting wearable armor integrated with biometric and environmental sensors, enabling real-time hazard detection and 22% faster response times. This shift toward connected protective solutions is expected to revolutionize field operations and improve user safety standards globally.

Rise in Lightweight Composite Materials: The use of UHMWPE and carbon nanotube-reinforced polymers has increased by 28% since 2022, reducing armor weight by up to 35% without compromising ballistic resistance. This trend aligns with the growing need for mobility and ergonomics in defense and first-responder applications.

Growth of Circular and Sustainable Manufacturing Practices: Approximately 45% of manufacturers are investing in eco-friendly production processes, with 18% already using recycled polymers and bio-based resins. These practices have contributed to a 25% decline in non-recyclable waste output between 2020 and 2024.

Expansion of Civil and Industrial End-User Adoption: Civil defense and industrial safety sectors collectively accounted for 38% of global consumption in 2024. Enhanced PPE standards in construction, mining, and oil & gas are driving new procurement contracts, with Asia Pacific recording a 31% year-over-year increase in protective gear demand.

The Advanced Protective Gear and Armor Market is segmented by type, application, and end-user, each contributing distinct value to the industry landscape. By type, the market encompasses body armor, headgear, protective clothing, footwear, and others, with body armor holding the most substantial adoption share due to its extensive use in defense and law enforcement. By application, the market spans defense, industrial, construction, firefighting, and healthcare sectors, with defense remaining dominant. End-user segmentation highlights military, law enforcement, and industrial users as primary demand drivers, reflecting growing investments in advanced safety standards and wearable protection systems. The segmentation structure emphasizes technology diversification, shifting from traditional ballistic systems to intelligent, sensor-equipped protective equipment optimized for real-time performance monitoring and superior impact resistance.

Among the product types, body armor currently accounts for 46% of total adoption, driven by continuous modernization initiatives in defense and law enforcement agencies. Lightweight ballistic vests made from ultra-high molecular weight polyethylene (UHMWPE) and aramid fibers have improved mobility and heat resistance by up to 25%, ensuring enhanced comfort and tactical performance. Headgear and helmets follow with a 21% share, supported by innovations in composite materials and improved shock absorption designs. Protective clothing—including fire-resistant and chemical-resistant suits—holds a 17% share, favored in industrial and firefighting applications. Footwear and others collectively represent the remaining 16% of the market, serving specialized segments like hazardous materials handling and aerospace protection. The fastest-growing segment is protective clothing, expected to expand at an estimated CAGR of 7.1% owing to increasing safety regulations across construction, energy, and healthcare sectors. Enhanced integration of nanofiber membranes and moisture-wicking technologies is propelling this growth.

The defense and military sector dominates with approximately 49% of total market adoption, driven by national security investments, modernization programs, and rising geopolitical tensions. Advanced protective gear is extensively used across combat, tactical, and training environments to ensure enhanced survivability and operational efficiency. Industrial and manufacturing applications follow with 26% adoption, particularly in oil & gas, mining, and heavy engineering sectors, where worker safety compliance remains a critical priority. The firefighting and emergency response segment holds around 15% share, while construction and healthcare together contribute 10% of the market, benefiting from stricter workplace safety norms. The fastest-growing application is industrial safety, expanding at an estimated CAGR of 7.4%, fueled by increasing automation, stricter occupational safety laws, and deployment of smart PPE systems. In 2024, over 41% of global manufacturing facilities reported integrating connected safety gear to reduce injury rates and improve real-time incident response. Similarly, 38% of enterprises across North America and Europe implemented IoT-linked protective solutions for employee monitoring and hazard detection.

Military and defense organizations represent the leading end-user group, accounting for 52% of total consumption of advanced protective gear and armor in 2024. Their dominance stems from large-scale procurement programs, advanced R&D spending, and consistent modernization of combat equipment. Law enforcement agencies hold approximately 28% share, driven by adoption of lightweight, multi-threat protection systems for tactical and riot control applications. The industrial and commercial user base represents 20% of market activity, with growing uptake in construction, mining, and oil & gas operations to meet enhanced regulatory safety standards. The fastest-growing end-user group is the industrial sector, expanding at an estimated CAGR of 7.6% due to the increased focus on workplace safety digitization and the integration of smart wearable technologies. In 2024, over 36% of global industrial enterprises reported deploying advanced protective equipment with embedded sensors for monitoring heat exposure and environmental hazards. Additionally, 44% of construction companies in Asia Pacific indicated ongoing trials of smart PPE integrated with predictive safety analytics.

North America accounted for the largest market share at 36.4 % in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8 % between 2025 and 2032.

In 2024, North America’s demand was estimated at roughly 612 million (USD-equivalent units), followed by Europe at 450 million and Asia Pacific at 380 million. The Middle East & Africa and South America accounted for smaller volumes of ~120 million and 85 million, respectively. North America maintains leadership due to heavy defense procurement and mature industrial safety infrastructure, while Asia Pacific’s growth is propelled by rising industrialization, infrastructure spending, and increasing safety regulations in countries such as China and India. By 2032, Asia Pacific’s uptake is projected to reach a volume of about 950 million units (USD scale equivalent), outpacing all other regions in incremental demand.

North America’s share of the advanced protective gear and armor market is approximately 36.4 % by volume in 2024. Demand is strongly driven by defense and homeland security agencies, industrial manufacturing, and emergency response sectors. Recent regulatory adjustments—such as stricter OSHA mandates and government grants for protective equipment modernization—have spurred procurement cycles. Technological trends in the region include AI-enabled wearable protective systems, sensor-embedded vests, and advanced composite materials to reduce weight while maintaining protection. One prominent U.S. company—3M—has expanded its ballistic and tactical gear division, developing hybrid ballistic fabrics and smart textile prototypes for military and law enforcement. Consumer (or institutional) behavior in North America shows higher adoption rates in sectors such as healthcare and finance, where secure environments demand protective protocols, extending beyond purely defense to critical infrastructure protection.

Europe holds about 26.7 % of global advanced protective gear and armor volume in 2024. Key national markets include Germany, the United Kingdom, and France. European regulatory bodies emphasize stringent safety, sustainability, and chemical compliance standards, pushing innovation toward eco-friendly materials and traceability. Emerging technologies such as smart fabrics, integrated sensors, and modular armor systems are gaining adoption in Europe more rapidly than elsewhere in response to regulation. German manufacturers, for instance, are developing reactive armor membranes that dynamically shift stiffness under impact. Regional consumer/institutional behavior in Europe is influenced by regulatory pressure, leading to higher demand for explainable and audit-friendly protective systems in public safety, infrastructure, and energy sectors.

In 2024, Asia Pacific ranked third in volume but is rapidly catching up, with industrial and defense procurement growing strongly. Top consuming countries include China, India, and Japan. The region’s infrastructure and manufacturing expansion fuels demand for protective gear across construction, mining, and defense. Technology hubs in China and India are investing in localized R&D for nanocomposites, smart PPE, and low-cost ballistic materials. A major Chinese firm recently launched a sensor-augmented helmet with hazard detection capabilities, gaining traction among industrial clients. In Asia Pacific, consumer/institutional behavior is increasingly shaped by e-commerce platforms and mobile AI applications, enabling quicker procurement of advanced gear even in remote industrial sites.

Key countries include Brazil and Argentina. South America accounts for approximately 6.1 % of the global advanced protective gear market in 2024. Infrastructure expansion, mining, and energy projects are key demand drivers. In Brazil, government incentives support local manufacturing of ballistic vests and safety garments, aiming to reduce import dependence. Local defense contractors are also increasing capacity to supply regional police forces. Consumer/institutional behavior tends to reflect demand tied to large public works and resource sector operations, with increased uptake of protective gear for construction and mining employees.

The Middle East & Africa region accounts for around 10.9 % of global volumes in 2024. Demand is heavily tied to oil & gas, infrastructure development, and defense modernization in GCC countries and South Africa. Technological modernization includes adoption of ruggedized protective fabrics and climate-tolerant gear suited to harsh environments. Local firms in the UAE and South Africa are increasingly investing in domestic assembly and materials blending. Consumer/institutional behavior in this region shows preference for gear tailored to high-heat, high-dust, and extreme operating conditions, driving demand for specialized protective textiles and modular systems.

United States - 22 % Market Share: Strong defense manufacturing, high end-user demand, and heavy R&D investment support its leading position.

China - 16 % Market Share: Large domestic production capacity, rapidly growing defense & industrial procurement, and increasing technological self-reliance in protective gear.

The Advanced Protective Gear and Armor Market is characterized by a fragmented competitive landscape, with numerous players vying for market share across various regions and application segments. In 2024, the combined market share of the top five companies was estimated at approximately 35%, indicating a diverse and competitive environment. Key players such as Honeywell International Inc., 3M Company, DuPont de Nemours, Inc., BAE Systems plc, and MSA Safety Incorporated lead in technological innovation, product diversification, and strategic partnerships. These companies have been actively investing in research and development to enhance product offerings, focusing on integrating smart technologies like wearable sensors and adaptive materials into their protective gear. Additionally, mergers and acquisitions have been prevalent, enabling firms to expand their product portfolios and geographical reach. For instance, Honeywell's acquisition of a leading wearable technology firm has bolstered its position in the smart protective gear segment. The market also sees the emergence of specialized startups introducing niche products tailored to specific industries, further intensifying competition. As the demand for advanced protective solutions grows, companies are increasingly focusing on sustainability, with several introducing eco-friendly materials and manufacturing processes to meet regulatory standards and consumer preferences.

BAE Systems plc

MSA Safety Incorporated

Avon Protection plc

Point Blank Enterprises, Inc.

ArmorSource LLC

Bolle Safety Standard Issue

Galls, LLC

The Advanced Protective Gear and Armor Market is experiencing significant technological advancements that are reshaping product offerings and performance standards. One of the most notable trends is the integration of smart technologies into protective gear. Wearable sensors embedded in helmets, vests, and gloves enable real-time monitoring of physiological parameters such as heart rate, body temperature, and stress levels. This data can be transmitted to command centers, allowing for proactive health and safety management. Additionally, the development of adaptive materials, including graphene and carbon nanotubes, has led to lighter and more flexible armor solutions without compromising protection levels. These materials offer enhanced ballistic resistance and durability, catering to the evolving needs of military and law enforcement agencies. Another emerging technology is the incorporation of augmented reality (AR) systems into helmets, providing users with real-time situational awareness and navigation aids. This integration enhances operational efficiency and safety in complex environments. Furthermore, advancements in manufacturing processes, such as 3D printing, are enabling the production of customized protective gear tailored to individual requirements, improving comfort and effectiveness. As these technologies continue to evolve, they are expected to drive innovation and set new standards in the advanced protective gear and armor market.

In June 2024, Honeywell International Inc. unveiled a new line of smart helmets equipped with integrated communication systems and environmental sensors, enhancing situational awareness for first responders. Source: www.honeywell.com

In March 2024, 3M Company announced the launch of a lightweight ballistic vest utilizing advanced composite materials, offering improved mobility and comfort for military personnel. Source: www.3m.com

In January 2024, DuPont de Nemours, Inc. introduced a flame-resistant garment line incorporating sustainable materials, aligning with growing environmental concerns in protective apparel. Source: www.dupont.com

In November 2023, BAE Systems plc secured a contract to supply next-generation armored vehicles featuring enhanced protection systems and modular designs for rapid deployment. Source: www.baesystems.com

The scope of the Advanced Protective Gear and Armor Market Report encompasses a comprehensive analysis of the global market, focusing on key segments such as product types, applications, end-users, and geographic regions. The report delves into various product categories, including ballistic vests, helmets, gloves, and full-body armor, examining their adoption rates, technological advancements, and performance metrics. Application areas covered include military and defense, law enforcement, industrial safety, and sports, highlighting the specific requirements and challenges within each sector. The report also provides insights into end-user perspectives, assessing factors influencing purchasing decisions, such as cost, comfort, and compliance with safety standards. Geographic analysis includes detailed evaluations of North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, identifying regional trends, growth drivers, and market dynamics.

Additionally, the report explores emerging technologies impacting the market, such as smart textiles, augmented reality systems, and sustainable materials, offering a forward-looking perspective on industry developments. By providing a holistic view of the market landscape, the report serves as a valuable resource for stakeholders seeking to understand current trends and future opportunities in the advanced protective gear and armor market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,680.0 Million |

| Market Revenue (2032) | USD 2,718.4 Million |

| CAGR (2025–2032) | 6.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Honeywell International Inc., 3M Company, DuPont de Nemours, Inc., BAE Systems plc, MSA Safety Incorporated, Avon Protection plc, Point Blank Enterprises, Inc., ArmorSource LLC, Bolle Safety Standard Issue, Galls, LLC |

| Customization & Pricing | Available on Request (10% Customization is Free) |