Reports

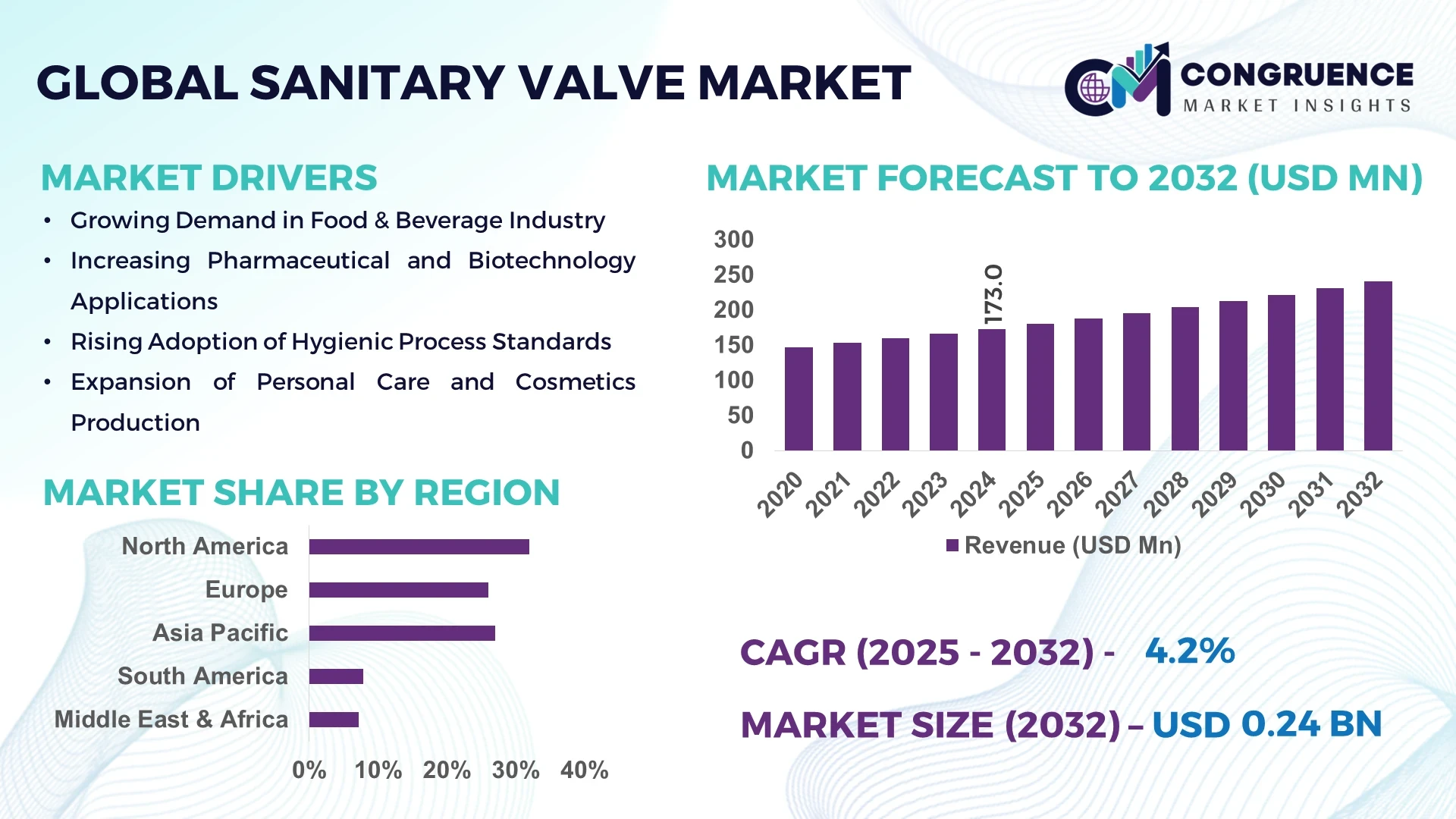

The Global Sanitary Valve Market was valued at USD 173.0 Million in 2024 and is anticipated to reach a value of USD 240.4 Million by 2032 expanding at a CAGR of 4.2% between 2025 and 2032.

The United States leads the marketplace with extensive production capacity for sanitary-grade stainless steel valves, significant capital allocation toward hygienic process equipment, broad deployment across food & beverage and pharmaceutical plants, and ongoing technical upgrades in valve metallurgy and automated actuation technologies. Investment activity has focused on expanding precision machining lines and integrating digital actuation modules for hygienic processes.

The Sanitary Valve Market serves critical industry sectors including food & beverage processing, pharmaceuticals, personal care and cosmetics manufacturing, and beverage/fermentation operations. Food & beverage and pharmaceuticals account for the largest consumption volumes due to strict hygienic requirements and frequent valve replacement cycles driven by sanitary standards. Recent product innovations include hygienic quick-disconnect designs, improved metal finishes (Ra ≤ 0.4 µm) for reduced microbial adhesion, integrated valve-actuator assemblies with CIP/SIP compatibility, and the proliferation of smart actuators with embedded sensors for performance monitoring. Regulatory and environmental drivers such as strengthened sanitary codes, more rigorous clean-in-place (CIP) validation protocols, and sustainability mandates for material recyclability have influenced procurement decisions and product design. Regionally, mature markets in North America and Western Europe show high uptake of automated and sensor-enabled sanitary valves, while Asia-Pacific demonstrates expanding demand tied to new processing plants and capacity expansions. Emerging trends include modular hygienic process skids incorporating pre-mounted sanitary valves, increased use of tri-clamp and hygienic butt-weld connections for rapid maintenance, and a shift toward digital valve lifecyle management—collectively pointing to steady technical evolution and broader adoption across process industries.

Artificial intelligence (AI) is rapidly changing the Sanitary Valve Market by enabling smarter operations, predictive maintenance, and process optimization across hygienic process lines. AI-driven analytics applied to sensor streams from smart actuators and valve-mounted condition sensors have demonstrated the ability to detect abnormal operation patterns—such as gradual torque increases, valve seating drift, or micro-leak signatures—allowing maintenance teams to intervene before failures occur. In practical deployments during 2024, fleet-wide predictive diagnostics were reported to reduce unplanned valve downtime by between 20% and 40% in beverage and pharmaceutical plants where large numbers of quarter-turn and control sanitary valves are used. These systems analyze vibration, current draw, cycle counts, and temperature trends to generate remaining useful life (RUL) estimates and prioritized maintenance tasks, which improves overall line availability and reduces waste from unscheduled stoppages.

For automation and process optimization, AI models optimize valve actuation profiles to reduce pressure spikes and product shear during transfer operations—outcomes that have measurably lowered product loss during SKU changeovers and reduced cleaning cycles in pilot implementations. In the context of the Sanitary Valve Market, AI integration also shortens commissioning times: model-based commissioning can calibrate hundreds of valve-actuator assemblies in a fraction of manual setup time, improving time-to-production for new process lines. From procurement and asset-management perspectives, AI-enhanced digital twins of sanitary valve assemblies permit simulation of flow behavior and service lifecycles under various CIP regimens, enabling decision-makers to forecast spare-parts needs more precisely and plan CAPEX with reduced uncertainty.

AI’s role is not limited to maintenance and commissioning. Advanced image and acoustic analysis—driven by machine learning—are improving leak detection sensitivity on buried or hard-to-inspect line segments, and natural-language summarization tools are being used to convert complex valve health telemetry into concise, actionable maintenance work orders. For the Sanitary Valve Market, these AI-driven efficiencies translate into lower total cost of ownership for automated valve fleets, improved regulatory compliance through better audit trails of valve performance and cleaning cycles, and higher throughput owing to fewer interruptions. As manufacturers supply valve-actuator packages with embedded analytics, buyers are increasingly evaluating lifecycle service contracts that include AI diagnostics, shifting vendor relationships from transaction-based sales to outcome-based maintenance partnerships. Overall, AI is establishing itself as a fundamental enabler of operational resilience, cost efficiency, and digital transformation across hygienic processing industries.

“In March 2024, a major valve manufacturer launched an AI-enabled smart control valve series featuring embedded sensors and on-board machine learning for predictive diagnostics; the initial commercial deployment included over 4,500 smart valves across chemical and process plants and delivered measurable reductions in unplanned valve interventions during the first six months.”

The Sanitary Valve Market dynamics are shaped by technological modernization, regulatory enforcement of hygienic standards, and shifting production patterns in key process industries. Sanitary valves are increasingly specified not only for material compatibility and cleanability but also for digital readiness—requiring integrated actuators, sensors, and communication interfaces. Demand drivers include facility expansions in emerging markets, higher frequency of sanitary valve replacements in high-cycle operations, and the need for valves that support faster product changeovers and validated CIP/SIP processes. Supply-side dynamics involve consolidation among valve OEMs and growing partnerships with automation suppliers to deliver pre-integrated valve-actuator-sensor solutions. On the demand side, end-users prioritize low-maintenance designs, traceable lifecycles for audit compliance, and reduced downtime. Environmental and sustainability pressures are influencing valve material selection and lifecycle programs, while rising interest in modular manufacturing is driving uptake of pre-assembled valve skids. Together, these forces create a market where engineering performance, digital capability, and service propositions determine competitive advantage.

Rapid expansion and modernization of food & beverage and pharmaceutical production facilities are primary drivers for the Sanitary Valve Market. These industries require valves that meet stringent hygienic standards, frequent washdown and sterilization cycles, and validated clean-in-place procedures. For example, high-throughput beverage plants often replace critical sanitary valves on accelerated schedules to reduce contamination risk and maintain production continuity. Pharmaceutical production lines require valves that support aseptic processing and product-contact traceability, leading to specifications for polished surfaces, FDA-compliant materials, and CIP/SIP compatibility. Investments in automated filling and aseptic transfer systems have increased the number of actuated sanitary valves per line, directly boosting demand for motorized butterfly, diaphragm, and ball valve types. The trend toward smaller-batch, multi-SKU production (driven by personalized medicines and craft beverage segments) further elevates the value of quick-actuating, cleanable valve designs that enable fast changeovers and minimal product loss.

A significant restraint for the Sanitary Valve Market is the higher upfront cost associated with smart actuators, integrated sensor packages, and certified sanitary materials. Embedded-sensor valve packages and validated automation systems require investment in both hardware and software, with smaller manufacturers often constrained by capital budgets. Total cost of ownership analyses show that while predictive-maintenance and digital features reduce long-term operating costs, the initial procurement and integration expenses—plus the need for secure OT/IT interfaces—can delay adoption. Additionally, complex regulatory validation (e.g., documentation for pharmaceutical process validation) increases time-to-deployment and engineering costs. In sectors with razor-thin margins or legacy facilities, the capital intensity of retrofitting actuated sanitary valves and associated control upgrades remains a barrier to rapid modernization, particularly for small-to-medium enterprises.

A major opportunity in the Sanitary Valve Market is the retrofit and aftermarket services segment. Many processing facilities operate legacy lines with manual valves or aging actuators that can be upgraded to smart, sensor-equipped units. Retrofit programs that replace only actuators and add modular sensing can deliver significant performance gains—improving uptime and enabling predictive maintenance—while avoiding full valve replacement costs. Service offerings such as condition-based maintenance contracts, remote monitoring subscriptions, and digital twin-enabled lifecycle management create recurring revenue streams for suppliers. Additionally, OEMs can expand aftermarket opportunities by offering certified refurbishment and recalibration services for sanitary valve assemblies, helping customers meet regulatory audit requirements while extending asset lifecycles. The growth of retrofit initiatives is supported by demonstrated reductions in downtime and improved spare-part forecasting that benefit processing operations across food, beverage, and pharma plants.

A consistent challenge impacting the Sanitary Valve Market is the complexity of regulatory compliance and process validation—especially in pharmaceutical and certain food segments. Valves used in aseptic production must satisfy strict material, surface finish, and documentation requirements, and installations frequently require qualification protocols (IQ/OQ/PQ). These validation activities extend project timelines and necessitate detailed supplier documentation, material traceability, and validated cleaning procedures. In multi-jurisdiction deployments, differing regulatory expectations further complicate product selection and engineering design. For manufacturers delivering global projects, the need to provide standardized validation packages and to adapt to regional sanitary codes increases administrative workload and can lengthen lead times. Ensuring consistent compliance while maintaining cost-effectiveness and speed of deployment remains a major operational and commercial challenge for suppliers and end-users alike.

Adoption of Integrated Smart Actuators for Predictive Maintenance: The Sanitary Valve Market is moving toward valve-actuator packages with embedded sensors that monitor torque, cycle count, and valve position. Commercial rollouts in 2024 demonstrated multi-site deployments where predictive diagnostics reduced emergency interventions by up to 35% within the first year.

Modular Hygienic Skids and Pre-Assembled Valve Banks: Process manufacturers increasingly purchase pre-fabricated process skids with pre-mounted sanitary valves and instrumentation. These modular solutions reduce on-site installation time, simplify qualification, and enable faster ramp-up—delivering measurable reductions in commissioning timelines for new facilities.

Higher-Spec Surface Finishes and Material Upgrades: Demand is rising for valves with improved surface finishes (Ra ≤ 0.4 µm) and more corrosion-resistant alloys to meet extended CIP/SIP cycles and aggressive cleaning chemistries. This trend is driving adoption of electropolishing and advanced passivation processes in valve production.

Expansion of Digital Services and Lifecycle Contracts: Suppliers in the Sanitary Valve Market are bundling hardware with digital services—remote monitoring, condition analytics, and predictive maintenance contracts—shifting commercial models from one-time sales to recurring revenue streams and outcome-based service agreements.

The Global Sanitary Valve Market demonstrates a diverse segmentation structure based on type, application, and end-user industries. Each segment contributes uniquely to overall demand, shaped by varying industry requirements, regulatory standards, and technological adoption. Product types such as ball valves, butterfly valves, diaphragm valves, and others are engineered to ensure precision control, hygiene, and compliance with stringent sanitation guidelines. Applications span across food and beverages, pharmaceuticals, biotechnology, and personal care, where safety and reliability are paramount. End-users range from large-scale manufacturers to niche biotechnology firms, each driving adoption patterns. The interplay of these segments highlights the importance of customization, innovation, and adherence to evolving global hygiene standards, while also reflecting the diverse consumption trends across regions and sectors.

Sanitary valves are broadly categorized into ball valves, butterfly valves, diaphragm valves, globe valves, and check valves. Among these, butterfly valves dominate the market due to their lightweight design, low maintenance requirements, and ability to handle high flow rates with minimal pressure drop. These features make them especially attractive for large-scale food and beverage and pharmaceutical production facilities. The fastest-growing type is diaphragm valves, which are increasingly preferred in pharmaceutical and biotechnology industries for their superior sealing capabilities and ability to prevent contamination in sterile processes. Ball valves, though widely used, cater more to industries requiring precision shut-off control, while globe and check valves serve niche applications such as flow regulation and backflow prevention in critical systems. Collectively, the growing demand for enhanced hygiene, ease of cleaning, and efficient process control is driving the evolution of these valve types.

The sanitary valve market spans multiple applications, including food and beverages, pharmaceuticals, biotechnology, and personal care industries. The food and beverage industry represents the leading application, driven by rising demand for processed food, dairy products, and beverages that require strict hygiene and safety compliance. The fastest-growing application is pharmaceuticals, fueled by expanding global drug production and advanced manufacturing processes requiring sterile and contamination-free environments. Biotechnology also plays a growing role, with valves designed to support bioprocessing, fermentation, and cell culture applications. Meanwhile, the personal care sector leverages sanitary valves for hygienic handling of creams, lotions, and other formulations. Each application area underscores the increasing emphasis on safety, regulatory compliance, and operational efficiency, making sanitary valves an essential component across industries.

End-users of sanitary valves include large-scale food and beverage producers, pharmaceutical manufacturers, biotechnology firms, and cosmetics companies. The food and beverage sector is the leading end-user, accounting for a substantial portion of demand due to large-scale processing facilities that require high hygiene standards and reliable fluid control systems. The pharmaceutical industry represents the fastest-growing end-user segment, benefiting from global investments in drug manufacturing, biopharmaceuticals, and cleanroom technologies. Biotechnology companies are also expanding their usage of sanitary valves in bioprocessing and advanced R&D applications, ensuring precision and contamination-free production. Additionally, the cosmetics and personal care sector contributes to niche demand, particularly in applications where consumer safety and product purity are critical. Across all end-user segments, the adoption of advanced valve technologies emphasizes automation, compliance with stringent sanitation standards, and operational efficiency, making sanitary valves integral to global industrial operations.

North America accounted for the largest market share at 32% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

The market dynamics differ across regions, with developed economies focusing on regulatory compliance, automation, and sustainability, while emerging regions prioritize expanding food, beverage, and pharmaceutical infrastructure. Europe emphasizes stringent quality and hygiene regulations, driving advanced valve adoption in dairy and personal care industries. Asia-Pacific’s growing biotechnology and pharmaceutical sectors are creating vast demand, while South America and the Middle East & Africa see growth through modernization of processing facilities and rising government investments in manufacturing and healthcare infrastructure.

North America held approximately 32% of the global sanitary valve market in 2024, positioning it as the leading regional contributor. The U.S. and Canada remain dominant due to the strong presence of food & beverage producers and pharmaceutical manufacturers requiring high-quality sanitary flow control systems. Strict FDA and USDA guidelines mandate hygienic processing equipment, reinforcing valve adoption across industries. Technological advancements, including digital monitoring and IoT-enabled smart valves, are transforming operations, improving efficiency and predictive maintenance. Government support for biopharmaceutical innovation further drives demand, making North America an innovation hub where compliance, automation, and digitalization converge to sustain growth in the sanitary valve market.

Europe represented nearly 28% of the sanitary valve market in 2024, driven primarily by Germany, the UK, and France. The region’s food processing, dairy, and pharmaceutical sectors are among the largest consumers, with demand strengthened by strict hygiene and safety regulations from the European Food Safety Authority (EFSA) and other governing bodies. Sustainability initiatives across the EU are accelerating the adoption of energy-efficient and environmentally friendly valve technologies. Furthermore, the integration of advanced automation systems and Industry 4.0 practices is becoming widespread in European manufacturing facilities. Europe’s strong emphasis on both regulatory compliance and technological innovation ensures its continuing influence on the global sanitary valve market.

Asia-Pacific accounted for around 25% of the global sanitary valve market in 2024, ranking second in terms of market size but first in growth momentum. China, India, and Japan are the top consumers, supported by massive investments in food processing, biotechnology, and pharmaceutical manufacturing facilities. Infrastructure modernization and government-driven initiatives to expand domestic production capacity are accelerating sanitary valve adoption. The region is also seeing strong growth in automation technologies, with smart valves and real-time monitoring systems being integrated into industrial plants. Emerging innovation hubs across China and India further drive competitiveness, making Asia-Pacific the fastest-expanding region in the sanitary valve market.

South America contributed close to 8% of the global sanitary valve market in 2024, with Brazil and Argentina leading demand. The region’s growing food & beverage exports and expanding pharmaceutical production facilities are major growth drivers. Infrastructure development, particularly in Brazil’s energy and industrial sectors, further supports sanitary valve adoption. Governments in the region are introducing favorable trade policies and investment incentives to boost local manufacturing capacity, making sanitary valve suppliers a critical part of regional supply chains. South America’s gradual modernization of production facilities ensures steady demand growth in the coming years.

The Middle East & Africa region accounted for approximately 7% of the sanitary valve market in 2024, with the UAE and South Africa standing out as key growth markets. Demand is being fueled by infrastructure development, oil & gas diversification, and rising investments in food processing and pharmaceutical manufacturing. The region is embracing technological modernization, with industries increasingly deploying advanced valve solutions to improve efficiency and safety. Local regulations and trade partnerships are also encouraging the adoption of hygienic and compliant equipment. The MEA region is becoming an attractive growth destination, supported by industrial diversification and regulatory alignment with global standards.

United States – 20% Market Share

The U.S. leads due to its advanced pharmaceutical and food processing industries, supported by strict hygiene regulations and widespread adoption of automation.

China – 15% Market Share

China dominates through large-scale food manufacturing and biotechnology investments, coupled with strong government backing for domestic industrial expansion.

The global sanitary valve market is highly competitive, with over 50 active players ranging from multinational corporations to specialized regional manufacturers. Competition is shaped by product differentiation, technological integration, and the ability to comply with stringent hygienic and safety standards. Leading companies are focusing on enhancing durability, reducing contamination risks, and incorporating smart monitoring systems into valve designs. Strategic initiatives such as product innovations, expansions into emerging markets, and mergers or acquisitions are frequent in this sector. Many players are investing heavily in advanced materials like stainless steel and high-performance polymers to meet the demands of industries such as food, beverage, pharmaceuticals, and biotechnology. The competitive environment also reflects an increasing emphasis on sustainability, with companies integrating eco-friendly manufacturing practices and energy-efficient valve designs. Innovation trends such as automation-ready sanitary valves and IoT-enabled monitoring solutions are further intensifying competition, pushing companies to differentiate not only through quality but also through digital adaptability and regulatory compliance.

Alfa Laval AB

Emerson Electric Co.

GEA Group AG

SPX FLOW, Inc.

ITT Inc.

Kieselmann GmbH

Dixon Valve & Coupling Company

KSB SE & Co. KGaA

Burkert Fluid Control Systems

Schubert & Salzer Control Systems GmbH

Crane Co.

GEMÜ Group

Technological advancements are significantly reshaping the sanitary valve market, with innovation aimed at improving hygiene, efficiency, and automation. Modern sanitary valves increasingly incorporate stainless steel with higher corrosion resistance, ensuring compliance with stringent food, pharmaceutical, and biotechnology standards. Automation is one of the most prominent technological trends, with valves integrated into programmable logic controllers (PLCs) and IoT-based monitoring systems to allow real-time performance analysis and predictive maintenance. Smart sanitary valves equipped with sensors can detect pressure changes, flow rates, and contamination risks, reducing downtime and enhancing safety across processing environments.

Another key development is the use of high-performance elastomers and polymer coatings, which enhance durability and reduce microbial buildup. Additive manufacturing, or 3D printing, is also emerging in prototype development, allowing faster customization and innovation in valve design. In addition, the adoption of clean-in-place (CIP) and sterilize-in-place (SIP) technologies ensures that sanitary valves meet the rigorous demands of modern production processes while minimizing manual intervention. Digital twins are being employed to model valve performance, helping manufacturers test and optimize designs before deployment. Looking forward, advancements in bio-based materials, coupled with sustainable engineering practices, are expected to influence valve production and drive eco-friendly adoption. These technological insights highlight the dynamic transformation of the sanitary valve industry, where precision, compliance, and digital integration are becoming central to competitive advantage.

• In February 2023, Alfa Laval expanded its hygienic valve product line with new double-seat valves designed to enhance cleanability and reduce cross-contamination risks in food and beverage processing. The innovation is targeted at manufacturers aiming for higher operational safety and compliance with strict sanitary regulations.

• In July 2023, Emerson introduced a new range of intelligent sanitary control valves equipped with digital positioners, enabling improved process accuracy and reduced energy consumption in pharmaceutical and biotechnology applications. These valves enhance real-time monitoring and contribute to process optimization.

• In March 2024, GEA Group launched an upgraded hygienic valve system featuring advanced sealing materials, designed to extend service life and reduce maintenance costs. The solution is particularly suited for high-demand applications in dairy and beverage industries.

• In May 2024, SPX FLOW unveiled an advanced sanitary diaphragm valve platform incorporating modular designs and sensor-based condition monitoring. This development enables better integration into automated systems, supporting predictive maintenance strategies in processing facilities.

The Global Sanitary Valve Market Report provides an extensive analysis of the industry’s structure, covering its segmentation by type, application, end-user industries, and geographic distribution. The report evaluates major sanitary valve types including ball valves, butterfly valves, diaphragm valves, and check valves, analyzing their adoption across diverse processing industries. Applications such as food and beverage, pharmaceuticals, biotechnology, dairy, and personal care are examined, highlighting how specific sanitary requirements influence demand patterns. End-user insights span large-scale industrial processors, small to mid-sized enterprises, and highly regulated sectors requiring strict hygiene standards.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering a comparative perspective on demand drivers, industrial infrastructure, and regulatory landscapes across these regions. It also outlines how regional trends such as automation adoption in North America, sustainability initiatives in Europe, rapid manufacturing growth in Asia-Pacific, and rising infrastructure investments in South America and the Middle East are shaping the global market.

In addition, the scope includes analysis of technology integration, particularly automation, IoT-based smart valves, digital twins, and clean-in-place systems that are influencing modern processing operations. The report further explores emerging opportunities in eco-friendly materials, digital monitoring, and advanced sealing technologies. By consolidating these insights, the report provides a comprehensive framework for decision-makers to assess opportunities, anticipate risks, and align strategies with evolving market dynamics.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 173.0 Million |

| Market Revenue (2032) | USD 240.4 Million |

| CAGR (2025–2032) | 4.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Alfa Laval AB, Emerson Electric Co., GEA Group AG, SPX FLOW, Inc., ITT Inc., Kieselmann GmbH, Dixon Valve & Coupling Company, KSB SE & Co. KGaA, Burkert Fluid Control Systems, Schubert & Salzer Control Systems GmbH, Crane Co., GEMÜ Group |

| Customization & Pricing | Available on Request (10% Customization is Free) |