Reports

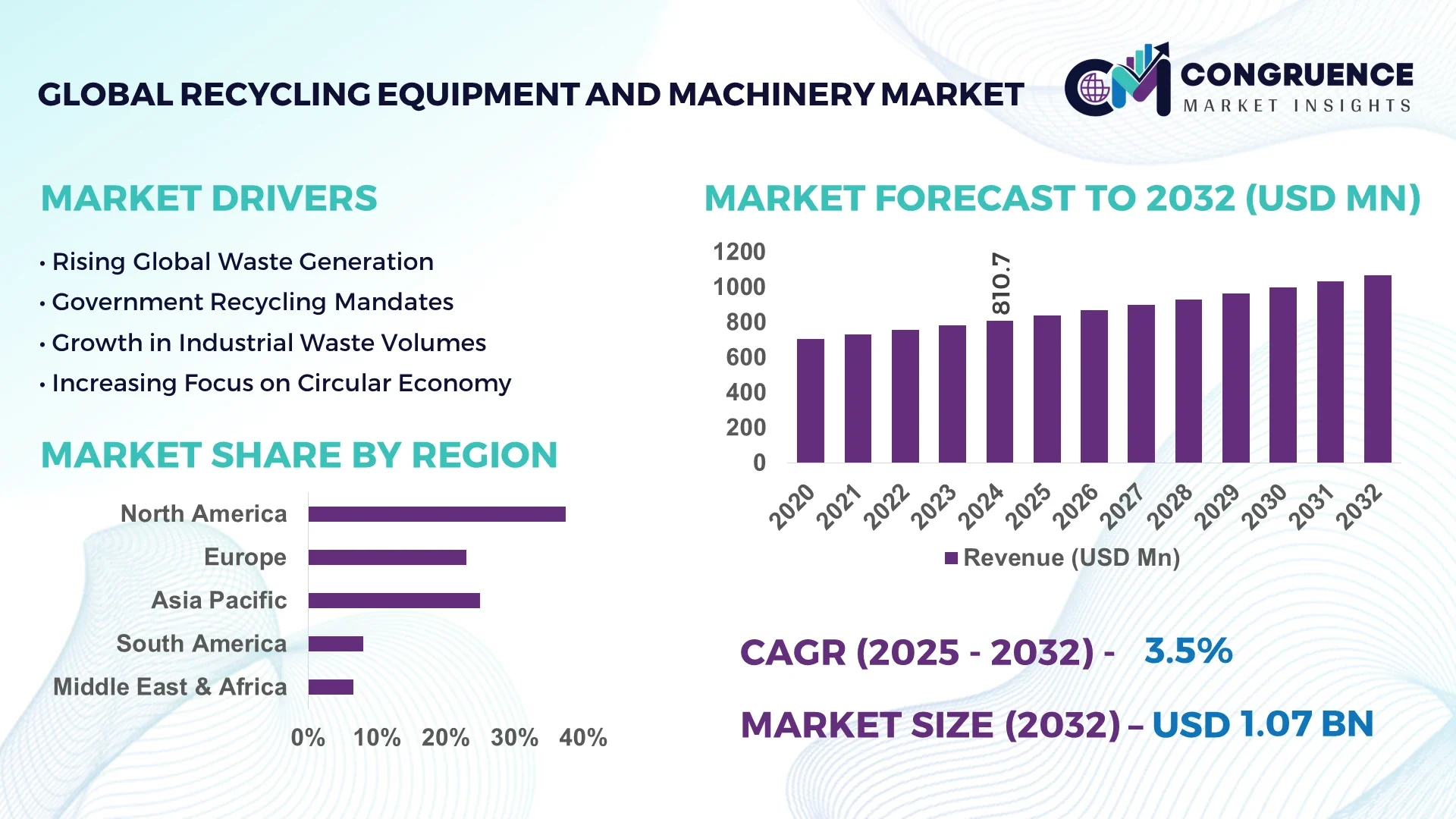

The Global Recycling Equipment and Machinery Market was valued at USD 810.7 Million in 2024 and is anticipated to reach a value of USD 1031.43 Million by 2032 expanding at a CAGR of 3.5% between 2025 and 2032.

The United States dominates the recycling equipment and machinery market, showcasing substantial investments in advanced recycling technologies and a strong regulatory framework that supports sustainable waste management practices. In 2024, the U.S. accounted for the largest share of the market, driven by the rising demand for efficient waste sorting and processing machinery.

Globally, the recycling equipment and machinery market is witnessing rapid advancements in mechanical recycling systems, including shredders, balers, and sorting machines. The market growth is fueled by increasing environmental concerns and stringent government regulations mandating waste reduction. In 2024 alone, over 70% of the global recycling machinery sales were attributed to equipment designed for plastics and electronic waste processing. Furthermore, the demand for automated and semi-automated machinery has surged, enhancing recycling throughput and reducing operational costs. With growing urbanization and industrialization, the need for innovative recycling solutions such as advanced optical sorters and conveyor systems continues to rise, pushing the market toward greater efficiency and sustainability.

Artificial Intelligence (AI) is revolutionizing the recycling equipment and machinery market by significantly improving the efficiency, accuracy, and automation of waste processing operations. AI-powered technologies, such as machine learning algorithms and computer vision systems, enable real-time identification and sorting of recyclable materials with high precision. In 2024, the integration of AI in recycling machinery enhanced sorting accuracy by up to 95%, reducing contamination in recycled materials and improving the quality of end products. AI also facilitates predictive maintenance of recycling equipment, minimizing downtime and optimizing operational performance by analyzing sensor data for early detection of mechanical faults.

Moreover, AI-driven robotics are increasingly employed in material recovery facilities to automate repetitive tasks, increasing productivity while lowering labor costs. Data analytics platforms powered by AI help recycling companies to optimize logistics and resource allocation, leading to more sustainable and cost-effective recycling processes. The deployment of AI in recycling equipment extends beyond sorting, as it also supports dynamic process adjustments based on input material variability, ensuring consistent throughput and efficiency. Overall, AI integration is propelling the recycling equipment and machinery market toward a future where smart, automated systems are standard, driving higher recovery rates and reducing environmental impact.

"In early 2025, a leading recycling machinery manufacturer launched an AI-enhanced optical sorting system capable of processing over 15 tons of mixed recyclables per hour with a material recognition accuracy exceeding 97%, setting new industry benchmarks in sorting speed and precision."

The recycling equipment and machinery market is shaped by various dynamic factors influencing its growth trajectory and adoption across industries. Increasing industrial waste generation, coupled with growing environmental regulations worldwide, has created a substantial need for advanced recycling solutions. The market is witnessing significant innovations in machinery design, improving the efficiency and sustainability of waste processing. Additionally, government incentives and support for circular economy initiatives drive the deployment of high-performance recycling equipment. However, challenges such as high initial investment costs and technical complexities in machinery operation pose constraints. Overall, the market dynamics highlight a balance between emerging growth opportunities and operational hurdles that industry players must navigate to capitalize on the evolving demand for recycling equipment and machinery.

One of the primary drivers of market growth is the rise in stringent environmental regulations across key regions mandating recycling and waste reduction. In 2024, more than 60 countries implemented new or enhanced laws targeting improved recycling rates and reduction of landfill usage. This has resulted in increased demand for efficient recycling equipment, including shredders, separators, and automated sorting systems. Industrial sectors such as construction, electronics, and packaging are investing heavily in recycling machinery to comply with these regulations and meet sustainability goals. Furthermore, corporate social responsibility commitments are pushing manufacturers to adopt advanced recycling technologies, driving market expansion.

Despite the increasing need for recycling equipment, high upfront capital investment remains a major restraint for many small to medium enterprises. Advanced recycling machinery, especially those integrated with AI and automation technologies, can require substantial financial outlays that deter widespread adoption. Maintenance and operational costs also add to the total expenditure, making it difficult for new entrants or smaller recycling firms to upgrade their existing equipment. Additionally, limited access to financing and leasing options further restricts market growth in developing regions where infrastructure development is still underway.

The global shift towards circular economy models presents significant opportunities for the recycling equipment and machinery market. Increasing efforts to reuse and recycle materials in industries such as automotive, packaging, and electronics are creating a rising demand for state-of-the-art recycling systems. In 2024, multiple multinational corporations announced initiatives focused on reducing raw material dependency through enhanced recycling processes. This trend encourages investments in modular and scalable recycling machinery that can handle diverse waste streams efficiently. Additionally, government-backed circular economy projects provide funding and incentives that further stimulate market growth and innovation.

One of the significant challenges facing the recycling equipment and machinery market is the complexity involved in processing heterogeneous and contaminated waste materials. Mixed waste streams, especially from municipal solid waste and electronic scrap, often contain contaminants that reduce the efficiency and lifespan of recycling machinery. The need for sophisticated pre-sorting and cleaning systems increases operational costs and complicates workflow. Moreover, inconsistent waste composition requires adaptable and flexible machinery, raising design and engineering challenges. These factors collectively impact throughput rates and the quality of recycled outputs, presenting a major obstacle for manufacturers and recyclers alike.

Rise in Modular and Prefabricated Construction:Modular recycling systems are gaining traction for their quick installation and scalability. Prefabricated machinery components allow recycling plants to expand capacity efficiently, reducing downtime and installation costs. Urban areas in Europe and North America are leading in adopting modular systems due to space and time constraints.

Automation and Smart Technology Integration:AI-powered optical sorters, robotic arms, and sensor-based machines are becoming standard. In 2024, automated sorting technology was installed in over 65% of new recycling lines globally, significantly improving accuracy and reducing labor. These innovations reduce contamination and increase throughput.

Energy-Efficient Equipment Design:Manufacturers are increasingly focused on reducing energy consumption. Technologies such as variable frequency drives (VFDs) and optimized motors lower operational costs and environmental impact. Machines designed for emerging waste types, including e-waste and mixed plastics, are gaining popularity.

Customized Industry-Specific Machinery:There is rising demand for recycling equipment tailored to sector-specific waste streams, especially in automotive and packaging industries. This trend drives the development of specialized shredders and separation technologies, enabling higher recovery rates and better material quality.

The Recycling Equipment and Machinery market is broadly segmented by type, application, and end-user to address diverse industry needs and maximize operational efficiency. Types include shredders, balers, separators, and conveyor systems, each serving a specific function in the recycling process. Applications span municipal solid waste management, industrial waste recycling, electronic waste processing, and packaging recycling, reflecting varied waste sources and treatment needs. End-users range from waste management companies and manufacturing industries to government agencies and SMEs, with differing machinery requirements based on scale and specialization. This segmentation provides valuable insights into demand drivers and growth opportunities across regions and sectors.

The shredders segment holds the largest market share at approximately 35%, as shredding is essential for reducing waste size and preparing materials for further processing. Shredders are widely used across municipal and industrial applications due to their versatility in handling plastics, metals, and mixed waste. Balers represent around 25% of the market, favored for their ability to compact recyclable materials, improving transport and storage efficiency. Separators, including AI-driven optical sorters and magnetic separators, constitute about 20% and are the fastest-growing segment. This growth is fueled by increasing demand for precise material separation to enhance recycling quality, especially for plastics and metals. Conveyor systems make up the remaining market share and primarily support automation in recycling plants. Their growth is steady but limited compared to other segments.

Municipal solid waste management leads the application segment with an estimated 40% market share, driven by urban population growth and strict waste disposal regulations. Recycling equipment used in this sector is designed for high-volume processing and varied waste types. Industrial recycling follows with around 30% share, as manufacturers increasingly adopt recycling to reduce raw material costs and comply with environmental policies. Electronic waste recycling is the fastest-growing application, expanding rapidly due to rising volumes of discarded electronics and the need for advanced machinery capable of recovering valuable metals and components. Packaging recycling accounts for roughly 20% of the market and benefits from bans on single-use plastics and increased consumer environmental awareness, encouraging investments in sorting and processing equipment.

Waste management companies dominate the end-user segment, accounting for over 45% market share, due to their large-scale operations requiring comprehensive recycling machinery solutions. These firms invest heavily in automated and AI-integrated equipment to optimize processing efficiency and material recovery. Manufacturing industries represent approximately 30% of the market, increasingly incorporating recycling equipment in-house to minimize waste disposal expenses and achieve sustainability goals. Government bodies and municipalities, with about 15% market share, are significant end-users as they build infrastructure to meet regulatory recycling targets. The fastest-growing end-user segment is small and medium enterprises (SMEs), particularly in emerging markets, where modular and cost-effective recycling machinery enables expansion and compliance with environmental standards.

North America accounted for the largest market share at 37.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

North America’s dominance is driven by advanced recycling infrastructure and high adoption of automated equipment across municipal and industrial sectors. Asia-Pacific’s rapid growth is supported by increasing urbanization, government initiatives for sustainable waste management, and rising industrialization. Europe holds a significant share due to stringent environmental regulations and a strong focus on circular economy practices. Meanwhile, emerging markets in South America and the Middle East & Africa are gradually increasing investments in recycling machinery to address waste challenges and improve resource recovery.

Pioneers Smart Recycling with Advanced Machinery Adoption

North America’s recycling equipment and machinery market shows robust demand, especially in the U.S. and Canada, where municipal solid waste recycling rates exceed 35%. Advanced shredders and AI-powered sorting machines are increasingly integrated to improve processing efficiency. The rise of electronic waste recycling has spurred investment in specialized machinery designed for delicate material separation. Moreover, government programs focused on plastic and metal recycling have accelerated adoption of balers and conveyor systems. This region also benefits from strong industrial recycling activity in sectors such as automotive and packaging, driving consistent demand for innovative recycling technologies and machinery upgrades.

Leads the Charge in Sustainable Recycling Solutions and Regulatory Compliance

Europe maintains a significant market presence, with Germany, France, and the UK leading equipment adoption due to strict waste management regulations and ambitious recycling targets exceeding 50% for certain materials. The market is witnessing a surge in demand for modular and prefabricated recycling systems that reduce installation time and operational costs. Automated sorting technologies, including optical and magnetic separators, are widely used across European recycling plants to enhance material recovery rates. Industrial and packaging waste recycling are key application areas, supported by government incentives encouraging manufacturers to integrate recycling machinery to reduce environmental impact.

Drives Growth through Rapid Industrialization and Urban Waste Management

Asia-Pacific is experiencing rapid growth in recycling equipment demand, particularly in China, Japan, and India, where urbanization and industrial waste volumes are rising sharply. The region’s governments are launching large-scale waste management projects incorporating advanced machinery such as high-capacity shredders and AI-enabled sorting systems. Plastic recycling machinery adoption is especially high, reflecting efforts to combat marine pollution and reduce landfill dependency. The rise of electronic and construction waste recycling industries further propels market growth, with manufacturers investing in modular and energy-efficient recycling machines tailored for varied local requirements.

Recycling Sector Expands with Infrastructure Development and Innovation

South America’s recycling equipment market is evolving, led by Brazil and Argentina, where growing environmental awareness is driving demand for efficient waste processing machinery. Shredders and balers are widely used to handle municipal and industrial waste, with increasing interest in automated sorting systems to improve recycling rates. Despite infrastructure challenges, investments in recycling technology have surged due to stricter environmental policies and support from international sustainability initiatives. The region is focusing on developing integrated recycling facilities that combine multiple machinery types to process diverse waste streams, boosting overall market potential.

Focus on Circular Economy and Emerging Recycling Technologies

In the Middle East & Africa, the recycling equipment market is gradually expanding with Saudi Arabia and South Africa as key players. Governments are launching sustainability programs aimed at reducing landfill use and increasing material recovery, prompting demand for balers, shredders, and separators. The market growth is supported by rising industrial waste recycling and increasing adoption of modular machinery suited for harsh environmental conditions. Although still developing, the region is witnessing increased awareness and investments from both private and public sectors, with a focus on plastic and metal recycling to meet regional environmental targets.

United States (28%): The U.S. leads due to advanced recycling infrastructure, high technological adoption, and strong regulatory frameworks supporting recycling equipment investments.

China (24%): China’s market is driven by large-scale waste generation, rapid urbanization, and government mandates promoting sustainable waste processing and advanced recycling machinery.

The recycling equipment and machinery market is highly competitive and characterized by the presence of numerous global and regional players focusing on innovation, product development, and strategic partnerships. Key companies are investing heavily in automation technologies, such as AI-based sorting systems and energy-efficient shredders, to differentiate their offerings. The market sees frequent collaborations between equipment manufacturers and recycling firms to tailor machinery to specific waste streams. Companies are also expanding their production capacities and enhancing after-sales service networks to capture larger shares in emerging markets. Product launches with enhanced durability and modular designs are increasingly common to meet evolving customer demands. Additionally, competitive pricing and customization options are crucial factors influencing purchasing decisions. The fragmentation of the market has led to mergers and acquisitions aimed at consolidating capabilities and expanding geographical reach, intensifying competition in regions like North America, Europe, and Asia-Pacific.

TOMRA Systems ASA

SSI Shredding Systems, Inc.

Vecoplan AG

Steinert GmbH

Eldan Recycling A/S

ANDRITZ AG

Untha shredding technology GmbH

CP Group

Pellenc ST

Vecoplan LLC

The Recycling Equipment and Machinery Market has witnessed significant technological advancements aimed at enhancing efficiency, accuracy, and sustainability. One of the most impactful technologies is sensor-based sorting, which uses near-infrared (NIR) spectroscopy and X-ray fluorescence (XRF) to identify and separate various materials with high precision. For example, NIR sorting systems can distinguish different types of plastics, boosting recycling purity levels by up to 30%. Additionally, robotics integrated with artificial intelligence (AI) are increasingly employed for automated waste handling. These systems improve sorting speeds and reduce human error, allowing plants to process several tons of recyclable material per hour.

Energy efficiency is another critical focus area. New shredders and compactors utilize advanced motor technologies that lower energy consumption by 20% compared to previous models, contributing to reduced operational costs and carbon footprints. IoT (Internet of Things) integration is transforming recycling equipment by enabling real-time monitoring, predictive maintenance, and remote diagnostics. This reduces downtime and enhances machinery lifespan. Furthermore, chemical recycling technologies are progressing, enabling the breakdown of hard-to-recycle plastics into raw materials for reuse. Modular design trends also allow customization and scalability, meeting diverse recycling needs in municipal and industrial settings. These innovations collectively drive the recycling equipment market toward higher productivity and environmental compliance.

In August 2023, Vecoplan AG introduced the VIZ 1700 shredder, designed to process large plastic waste from the automotive industry. This high-throughput shredder boasts a 20% increase in productivity, significantly improving material handling efficiency in recycling operations.

In February 2024, TOMRA Systems ASA launched the Innosort Flake, an optical sorting system capable of simultaneously sorting plastic flakes by color, polymer type, and transparency. This innovation enhances the purity and quality of recycled plastic materials, facilitating their reuse in manufacturing processes.

In May 2024, ANDRITZ AG unveiled a next-generation wet recycling technology for paper and cardboard waste. This system increases fiber recovery rates by up to 15% while significantly reducing water usage during processing, contributing to more sustainable recycling practices.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

The Recycling Equipment and Machinery Market report provides a comprehensive overview of the global industry, encompassing key technologies, market segments, and regional dynamics. It covers various types of recycling equipment including shredders, balers, compactors, and sorting machines, highlighting their applications across industries such as plastics, metals, paper, and e-waste recycling. The report also analyzes the growing demand from end-users like municipal waste management, industrial sectors, and commercial establishments, reflecting increasing environmental regulations and sustainability initiatives worldwide.

This market report offers detailed insights into technological advancements such as automation, AI-enabled sorting, and energy-efficient machinery, which are transforming recycling processes by improving material recovery rates and reducing operational costs. It further examines emerging trends like the rise of modular and prefabricated equipment designs that enhance flexibility and reduce installation time. Geographical segmentation highlights the market’s expansion in North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, each driven by unique regulatory frameworks and economic activities.

Moreover, the report outlines challenges such as high initial investment costs and the need for skilled labor, balanced by opportunities stemming from increasing waste generation and circular economy practices. Overall, this report serves as an essential resource for manufacturers, investors, policymakers, and other stakeholders aiming to understand the current landscape and future prospects of the recycling equipment and machinery market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 810.7 Million |

|

Market Revenue in 2032 |

USD 1,031.43 Million |

|

CAGR (2025 - 2032) |

3.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

TOMRA Systems ASA, SSI Shredding Systems, Inc., Vecoplan AG, Steinert GmbH, Eldan Recycling A/S, ANDRITZ AG, Untha shredding technology GmbH, CP Group, Pellenc ST, Vecoplan LLC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |