Reports

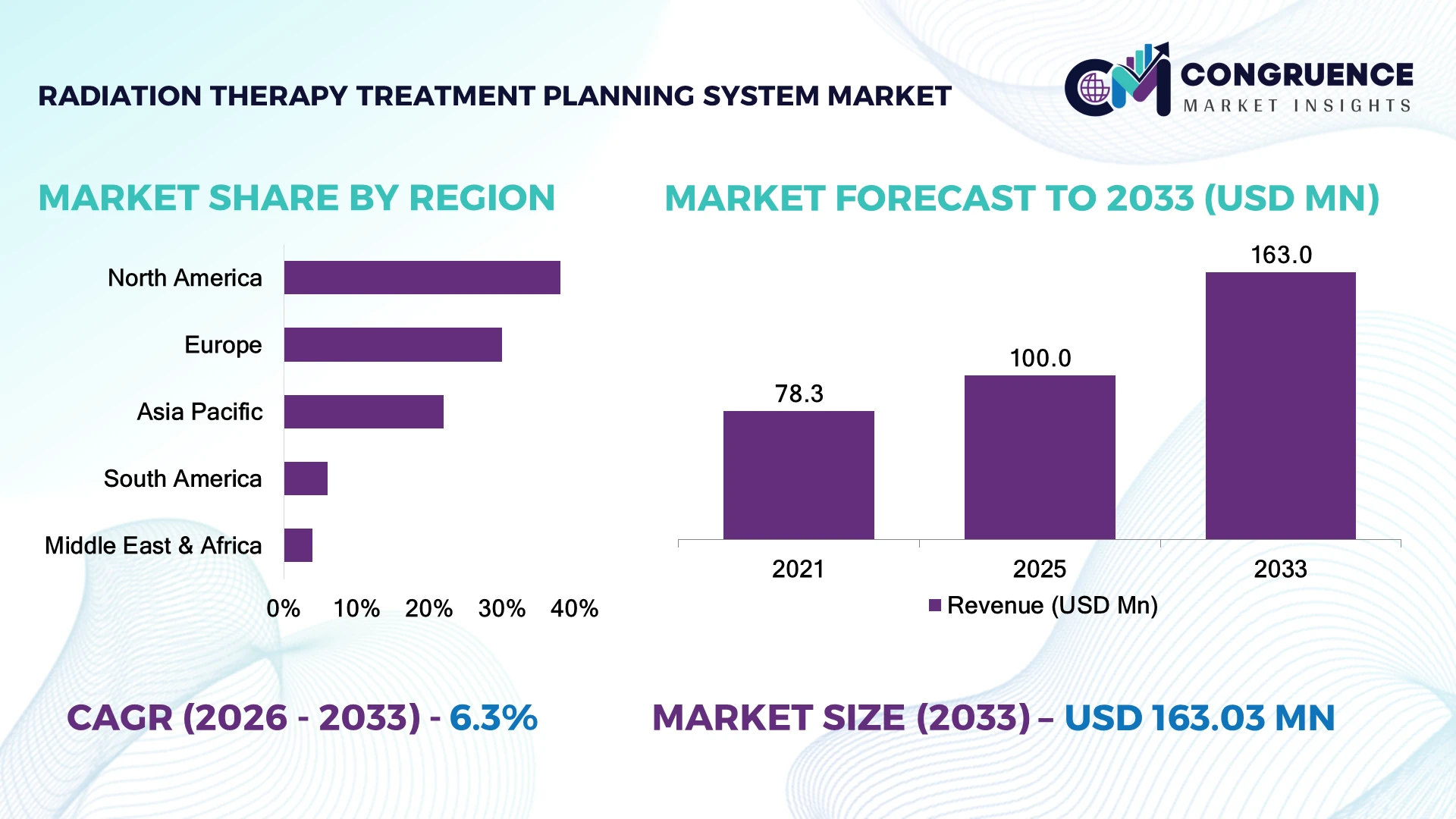

The Global Radiation Therapy Treatment Planning System Market was valued at USD 100.0 Million in 2025 and is anticipated to reach a value of USD 163.0 Million by 2033 expanding at a CAGR of 6.3% between 2026 and 2033. Growth is driven by AI-enabled treatment optimization, integration of image-guided radiotherapy platforms, and rising adoption of precision oncology workflows across cancer care facilities.

The United States dominates the market with approximately 35% share, supported by advanced oncology infrastructure, over 60% adoption of digital treatment planning workflows in leading cancer centers, and strong investments in AI-based radiotherapy systems. China is expanding rapidly with more than 20% regional deployment growth driven by hospital modernization programs. Compared with India, where adoption remains concentrated in metropolitan cancer institutes, the U.S. maintains a wider installed base and higher automation penetration.

Strategic investments in intelligent planning platforms will determine long-term competitive positioning.

Market Size & Growth: Valued at USD 100.0 Million in 2025 and projected at USD 163.0 Million by 2033, supported by AI-driven precision treatment workflows and advanced oncology infrastructure.

Top Growth Drivers: AI integration contributes to over 40% of technology adoption momentum, image-guided radiotherapy supports nearly 35% of deployments, and hospital digitization influences more than 30% of procurement decisions.

Short-Term Forecast: By 2028, automation-enabled planning systems reduce treatment preparation time by approximately 25% and improve workflow efficiency across oncology departments.

Emerging Technologies: AI-based contouring, cloud-enabled treatment planning, and adaptive radiotherapy platforms are reshaping advanced radiation oncology operations.

Regional Leaders: North America reaches approximately USD 57 Million, Europe USD 45 Million, and Asia-Pacific USD 38 Million by 2033, with AI adoption accelerating across major cancer centers.

Consumer/End-User Trends: More than 50% of large hospitals prioritize integrated treatment planning solutions to improve multidisciplinary oncology coordination.

Pilot/Case Example: In 2024, AI-assisted radiotherapy planning implementations achieved up to 30% reduction in manual contouring workload in clinical environments.

Competitive Landscape: Leading companies hold significant market influence, with major players including Elekta, Varian Medical Systems, Philips, RaySearch Laboratories, and Accuray.

Regulatory & ESG Impact: Digital radiotherapy standards and efficiency-focused healthcare policies improve resource utilization by reducing repeat planning procedures by nearly 15%.

Investment & Funding: More than USD 500 Million has been directed toward oncology software innovation, partnerships, and AI-based healthcare technology expansion.

Innovation & Future Outlook: Next-generation systems focus on real-time adaptive planning, automated decision support, and connected oncology ecosystems to strengthen global treatment capabilities.

Radiation Therapy Treatment Planning System solutions are becoming essential across oncology networks due to increasing cancer treatment complexity, demand for personalized radiation doses, and integration of advanced imaging technologies. Approximately 45% of new radiotherapy installations prioritize software-driven planning capabilities, while healthcare providers are upgrading systems to comply with evolving clinical standards and operational efficiency requirements. Global supply chain adjustments for medical software and imaging components are encouraging regional partnerships and localized technology deployment, creating new opportunities for advanced treatment planning platforms.

The Radiation Therapy Treatment Planning System Market is becoming strategically important as healthcare providers shift toward precision oncology, automated workflows, and integrated digital treatment ecosystems. Hospitals are prioritizing systems that improve clinical accuracy, reduce planning complexity, and support personalized cancer care delivery. Recent healthcare infrastructure modernization initiatives across emerging economies are accelerating investments in advanced radiotherapy capabilities.

Modern AI-assisted planning platforms improve treatment preparation efficiency by reducing manual contouring and optimization workloads by nearly 30% compared with conventional planning methods. North America continues to lead through established oncology networks and technology adoption, while Asia-Pacific is expanding through hospital upgrades and government-supported cancer care programs.

Radiation centers are increasingly adopting cloud-connected platforms, automated quality assurance tools, and adaptive planning technologies to manage rising patient volumes. For example, large oncology hospitals implementing AI-supported planning workflows are improving treatment turnaround times while maintaining clinical accuracy. Companies are strengthening market positions through software partnerships, regional expansion, and integration with imaging and radiotherapy equipment providers.

The next phase of competition will depend on technological differentiation, deployment flexibility, and the ability to deliver scalable precision treatment solutions across global healthcare systems.

The rapid integration of artificial intelligence and image-guided radiotherapy is accelerating demand for advanced treatment planning systems, with AI-assisted workflows reducing manual contouring workloads by nearly 30% and improving planning consistency by over 20% in oncology settings. The United States and Germany are expanding investments in automated radiotherapy infrastructure as cancer centers modernize clinical operations. Growing adoption of adaptive planning platforms is pushing companies to increase R&D spending, establish software partnerships, and integrate machine learning capabilities into existing solutions. The strategic advantage lies in reducing treatment preparation time while enabling hospitals to manage rising patient volumes with fewer operational bottlenecks.

High acquisition costs, complex system integration, and dependency on specialized infrastructure remain key barriers for widespread deployment of radiation therapy treatment planning systems. Advanced platforms require significant investment in compatible imaging equipment, trained specialists, and cybersecurity frameworks, with implementation expenses often increasing total project costs by 20–40%. Countries such as India and Brazil face scalability limitations due to uneven access to advanced oncology facilities and trained radiotherapy professionals. Interoperability challenges between planning software and legacy hospital systems affect deployment efficiency. Companies are addressing these constraints through modular platforms, cloud-based solutions, localized support networks, and long-term service agreements to improve affordability and operational flexibility.

The expansion of cloud-enabled treatment planning and automated oncology workflows creates new opportunities for healthcare providers seeking scalable digital infrastructure. Cloud-based platforms can reduce IT maintenance requirements by approximately 25% while enabling centralized planning across multiple facilities. Japan, South Korea, and China are investing in smart healthcare ecosystems that support remote collaboration and advanced radiotherapy management. AI-driven automation, including auto-segmentation and adaptive treatment optimization, is becoming a key innovation area, with more than 50% of new oncology software upgrades prioritizing intelligent workflow features. Companies are strengthening their positions through strategic collaborations, software innovation, and ecosystem partnerships focused on connected cancer care delivery.

The market faces execution challenges related to integrating advanced planning systems into diverse clinical environments, maintaining cybersecurity standards, and addressing skilled workforce shortages. Approximately 35% of oncology facilities in developing healthcare markets experience limitations in adopting highly automated radiotherapy technologies due to infrastructure and training gaps. Increasing regulatory requirements for AI validation and clinical accuracy create additional operational pressure for technology providers. Countries including the United States and United Kingdom are emphasizing compliance-driven digital healthcare frameworks, requiring continuous software updates and quality monitoring. Companies must invest in workforce training, interoperability improvements, and secure platform architectures to maintain consistent deployment performance and long-term competitiveness.

AI Workflow Integration Growth Artificial intelligence-based treatment planning is becoming a core operational upgrade, with automated contouring and optimization tools reducing manual planning workload by around 30% and improving workflow efficiency by over 20%. Leading oncology centers in the United States are integrating AI-assisted platforms to handle increasing patient volumes and improve treatment consistency. Companies are responding through software partnerships, algorithm development, and integration of AI modules into existing radiotherapy ecosystems.

Cloud Oncology Deployment Expansion Cloud-enabled treatment planning platforms are gaining adoption as healthcare networks seek centralized oncology operations, with approximately 25% lower IT maintenance requirements and over 40% of enterprises prioritizing remote collaboration capabilities. Hospitals in Japan and Singapore are expanding digital cancer care infrastructure through connected planning systems. Vendors are scaling cloud partnerships and cybersecurity investments to support distributed treatment workflows.

Adaptive Radiotherapy Advancement Real-time adaptive planning is transforming radiation delivery processes, with advanced systems improving treatment adjustment speed by nearly 35% and supporting more personalized dose management. Cancer institutes in Germany and the United Kingdom are increasing adoption due to stricter clinical precision requirements. Companies are investing in automation, imaging integration, and next-generation planning software to strengthen clinical accuracy.

Interoperability Standardization Shift Healthcare providers are prioritizing integrated treatment ecosystems as interoperability challenges affect approximately 20% of technology deployment projects. Regulatory focus on digital health standards and cybersecurity compliance is accelerating demand for compatible platforms. Companies are improving system connectivity through open architecture, hospital partnerships, and modular upgrades, creating more flexible radiotherapy infrastructure.

Radiation therapy treatment planning software represents the leading segment, accounting for approximately 55% of market adoption due to its critical role in dose optimization, image integration, and workflow automation. Its dominance is supported by widespread installation across hospitals using intensity-modulated radiation therapy (IMRT) and image-guided radiation therapy (IGRT) systems. Three-dimensional treatment planning systems maintain a strong installed base with nearly 30% adoption, particularly in established oncology centers requiring reliable clinical workflows. AI-integrated treatment planning solutions are the fastest-growing type, driven by demand for automated contouring, adaptive planning, and precision oncology. Adoption of AI-enabled platforms is increasing as hospitals target 25–30% reductions in manual planning activities. Two-dimensional planning systems continue to decline due to limited customization, while emerging cloud-based solutions are gaining attention for scalable deployment. Companies are shifting investment toward intelligent software platforms, automation capabilities, and integrated oncology ecosystems.

External beam radiation therapy is the leading application segment, representing approximately 70% of treatment planning system usage due to its broad clinical application across cancer types and compatibility with advanced planning technologies. Demand remains concentrated in hospitals managing high patient volumes, where planning accuracy and workflow speed directly influence treatment capacity. Intensity-modulated radiation therapy applications account for nearly 45% of advanced planning deployments, supported by increasing adoption of personalized dose delivery. Stereotactic radiosurgery and stereotactic body radiation therapy are among the fastest-growing applications, expanding as oncology providers adopt highly precise treatment approaches. These applications are gaining traction with more than 20% annual procedure volume growth in advanced cancer centers. Brachytherapy and other specialized applications maintain strategic importance for targeted treatments. Companies are enhancing product portfolios through adaptive planning tools, imaging integration, and workflow automation to address expanding precision oncology requirements.

Hospitals and oncology centers represent the leading end-user segment, accounting for approximately 65% of treatment planning system demand due to their large patient volumes, advanced radiotherapy infrastructure, and multidisciplinary cancer care programs. Large healthcare networks prioritize integrated planning platforms that connect imaging, treatment delivery, and clinical decision workflows. Specialty cancer institutes contribute nearly 25% of deployments as they expand precision treatment capabilities and adopt advanced automation technologies. Ambulatory cancer centers are the fastest-growing end-user group, driven by increasing outpatient oncology services and decentralized treatment models. Adoption in these facilities is rising as compact, cloud-enabled solutions improve accessibility and reduce infrastructure requirements. Research institutions and academic centers continue supporting innovation through clinical trials and technology validation. Companies are targeting these segments through flexible licensing models, service partnerships, and customized solutions designed for different facility sizes and operational needs.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America held approximately 38% of the global Radiation Therapy Treatment Planning System Market in 2025, supported by advanced oncology infrastructure, high adoption of image-guided radiotherapy, and strong integration of AI-based planning solutions. The United States contributes nearly 85% of the regional market due to its extensive network of cancer centers and advanced radiation oncology facilities. More than 70% of major oncology hospitals in the country use digital treatment planning platforms integrated with advanced imaging systems. Healthcare providers are increasing investments in automated planning, cloud connectivity, and precision oncology partnerships to improve treatment efficiency and clinical consistency.

United States Market Outlook: The United States remains the primary growth engine, supported by large-scale cancer care infrastructure, technology leadership, and strong vendor presence. Over 1,500 radiation therapy facilities operate nationwide, creating significant demand for advanced planning platforms. Hospitals are prioritizing AI-assisted treatment optimization and integrated oncology software solutions to improve workflow capacity and patient-specific treatment accuracy.

Europe accounted for approximately 30% of the global Radiation Therapy Treatment Planning System Market in 2025, driven by established healthcare systems, advanced radiotherapy adoption, and strong regulatory emphasis on treatment accuracy. Germany, the United Kingdom, and France represent the largest deployment markets, supported by modern oncology facilities and government-backed cancer care programs. More than 60% of leading European cancer centers have adopted advanced treatment planning workflows incorporating automation and imaging integration. Increasing focus on healthcare digitization and standardized oncology protocols is encouraging hospitals to upgrade legacy planning systems. Companies are expanding through partnerships with hospitals and technology providers to improve interoperability and clinical workflow efficiency.

Germany Market Outlook: Germany leads Europe through advanced medical infrastructure, strong engineering capabilities, and high adoption of precision radiotherapy technologies. The country accounts for nearly 30% of Europe’s treatment planning system demand, supported by more than 1,000 radiotherapy centers. Healthcare providers are investing in automated planning platforms and integrated oncology networks to enhance treatment quality and operational performance.

Asia-Pacific represented approximately 22% of the global Radiation Therapy Treatment Planning System Market in 2025 and is the fastest-expanding market due to rising cancer incidence, healthcare modernization, and increasing investment in radiotherapy infrastructure. China, Japan, South Korea, and India account for the majority of regional deployments. China contributes nearly 45% of Asia-Pacific demand, supported by large-scale hospital upgrades and expansion of cancer treatment facilities. Over 50% of newly installed radiotherapy systems in major Chinese hospitals incorporate advanced planning capabilities. Companies are increasing regional partnerships, localized software support, and manufacturing collaborations to improve accessibility and deployment speed.

China Market Outlook: China dominates the Asia-Pacific market with expanding oncology infrastructure, domestic healthcare technology development, and government-supported cancer treatment initiatives. The country has more than 3,000 radiotherapy facilities, creating significant demand for advanced planning systems. Local and international companies are focusing on AI-enabled platforms and integrated treatment solutions to support large patient populations.

South America accounted for approximately 6% of the global Radiation Therapy Treatment Planning System Market in 2025, with demand concentrated in Brazil, Argentina, and Chile. The market is shaped by modernization of oncology facilities, increasing private healthcare investment, and efforts to improve cancer treatment accessibility. Brazil represents nearly 50% of regional demand due to its larger healthcare infrastructure and concentration of specialized cancer centers. Approximately 35% of radiotherapy facilities in major South American economies are upgrading toward digital treatment planning systems. Companies are addressing infrastructure gaps through regional partnerships, service agreements, and cost-efficient software solutions to expand adoption.

Brazil Market Outlook: Brazil remains the largest South American market due to its extensive healthcare network and growing oncology treatment capacity. The country operates more than 250 radiotherapy facilities, creating demand for modern planning technologies. Healthcare providers are increasingly adopting integrated treatment platforms to improve efficiency and expand access to advanced cancer care services.

Middle East & Africa accounted for approximately 4% of the global Radiation Therapy Treatment Planning System Market in 2025, supported by healthcare modernization programs, private hospital expansion, and government investments in cancer treatment infrastructure. Countries including Saudi Arabia, the United Arab Emirates, and South Africa represent the majority of regional adoption. Saudi Arabia contributes nearly 35% of regional demand due to large-scale healthcare transformation initiatives and oncology infrastructure development. More than 40% of major cancer hospitals in Gulf countries are integrating advanced digital treatment planning workflows. Companies are strengthening regional presence through technology partnerships, localized support services, and infrastructure-focused collaborations.

Saudi Arabia Market Outlook: Saudi Arabia is the leading Middle Eastern market due to healthcare investment programs, advanced hospital development, and increasing focus on oncology services. The country is expanding specialized cancer centers under national healthcare transformation initiatives, with more than 50 oncology facilities supporting demand for modern radiotherapy planning technologies. International vendors are targeting partnerships to improve technology deployment and clinical capabilities.

The Radiation Therapy Treatment Planning System Market is contested by global oncology technology leaders including Varian Medical Systems, Elekta, RaySearch Laboratories, Philips, and Accuray, competing with specialized software innovators and regional healthcare technology providers. The top five players collectively account for approximately 65% of the market, creating a concentrated structure led by OEM ecosystems and independent planning software specialists. Competition is driven by AI capabilities, interoperability, workflow automation, and customization, with advanced platforms improving planning efficiency by 20–30% and reducing manual workload by nearly 30%. Varian and Elekta compete through integrated hardware-software ecosystems, while RaySearch differentiates through vendor-neutral planning solutions. Companies are expanding through partnerships, AI investments, and software upgrades. The market is shifting toward adaptive radiotherapy and cloud-enabled platforms, while high clinical validation requirements and integration complexity remain key entry barriers. Winning requires superior automation, clinical reliability, and flexible deployment models.

Elekta AB

RaySearch Laboratories

Koninklijke Philips N.V.

Accuray Incorporated

IBA (Ion Beam Applications)

MIM Software Inc.

Brainlab AG

Siemens Healthineers

Canon Medical Systems Corporation

ViewRay Technologies

Prowess Inc.

Artificial intelligence and machine learning are transforming treatment planning by automating segmentation, optimization, and quality checks. AI-assisted platforms reduce manual planning workload by approximately 30% and improve workflow consistency by more than 20% compared with conventional approaches. Leading vendors are integrating deep-learning models into planning software to support adaptive radiotherapy, faster clinical decisions, and personalized treatment strategies.

Cloud-based oncology platforms and interoperable treatment ecosystems are gaining adoption as hospitals seek scalable infrastructure and centralized workflows. Cloud deployment can lower IT maintenance requirements by nearly 25% while enabling multi-site collaboration. Compared with legacy standalone systems, modern connected platforms improve data exchange efficiency by over 35%, benefiting large healthcare networks and enterprise oncology groups.

Adaptive radiotherapy, automated planning algorithms, and real-time imaging integration represent the next technology shift for 2026–2028. Companies investing in AI validation, cybersecurity, and cross-platform compatibility are positioned to gain competitive advantage. Vendors with flexible software architectures will benefit as hospitals move from equipment-focused purchasing toward intelligent treatment management ecosystems.

May 2025 RaySearch Laboratories launched RayStation v2025 with automated treatment planning using machine learning and the ECHO algorithm, adding 201 deep-learning segmentation models. The update strengthens workflow automation and improves planning consistency for oncology centers adopting advanced radiotherapy solutions. Source: www.raysearchlabs.com

July 2025 RaySearch Laboratories and Radiology Oncology Systems announced a strategic partnership combining refurbished linear accelerators with advanced planning software. The collaboration supported deployment agreements across Argentina, Mexico, and the United States, improving access to cost-efficient radiotherapy infrastructure. Source: www.raysearchlabs.com

September 2025 GE HealthCare introduced updates to its Intelligent Radiation Therapy workflow solution, integrating RayStation connectivity to reduce simulation-to-treatment planning time from seven days to seven minutes for early adopters. The advancement improves oncology workflow speed and operational efficiency. Source: www.gehealthcare.com

February 2026 RaySearch Laboratories announced that The Royal Marsden NHS Foundation Trust completed online adaptive treatment using RayStation with an Elekta linear accelerator. The deployment expanded adaptive radiotherapy access using conventional equipment rather than specialized machines.

The Radiation Therapy Treatment Planning System Market Report covers detailed analysis across major system types, including advanced treatment planning software, AI-enabled platforms, and adaptive planning solutions. The report evaluates applications such as external beam radiotherapy, stereotactic treatments, and specialized oncology procedures, along with end-users including hospitals, cancer centers, research institutions, and ambulatory facilities. Regional assessment includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level deployment insights.

The study examines technology trends, competitive positioning, adoption patterns, interoperability developments, and emerging opportunities across the radiation oncology ecosystem. Covering more than 10 leading industry participants, the report supports strategic decisions related to investment planning, partnerships, product expansion, digital transformation, and long-term competitive positioning between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 100.0 Million |

| Market Revenue (2033) | USD 163.0 Million |

| CAGR (2026–2033) | 6.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Varian Medical Systems; Elekta AB; RaySearch Laboratories; Koninklijke Philips N.V.; Accuray Incorporated; IBA (Ion Beam Applications); MIM Software Inc.; Brainlab AG; Siemens Healthineers; Canon Medical Systems Corporation; ViewRay Technologies; Prowess Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |