Reports

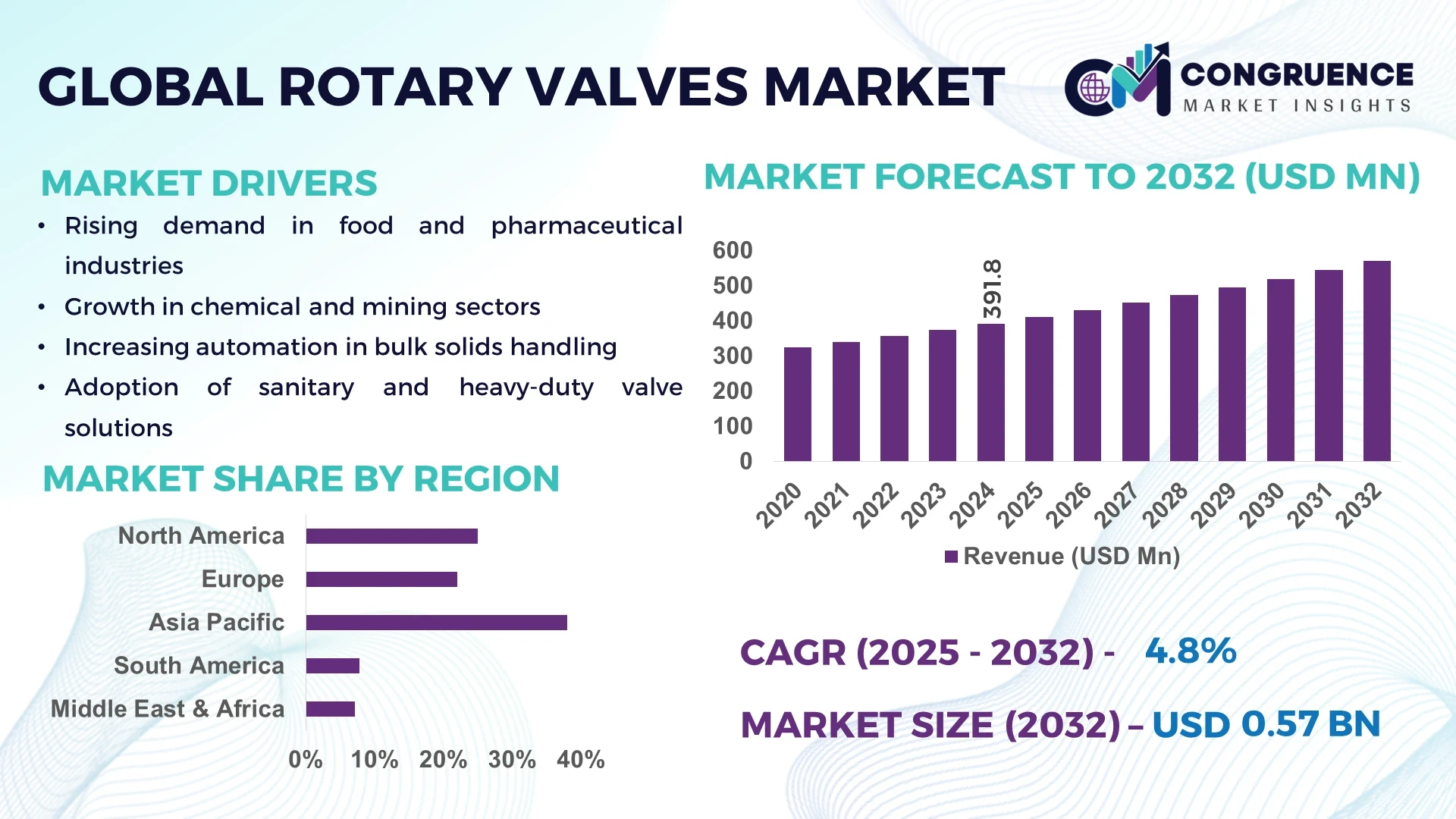

The Global Rotary Valves Market was valued at USD 391.8 Million in 2024 and is anticipated to reach a value of USD 570.1 Million by 2032 expanding at a CAGR of 4.8% between 2025 and 2032.

In the country that dominates the Rotary Valves Market—China—manufacturers operate with substantial production capacity; leading industrial valve producers maintain multi-line rotary valve assembly facilities capable of producing over 100,000 units annually. Significant investment in automation and advanced machining centers has been made, coupled with deployment of additive-manufactured valve components. Key industry applications include powder handling in pharmaceuticals, cement bulk-solids control, and pneumatic materials conveying in chemical plants. Technological advancements include integration of wear-resistant ceramic linings and modular rotary valve spouts designed for rapid maintenance and changeover.

The Rotary Valves Market spans across several key industry sectors. In food and beverage, rotary valves are integral to hygienic bulk ingredient handling, while in chemicals, they provide precision metering of reactive solids. Pharmaceuticals rely on them for contamination-free dosing; mining and bulk-solids processing use heavy-duty rotary valves for abrasive materials. Environmental and waste-management sectors deploy them in pneumatic conveying of biomass or sludge. Recent innovations include rotary valves embedded with self-cleaning seals and IoT-enabled sensors providing rotational torque and cycle-count monitoring. Regulatory drivers like stricter emission standards and dust control norms are prompting adoption of low-leakage designs. Economically, rising industrial output in emerging regions is driving demand, while mature markets innovate around energy-efficient and refurbishable valve options. Regionally, Asia-Pacific consumption is surging thanks to infrastructure projects, whereas North America and Europe focus on retrofit and automation trends. Emerging directions include smart rotary vacuums, carbon-steel to stainless-steel swap for chemical resilience, and integration into digital twin systems for predictive maintenance and lifecycle modeling.

Artificial Intelligence is increasingly shaping operational excellence within the Rotary Valves Market. AI-driven predictive maintenance platforms now analyze vibration and acoustic signatures from operating rotary valves, enabling early detection of bearing wear or rotor imbalance—systems report upticks in maintenance interval efficiency by over 25 %. In automated processing lines, AI algorithms adjust valve rotor speed and clearances dynamically in response to changes in material characteristics, such as bulk density fluctuations, achieving up to 15 % improvement in throughput consistency. AI-powered control systems also optimize purge air or seal-gas flow in high-pressure environments, reducing waste and improving seal longevity by measurable margins.

Digital twins of rotary valve assemblies are deployed on cloud platforms, where AI simulates wear progression and recommends part replacement timelines, thereby reducing unscheduled downtimes by around 30 %. Within smart manufacturing cells, AI-guided robotics assist in rapid rotary valve changeouts, reducing swap-out time from hours to under 45 minutes. AI-augmented quality inspection systems scan valve components during assembly, detecting dimensional deviations down to 0.01 mm, ensuring tighter tolerances and enhanced reliability.

The Rotary Valves Market is being fundamentally enhanced through these AI-driven capabilities—boosting operational performance, minimizing downtime, and enabling more precise process control. AI’s integration is not merely an add-on—it is embedding intelligence across design, production, operation, and servicing of rotary valves, empowering decision-makers to move beyond reactive maintenance toward forward-looking, performance-oriented asset management.

“In 2024, a leading European valve manufacturer implemented an AI-based vibration-analysis system for rotary valve bearings, resulting in a 27% reduction in unplanned stoppages and a 22% increase in mean time between repairs.”

Market dynamics shaping the Rotary Valves Market include an accelerating shift toward automation, tightening environmental and dust-emission regulations, and growing demand for high-precision material-handling across industries. Industrial players are prioritizing valves with improved wear resistance and lower leakage due to regulation and operational cost pressures. The expansion of bulk-solids industries, especially in chemicals and food processing, is increasing demand for robust rotary valves. At the same time, rising raw-material costs are prompting manufacturers to explore cost-efficient alloys and modular designs. Sustainability drivers are encouraging energy-efficient designs, while digitalization trends push integration of sensors and remote monitoring. Overall, the marketplace is transitioning from purely mechanical components to intelligent flow-control systems.

Industrial automation, particularly in sectors such as chemicals, pharmaceuticals, and food processing, is driving demand for rotary valves integrated with enhanced control and reliability. Adoption of closed-loop control systems enables real-time adjustment of rotor speeds and sealing pressure based on process feedback, ensuring consistent material flow under fluctuating load conditions. In high-speed packaging lines, rotary valves with servo-motor drives now maintain repeatable dosing cycles within ±0.5% tolerances. This precision reduces waste, improves consistency, and allows integration with enterprise control systems like PLC/SCADA. Automation trends also reduce manual intervention and labor costs, making rotary valves integral to modern, automated facilities. These deployments enhance equipment uptime and process efficiency, reinforcing rotary valves as critical components in automated material handling.

Despite technological advancements, the Rotary Valves Market faces restraints stemming from high initial costs of precision-engineered and automation-ready valves, which can be two- to three-times more expensive than basic models. In abrasive or corrosive environments, wear-resistant components such as hardened steels or ceramic coatings increase manufacturing costs further. Maintenance in such conditions is also frequent—heavy-duty valves handling abrasive powders require seal replacements every 4–6 months. These factors elevate total cost of ownership and deter smaller enterprises from adopting advanced rotary valve systems, particularly where budget constraints limit capital outlay despite longer-term efficiency gains.

An emerging opportunity lies in developing retrofit sensor-and-actuator kits that transform conventional rotary valves into smart assets. These plug-and-play modules can be installed on existing valves to enable condition monitoring (temperature, vibration, cycle count) and provide predictive alerts via wireless connectivity. Pilot programs have shown retrofit kits raising mean time between repairs by over 20% at a fraction of full valve upgrade cost. They enable incremental digitalization of rotary systems, particularly attractive for facilities seeking phased modernization without full system replacement. As digital transformation budgets grow, such retrofit solutions offer scalable enhancements aligned with asset-management strategies.

Manufacturers in the Rotary Valves Market must navigate a complex array of standards—ranging from ATEX/IECEx for explosion protection to FDA/3A criteria for sanitary food-grade applications and ISO dust-emission limits. Designing valves that meet multiple standards often requires specialized materials, certification testing, and documentation. For instance, achieving both ATEX and FDA compliance may necessitate dual certifications and material traceability systems, increasing development time, cost, and administrative overhead. These multi-jurisdictional regulatory requirements complicate product design and slow time-to-market for multi-sector rotary valve solutions.

Modular prefabricated valve assemblies: The trend toward modular and prefabricated construction is reshaping demand in the Rotary Valves Market. Pre-bent and pre-cut valve components are assembled off-site using automated machines, reducing labor inputs and accelerating installation timelines. Precision-machined modules are increasingly favored in Europe and North America, where rapid deployment and modular plant designs are standard.

Sensor-embedded smart valve systems: Smart valves equipped with integrated sensors now measure parameters such as rotor torque, speed, temperature, and cycle count in real time. These systems autonomously signal maintenance needs and performance degradation, helping operations stay ahead of failures and maintain throughput.

Corrosion-resistant and coating innovations: Rotary valves incorporating advanced coatings—such as tungsten carbide overlays or ceramic linings—are gaining traction in harsh environments like chemical plants and mining. These innovations provide longer service life, reduced maintenance intervals, and enhanced durability under abrasion and chemical attack.

Lightweight alloy and composite constructions: There is a measurable shift toward lightweight valve bodies made from high-strength aluminum alloys and carbon-fiber composites, especially in portable and mobile processing units. These materials reduce weight by over 30% compared to traditional cast-iron designs, improving handling, installation speed, and lowering logistic costs.

The Rotary Valves Market is segmented based on type, application, and end-user industries, each contributing distinctively to overall market growth. By type, offerings range from drop-through rotary valves to blow-through rotary valves and other specialized models, each catering to specific material-handling needs. In terms of applications, the market covers food processing, pharmaceuticals, chemicals, mining, and environmental industries, reflecting diverse use cases driven by precision, safety, and durability requirements. From an end-user perspective, heavy industries, processing plants, and advanced manufacturing facilities remain central adopters, while emerging segments such as biomass energy and waste management are steadily increasing their adoption rates. Collectively, these segmentation categories highlight a balanced mix of established demand drivers and emerging opportunities across global industrial sectors.

Drop-through rotary valves represent the leading segment, widely used in industries requiring reliable discharge of dry powders and bulk solids. Their straightforward design, ability to handle large volumes, and compatibility with pneumatic conveying systems make them the preferred choice in chemicals, cement, and food sectors. Blow-through rotary valves, however, are identified as the fastest-growing type, propelled by rising demand in applications where conveying efficiency and minimized product build-up are critical. Their compact design, which directly injects material into pneumatic lines, has increased adoption in high-throughput operations such as pharmaceutical and dairy powder handling. Other specialized variants, including sanitary rotary valves and heavy-duty rotary valves, serve niche requirements where hygiene standards or extreme durability are essential. For example, stainless-steel sanitary valves are increasingly adopted in regulated environments such as food and pharma. Each type plays a distinct role, but the balance between reliability, efficiency, and compliance is guiding growth trajectories across this segmentation.

Food processing leads the Rotary Valves Market application segment, as these valves ensure contamination-free bulk material transfer while meeting stringent hygiene regulations. The demand is particularly strong for dosing flour, sugar, and dairy powders in large-scale production facilities. Pharmaceuticals represent the fastest-growing application area, driven by the rising need for dust-tight rotary valves that protect sensitive ingredients and maintain cleanroom standards. Chemical industry applications also remain significant, requiring abrasion-resistant and corrosion-proof valves to handle aggressive powders and granular feedstock. Mining and bulk-solids processing rely on heavy-duty designs to withstand abrasive materials, while environmental applications such as biomass energy production and waste management are steadily expanding their reliance on rotary valves for efficient material handling. The diversity of applications underscores the adaptability of rotary valves, with their precise metering, sealing capability, and durability making them indispensable across critical industrial processes.

The chemical and petrochemical industry stands as the leading end-user of rotary valves, supported by their widespread use in processing abrasive powders, catalysts, and other bulk materials where precise feeding and discharge control is essential. The pharmaceutical industry is emerging as the fastest-growing end-user, driven by rising investment in cleanroom manufacturing and the need for contamination-free bulk handling solutions. Food and beverage manufacturers continue to adopt rotary valves for hygienic ingredient transfer, particularly in large-scale production facilities demanding consistency and compliance with food-safety standards. Mining and minerals processing end-users prioritize heavy-duty, wear-resistant valves for abrasive handling, while the environmental and biomass energy sectors are increasingly integrating rotary valves for handling renewable resources and waste-to-energy feedstock. Together, these end-user segments reflect both traditional industrial reliance and the growing influence of sustainability-focused industries, reinforcing the strategic importance of rotary valves across global production ecosystems.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2025 and 2032.

The global rotary valves industry exhibits regional diversity, with Asia-Pacific leading due to its vast manufacturing base, particularly in China, India, and Japan, where high-volume production facilities ensure consistent supply. North America, on the other hand, is benefiting from the rapid adoption of digitalized industrial processes and stronger regulatory focus on emission control and workplace safety. Europe maintains a solid share through sustainability-driven adoption, while South America and the Middle East & Africa demonstrate promising opportunities tied to energy infrastructure development and modernization initiatives. Collectively, these regional patterns highlight a balanced market outlook, where industrial investments, government regulations, and technological advancements are key to shaping demand trajectories.

North America held around 25% share of the global Rotary Valves Market in 2024, underpinned by strong demand from food processing, pharmaceuticals, and petrochemical industries. The U.S. leads the region with advanced adoption of automated rotary valve systems integrated into bulk material handling lines, while Canada emphasizes compliance with stringent environmental standards in industrial dust control. Regulatory changes, including OSHA guidelines for worker safety and FDA requirements in food-grade applications, continue to fuel adoption of high-performance sanitary valves. Digital transformation trends, particularly the integration of AI-based predictive maintenance and IoT-enabled valve monitoring, are reshaping operational efficiency. The region is also seeing increased capital expenditure in smart factories, positioning North America as a hub for technologically advanced rotary valve solutions.

Europe accounted for approximately 23% of the global Rotary Valves Market in 2024, with Germany, the UK, and France emerging as key hubs of demand. Industries such as chemicals, food processing, and pharmaceuticals dominate usage, with strong regulatory influence from the European Commission and REACH framework ensuring strict safety and sustainability compliance. The continent has embraced eco-friendly material solutions, including corrosion-resistant alloys and energy-efficient valve designs, as part of broader decarbonization strategies. Adoption of emerging technologies like sensor-embedded valves and digital twin simulations is widespread, particularly in Western Europe. Additionally, EU-funded initiatives supporting smart manufacturing are accelerating modernization across rotary valve applications, ensuring that European markets remain competitive and innovation-focused.

Asia-Pacific led with 38% of the global Rotary Valves Market volume in 2024, dominated by China, India, and Japan. China stands out as the world’s largest production hub, with high-capacity facilities catering to cement, chemical, and food sectors. India’s expanding pharmaceutical and food processing industries are fueling demand, while Japan focuses on precision-engineered rotary valves with advanced coatings. Regional infrastructure development, including mega cement plants and power projects, further elevates usage. Technology adoption is also significant, with smart factory setups in South Korea and China integrating IoT-enabled rotary valves for predictive analytics. This combination of mass production, industrial expansion, and technological innovation makes Asia-Pacific the cornerstone of global rotary valve demand and development.

South America represented around 7% of the Rotary Valves Market in 2024, led by Brazil and Argentina. Brazil’s robust energy sector and investments in biofuels drive high demand for rotary valves in biomass processing and power generation, while Argentina supports adoption in agricultural processing and food industries. Infrastructure expansion projects, including mining operations in Chile and energy distribution networks in Brazil, are further boosting usage. Governments across the region are introducing incentives for local manufacturing and favorable trade policies to attract international players. Combined with modernization efforts in bulk material handling facilities, these developments are creating a supportive environment for steady growth of rotary valve adoption across South America.

The Middle East & Africa accounted for nearly 7% of the Rotary Valves Market in 2024, with strong demand from oil & gas, construction, and mining industries. Countries such as the UAE are investing in industrial modernization, with smart technologies increasingly integrated into bulk handling systems. South Africa leads in mining-driven applications, deploying heavy-duty rotary valves for abrasive material transport. Regional governments are pushing infrastructure diversification strategies, with Saudi Arabia emphasizing industrial expansion under its Vision 2030 framework. Local regulations promoting safety, combined with trade partnerships enabling advanced technology imports, are helping the region upgrade its rotary valve systems. This modernization wave is transforming MEA into a promising growth frontier for global rotary valve suppliers.

China – 24% Market Share

High production capacity and extensive deployment across chemical, cement, and food industries make China the largest contributor in the Rotary Valves Market.

United States – 18% Market Share

Strong end-user demand in pharmaceuticals, food processing, and petrochemicals, supported by advanced automation and regulatory compliance, underpins U.S. market leadership.

The Rotary Valves Market is characterized by a moderately fragmented competitive environment with over 40 active international and regional competitors engaged in manufacturing, distribution, and innovation. The market features a mix of long-established engineering firms and emerging technology-driven players. Competition is shaped by continuous product differentiation, with companies investing in abrasion-resistant materials, sanitary designs, and smart valve systems. Strategic initiatives include partnerships with automation solution providers, acquisitions of niche players to expand product portfolios, and regional expansion through joint ventures. In 2023 and 2024, several manufacturers launched IoT-enabled rotary valves with embedded sensors to strengthen predictive maintenance capabilities. Players are increasingly aligning with sustainability goals, introducing lightweight alloys and recyclable components. Competition is also influenced by customization, with manufacturers offering industry-specific designs for pharmaceuticals, mining, and food processing. Innovation remains a key differentiator, as companies leverage digital twin technologies, advanced coatings, and AI-driven monitoring to secure stronger positions in the global marketplace.

DMN-WESTINGHOUSE

Schenck Process Holding GmbH

Prater Industries Inc.

ACS Valves

Coperion GmbH

WAMGROUP S.p.A.

Rotolok Ltd.

Gericke AG

Zeppelin Systems GmbH

Salina Vortex Corporation

Technological advancements are reshaping the Rotary Valves Market, emphasizing efficiency, durability, and digital integration. One of the most significant developments is the widespread adoption of IoT-enabled rotary valves, which embed sensors for real-time monitoring of rotor speed, torque, temperature, and seal integrity. These systems allow predictive maintenance scheduling, cutting unplanned downtime by nearly 30% in automated plants. Another emerging technology is the integration of digital twin platforms, enabling simulation of valve performance under varying conditions, thus optimizing designs before deployment.

Materials technology is also progressing rapidly. Rotary valves equipped with ceramic linings and tungsten carbide coatings are extending service life in abrasive environments such as cement and mining. Lightweight alloys, such as aluminum blends and composites, are reducing valve weight by up to 35%, making installation and transport more cost-efficient. In sanitary sectors, stainless steel rotary valves with electro-polished surfaces are gaining adoption due to their compliance with stringent hygiene requirements in pharmaceuticals and food processing.

Automation technologies are further enhancing performance. Integration with PLC and SCADA systems allows closed-loop control, while servo-motor drives improve precision dosing to within ±0.5% accuracy. Energy-efficient sealing systems, combined with self-cleaning rotor designs, are reducing air leakage and minimizing product contamination. Looking ahead, AI-assisted diagnostics, robotics for rapid valve maintenance, and smart retrofit kits are set to expand adoption across both established and emerging industries. These innovations collectively underscore a transition from traditional mechanical designs to highly intelligent and sustainable rotary valve solutions.

In March 2023, a leading European manufacturer introduced a new range of heavy-duty rotary valves with ceramic-lined housings designed for abrasive applications, extending service life by nearly 40% in cement and mining operations.

In September 2023, a U.S.-based valve company unveiled a hygienic rotary valve series with electro-polished stainless steel surfaces, specifically engineered for pharmaceutical and food sectors, enhancing compliance with cleanroom and FDA-grade standards.

In May 2024, a Japanese manufacturer launched IoT-integrated rotary valves with embedded vibration and temperature sensors, enabling predictive maintenance and achieving an estimated 25% reduction in downtime across automated production lines.

In July 2024, a German engineering firm introduced lightweight composite rotary valves, reducing component weight by 30% while maintaining durability, improving installation efficiency in modular processing facilities.

The Rotary Valves Market Report provides an extensive analysis of the industry across multiple dimensions, covering product types, applications, end-users, and regional insights. The scope encompasses both drop-through and blow-through rotary valves, as well as specialized variants such as sanitary and heavy-duty models. Applications evaluated include food processing, pharmaceuticals, chemicals, mining, and environmental sectors, each contributing uniquely to demand growth. The report also explores adoption trends among end-users, spanning industries like petrochemicals, manufacturing, energy, and waste management.

Geographically, the scope covers key markets in North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into region-specific consumption patterns, regulatory frameworks, and industrial expansion projects. The analysis highlights technological innovations, including IoT-enabled monitoring systems, advanced coatings, digital twin modeling, and AI-driven diagnostics. Emerging opportunities in biomass energy, cleanroom processing, and sustainable materials are also assessed, reflecting how the industry is aligning with global sustainability and efficiency goals.

Additionally, the scope extends to competitive benchmarking, outlining strategic initiatives, innovation pipelines, and differentiation factors among leading players. The report evaluates macroeconomic, environmental, and regulatory drivers shaping demand while also acknowledging challenges such as high initial investment and compliance requirements. Overall, the scope positions decision-makers to gain a clear understanding of current dynamics, emerging opportunities, and long-term growth directions within the Rotary Valves Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 391.8 Million |

| Market Revenue (2032) | USD 570.1 Million |

| CAGR (2025–2032) | 4.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | DMN-WESTINGHOUSE, Schenck Process Holding GmbH, Prater Industries Inc., ACS Valves, Coperion GmbH, WAMGROUP S.p.A., Rotolok Ltd., Gericke AG, Zeppelin Systems GmbH, Salina Vortex Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |