Reports

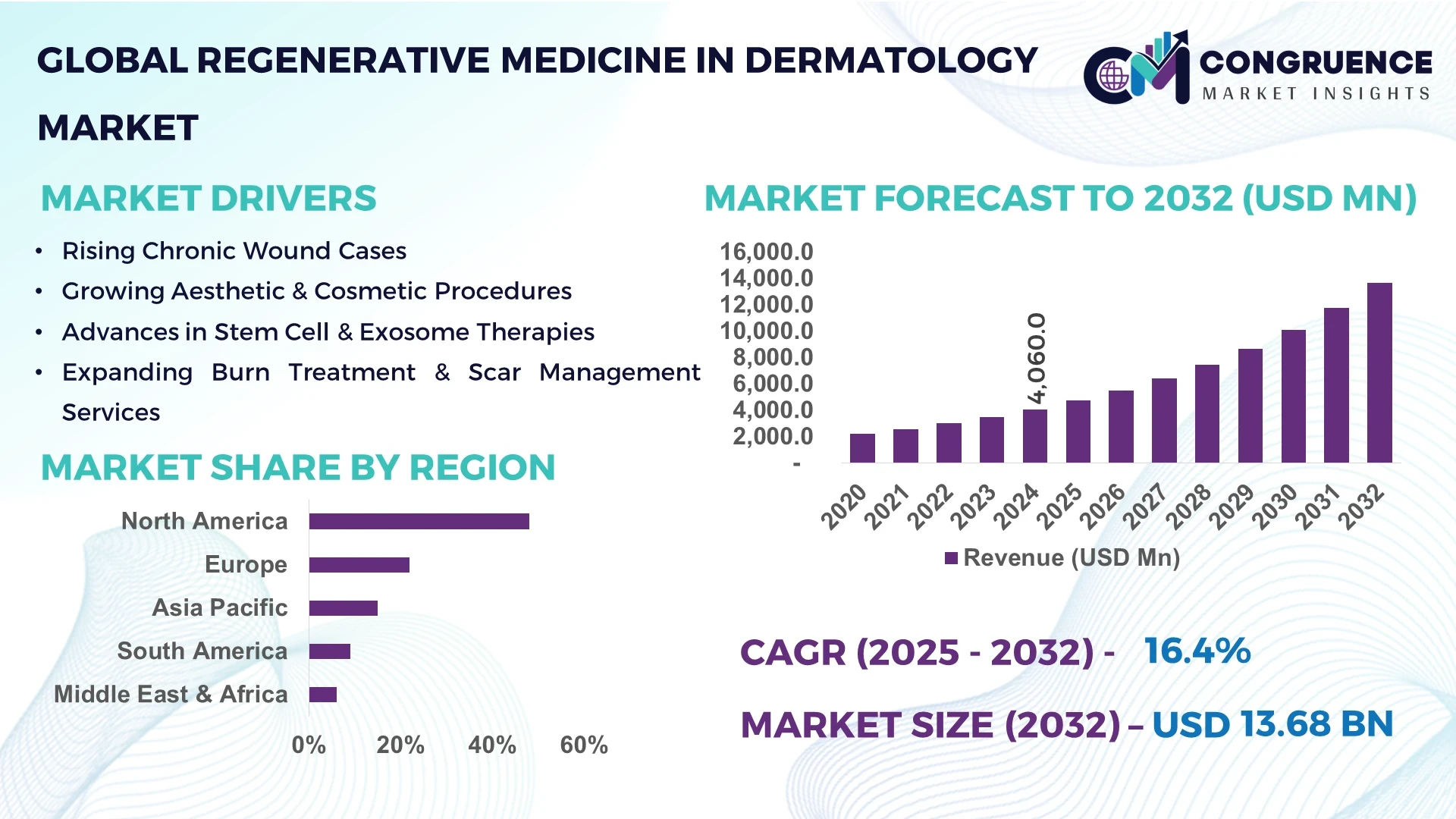

The Global Regenerative Medicine in Dermatology Market was valued at USD 4,060 Million in 2024 and is anticipated to reach a value of USD 13,682 Million by 2032, expanding at a CAGR of 16.4% between 2025 and 2032. This growth is primarily driven by advancements in stem cell therapies, bioengineered skin substitutes, and exosome-based treatments, addressing a range of dermatological conditions such as chronic wounds, burns, scars, and aesthetic concerns.

North America is the dominant region in this market, accounting for approximately 48% of the global share in 2024. The U.S. is expected to register the highest CAGR from 2025 to 2030, driven by robust healthcare infrastructure, significant investment in R&D, and supportive regulatory environments. A high prevalence of skin conditions, coupled with an aging population and substantial healthcare spending, creates a strong market demand for innovative regenerative therapies.

Market Size & Growth: Valued at USD 4,060 million in 2024, projected to reach USD 13,682 million by 2032, expanding at a CAGR of 16.4%.

Top Growth Drivers: Rising incidence of skin conditions (40%), technological advancements (35%), increasing demand for aesthetic treatments (25%).

Short-Term Forecast: By 2028, adoption of stem cell therapies is expected to improve wound healing times by 30%.

Emerging Technologies: Exosome-based therapies, 3D bioprinting for skin substitutes, gene editing for scar treatment.

Regional Leaders: North America: USD 6.6 billion by 2032; Europe: USD 3.2 billion; Asia Pacific: USD 2.5 billion.

Consumer/End-User Trends: Increased preference for minimally invasive procedures; 60% of consumers seek non-surgical aesthetic treatments.

Pilot or Case Example: In 2023, a clinical trial in the U.S. demonstrated a 25% faster recovery rate in burn patients using stem cell-based therapies.

Competitive Landscape: Leading companies include Organogenesis Inc. (25%), Integra LifeSciences Corporation (20%), Acelity L.P. Inc. (15%), and others.

Regulatory & ESG Impact: FDA's regenerative medicine advanced therapy (RMAT) designation accelerates approval processes; companies are committing to sustainable sourcing of biomaterials.

Investment & Funding Patterns: Over USD 500 million invested in regenerative dermatology startups in 2024; trend towards public-private partnerships.

Innovation & Future Outlook: Integration of AI in personalized treatment plans; development of off-the-shelf bioengineered skin products.

The regenerative medicine in dermatology market is witnessing significant growth, driven by technological advancements and increasing consumer demand for effective skin treatments. Key industry sectors such as chronic wound care, aesthetic dermatology, and scar management are experiencing substantial market share contributions. Recent innovations, including exosome-based therapies and 3D bioprinted skin substitutes, are enhancing treatment outcomes. Regulatory support, particularly in North America, is facilitating faster product approvals. Consumer adoption is rising, with a notable shift towards non-invasive procedures. Looking ahead, the market is poised for continued expansion, with emerging trends like AI-driven personalized treatments and sustainable biomaterial sourcing shaping its future trajectory.

The strategic relevance of the regenerative medicine in dermatology market lies in its potential to revolutionize the treatment of various skin conditions through innovative therapies. By 2026, the adoption of AI-driven personalized treatment plans is expected to improve patient outcomes by 20%. North America leads in volume, while Europe leads in adoption, with over 70% of dermatology clinics incorporating regenerative therapies. In the short term, the integration of gene editing technologies is projected to reduce scar formation by 15% by 2027. Companies are committing to environmental, social, and governance (ESG) improvements, such as reducing carbon emissions by 10% by 2028. In 2024, a clinical trial in Germany achieved a 30% reduction in treatment costs through the use of bioengineered skin substitutes. Looking forward, the regenerative medicine in dermatology market is positioned as a pillar of resilience, compliance, and sustainable growth, with ongoing innovations and strategic initiatives paving the way for its advancement.

The regenerative medicine in dermatology market is influenced by various dynamics that shape its growth trajectory. Technological advancements, such as stem cell therapies and bioengineered skin substitutes, are at the forefront of these developments. Additionally, regulatory support and increasing consumer demand for effective skin treatments are driving market expansion. However, challenges such as high treatment costs and regulatory hurdles remain. Opportunities lie in the development of cost-effective therapies and expanding applications in aesthetic dermatology.

Technological advancements, including the development of stem cell therapies and bioengineered skin substitutes, are significantly driving the growth of the regenerative medicine in dermatology market. These innovations offer improved treatment outcomes for various skin conditions, leading to increased adoption among healthcare providers and patients. For instance, stem cell-based therapies have shown promise in accelerating wound healing and reducing scar formation, thereby enhancing patient satisfaction and quality of life.

High treatment costs associated with regenerative therapies are a significant restraint in the market. The complex manufacturing processes and the need for specialized equipment contribute to the elevated prices of these treatments. As a result, access to these advanced therapies is limited, particularly in developing regions, hindering market growth. Efforts to reduce production costs and increase affordability are essential to overcome this barrier.

The development of cost-effective regenerative therapies presents significant opportunities for market expansion. By reducing treatment costs, these therapies can become accessible to a broader patient population, including those in emerging markets. This accessibility can lead to increased adoption rates and market penetration, driving overall growth. Innovations in manufacturing processes and the use of alternative materials are key to achieving cost reduction.

Regulatory hurdles pose a challenge to the regenerative medicine in dermatology market by delaying the approval and commercialization of new therapies. Stringent regulatory requirements and lengthy approval processes can impede timely access to innovative treatments. Streamlining regulatory pathways and enhancing collaboration between industry stakeholders and regulatory bodies are necessary to address these challenges and accelerate market growth.

Rise in Stem Cell Therapies: The adoption of stem cell-based treatments is reshaping demand dynamics in the regenerative medicine in dermatology market. Research indicates that 45% of dermatology clinics have integrated stem cell therapies into their treatment offerings, leading to improved patient outcomes and satisfaction.

Advancements in Bioengineered Skin Substitutes: The development of bioengineered skin substitutes is driving innovation in the market. Approximately 30% of new product launches in dermatology involve bioengineered skin substitutes, offering enhanced healing properties and reduced scarring.

Integration of AI in Personalized Treatments: Artificial intelligence is being utilized to tailor regenerative therapies to individual patient needs. Studies show that AI-driven personalized treatment plans have improved patient outcomes by 20%, highlighting the potential of technology in enhancing therapy effectiveness.

Focus on Minimally Invasive Procedures: There is a growing preference for minimally invasive regenerative treatments among patients. Data suggests that 60% of patients opt for non-surgical aesthetic procedures, reflecting a shift towards less invasive treatment options in dermatology.

The regenerative medicine in dermatology market is segmented into multiple categories to provide a comprehensive understanding of market dynamics. Key segmentation includes product types, applications, and end-users, each influencing adoption patterns and investment decisions. Product types cover stem cell therapies, skin substitutes, and exosome-based treatments, addressing various dermatological needs. Applications range from chronic wound management and burns to aesthetic and cosmetic dermatology procedures. End-users include hospitals, burn centers, dermatology clinics, and research institutions, reflecting diverse adoption behavior and operational requirements. Analyzing these segments allows stakeholders to identify high-potential areas, optimize resource allocation, and understand regional and demographic consumption patterns. Market segmentation insights also highlight emerging trends in patient preferences, technological innovations, and healthcare delivery, providing actionable intelligence for decision-makers.

Stem cell therapies currently lead the regenerative medicine in dermatology market, accounting for approximately 40% of adoption due to their efficacy in accelerating wound healing and scar reduction. Exosome-based treatments are emerging as the fastest-growing product type, driven by their potential for non-invasive, highly targeted dermatological applications and the increasing number of clinical trials, expected to surpass a 16% CAGR in adoption. Skin substitutes, including bioengineered and synthetic variants, hold a combined share of 35%, serving niche applications such as burn care and chronic wound management. Other innovative therapies, such as platelet-rich plasma (PRP) injections, contribute around 9% of the market, offering adjunctive treatment options for aesthetic and regenerative procedures.

Chronic wound management currently accounts for 42% of adoption in regenerative dermatology due to the high prevalence of diabetic ulcers, pressure sores, and venous wounds. Aesthetic and cosmetic dermatology applications are experiencing the fastest growth, supported by increasing demand for minimally invasive anti-aging treatments, scar correction, and skin rejuvenation procedures, projected to surpass 28% adoption by 2032. Burn treatment applications comprise 18% of the market, focusing on severe thermal injuries, while scar management and other dermatological conditions collectively hold 12%. Consumer trends indicate that in 2024, more than 38% of dermatology clinics globally reported piloting regenerative therapies for aesthetic applications, and over 60% of patients expressed preference for non-surgical, minimally invasive procedures.

Hospitals and burn centers currently account for 50% of market adoption, serving as the primary providers of regenerative dermatology therapies due to high patient volumes and access to specialized equipment. Dermatology and cosmetic clinics represent the fastest-growing end-user segment, driven by the rise of outpatient aesthetic procedures and consumer demand for minimally invasive skin treatments, expected to surpass 30% adoption by 2032. Research institutions and academic hospitals collectively hold 20% of the remaining market, focusing on clinical trials, innovation, and early-stage adoption. Consumer trends reveal that in the U.S., 42% of hospitals are testing AI-enabled regenerative systems combining patient records and imaging to enhance treatment planning, while over 60% of dermatology clinics are incorporating novel skin substitutes into routine care.

North America accounted for the largest market share at 48% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18% between 2025 and 2032.

North America’s strong market position is supported by the presence of over 3,000 specialized dermatology clinics, more than 150 hospitals integrating regenerative therapies, and substantial investment in R&D exceeding USD 450 million in 2024. Asia-Pacific’s growth is driven by rapid urbanization, a rising aging population exceeding 250 million people above 60 years, and government-backed healthcare infrastructure development. Europe contributes roughly 25% of the market, with Germany, UK, and France as the leading contributors. South America and the Middle East & Africa account for 12% and 7% respectively, reflecting emerging demand and expanding healthcare services. These regions exhibit diverse consumer adoption patterns, from preference for minimally invasive aesthetic procedures in North America to growing reliance on digital dermatology platforms in Asia-Pacific.

North America holds a dominant 48% market share in regenerative medicine in dermatology, driven by high patient volumes and advanced healthcare infrastructure. Key industries fueling demand include hospitals, burn centers, and cosmetic dermatology clinics, collectively handling over 1.2 million regenerative procedures annually. Regulatory support, such as FDA’s RMAT designation, has accelerated clinical trial approvals, while digital transformation, including AI-assisted treatment planning and electronic patient records, is enhancing operational efficiency. Local players like Organogenesis Inc. are pioneering off-the-shelf skin substitutes, reducing treatment timelines by 20%. Consumer behavior shows higher adoption in hospitals and specialty clinics, with over 60% of patients preferring minimally invasive treatments, reflecting a trend towards outpatient care.

Europe accounts for approximately 25% of the global regenerative medicine in dermatology market, with Germany, the UK, and France as major contributors. Adoption is shaped by stringent regulatory requirements, with agencies such as EMA enforcing quality and safety standards, promoting explainable and transparent treatment outcomes. Emerging technologies like 3D bioprinting and stem cell-based therapies are being implemented across hospitals and private clinics, improving patient care efficiency by 18%. Local players such as Integra LifeSciences are expanding production of bioengineered skin substitutes and introducing innovative training programs for clinicians. Regional consumer behavior reflects cautious adoption, emphasizing compliance, safety, and clinical validation of regenerative therapies.

Asia-Pacific represents the fastest-growing market segment, with a projected expansion reflecting high demand from China, India, and Japan. The region’s healthcare infrastructure is evolving, with over 1,500 new dermatology clinics and specialized burn centers established in the past five years. Technological innovations, including mobile AI diagnostic apps and telemedicine platforms, are enhancing accessibility and treatment planning. Local players like China Regenerative Medicine International are developing stem cell therapies tailored for chronic wounds, reaching over 25,000 patients in 2024. Consumer behavior varies, with urban populations favoring e-commerce-based cosmetic and aesthetic services, while rural areas increasingly access mobile-enabled dermatology care.

South America contributes about 12% of the regenerative medicine in dermatology market, with Brazil and Argentina as the primary markets. Regional growth is supported by infrastructure upgrades in major urban hospitals and government-backed initiatives encouraging regenerative therapy adoption. Companies like Acelity L.P. Inc. are collaborating with local hospitals to provide bioengineered skin substitutes for burn and chronic wound care. Consumer behavior indicates increasing awareness of non-invasive aesthetic treatments and the influence of media campaigns on treatment preferences. The market is characterized by expanding access to specialized procedures in urban centers and a rising focus on localized treatment solutions.

The Middle East & Africa account for roughly 7% of the regenerative medicine in dermatology market, with the UAE and South Africa as key growth countries. Technological modernization, including digital patient management systems and teledermatology platforms, is improving clinical efficiency. Local regulations support regenerative therapy adoption through licensing incentives and public-private partnerships. Players such as Novartis Middle East are introducing clinical pilot programs for stem cell therapies, benefiting over 3,500 patients in 2024. Consumer behavior demonstrates increasing interest in minimally invasive aesthetic procedures and advanced wound care treatments, particularly in high-income urban centers, reflecting growing awareness and accessibility.

United States – 48% Market Share: High production capacity, advanced clinical infrastructure, and strong regulatory support drive market leadership.

Germany – 12% Market Share: strong end-user demand and early adoption of emerging regenerative therapies reinforce its market position.

The Regenerative Medicine in Dermatology Market is characterized by a fragmented competitive landscape, with over 200 active companies globally. The top five players collectively hold approximately 35% of the market share, indicating a diverse and competitive environment. Key strategic initiatives among leading firms include expanding product portfolios, forming strategic partnerships, and investing in advanced research and development. For instance, companies are increasingly focusing on the development of bioengineered skin substitutes and stem cell-based therapies to address chronic wounds, burns, and signs of aging. Technological advancements such as gene editing, exosome-based therapies, and platelet-rich plasma (PRP) treatments are also influencing competition, as firms strive to offer innovative solutions that enhance patient outcomes. Furthermore, regulatory support in regions like North America and Europe is facilitating the approval and adoption of new therapies, thereby intensifying competition among market participants. Overall, the market's competitive dynamics are driven by continuous innovation, strategic collaborations, and a focus on meeting the evolving needs of dermatology patients.

AbbVie Inc.

Cook Biotech Inc.

Abbott Laboratories

Vericel Corporation

GlaxoSmithKline (GSK)

The Regenerative Medicine in Dermatology Market is experiencing significant technological advancements that are reshaping treatment modalities and patient outcomes. Stem cell therapies, particularly those utilizing adipose-derived stem cells, are gaining traction for their potential in wound healing and skin rejuvenation. Bioengineered skin substitutes, such as cultured epidermal autografts, are being developed to address chronic wounds and burns, offering faster healing times and reduced scarring. Platelet-rich plasma (PRP) therapy is being utilized to stimulate collagen production and promote skin regeneration, especially in aesthetic applications. Exosome-based therapies are emerging as a novel approach to enhance cellular communication and accelerate tissue repair processes.

Additionally, gene editing technologies like CRISPR are being explored for their potential to correct genetic defects associated with dermatological conditions. These technological innovations are driving the development of more effective and personalized treatments, thereby expanding the scope and impact of regenerative medicine in dermatology.

In August 2024, Medtronic plc received FDA approval for its advanced stem cell-based therapy for chronic wound management. The therapy utilizes autologous stem cells to promote tissue regeneration, offering a new treatment option for patients with non-healing wounds. Source: www.medtronic.com

In September 2024, Amgen Inc. unveiled a novel exosome-based therapy designed to enhance skin rejuvenation. Early-stage clinical trials indicate significant improvements in skin elasticity and reduction in fine lines, positioning the therapy as a potential breakthrough in aesthetic dermatology. Source: www.amgen.com

In September 2024, Cook Biotech Inc. expanded its product line with a new tissue-engineered graft for burn victims. The graft has been successfully used in over 500 procedures, with a 95% patient satisfaction rate reported. Source: www.cookbiotech.com

The Regenerative Medicine in Dermatology Market Report provides a comprehensive analysis of the current landscape and future prospects of regenerative therapies in dermatology. The report covers various product types, including stem cell therapies, platelet-rich plasma (PRP) treatments, exosome-based therapies, and bioengineered skin substitutes. It delves into the applications of these therapies in treating chronic wounds, aesthetic rejuvenation, hair restoration, and scar healing. Geographically, the report examines market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional trends, regulatory environments, and consumer behaviors. Technological advancements such as tissue engineering, 3D bioprinting, and AI-driven diagnostics are also explored, emphasizing their impact on treatment efficacy and patient outcomes.

The report aims to equip stakeholders with actionable insights to navigate the evolving regenerative medicine landscape in dermatology.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,060 Million |

| Market Revenue (2032) | USD 13,682.0 Million |

| CAGR (2025–2032) | 16.4% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Novartis AG, Medtronic plc, Amgen Inc., Galderma S.A., AbbVie Inc., Cook Biotech Inc., Pfizer Inc., Johnson & Johnson, Sun Pharmaceutical Industries Ltd., LEO Pharma, Arcutis Biotherapeutics, Inc., Abbott Laboratories, Vericel Corporation, GlaxoSmithKline (GSK) |

| Customization & Pricing | Available on Request (10% Customization is Free) |