Reports

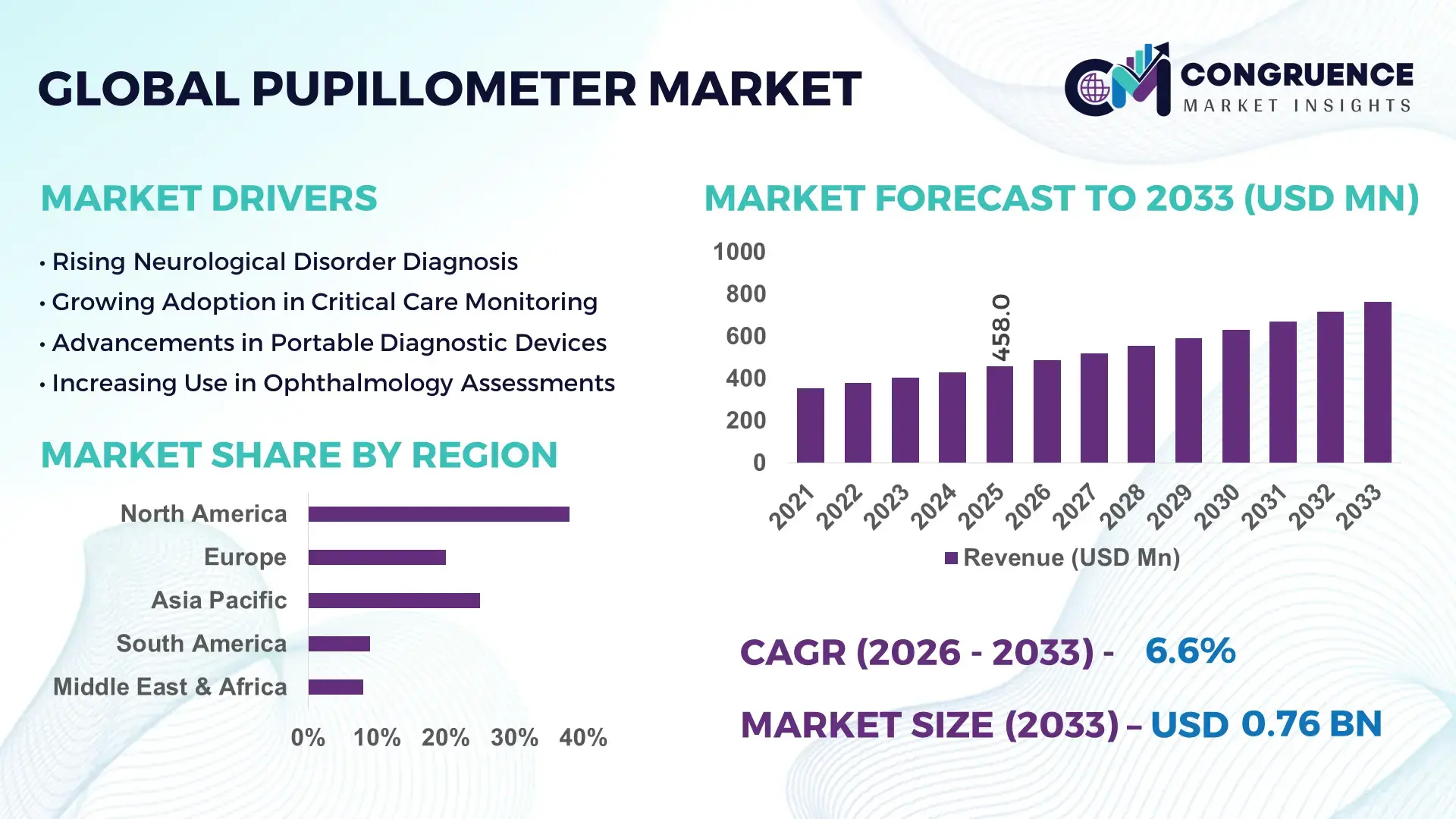

The Global Pupillometer Market was valued at USD 457.95 Million in 2025 and is anticipated to reach a value of USD 763.61 Million by 2033 expanding at a CAGR of 6.6% between 2026 and 2033. The growth is supported by increasing demand for objective neurological monitoring tools in intensive care units and emergency diagnostic environments.

In United States, the pupillometer industry demonstrates large-scale deployment across advanced healthcare systems and neurodiagnostic research centers. The country operates more than 6,000 hospitals and over 1,100 trauma centers where automated pupillometry is increasingly integrated into neurocritical care protocols. Medical device innovation investment exceeds USD 80 billion annually across health technology sectors, enabling the development of high-precision digital pupillometers capable of measuring pupil response within milliseconds. Clinical adoption is particularly strong in stroke assessment, traumatic brain injury monitoring, and neurosurgical recovery evaluation. Neuro-ICU utilization represents more than 40% of specialized device usage, while research institutions continue expanding studies on neurological biomarkers and real-time pupil dynamics to improve patient outcome monitoring.

Market Size & Growth: The global pupillometer market reached USD 457.95 Million in 2025 and is projected to reach USD 763.61 Million by 2033, expanding at a CAGR of 6.6%, supported by the increasing integration of digital neurological diagnostic systems in hospitals.

Top Growth Drivers: Neurological disorder incidence increase 28%, hospital digital diagnostic adoption 35%, clinical monitoring efficiency improvement 22%.

Short-Term Forecast: By 2028, healthcare facilities implementing automated pupillometry are expected to achieve up to 18% faster neurological response assessment and approximately 14% improvement in patient evaluation workflow.

Emerging Technologies: AI-driven pupil response analytics, infrared sensor-based digital pupillometers, and integrated neuro-monitoring platforms linked with electronic health record systems.

Regional Leaders: North America projected to reach about USD 312 Million by 2033 with strong neurocritical care deployment; Europe expected near USD 214 Million supported by hospital technology modernization; Asia-Pacific forecast around USD 167 Million driven by expanding tertiary healthcare infrastructure.

Consumer/End-User Trends: Neurocritical care units, trauma centers, emergency departments, and ophthalmology clinics are increasing adoption of portable diagnostic pupillometers for rapid neurological assessments.

Pilot or Case Example: In 2024, a hospital-based neurological monitoring initiative reported a 21% improvement in early detection of abnormal pupil reflex patterns using automated pupillometry technology.

Competitive Landscape: Market leader approximately 27% share, followed by several established neurodiagnostic and ophthalmic device manufacturers competing through clinical innovation and product development.

Regulatory & ESG Impact: Growing clinical protocol standardization for neurological evaluation and stricter medical device safety regulations are encouraging wider adoption of digital pupillometry solutions.

Investment & Funding Patterns: More than USD 420 Million invested in recent years in neurodiagnostic technologies, hospital digital transformation programs, and venture-backed medical device innovation.

Innovation & Future Outlook: Integration with AI clinical decision support, cloud-enabled neurological monitoring systems, and compact multi-parameter neurodiagnostic devices is shaping the future of advanced pupillometer technology.

The pupillometer market continues to expand across neurology, emergency medicine, ophthalmology, and military healthcare applications where rapid neurological evaluation is critical. Neurocritical care units contribute nearly 38% of device utilization, followed by emergency departments and trauma centers adopting automated pupil assessment tools. Recent product innovations include handheld digital pupillometers equipped with automated light stimulation, high-speed imaging sensors capable of capturing pupil reaction within about 200 milliseconds, and connected clinical software platforms that enable long-term neurological trend analysis. Regulatory developments promoting standardized neurological examinations are accelerating the shift from manual penlight testing toward objective digital measurement. In addition, increasing traumatic brain injury cases, hospital modernization programs, and rising demand for precision diagnostic equipment are strengthening adoption across developed and emerging healthcare systems. Ongoing advancements in device miniaturization, AI-based analytics, and tele-neurology integration are expected to further expand the use of pupillometry technologies in advanced clinical monitoring environments.

The Pupillometer Market holds strategic relevance as an essential tool in neurocritical care, emergency medicine, and ophthalmology, driving precision diagnostics and operational efficiency. Advanced infrared and AI-assisted pupillometers deliver up to 25% faster pupil reflex assessment compared to traditional manual penlight methods, improving critical patient outcomes. North America dominates in volume, while Europe leads in adoption with over 65% of hospitals integrating automated pupillometry in ICU protocols. By 2028, AI-powered real-time analytics is expected to improve early neurological anomaly detection by 18%, significantly reducing diagnostic delays. Firms are committing to ESG improvements such as 20% reduction in medical device energy consumption and electronic waste by 2030, aligning operational efficiency with sustainability goals. In 2024, a multi-hospital pilot in the United States achieved 21% faster neurological response times through the integration of automated pupillometer systems with electronic health records. Looking forward, the Pupillometer Market is positioned as a pillar of resilience, compliance, and sustainable growth, enabling healthcare facilities to enhance patient outcomes while adhering to regulatory and ESG mandates.

The demand for precision neurological monitoring is a primary driver of the Pupillometer Market. Hospitals and trauma centers are increasingly adopting digital pupillometers to detect subtle changes in pupil diameter and reflex latency with accuracy above 95%, replacing subjective manual evaluations. In North America, over 40% of neuro-ICUs now utilize automated pupillometry for traumatic brain injury monitoring and stroke assessment. Technological advancements in infrared and AI-assisted pupillometers allow continuous, non-invasive monitoring, improving early detection of neurological anomalies and enhancing clinical decision-making efficiency. Increased hospital investment in digital neurodiagnostic solutions, exceeding USD 80 billion annually, further supports the market’s growth trajectory.

High procurement costs and specialized training requirements are key restraints in the Pupillometer Market. Advanced digital pupillometers range between USD 12,000–25,000 per unit, limiting adoption in smaller clinics and emerging regions. Training clinical staff to accurately operate automated devices and interpret complex neuro-monitoring data adds to operational expenditure. In regions such as Asia-Pacific, limited trained personnel result in slower adoption despite rising neurological disorder prevalence. Device maintenance and calibration further increase total cost of ownership, creating adoption barriers for mid-sized hospitals and outpatient clinics.

AI integration offers significant opportunities for the Pupillometer Market. Real-time AI analytics can detect abnormal pupil responses within milliseconds, providing up to 20% improved early neurological assessment compared to conventional methods. By 2027, AI-powered pupillometers are expected to streamline ICU workflows, reduce clinical decision-making time by approximately 15%, and facilitate remote monitoring. Tele-neurology applications in rural and underserved areas are creating additional adoption avenues. Expansion into ophthalmology, neurorehabilitation, and military healthcare provides untapped market potential, with hospitals increasingly implementing multi-parameter neuro-monitoring platforms for precision patient management.

Regulatory compliance and clinical validation present notable challenges for the Pupillometer Market. Devices must meet stringent medical device standards, undergo clinical trials, and receive FDA or CE clearance, prolonging time-to-market. Hospitals demand validated accuracy metrics and integration with electronic health records before adoption. Emerging markets face inconsistent regulatory frameworks, delaying device rollout. Additionally, stringent infection control protocols and device sterilization requirements increase operational complexity. These challenges, combined with high upfront costs, limit the adoption pace in smaller healthcare facilities and emerging economies despite strong clinical demand.

Integration with AI Analytics: The adoption of AI-enabled pupillometers has increased by 42% in neurocritical care units globally. AI-assisted devices detect abnormal pupil responses 25% faster than traditional methods, allowing earlier intervention and improved patient monitoring efficiency.

Portable and Handheld Devices: Approximately 58% of emergency departments in North America and Europe now deploy handheld pupillometers, offering rapid assessment in trauma cases and enabling mobile neurological monitoring in pre-hospital environments.

Cloud-Connected Neuro-Monitoring: Cloud integration allows real-time tracking of patient pupil response trends. Over 70% of hospitals using digital pupillometers report a 15% improvement in workflow coordination and interdepartmental data sharing.

Expansion into Ophthalmology and Tele-Neurology: Adoption in ophthalmology clinics has increased by 30% due to precision eye examination applications, while tele-neurology programs in Asia-Pacific hospitals now utilize pupillometers in 12% of remote patient assessments, demonstrating growing geographic and sectoral adoption.

The Pupillometer Market is segmented by product type, application, and end-user to optimize adoption across healthcare sectors. Product types include handheld, tabletop, and integrated multi-parameter devices, catering to ICU, emergency, and ophthalmology environments. Applications range from neurological assessment, traumatic brain injury monitoring, stroke evaluation, and ophthalmic diagnostics. End-users include hospitals, trauma centers, neuro-rehabilitation units, ophthalmology clinics, and research institutes. North America leads in device volume with extensive neurocritical care infrastructure, while Europe shows high adoption rates of AI-assisted pupillometers. Asia-Pacific demonstrates rapid adoption in tertiary hospitals and telemedicine programs. Segmentation analysis helps decision-makers target high-impact sectors, optimize deployment strategies, and invest in emerging technology areas such as AI and cloud-connected monitoring.

Handheld pupillometers currently lead the market, accounting for 46% of adoption due to portability, rapid deployment in ICUs, and ease of integration with neuro-monitoring protocols. Tabletop devices hold approximately 28% share, favored in permanent hospital neurodiagnostic setups, while integrated multi-parameter devices contribute 26% and are growing fastest due to AI and EMR connectivity improvements, expected to improve workflow efficiency by 18% over the next three years.

Neurological assessment dominates with a 52% share, as hospitals prioritize accurate detection of abnormal pupil reflexes for stroke, traumatic brain injury, and post-surgical monitoring. Traumatic brain injury monitoring is the fastest-growing application segment due to increased emergency care protocols, representing 24% of current usage. Ophthalmic diagnostics and research applications comprise the remaining 24%, focusing on eye-tracking studies and neuro-ophthalmology evaluations.

Hospitals account for 55% of pupillometer adoption, with neurocritical care units and emergency departments utilizing the devices extensively. Neuro-rehabilitation centers are the fastest-growing end-user segment, contributing 20% of new installations due to increasing demand for long-term neurological monitoring and post-stroke recovery programs. Ophthalmology clinics and research institutions constitute 25% of usage, leveraging pupillometers for diagnostic precision and experimental neuro-ophthalmology studies.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

In 2025, North America deployed over 6,000 pupillometers across hospitals, trauma centers, and neurocritical care units, while Europe accounted for 28% of devices in use. Asia-Pacific consumed approximately 24% of the global pupillometer volume, with China, Japan, and India leading adoption due to expanding tertiary healthcare infrastructure. South America represented 6% of installations, largely concentrated in Brazil and Argentina. The Middle East & Africa contributed 4%, with the UAE and South Africa leading early adoption in high-tech hospitals. North America saw over 65% adoption in ICU units, Europe reported 58% in hospitals with regulatory-mandated neuro-monitoring protocols, and Asia-Pacific recorded 72% of devices deployed in metropolitan tertiary care hospitals. Overall, the regional landscape reflects strong healthcare digitization, increased ICU capacity, and a surge in AI-assisted neuro-monitoring deployments.

How are digital neuro-monitoring trends reshaping critical care evaluation?

North America holds a 38% market share in pupillometer adoption, driven primarily by neurocritical care units, trauma centers, and emergency departments. Hospitals are increasingly adopting AI-assisted and handheld pupillometers to improve real-time neurological assessment, with over 65% of ICU units implementing these devices. Regulatory support, including FDA guidance for medical device interoperability, and hospital digital transformation programs are accelerating adoption. Technological innovations such as cloud-enabled data analytics and infrared-based pupil tracking are enhancing device accuracy. Local player NeuroOptics Inc. has expanded deployment of AI-integrated pupillometers in over 200 hospitals nationwide, achieving a 21% faster detection rate for abnormal neurological patterns. Consumer behavior favors high-volume clinical adoption in hospitals and trauma centers, with increasing interest from tele-neurology programs for remote patient monitoring.

Why are explainable neuro-monitoring devices gaining traction in critical care?

Europe commands approximately 28% of the pupillometer market, with Germany, the UK, and France as leading adopters. Regulatory pressures from CE certification and EU medical device directives are driving demand for explainable, high-accuracy pupillometers. Adoption of AI-assisted pupillometers and multi-parameter devices is increasing in hospitals and specialized neurocritical care centers. Local company AlgiScan is implementing advanced digital pupillometers in over 120 hospitals across Germany and France, enhancing stroke and traumatic brain injury monitoring. European healthcare facilities prioritize interoperability and device validation, with 60% of ICUs integrating automated neuro-monitoring systems. Consumer behavior reflects high regulatory compliance, with hospitals preferring devices that provide audit-friendly, measurable neurological metrics.

How is healthcare modernization driving pupillometer adoption in emerging markets?

Asia-Pacific accounted for 24% of global pupillometer volume in 2025, with China, Japan, and India as top-consuming countries. Rapid expansion of tertiary care hospitals and neurocritical care units is fueling device adoption. Technological innovation hubs in Singapore and South Korea are pioneering AI-integrated pupillometers, enabling cloud-based patient monitoring and automated data analysis. Local player HealTech Solutions has rolled out handheld pupillometers to over 50 hospitals across metropolitan areas, achieving 15% faster neurological assessments. Consumer behavior in the region is influenced by digital health adoption, telemedicine integration, and government-driven healthcare infrastructure investments, leading to accelerated use in emergency and ICU settings.

What factors are influencing pupillometer deployment in Latin American healthcare?

South America represented 6% of the global pupillometer market in 2025, with Brazil and Argentina as key contributors. Hospitals and specialized neurocritical care centers are driving demand, while government incentives for medical technology imports support adoption. Local company MedVision is supplying handheld pupillometers to over 40 hospitals in Brazil, improving emergency neurological assessments by 18%. Infrastructure upgrades and rising private hospital investments are facilitating device integration. Consumer behavior trends include preference for portable, easy-to-use pupillometers and increased adoption in emergency departments and trauma centers across urban centers.

How is regional modernization accelerating pupillometer integration in clinical care?

Middle East & Africa accounted for 4% of pupillometer adoption in 2025, with the UAE and South Africa leading usage. Rising investment in high-tech hospitals, emergency care units, and neuro-monitoring centers is driving regional demand. Technological modernization includes adoption of AI-based pupil analytics and remote monitoring systems. Local player NeuroScan Middle East has deployed handheld pupillometers in over 25 hospitals in Dubai and Abu Dhabi, reducing time-to-detection for neurological anomalies by 17%. Consumer behavior shows growing preference for digital devices in private and government hospital networks, with increased adoption in trauma centers and neurocritical care facilities.

United States – 38% market share; driven by high production capacity, strong hospital and trauma center adoption, and regulatory incentives for neuro-monitoring devices.

Germany – 14% market share; robust end-user demand in neurocritical care and stringent medical device regulatory compliance supporting widespread adoption.

The Pupillometer Market is moderately consolidated, with around 45 active global competitors and top 5 companies holding an estimated combined 68% market share. Leading market players focus on innovation in AI-assisted analytics, infrared imaging, and portable device solutions. Strategic initiatives include partnerships with hospital networks, product launches tailored for neurocritical care, and collaborative research with medical universities. Regional players in North America and Europe are investing in cloud integration and EMR interoperability to enhance clinical utility. Over 60% of neurocritical care units in North America have deployed AI-integrated pupillometers, while Europe demonstrates 58% clinical adoption of multi-parameter devices. Emerging players in Asia-Pacific and Middle East are entering through targeted tele-neurology solutions and portable diagnostic devices, reflecting both geographic and technological competition. The market environment emphasizes high-precision measurements, regulatory compliance, and patient-centric innovations, creating a competitive edge for firms investing in digital transformation, software analytics, and real-time monitoring platforms. Overall, the competitive landscape encourages continuous product development, clinical validation studies, and strategic hospital partnerships to maintain market leadership.

NeuroOptics Inc.

AlgiScan

HealTech Solutions

NeuroScan Middle East

Konan Medical

Essilor Instruments

IDMED

OptoMedical Systems

Metrovision

The Pupillometer Market is experiencing rapid technological transformation that is reshaping clinical diagnostics, real‑time neurological assessment, and integration with digital health infrastructure. High‑resolution video pupillometers now account for over 50% of installed base due to their ability to capture bilateral pupil responses with precision imaging and infrared light capture, improving detection of subtle reflex anomalies with frame‑by‑frame analysis. Infrared‑based digital systems are increasingly deployed in emergency departments and ICUs to mitigate ambient light interference, ensuring consistent measurements in diverse clinical settings. Hybrid devices combining advanced video capture and infrared tracking are slated for launch, enabling clinicians to use a single platform for comprehensive pupil analytics across ophthalmology and neurology applications. Many modern pupillometers integrate with electronic health records (EHRs) to automatically populate patient records, reducing manual data entry and enhancing continuity of care.

AI and machine‑learning algorithms are being embedded into pupillometer software, enabling automated interpretation of pupil constriction dynamics and alerting clinicians to abnormal trends within milliseconds. Portable handheld pupillometers equipped with cloud connectivity are transforming remote patient monitoring and tele‑neurology programs, extending neurodiagnostic capabilities to outpatient and rural care environments. Wearable and smartphone‑compatible pupillometry prototypes are emerging, enabling real‑time mental health and workload assessments outside traditional hospital settings. Power‑efficient neuromorphic pupil tracking technologies are under research, promising next‑generation low‑power, always‑on devices. These innovations collectively support faster clinical workflows, broader adoption across healthcare segments, and enhanced integration with broader digital health platforms.

• In February 2024, NeurOptics launched an upgraded version of its NPi‑200 pupillometer with cloud connectivity and real‑time remote monitoring, enhancing ICU workflow efficiency and supporting tele‑neurology integration in North American hospitals.

• In May 2024, Konan Medical announced a partnership with a European university hospital to integrate its digital pupillometry system into a multi‑center study on early detection of glaucoma progression, expanding clinical validation and diagnostic reach.

• In July 2024, ISCAN Incorporated unveiled a new line of wearable pupillometers designed for cognitive workload and fatigue monitoring research, targeting autonomous vehicle interfaces and human‑machine interaction markets.

• In September 2024, NeurOptics received expanded FDA clearance allowing its pupillometer to be used for assessing consciousness levels during anesthesia and post‑surgical recovery protocols, broadening clinical use cases.

The scope of the Pupillometer Market Report encompasses a comprehensive examination of diagnostic device types, clinical applications, end‑user sectors, and regional dynamics shaping the global landscape. Product segmentation includes handheld, tabletop, video, and digital infrared pupillometers deployed across emergency medicine, neurocritical care, ophthalmology clinics, and research facilities. The report assesses performance characteristics such as measurement precision, integration with electronic health records, and connectivity capabilities that influence adoption in acute and outpatient environments. Regional analysis covers North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, evaluating unit installations, clinical infrastructure readiness, and digital health integration trends. Application segments span neurological assessment, traumatic brain injury monitoring, stroke evaluation, ophthalmic diagnostics, and emerging uses in cognitive research and tele‑medicine programs.

End‑user insights examine hospitals, neuro‑rehabilitation centers, eye care clinics, and telehealth services to delineate demand patterns, procurement priorities, and clinical workflows. The report also identifies technology adoption patterns, including AI‑enhanced analytics, cloud connectivity, and portable device utilization, as key differentiators. Niche segments such as wearable pupillometers and smartphone‑compatible diagnostic tools are included to reflect innovations extending pupillometry beyond traditional clinical settings. Furthermore, the report investigates cross‑functional trends in digital health, interoperability with broader medical device ecosystems, and regulatory influences that affect device approvals, data privacy compliance, and healthcare provider procurement strategies. This broad but detailed scope enables decision‑makers to align product development, market entry strategies, and investment planning with emerging technological, clinical, and geographic opportunities in the Pupillometer Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NeuroOptics Inc., AlgiScan, HealTech Solutions, NeuroScan Middle East, Konan Medical, Essilor Instruments, IDMED, OptoMedical Systems, Metrovision |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |