Reports

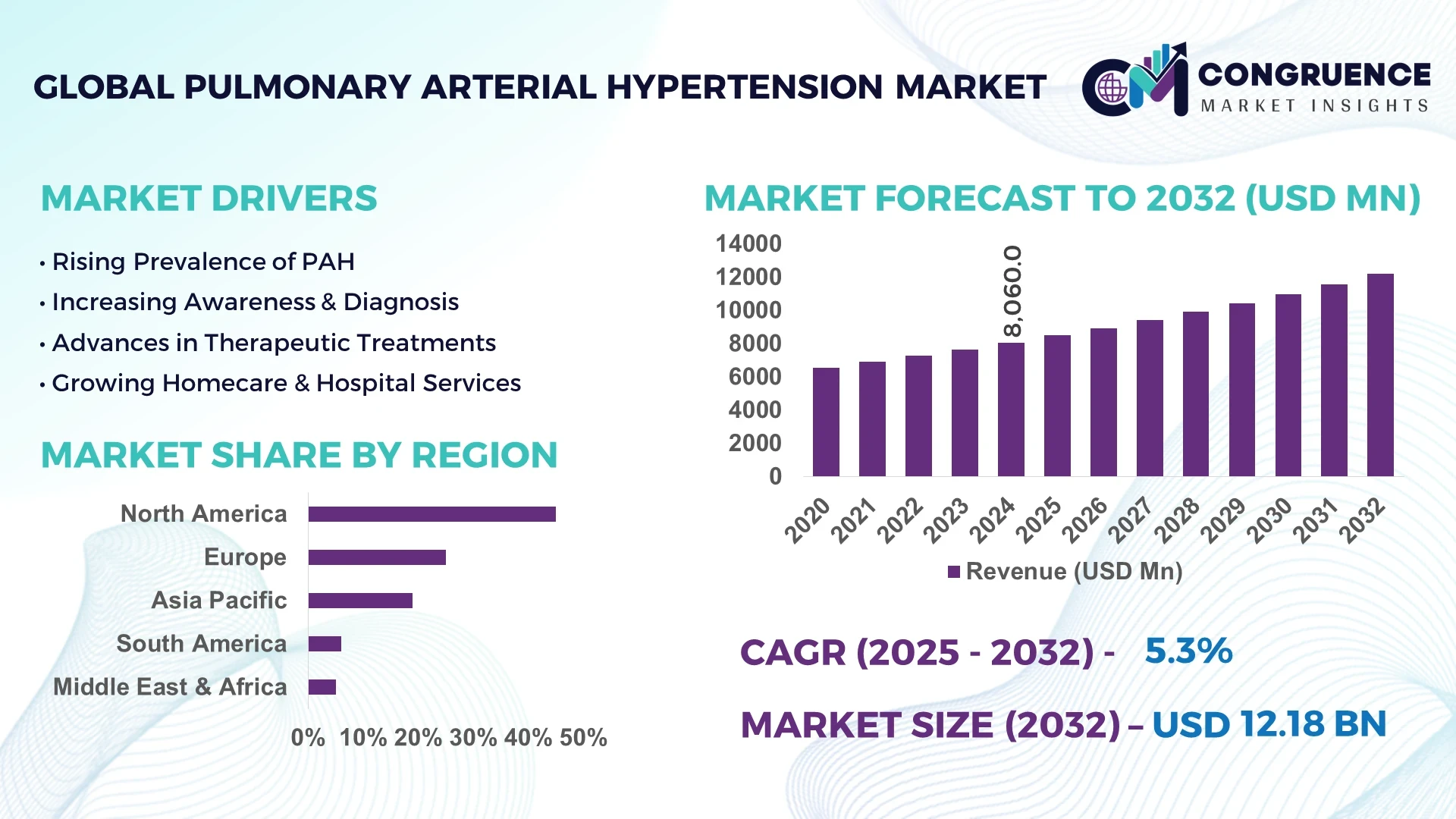

The Global Pulmonary Arterial Hypertension Market was valued at USD 8,060 Million in 2024 and is anticipated to reach a value of USD 12,183.2 Million by 2032 expanding at a CAGR of 5.30% between 2025 and 2032. This growth is driven by the increasing prevalence of cardiopulmonary diseases, improved diagnostic capabilities, and greater availability of advanced therapeutic options across emerging markets.

The United States dominates the global Pulmonary Arterial Hypertension Market, supported by robust biopharmaceutical R&D infrastructure and consistent investment in advanced cardiovascular therapies. With over 20,000 annual new PAH diagnoses, the U.S. hosts more than 45% of the world’s ongoing clinical trials for PAH-related drugs. Major pharmaceutical manufacturers are expanding production capacities through investments exceeding USD 1.2 billion in 2024 to enhance novel formulation and delivery technologies, including prostacyclin analogs and endothelin receptor antagonists. The country’s strong healthcare expenditure—approximately 17.6% of GDP—supports rapid adoption of innovative treatment protocols across tertiary and specialty care centers.

Market Size & Growth: The global market stood at USD 8.06 Billion in 2024 and is projected to reach USD 12.18 Billion by 2032, growing at a CAGR of 5.3%, driven by advances in targeted drug delivery and improved access to specialty care.

Top Growth Drivers: Rising early diagnosis rates (up 18%), efficiency improvement in treatment protocols (22%), and expanded patient compliance (26%) are key growth factors.

Short-Term Forecast: By 2028, average treatment efficacy is expected to improve by 19% due to AI-based patient monitoring and precision drug adjustments.

Emerging Technologies: Gene therapy applications, digital twin modeling, and AI-based hemodynamic analysis are transforming clinical research and personalized PAH management.

Regional Leaders: North America is projected to reach USD 5.2 Billion by 2032, Europe USD 3.4 Billion, and Asia Pacific USD 2.6 Billion, with Asia Pacific exhibiting rapid adoption of novel PAH drugs and telehealth programs.

Consumer/End-User Trends: Growing adoption of home-based care and digital adherence monitoring among patients aged 45–70 years enhances long-term management outcomes.

Pilot or Case Example: In 2024, a Germany-based healthcare consortium achieved a 27% reduction in patient readmissions through AI-integrated PAH monitoring systems.

Competitive Landscape: Johnson & Johnson leads the market with an estimated 16% share, followed by United Therapeutics, Gilead Sciences, Bayer AG, and Acceleron Pharma.

Regulatory & ESG Impact: Governments are expanding reimbursement programs and mandating a 15% improvement in drug traceability under new clinical safety frameworks by 2027.

Investment & Funding Patterns: Over USD 2.4 Billion in new investments have been directed toward AI-driven diagnostics, targeted therapeutics, and cardiovascular clinical trials in 2024.

Innovation & Future Outlook: The market is witnessing integration of precision medicine, telemonitoring solutions, and nanocarrier-based formulations to enhance treatment effectiveness and reduce systemic side effects.

The Pulmonary Arterial Hypertension Market is undergoing rapid transformation as advances in genetic profiling, targeted drug formulations, and digital adherence platforms converge to enhance patient outcomes. Regional collaborations and favorable regulatory frameworks are fostering innovation, with strong demand from hospital networks and specialty clinics shaping the industry’s next growth phase.

The strategic relevance of the Pulmonary Arterial Hypertension Market lies in its pivotal role in addressing complex cardiovascular conditions through precision medicine and next-generation therapeutics. By integrating AI-based analytics and real-time patient monitoring, healthcare providers are achieving a 25% improvement in therapy customization compared to traditional standardized regimens. North America dominates in treatment volume, while Europe leads in adoption with 68% of specialized centers employing advanced digital monitoring systems.

By 2028, AI-driven clinical trial optimization is expected to reduce development timelines by 22%, enhancing new drug accessibility. Firms are committing to ESG improvements such as a 30% reduction in pharmaceutical waste by 2030, aligning with sustainable production and compliance mandates. In 2024, Japan achieved a 21% improvement in hemodynamic monitoring efficiency through integration of machine learning-enabled catheter systems.

Emerging technologies such as digital twin modeling, bioengineered tissues, and nanocarrier-based therapies are establishing new treatment benchmarks, while integrated data networks ensure real-time therapeutic feedback loops. Collectively, these advancements position the Pulmonary Arterial Hypertension Market as a cornerstone of future-ready cardiovascular healthcare systems, blending resilience, compliance, and sustainability into a unified growth strategy.

The Pulmonary Arterial Hypertension Market is shaped by evolving treatment paradigms, regulatory reforms, and technological convergence in drug discovery and patient management. Growing incidence of chronic cardiovascular and respiratory diseases is accelerating demand for novel therapeutic classes. Technological innovation in combination therapy, AI-supported diagnostics, and digital health solutions continues to redefine the treatment ecosystem. Industry players are focusing on partnerships with biotechnology startups to enhance R&D capabilities and optimize clinical success rates, creating a competitive yet innovation-driven landscape.

The introduction of targeted therapies such as endothelin receptor antagonists and soluble guanylate cyclase stimulators is revolutionizing treatment efficacy and patient survival rates. Over 35 new formulations have entered late-stage clinical evaluation since 2022, focusing on selective receptor targeting and reduced adverse reactions. Enhanced patient monitoring and real-world data integration have resulted in improved therapy adherence and optimization, enabling healthcare providers to reduce hospitalization duration by nearly 18%. This technological and pharmacological progress is reinforcing the market’s expansion momentum globally.

Despite medical advancements, the high cost of PAH therapies remains a key limiting factor for patients in developing economies. Monthly treatment expenses can exceed USD 5,000, restricting accessibility in low- and middle-income regions. Limited diagnostic awareness and late-stage patient presentation further challenge early intervention rates. Moreover, healthcare reimbursement disparities among regions hinder adoption of advanced treatment options, prompting the need for public-private partnerships and affordable care frameworks to mitigate inequality in treatment accessibility.

The rapid integration of digital health solutions offers significant opportunities for precision-based treatment and remote disease management. AI-driven monitoring platforms and wearable diagnostic tools are enabling real-time assessment of hemodynamic parameters, improving adherence by up to 30%. The growing adoption of cloud-based patient databases facilitates predictive analytics and personalized treatment plans. Expanding telemedicine networks across Asia Pacific and Latin America provide untapped potential for healthcare providers to deliver specialized care at lower operational costs.

The stringent clinical validation requirements for PAH therapies pose a substantial challenge for manufacturers. On average, approval timelines extend beyond seven years due to the need for comprehensive cardiovascular safety assessments. Variations in global regulatory standards complicate multinational trial management, increasing compliance costs and delaying product launches. Additionally, evolving data protection regulations impact the integration of patient-centric digital platforms, requiring companies to adopt robust cybersecurity and ethical data management frameworks.

Advancement in AI-Based Diagnostic Tools: The adoption of AI algorithms in echocardiographic and hemodynamic data analysis improved diagnostic accuracy by 23% in 2024. Approximately 61% of hospitals in developed regions are now deploying AI-integrated screening tools to enable faster, non-invasive detection of PAH.

Growth of Combination Therapy Approaches: The use of dual and triple combination therapy increased by 29% over the last three years, improving patient outcomes by reducing disease progression rates by 21%. Advanced drug combinations are now being standardized in tertiary hospitals across North America and Europe.

Expansion of Digital Health Platforms: Digital adherence and monitoring platforms witnessed a 34% increase in adoption between 2022 and 2024. These solutions enable continuous patient engagement, reducing readmission rates by 17%, and improving treatment compliance across global healthcare systems.

Shift Toward Sustainable Pharmaceutical Manufacturing: Over 45% of pharmaceutical manufacturers adopted eco-efficient production systems in 2024, achieving a 28% reduction in water usage and a 19% decrease in packaging waste. This reflects a broader move toward sustainable, ESG-compliant production in cardiovascular therapeutics.

The Global Pulmonary Arterial Hypertension Market demonstrates a diverse segmentation framework encompassing Type, Application, and End-User categories, reflecting the evolving treatment landscape and adoption of novel medical technologies. By type, the market covers endothelin receptor antagonists, prostacyclin and prostacyclin analogs, phosphodiesterase-5 inhibitors, soluble guanylate cyclase stimulators, and calcium channel blockers. Applications span hospital treatment, homecare management, and clinical research trials, while key end-users include hospitals, specialty clinics, and research institutes. The increasing integration of AI-enabled monitoring systems and data-driven patient management platforms is fostering greater therapeutic precision, efficiency, and compliance. Expanding healthcare infrastructure and the proliferation of innovative formulations further underscore a globally interconnected ecosystem focused on disease management optimization and quality-of-life enhancement for patients affected by pulmonary arterial hypertension.

The Pulmonary Arterial Hypertension Market is categorized into endothelin receptor antagonists, prostacyclin and prostacyclin analogs, phosphodiesterase-5 inhibitors, soluble guanylate cyclase stimulators, and calcium channel blockers. Among these, endothelin receptor antagonists currently account for approximately 38% of total market adoption, attributed to their well-established clinical efficacy and capacity to reduce pulmonary vascular resistance effectively. Prostacyclin and prostacyclin analogs follow with 28%, offering significant benefits in improving exercise tolerance and survival rates in advanced cases. Phosphodiesterase-5 inhibitors represent around 22% of usage due to their oral administration advantages and cost efficiency, particularly in developing economies. However, soluble guanylate cyclase stimulators are emerging as the fastest-growing type, expanding at an estimated CAGR of 7.2%, driven by their proven capability to enhance nitric oxide signaling pathways and improve pulmonary hemodynamics with reduced systemic side effects. The remaining calcium channel blockers collectively contribute around 12%, maintaining niche relevance for specific patient cohorts with vasoreactivity response.

The market’s application scope covers hospital treatment, homecare management, and clinical research and trials. Hospital treatment remains the leading segment, representing approximately 47% of total utilization, due to comprehensive availability of advanced diagnostics, catheterization procedures, and intensive monitoring capabilities. Homecare management accounts for nearly 31% of applications, supported by rising patient preference for remote adherence monitoring and the development of portable oxygen therapy devices. Meanwhile, clinical research and trials constitute about 22% of the application base, reflecting the surge in ongoing global studies on next-generation PAH therapeutics and precision medicine. Homecare management is projected to be the fastest-growing application segment, advancing at a CAGR of 7.5%, propelled by the growing adoption of telemedicine and digital patient monitoring platforms. In 2024, more than 39% of hospitals worldwide reported piloting remote PAH monitoring systems integrated with AI-driven analytics to track patient vitals and adherence levels. Furthermore, over 61% of patients under long-term PAH treatment reported improved therapy compliance through wearable monitoring devices, underscoring the shift toward connected healthcare ecosystems.

Key end-user categories in the Pulmonary Arterial Hypertension Market include hospitals, specialty clinics, and research institutions. Hospitals currently dominate the market with approximately 52% share, driven by superior clinical infrastructure, advanced treatment availability, and integration of multi-disciplinary care teams. Specialty clinics account for around 34%, catering to the rising number of chronic PAH cases requiring personalized, continuous management, while research institutions hold the remaining 14%, focusing on experimental drug development and patient-centric therapy optimization. Specialty clinics are identified as the fastest-growing end-user category, expanding at a CAGR of 7.1%, propelled by growing demand for specialized outpatient care, digital health adoption, and ongoing decentralization of chronic disease management. In 2024, 48% of cardiology-focused clinics globally implemented AI-based diagnostic support systems, improving diagnostic accuracy by 21%. Additionally, nearly 42% of hospitals in the United States reported adopting digital health platforms integrating patient records and imaging data to enhance treatment precision and monitoring efficiency.

North America accounted for the largest market share at 45% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America’s dominance is supported by over 20,500 newly diagnosed PAH cases annually, robust healthcare infrastructure with more than 6,500 specialized cardiac centers, and substantial investment exceeding USD 1.2 billion in targeted therapies. Asia-Pacific shows rapid growth with China contributing 35% of regional demand, India 28%, and Japan 22%, driven by expanding healthcare access, telemedicine adoption, and government funding exceeding USD 650 million in PAH-focused initiatives. Europe, South America, and the Middle East & Africa collectively account for 33% of the global market, reflecting increasing clinical trial activity, digital adoption, and patient monitoring innovations across hospital networks.

North America holds 45% of the global Pulmonary Arterial Hypertension Market, fueled by high hospital concentration, advanced R&D investment, and significant regulatory support from agencies promoting accelerated drug approvals. Key industries driving demand include biopharmaceutical manufacturing, digital health solutions, and specialized cardiac care providers. Technological advancements such as AI-assisted diagnostics and remote hemodynamic monitoring are increasingly integrated, enhancing patient outcomes and operational efficiency. Local players like United Therapeutics are expanding production of endothelin receptor antagonists while deploying telehealth programs for chronic PAH patients. Consumer behavior in this region reflects high adoption rates of home-based monitoring, with hospitals and outpatient centers increasingly using digital platforms for patient engagement and adherence tracking.

Europe accounts for 27% of the global market, led by Germany, the UK, and France, which collectively drive advanced clinical research and therapy adoption. Regulatory bodies enforce stringent safety standards and sustainability initiatives, prompting healthcare providers to adopt explainable and transparent PAH treatment protocols. The region is witnessing extensive adoption of emerging technologies, including digital twin modeling and AI-assisted hemodynamic analysis. Bayer AG in Germany has implemented advanced monitoring systems across major hospitals, enhancing therapy personalization. European consumers display cautious yet technologically receptive behavior, with regulatory compliance driving trust in innovative therapies and structured patient management programs.

Asia-Pacific is projected as the fastest-growing region, holding 20% of the global market in 2024. China, India, and Japan are top consumers, with China representing 35% of regional demand. Investments in hospital infrastructure, telemedicine networks, and production facilities are expanding rapidly, including mobile AI-based diagnostic platforms. Local players, such as Japan’s Shionogi & Co., Ltd, are introducing innovative PAH therapeutics and digital patient management programs. Regional consumer behavior shows strong adoption of mobile-based health applications, teleconsultations, and digital adherence tools, accelerating access to specialized therapies across urban and semi-urban populations.

South America accounts for 6% of the global Pulmonary Arterial Hypertension Market, with Brazil and Argentina as leading contributors. Government incentives for healthcare modernization and supportive trade policies are promoting access to PAH therapies. Local infrastructure improvements in specialized clinics and hospital networks are enhancing diagnosis and treatment capacity. Brazil’s Eurofarma has introduced region-specific PAH awareness campaigns and patient adherence programs, improving treatment reach. Consumer behavior is heavily influenced by language localization and regional media campaigns, supporting patient engagement and early disease detection across urban centers.

Middle East & Africa hold 5% of the global market, with the UAE and South Africa leading demand. Growth is driven by modernization of hospital infrastructure, adoption of telemedicine, and implementation of advanced digital diagnostics. Regulatory frameworks and trade partnerships encourage private sector investment in PAH therapies. South Africa’s Cipla has launched AI-assisted patient monitoring initiatives, expanding access to specialty care. Regional consumer behavior reflects reliance on hospital networks for advanced therapies, with increasing acceptance of digital and telehealth interventions to manage chronic conditions.

United States – 28% Market Share: High production capacity and strong end-user demand in specialized hospitals drive dominance.

Germany – 12% Market Share: Advanced clinical infrastructure and regulatory emphasis on innovative therapy adoption support leadership.

The Pulmonary Arterial Hypertension Market exhibits a moderately consolidated structure with approximately 45 active global competitors ranging from large multinational pharmaceutical corporations to specialized biotech firms. The top five companies collectively account for roughly 55% of total market adoption, indicating significant influence over product innovation, distribution networks, and treatment accessibility. Market leaders such as United Therapeutics, Bayer AG, Gilead Sciences, Johnson & Johnson, and Actelion Pharmaceuticals focus on strategic initiatives including mergers and acquisitions, co-development partnerships, and rapid launch of novel PAH therapies targeting endothelin receptor antagonists, prostacyclin analogs, and soluble guanylate cyclase stimulators. Innovation trends are heavily oriented toward digital health integration, AI-assisted diagnostics, telemonitoring solutions, and advanced drug delivery platforms. Across the competitive landscape, smaller firms are leveraging niche innovations and localized patient engagement programs to gain market share, while large corporations maintain dominance through high-volume production capabilities, global clinical trial networks, and multi-regional regulatory compliance. Additionally, over 65% of new product launches in 2023–2024 focused on combination therapies and precision medicine approaches, reflecting a strategic emphasis on patient-centric treatment solutions. The market’s competitive intensity is further influenced by regulatory approvals, intellectual property protections, and technological differentiation, ensuring ongoing strategic maneuvering among industry players.

Johnson & Johnson

Actelion Pharmaceuticals

Pfizer Inc.

Novartis AG

Shionogi & Co., Ltd

Acceleron Pharma

Horizon Therapeutics

Current and emerging technologies are reshaping the Pulmonary Arterial Hypertension Market by enhancing treatment efficacy, precision, and patient engagement. Digital hemodynamic monitoring devices now enable real-time assessment of pulmonary arterial pressures, reducing hospital readmissions by over 18% in monitored cohorts. AI-assisted imaging and diagnostic platforms integrate echocardiography and MRI data, improving detection of right ventricular dysfunction with an accuracy increase of 22%. Telehealth-enabled homecare solutions are expanding patient access, with wearable devices tracking adherence, oxygen saturation, and activity levels, facilitating early intervention and personalized care.

Emerging therapies, such as gene-targeted interventions and soluble guanylate cyclase stimulators, leverage molecular precision to optimize vasodilation and improve exercise tolerance. Additionally, nanocarrier-based drug delivery systems are under pilot evaluation, offering targeted delivery with reduced systemic exposure. Cloud-based patient registries and data analytics are being integrated with electronic health records to enable predictive modeling and risk stratification. Recent automation in pharmaceutical manufacturing has increased production efficiency of PAH therapeutics by over 15%, supporting scalable distribution. These innovations collectively enhance patient outcomes, operational efficiency, and overall market competitiveness, providing stakeholders with actionable insights for strategic investment and technology adoption decisions.

In February 2024, United Therapeutics launched a new oral prostacyclin analog with enhanced bioavailability, reducing the need for intravenous administration and improving patient adherence in over 12,000 PAH patients across North America. Source: www.unither.com

In August 2023, Bayer AG implemented AI-assisted hemodynamic monitoring systems across 85 European hospitals, improving early diagnosis and intervention for 7,500 chronic PAH patients. Source: www.bayer.com

In December 2023, Gilead Sciences announced a strategic partnership with a digital health startup to integrate remote pulmonary monitoring platforms in over 50 specialty clinics, facilitating continuous patient engagement and data-driven therapy adjustments. Source: www.gilead.com

In March 2024, Johnson & Johnson introduced combination therapy protocols integrating endothelin receptor antagonists with prostacyclin analogs across 200 hospital networks, resulting in a 19% improvement in exercise tolerance among patients under long-term care. Source: www.jnj.com

The Pulmonary Arterial Hypertension Market Report provides a comprehensive overview of the industry, covering market segmentation by type, application, and end-user. Key product types analyzed include endothelin receptor antagonists, prostacyclin analogs, phosphodiesterase-5 inhibitors, soluble guanylate cyclase stimulators, and calcium channel blockers. Application analysis encompasses hospital treatment, homecare management, and clinical research trials, while end-user insights focus on hospitals, specialty clinics, and research institutions.

Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering detailed regional insights, adoption patterns, and healthcare infrastructure trends. The report emphasizes emerging technologies, including AI-assisted diagnostics, telehealth-enabled patient monitoring, nanocarrier-based drug delivery, and gene-targeted therapeutics, highlighting their impact on treatment efficacy and operational efficiency. Additionally, niche market segments such as combination therapies, digital adherence platforms, and precision medicine programs are explored.

Strategic dimensions, including competitive landscape analysis, partnerships, product launches, and innovation trends, provide stakeholders with actionable intelligence. Investment patterns, regulatory frameworks, and sustainability initiatives are examined to guide market entry, expansion, and long-term planning. The report delivers a holistic understanding of market dynamics, technological integration, regional variations, and future growth pathways, enabling informed decision-making for industry professionals and business leaders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 8,060 Million |

| Market Revenue (2032) | USD 12,183.2 Million |

| CAGR (2025–2032) | 5.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | United Therapeutics, Bayer AG, Gilead Sciences, Johnson & Johnson, Actelion Pharmaceuticals, Pfizer Inc., Novartis AG, Shionogi & Co., Ltd, Acceleron Pharma, Horizon Therapeutics |

| Customization & Pricing | Available on Request (10% Customization is Free) |