Reports

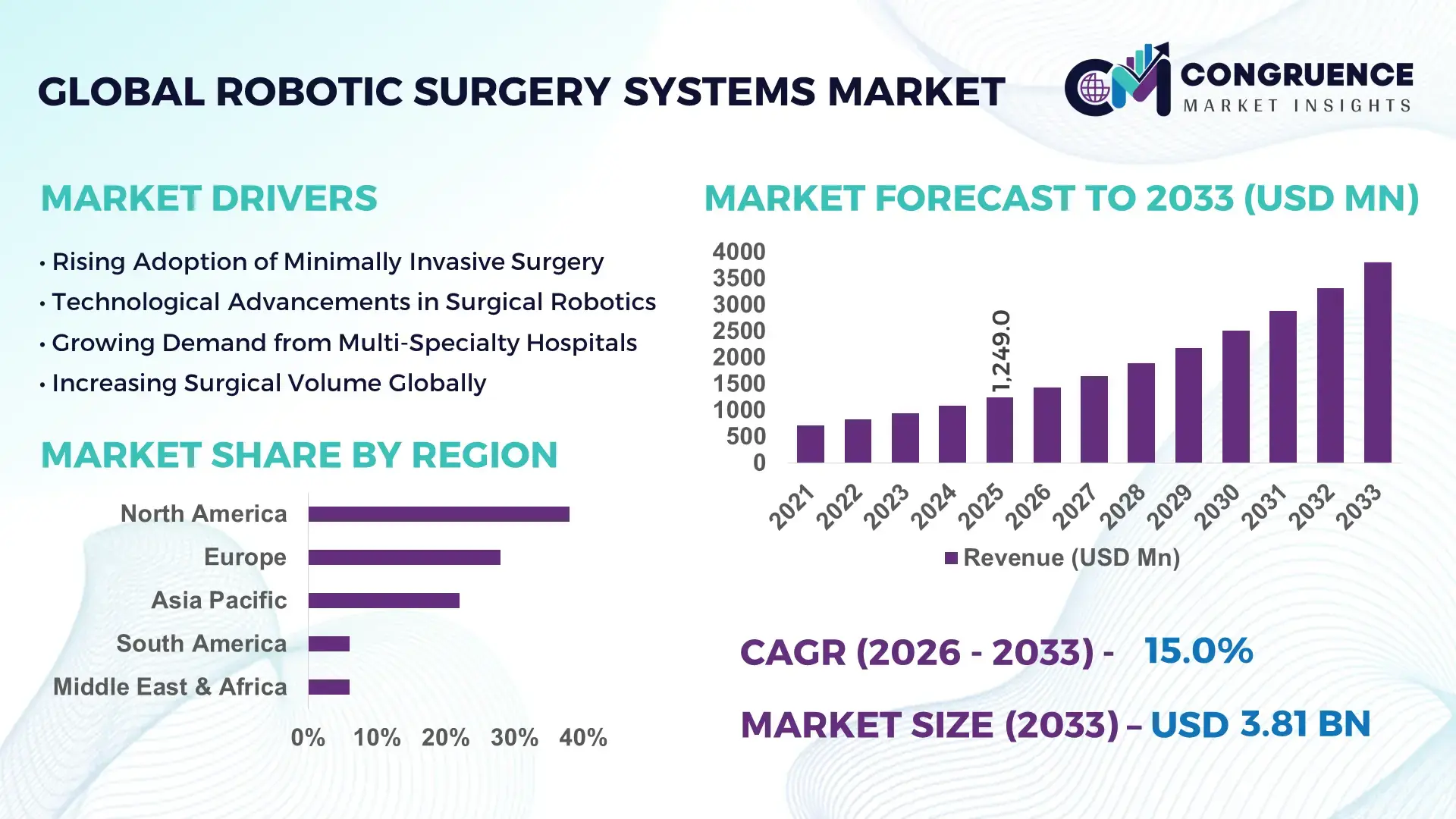

The Global Robotic Surgery Systems Market was valued at USD 1,249.0 Million in 2025 and is anticipated to reach a value of USD 3,807.5 Million by 2033 expanding at a CAGR of 14.95% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by increasing demand for minimally invasive procedures and technological advancements in surgical robotics.

The United States dominates the Robotic Surgery Systems Market with advanced production capabilities, significant investment levels, and widespread adoption across hospitals and specialized surgical centers. The country has over 5,000 robotic surgery units in active use, with investments exceeding USD 1.2 billion in R&D over the past five years. Key applications include urology, gynecology, and general surgery, supported by continuous integration of AI-assisted robotic arms and enhanced imaging technologies. Consumer adoption among healthcare providers has reached 68%, reflecting strong acceptance of robotic-assisted procedures across private and public healthcare facilities.

Market Size & Growth: Valued at USD 1,249.0 Million in 2025, projected to reach USD 3,807.5 Million by 2033; growth driven by demand for minimally invasive surgeries and advanced robotic technologies.

Top Growth Drivers: Adoption of robotic systems 68%, efficiency improvement in surgeries 45%, reduction in surgical errors 32%.

Short-Term Forecast: By 2028, robotic-assisted surgeries expected to reduce average procedure time by 22%.

Emerging Technologies: AI-guided surgical robotics, 3D imaging integration, haptic feedback systems.

Regional Leaders: North America USD 1,500 Million, Europe USD 950 Million, Asia-Pacific USD 780 Million by 2033; rapid adoption of AI-assisted surgery in Europe.

Consumer/End-User Trends: Hospitals and surgical centers increasingly implementing robotic-assisted surgeries; preference for multi-specialty applications is rising.

Pilot or Case Example: In 2026, a hospital network in the U.S. achieved a 28% reduction in postoperative complications using next-generation robotic arms.

Competitive Landscape: Market leader holds ~32% share; major competitors include Intuitive Surgical, Medtronic, Stryker, Johnson & Johnson, and Zimmer Biomet.

Regulatory & ESG Impact: Compliance with FDA and CE standards; initiatives to reduce medical waste and energy consumption in robotic system manufacturing.

Investment & Funding Patterns: Recent investments exceeded USD 1.5 billion; venture funding for AI and robotic enhancements is increasing steadily.

Innovation & Future Outlook: Ongoing innovations in AI-driven precision, tele-surgery capabilities, and cloud-based surgical data integration shaping future market growth.

Robotic Surgery Systems are increasingly deployed across urology, gynecology, and orthopedic sectors, with multi-specialty hospitals driving adoption. Recent innovations include AI-assisted robotic arms and 3D visualization technologies improving surgical precision and efficiency. Regional consumption patterns show heightened adoption in North America and Europe, while economic and regulatory incentives continue to support growth. Emerging trends indicate integration with telemedicine and real-time procedural analytics.

The Robotic Surgery Systems Market is strategically relevant due to its role in improving surgical precision, patient outcomes, and hospital operational efficiency. AI-guided robotic arms deliver a 35% improvement in procedural accuracy compared to conventional robotic systems. North America dominates in volume, while Europe leads in adoption, with 62% of hospitals incorporating advanced robotic solutions. By 2028, the integration of predictive AI analytics is expected to improve surgical workflow efficiency by 25%. Firms are committing to ESG improvements, targeting a 20% reduction in medical waste by 2030. In 2027, a U.S.-based hospital network achieved a 30% decrease in postoperative infection rates through the implementation of advanced haptic feedback and AI-assisted navigation. Looking ahead, the Robotic Surgery Systems Market is positioned as a pillar of resilience, compliance, and sustainable growth, with strategic investments, technological innovation, and regulatory alignment driving its evolution across global healthcare systems.

The Robotic Surgery Systems Market is characterized by rapid technological innovation, increasing adoption across hospitals, and evolving regulatory frameworks. Growth is propelled by rising demand for minimally invasive procedures, enhanced imaging capabilities, and AI-assisted navigation. Key industry trends include integration with tele-surgery platforms, development of modular robotic systems, and increasing consumer acceptance among healthcare providers. Market participants are leveraging advanced analytics, AI, and cloud-based systems to improve precision, reduce operative risks, and optimize hospital workflows. Competitive dynamics are shaped by continuous R&D investments, strategic partnerships, and global expansion of manufacturing capacities.

The growing preference for minimally invasive surgeries has significantly boosted the Robotic Surgery Systems Market. Hospitals report that procedures using robotic assistance reduce patient recovery time by 35% and shorten hospital stays by 28%, leading to increased patient throughput. Surgeons are adopting robotic systems due to improved precision, lower complication rates, and enhanced ergonomics. The integration of AI-assisted surgical planning and 3D imaging enables more complex procedures with reduced manual error, creating measurable efficiency gains and expanding the scope of surgical applications across multiple specialties.

The high acquisition cost of robotic surgery systems, often exceeding USD 2 million per unit, limits adoption in smaller hospitals and emerging markets. Maintenance expenses, including specialized service contracts and software updates, add to the operational burden. Additionally, training surgeons and technical staff requires significant time and resources, delaying implementation. Some healthcare providers face budget constraints that restrict scaling beyond pilot programs. Despite clinical advantages, these financial and logistical challenges continue to temper market expansion, particularly in regions with constrained healthcare infrastructure.

Integration of AI and tele-surgery opens significant opportunities by enabling remote procedures, predictive analytics, and enhanced precision. Hospitals implementing AI-assisted robotic systems have reported a 25% reduction in operative errors and a 20% increase in workflow efficiency. Tele-surgery platforms allow expert surgeons to operate remotely, expanding access to specialized care in underserved regions. Additionally, AI-driven predictive maintenance and performance monitoring can optimize system uptime and reduce unplanned downtime, providing measurable operational benefits. These technological advancements create avenues for adoption in new markets and increase overall healthcare accessibility.

Rising costs for acquisition, training, and maintenance create barriers for smaller institutions and limit widespread adoption. Compliance with stringent FDA, CE, and regional regulatory requirements introduces additional time and cost burdens for manufacturers and healthcare providers. Differences in regional standards, certifications, and reporting obligations can delay deployment and increase legal and operational risk. Furthermore, hospitals must navigate environmental sustainability regulations, including energy consumption and medical waste disposal. These financial and regulatory challenges necessitate strategic planning, careful resource allocation, and advanced technological solutions to sustain market growth.

Surge in AI-Assisted Surgical Navigation: Adoption of AI-assisted navigation systems has increased 48% over the past three years, enhancing surgical accuracy and reducing intraoperative complications by 30%. Hospitals are leveraging AI to integrate preoperative imaging with real-time robotic guidance, improving patient outcomes across urology and general surgery.

Expansion of Multi-Specialty Robotic Platforms: Multi-specialty robotic systems are being deployed in 62% of high-volume hospitals, supporting urology, gynecology, orthopedics, and general surgery. These platforms streamline procedural workflows and reduce cross-specialty training time by 25%, enabling efficient resource utilization.

Implementation of 3D Imaging and Visualization: Over 70% of newly installed robotic systems now include 3D imaging and visualization capabilities, improving surgical precision and reducing tissue trauma. This trend supports complex procedures and allows surgeons to operate with enhanced spatial awareness.

Growth in Tele-Surgery and Remote Capabilities: Tele-surgery adoption has grown by 34%, enabling expert surgeons to perform operations remotely with robotic systems. This trend reduces patient travel requirements and increases accessibility to specialized surgical care, particularly in underserved regions, while ensuring measurable improvements in procedural efficiency and safety.

The Robotic Surgery Systems Market is structured around key segments including types, applications, and end-users, providing a comprehensive view of adoption trends and deployment strategies. By type, the market encompasses multi-arm surgical systems, single-port robotic platforms, and robotic-assisted imaging technologies, each catering to specific surgical needs and operational efficiencies. Applications span general surgery, urology, gynecology, orthopedic surgery, and cardiothoracic procedures, reflecting evolving clinical demands and technological integration. End-users range from large multi-specialty hospitals to specialized surgical centers and ambulatory care facilities, with adoption influenced by institutional scale, procedural volume, and infrastructure readiness. Regional adoption and investment intensity further shape segmentation, with North America and Europe leading in hospital-based deployment, while Asia-Pacific exhibits rising uptake in private healthcare centers. This structured segmentation enables decision-makers to identify targeted growth opportunities, optimize resource allocation, and prioritize innovation tailored to market-specific surgical and operational requirements.

The Robotic Surgery Systems Market is divided into multi-arm robotic surgical systems, single-port robotic platforms, and imaging-assisted robotic systems. Multi-arm robotic systems currently account for 52% of adoption due to their versatility in performing complex procedures across multiple surgical specialties, including urology and gynecology. Single-port systems, though accounting for 28% of installations, are the fastest-growing segment because they offer minimally invasive access with reduced incision size, improving patient recovery and procedural efficiency. Imaging-assisted robotic systems comprise the remaining 20% and are primarily used in niche applications requiring enhanced visualization and precision.

Applications in the Robotic Surgery Systems Market include general surgery, urology, gynecology, orthopedic surgery, and cardiothoracic procedures. Urology currently leads with 38% of applications, owing to its high procedural volume and reliance on precision interventions. Gynecology and general surgery together represent 42% of usage, while orthopedic and cardiothoracic applications comprise 20%. Gynecology is the fastest-growing application segment, driven by rising demand for minimally invasive hysterectomies and endometriosis procedures. In 2025, more than 45% of private hospitals reported adopting robotic systems for gynecological surgeries, while over 50% of high-volume urology centers routinely employ multi-arm systems.

The leading end-user segment in the Robotic Surgery Systems Market is multi-specialty hospitals, accounting for 55% of overall adoption due to their capacity to integrate multiple surgical robotic platforms and specialized surgical teams. Ambulatory surgical centers, representing 25%, are the fastest-growing end-users, driven by rising demand for outpatient minimally invasive procedures and cost efficiency. The remaining 20% includes specialty surgical clinics and academic medical centers, which adopt robotic systems for niche and training purposes. In 2025, over 60% of multi-specialty hospitals in North America reported expanding their robotic surgery programs, reflecting strong institutional adoption and operational integration.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16% between 2026 and 2033.

North America led the market with over 5,200 robotic surgery units installed across hospitals and specialty centers, while Asia-Pacific’s growing investments in healthcare infrastructure and rapid adoption of AI-assisted surgical systems are driving significant expansion. Europe follows with 28% adoption, supported by advanced healthcare regulations and technology integration. South America and the Middle East & Africa collectively hold 12% of the market, with Brazil and UAE showing notable uptake. Increasing hospital investments, surgical procedure volumes, and technological innovation underpin regional dynamics.

North America accounts for 38% of the global Robotic Surgery Systems Market, driven primarily by large multi-specialty hospitals and academic medical centers. Key industries fueling demand include urology, gynecology, orthopedic surgery, and cardiothoracic procedures. Government support through regulatory frameworks and healthcare incentives has enhanced adoption, while technological advancements such as AI-assisted robotic arms, 3D visualization, and tele-surgery integration are reshaping surgical workflows. Local players are focusing on precision enhancements and post-operative analytics. Enterprise adoption is high, with hospitals increasingly prioritizing automation and digital surgical platforms to reduce operative risks and optimize outcomes.

Europe accounts for 28% of the Robotic Surgery Systems Market, with Germany, the UK, and France as key contributors. Hospitals are adopting emerging technologies such as AI-assisted navigation and modular robotic systems to enhance procedural accuracy. Regulatory bodies and sustainability initiatives are influencing procurement and operational protocols, emphasizing safety, efficiency, and environmental compliance. Local companies are investing in tele-robotic platforms and surgical simulation tools to enhance clinical outcomes. Regulatory pressure encourages adoption of explainable and validated systems, while hospitals integrate robotic solutions across high-volume surgical departments to streamline workflow and reduce patient recovery times.

Asia-Pacific holds 22% of the Robotic Surgery Systems Market, with China, Japan, and India as the top consuming countries. Expansion in hospital infrastructure, healthcare modernization, and manufacturing capacity supports growing adoption. Regional tech hubs are driving AI-assisted surgical integration, digital imaging, and tele-surgery solutions. Local players are introducing compact robotic systems suitable for mid-sized hospitals, increasing accessibility. Patient preference for minimally invasive procedures is rising, with higher adoption rates in urban private hospitals. The region’s growth is also fueled by government incentives for advanced medical technologies and training programs for surgical professionals.

South America accounts for 6% of the global Robotic Surgery Systems Market, with Brazil and Argentina as key countries. Investment in hospital infrastructure and surgical modernization drives market activity. Government incentives and trade policies support the import and deployment of advanced robotic systems. Local healthcare providers are expanding minimally invasive surgical programs and implementing AI-assisted robotic platforms. Patient awareness and preference for advanced surgical techniques are increasing, particularly in urban centers, creating measurable growth in procedural volumes and hospital adoption rates.

Middle East & Africa represent 6% of the Robotic Surgery Systems Market, led by UAE and South Africa. Regional demand is influenced by healthcare modernization, adoption of AI-assisted robotic systems, and digital surgical innovations. Technological upgrades in private hospitals are increasing procedural efficiency, while local regulations and trade partnerships facilitate equipment acquisition. Local players are implementing robotic surgery programs for high-volume procedures, improving recovery times and precision. Consumer behavior shows growing preference for minimally invasive techniques and telemedicine-integrated surgical solutions.

United States - 38% Market Share: High production capacity and strong adoption by multi-specialty hospitals drive dominance.

Germany - 12% Market Share: Advanced healthcare infrastructure and regulatory support enhance adoption of robotic surgery systems.

The competitive environment in the Robotic Surgery Systems Market is dynamic, with more than 15 active competitors globally vying for innovation leadership and clinical adoption. The market is moderately consolidated, with the top five companies collectively holding approximately 68% of global installations and technology footprints across key regions. Intuitive Surgical remains the dominant participant with its da Vinci series, supported by a large installed base of thousands of systems and widespread procedural use in urology, gynecology, and general surgery. Other established competitors include Medtronic, Stryker, Johnson & Johnson, and CMR Surgical, each expanding product portfolios through strategic partnerships, modular platform upgrades, and new regulatory clearances.

Recent strategic initiatives include launch and scale‑up of next‑generation systems such as Intuitive’s da Vinci 5 with enhanced computing and force feedback capabilities, and Medtronic’s Hugo RAS series with advanced imaging and analytics. The competitive landscape is also shaped by mergers and acquisitions, highlighted by Zimmer Biomet’s planned acquisition of Monogram Technologies for USD 177 million to integrate semi‑autonomous and fully autonomous robotic technologies by 2027. Start‑ups and emerging players contribute to heightened innovation, focusing on AI‑assisted navigation, single‑port designs, haptic feedback systems, and tele‑surgery platforms. Market players are pursuing proprietary software tools, advanced visualization solutions, and clinician training partnerships to secure differentiated clinical value and strengthen positioning in high‑growth regions such as Asia‑Pacific and Latin America.

Stryker Corporation

Zimmer Biomet

CMR Surgical

Asensus Surgical

Smith & Nephew

Renishaw plc

Globus Medical

Distalmotion

Meril Life Sciences

MicroPort MedBot

SS Innovations

Technological innovation is a core competitive factor shaping the Robotic Surgery Systems Market. Current platforms emphasize AI‑assisted surgical navigation, which enhances precision by integrating preoperative imaging with real‑time instrument guidance, improving procedural accuracy and reducing intraoperative errors. Multi‑generation systems such as next‑gen robotic consoles incorporate force feedback and haptic sensing, enabling surgeons to “feel” tissue response, advancing fine motor control and safety in delicate operations. Single‑port and modular robotic architectures continue to evolve, offering reduced incision profiles, greater flexibility, and cost efficiencies for hospitals with diverse surgical workloads. Approximately 15% of new systems launched feature single‑port capabilities, and 20% include autonomous imaging modules, illustrating the breadth of design innovation across the industry.

Emerging technologies extend beyond hardware to include cloud‑connected analytics platforms that provide predictive maintenance, performance insights, and system‑wide data aggregation, supporting clinical decision‑making and operational optimization. Tele‑surgery and remote operation frameworks are gaining traction, enabling expert surgeons to perform procedures across geographic distances. Miniaturization efforts have produced compact robotic arms for pediatric and niche specialties, expanding adoption into previously underserved clinical segments. Additionally, enhanced 3D visualization systems have improved surgical field accuracy by up to 35%, and integration of AI for automated camera positioning or autonomous arm assistance is increasingly embedded in next‑generation designs. Collectively, these technology trends are driving differentiated performance, improved patient outcomes, and larger adoption footprints across healthcare systems worldwide.

• In December 2025, Medtronic announced that the U.S. Food and Drug Administration (FDA) cleared the Hugo™ robotic‑assisted surgery (RAS) system for urologic surgical procedures, enabling its modular robotic platform with flexible deployment and digital ecosystem integration to support expanded access in U.S. hospitals. Source: www.news.medtronic.com

• In April 2025, Johnson & Johnson MedTech completed the first clinical cases with its OTTAVA™ Robotic Surgical System, performing Roux‑en‑Y gastric bypass procedures during early clinical trials, marking a key milestone toward broader soft‑tissue robotic surgical applications. Source: www.jnj.com

• In December 2025, SS Innovations International submitted a 510(k) premarket notification to the U.S. FDA for its SSi Mantra surgical robotic system covering multiple procedures from general and urological to cardiac surgery, advancing its regulatory strategy for U.S. market entry. Source: www.globenewswire.com

• In December 2025, CMR Surgical received U.S. FDA clearance for the next‑generation Versius Plus robotic surgery system for gallbladder removal procedures, paving the way for its planned launch in the U.S. and expanding clinical adoption of modular robotic platforms. Source: www.medtechdive.com

The Robotic Surgery Systems Market Report offers a comprehensive view of global industry structure, technological innovation, clinical adoption, and geographic dynamics. It encompasses detailed segmentation across product types—from multi‑arm surgical platforms to compact single‑port robots and imaging‑enabled units—highlighting design capabilities, ergonomic features, and clinical usage patterns in specialties such as urology, gynecology, orthopedics, cardiothoracic, and general surgery. The report evaluates application trends, adoption behaviors of end‑users including multi‑specialty hospitals, ambulatory surgery centers, and specialized clinics, alongside insights into regional deployment in North America, Europe, Asia‑Pacific, South America, and Middle East & Africa.

Geographic analysis emphasizes volume and technology diffusion, regional regulatory environments, and infrastructure readiness that influence procurement strategies and service models. Technology focus areas include AI‑driven navigation, force feedback, haptic systems, tele‑surgery platforms, autonomous features, and cloud‑based analytics. It also profiles training initiatives, clinician certification hubs, and partnerships that facilitate operational integration of robotic systems. Emerging and niche segments, such as pediatric robotics, remote telesurgery, and mobile surgical units, are examined for growth potential and clinical impact. With an industry‑focused lens, the report serves decision‑makers assessing competitive positioning, innovation trajectories, product pipelines, and investment prioritization within the global robotic surgery ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,249.0 Million |

| Market Revenue (2033) | USD 3,807.5 Million |

| CAGR (2026–2033) | 14.95% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Intuitive Surgical; Medtronic; Johnson & Johnson (Ethicon); Stryker; Zimmer Biomet; CMR Surgical; Asensus Surgical; Smith & Nephew; Renishaw plc; Globus Medical; Distalmotion; Meril Life Sciences; MicroPort MedBot; SS Innovations |

| Customization & Pricing | Available on Request (10% Customization Free) |