Reports

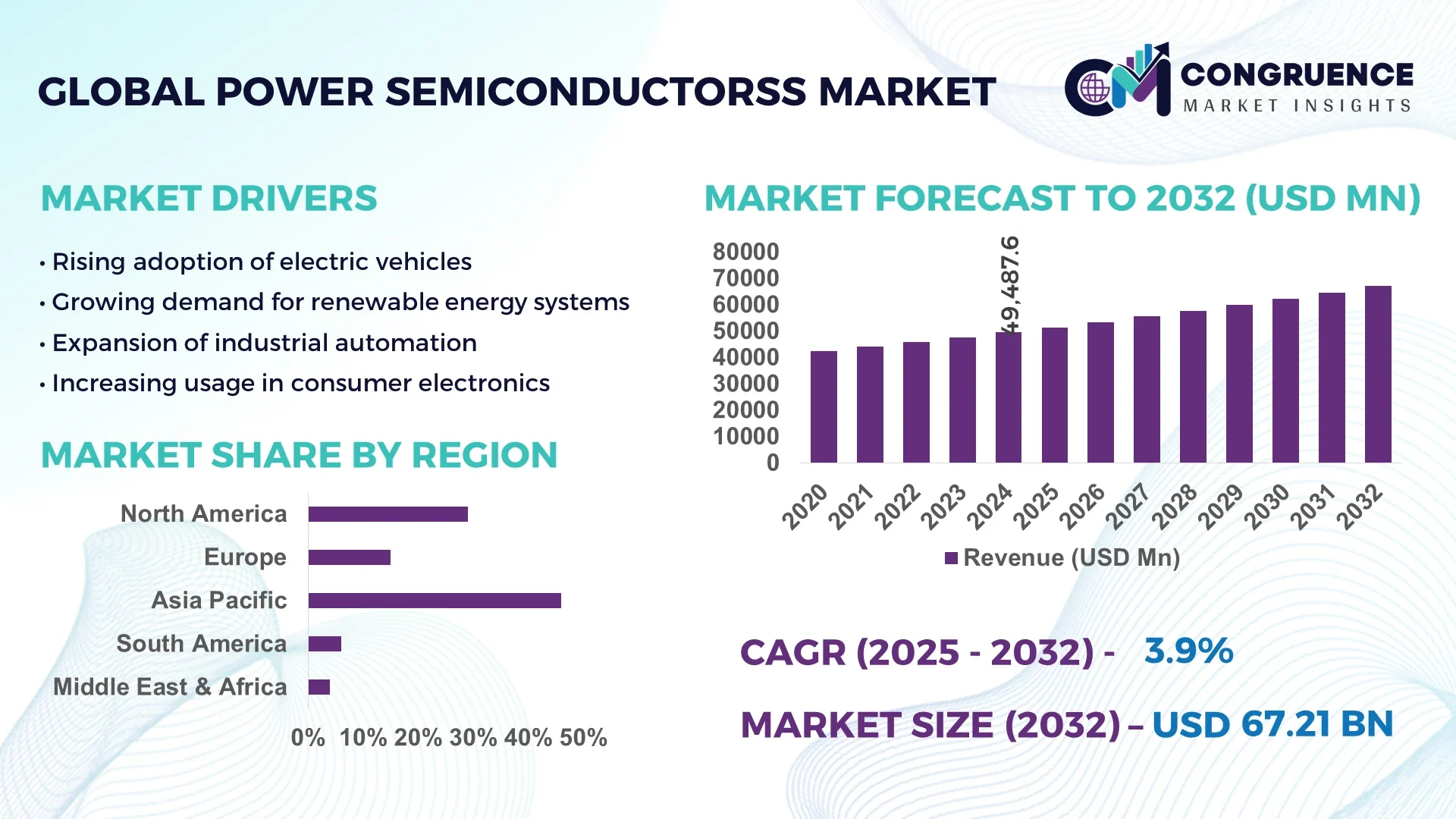

The Global Power Semiconductors Market was valued at USD 49487.57 Million in 2024 and is anticipated to reach a value of USD 67207.92 Million by 2032 expanding at a CAGR of 3.9% between 2025 and 2032.

China significantly influences the global Power Semiconductors Market with its substantial production capacity, extensive investments in silicon carbide (SiC) and gallium nitride (GaN) technologies, and strong integration of power devices into electric vehicle infrastructure, renewable energy and industrial automation systems—bolstering technological advancements in high-voltage IGBT modules and wide-bandgap semiconductors with ongoing enhancements in wafer fabrication precision and thermal management techniques.

Key segments in this evolving market include automotive electrification, particularly battery electric vehicles (BEVs), renewable energy inverters, industrial motor drives, and power supplies for data centers. Notably, IGBT modules continue to play a pivotal role in BEV powertrains, while BCD (Bipolar-CMOS-DMOS) processes are driving smarter, more integrated power management solutions. Recent technological innovations encompass the shift toward compound semiconductors such as SiC and GaN, enabling higher efficiency and reduced thermal losses. Regulatory and environmental imperatives—such as energy efficiency standards and carbon reduction mandates—are compelling manufacturers to adopt lower-loss materials and optimize performance. Economic drivers, including infrastructure modernization in developing economies and demand from high-growth verticals like EV charging networks and grid stabilization, are accelerating adoption. Regional consumption patterns show robust growth in Asia-Pacific, driven by industrial automation and renewable capacity expansion, alongside steady demand in North America and Europe for advanced power solutions. Emerging trends shaping the future include the integration of embedded smart sensing in power modules, miniaturization of packaging, digital twin-based predictive maintenance, and convergence with AI-enabled power system optimization. As the market evolves, decision-makers are focusing investments on scalable, resilient, and high-efficiency power semiconductor architectures tailored to future electrified and sustainable applications.

AI is reshaping the Power Semiconductors Market through transformative enhancements in design precision, manufacturing efficiency, predictive maintenance, and supply chain optimization. Across chip design workflows, AI-driven Electronic Design Automation (EDA) tools are accelerating layout generation, optimizing power-performance-area (PPA) metrics, and shortening development timelines from months to weeks—ultimately boosting design productivity and enabling more efficient semiconductor solutions. AI is also being applied on the factory floor: machine learning analytics reduce defect rates, increase yields, and optimize resource utilization during wafer fabrication. In process engineering, AI-based control systems adjust manufacturing parameters in real time, improving consistency and lowering energy consumption.

In addition, AI-powered predictive maintenance is enhancing the reliability and throughput of power semiconductor production by proactively identifying equipment anomalies and minimizing unplanned downtime. Within the supply chain, AI forecasts materials demand and flags potential disruptions, enabling manufacturers to maintain optimal inventory and respond swiftly to component shortages. These AI applications collectively elevate operational performance across the Power Semiconductors Market, enabling smarter production, faster time-to-market, and superior quality. By embedding AI across design, production, testing, and logistics, organizations are cultivating a more resilient, efficient, and innovative power semiconductor ecosystem, unlocking greater value for industry decision-makers and professionals.

“Synopsys reports that its AI-powered DSO.ai tool was used in over 100 commercial chip tape-outs by 2023, enabling increases in productivity and reductions in power consumption; further innovations like VSO.ai and TSO.ai are delivering up to 10× improvements in verification coverage and around 30 % boosts in IP verification throughput.”

The Power Semiconductors Market is experiencing dynamic shifts driven by advancements in wide-bandgap materials, growing electrification trends, and expanding renewable integration. Automotive electrification is a primary influence, with electric vehicles requiring efficient inverters, onboard chargers, and battery management systems built on IGBT and SiC technologies. Renewable energy adoption, particularly in solar and wind, fuels demand for high-performance modules that improve grid efficiency and energy conversion. Industrial automation and robotics are adding to consumption with increased deployment of smart motor drives and efficient power control systems. Simultaneously, data center expansion and 5G infrastructure are stimulating demand for low-loss, compact semiconductors. While technological progress and regulatory frameworks drive market expansion, challenges such as manufacturing complexity and raw material dependencies continue to shape the competitive landscape. Decision-makers are focusing on balancing innovation with cost-efficiency, driving investments in scalable designs and digital integration for long-term market sustainability.

The increasing shift toward electric vehicles and renewable energy installations is a major growth driver in the Power Semiconductors Market. Electric vehicles demand high-efficiency inverters, DC-DC converters, and fast-charging capabilities, which are enabled by SiC and GaN-based semiconductors offering higher voltage tolerance and reduced switching losses. The global EV fleet exceeded 18 million in 2024, significantly increasing the requirement for power modules in drivetrains and charging infrastructure. Likewise, solar PV capacity additions surpassed 400 GW in 2024, spurring demand for inverters and advanced semiconductor devices. This surge in electrification is creating sustained momentum for next-generation semiconductor technologies that enhance performance, efficiency, and reliability across mobility and energy ecosystems.

Despite strong demand, the Power Semiconductors Market faces challenges due to the technical complexity and cost intensity of manufacturing advanced devices. Wide-bandgap semiconductors such as SiC and GaN require specialized substrates, epitaxial layers, and precision wafer fabrication, which involve higher capital expenditure and operational costs. Wafer defect density and yield variability continue to hinder mass adoption, particularly for large-area SiC wafers. In 2024, average SiC wafer production costs remained nearly five times higher than silicon equivalents, limiting affordability for smaller manufacturers and slowing scale-up in cost-sensitive applications. These restraints necessitate continuous R&D investments and supply chain optimization to balance efficiency with economic viability in the global market.

The emergence of AI and digital twin applications in the Power Semiconductors Market offers significant opportunities to streamline operations, optimize energy use, and improve yield rates. AI-powered process optimization is already reducing defect levels in wafer fabrication by more than 20% in pilot deployments, while digital twin models are enabling predictive simulation for device performance under varied conditions. This innovation not only reduces time-to-market but also enhances scalability for customized applications in EV, data centers, and renewable systems. Furthermore, AI-enabled supply chain forecasting supports proactive resource planning amid fluctuating raw material availability. As digital adoption accelerates, companies integrating these technologies stand to gain a competitive advantage through reduced costs, higher efficiency, and faster innovation cycles.

A critical challenge in the Power Semiconductors Market is the heavy reliance on specialized raw materials such as silicon carbide powders, gallium nitride substrates, and rare earth elements. Fluctuating supply availability, geopolitical tensions, and concentration of suppliers in specific regions expose the industry to volatility. In 2024, supply shortages of SiC wafers delayed shipments for several major EV manufacturers, highlighting the vulnerability of the ecosystem. Additionally, energy-intensive processing of these materials raises sustainability concerns and increases exposure to regulatory pressures on emissions. These factors complicate planning and increase costs, forcing manufacturers to diversify sourcing strategies and invest in recycling or alternative material research to mitigate long-term risks.

• Expansion of Wide-Bandgap Semiconductors: The adoption of wide-bandgap materials such as silicon carbide (SiC) and gallium nitride (GaN) is accelerating across multiple industries due to their superior efficiency and thermal performance. In 2024, shipments of SiC MOSFETs increased by more than 40% compared to the previous year, driven primarily by electric vehicle inverters and industrial motor drives. GaN devices are increasingly applied in fast-charging solutions, enabling compact designs with improved power density. This rapid transition is reshaping supplier strategies, with leading manufacturers investing in large-scale wafer production to meet rising demand from automotive and renewable energy applications.

• Integration of Power Semiconductors in Data Centers: The exponential rise in data traffic from cloud computing and AI workloads is creating heightened demand for energy-efficient power devices. Advanced semiconductors are enabling higher power conversion efficiency in data centers, with SiC-based power supplies achieving efficiency ratings above 98%. Hyperscale operators are investing in wide-bandgap technology to reduce operating costs and manage thermal loads across server farms. In 2024 alone, over 30% of new high-capacity data centers incorporated SiC-based rectifiers and power modules, reflecting a clear shift toward efficiency-driven infrastructure upgrades.

• Growth of Fast-Charging Infrastructure for Electric Vehicles: The rapid deployment of ultra-fast charging stations is significantly boosting demand for high-voltage power semiconductor modules. Public charging stations capable of 350 kW output require efficient and compact power devices, particularly SiC MOSFETs, which offer reduced switching losses and support high-frequency operation. In Europe, over 12,000 fast-charging stations were operational by mid-2024, with each installation requiring multiple high-capacity semiconductor modules. This trend is pushing suppliers to develop robust, high-power density solutions tailored to withstand heavy usage cycles and demanding thermal environments.

• Miniaturization and Advanced Packaging Technologies: As consumer electronics and automotive systems demand compact designs, the Power Semiconductors Market is experiencing strong adoption of advanced packaging solutions such as chip-on-wafer, wafer-on-substrate, and 3D stacking. Miniaturized modules reduce system size while enhancing thermal conductivity and reliability. In 2024, the share of power modules adopting double-sided cooling designs grew by 25%, driven by requirements in EV powertrains and renewable energy converters. This packaging evolution is not only enhancing performance but also reducing costs in mass production, positioning it as a key enabler of next-generation semiconductor deployment.

The Power Semiconductors Market is structured across three primary segments: types, applications, and end-users. By type, the market spans discrete devices, modules, and ICs, each serving specific operational requirements. Discrete semiconductors remain widely used for cost-sensitive applications, while modules are central to high-voltage, high-efficiency systems in automotive and industrial domains. From an application perspective, electric vehicles, renewable energy systems, data centers, and industrial motor drives dominate demand. EVs lead consumption with rising adoption of electrified transport, while renewable inverters and high-capacity servers represent rapidly scaling uses. End-user insights reveal automotive and industrial sectors as primary consumers, with utilities and data centers also driving adoption. Consumer electronics, though smaller in share, remain consistent contributors to growth. Together, these segments highlight the multifaceted demand across industries seeking reliable, efficient, and sustainable power solutions.

In terms of types, power modules account for the largest share in the Power Semiconductors Market, as they deliver superior efficiency and compactness in high-voltage applications such as electric vehicles, renewable energy inverters, and grid management systems. Their ability to integrate multiple devices into a single package reduces design complexity while enhancing performance. Discrete semiconductors, including diodes, transistors, and thyristors, remain essential for low- and medium-power systems due to cost-effectiveness and wide availability. However, integrated circuits (ICs) designed for power management are witnessing the fastest growth, supported by the proliferation of consumer electronics and the miniaturization of automotive systems. The growing integration of smart sensing features within ICs is also enabling adaptive control in power distribution. Niche products such as GaN-based devices are gaining momentum in fast-charging and telecom equipment, offering high efficiency in compact form factors. Collectively, these diverse types ensure the market caters to both high-power industrial needs and rapidly scaling consumer demand.

Electric vehicles represent the leading application in the Power Semiconductors Market, driven by the increasing shift toward sustainable transportation and the demand for high-efficiency powertrain solutions. Power modules and IGBTs are essential for battery management systems, inverters, and onboard chargers, making EVs a cornerstone of market demand. Renewable energy applications, particularly solar and wind inverters, are the fastest-growing segment as global capacity expansion accelerates and grid operators demand high-efficiency power conversion solutions. Data centers are also emerging as critical consumers, with advanced semiconductors improving energy efficiency and reducing thermal loads in large-scale server farms. Industrial motor drives, a longstanding application, continue to contribute steadily with the rising deployment of automation and robotics across global manufacturing facilities. Consumer electronics, including smartphones and laptops, leverage GaN and SiC devices for compact, energy-efficient charging solutions. Together, these applications highlight the growing role of power semiconductors in enabling electrification, efficiency, and digital transformation across industries.

Automotive stands as the leading end-user in the Power Semiconductors Market, as electrification and hybridization trends accelerate demand for efficient modules and high-voltage switching devices. The rapid expansion of EV fleets worldwide underscores the sector’s dominance, with semiconductors serving as the backbone of propulsion, charging, and safety systems. Utilities and energy providers represent the fastest-growing end-user segment, spurred by large-scale renewable integration, smart grid deployment, and the need for efficient power conversion systems in decentralized energy networks. Industrial end-users maintain strong adoption levels, particularly in automation, robotics, and motor drive systems, ensuring stable demand. Data centers are becoming increasingly influential, with hyperscale operators investing heavily in wide-bandgap semiconductors to improve energy performance. Consumer electronics remain a consistent contributor, with growth driven by compact, fast-charging solutions for mobile devices. This diverse end-user base demonstrates the adaptability of power semiconductors, catering to mobility, energy, industrial, and digital sectors alike.

Asia-Pacific accounted for the largest market share at 46% in 2024 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

The dominance of Asia-Pacific is attributed to the concentration of semiconductor manufacturing hubs, robust industrial output, and rising EV production across China, Japan, and South Korea. North America and Europe maintain significant positions, supported by technological innovation and regulatory backing for clean energy integration. Meanwhile, South America and Middle East & Africa are witnessing rapid adoption, fueled by infrastructure modernization, renewable energy projects, and government-led industrial diversification programs.

Advanced Technology Adoption Driving Power Systems Evolution

North America captured 24% of the global Power Semiconductors Market in 2024, supported by strong demand from electric vehicles, aerospace, and industrial automation sectors. The U.S. remains the key contributor, with federal and state-level incentives accelerating EV adoption and grid modernization. Regulatory measures such as energy efficiency mandates are pushing utilities and manufacturers to integrate wide-bandgap devices for higher performance. Digital transformation is prominent, with leading companies adopting AI-based design and manufacturing solutions to optimize production efficiency. Technological advancements in SiC power modules and integration of smart sensing in industrial drives continue to reinforce the region’s role as a hub for innovation.

Green Transition Accelerating Semiconductor Integration

Europe represented 19% of the global Power Semiconductors Market in 2024, with Germany, the UK, and France being major contributors. The European Union’s stringent sustainability targets and policies promoting renewable integration have created robust demand for efficient power conversion devices. Countries are investing heavily in wind and solar installations, with Germany leading in renewable inverters deployment. Wide-bandgap technologies are being rapidly adopted across automotive electrification programs, particularly in premium EV manufacturing. Regulatory bodies are also pushing for greener production processes, with initiatives under the European Green Deal encouraging semiconductor suppliers to innovate eco-friendly materials and reduce carbon footprints.

Manufacturing Dominance and Rapid Electrification Momentum

Asia-Pacific held 46% of the global Power Semiconductors Market in 2024, making it the largest regional segment. China dominates with extensive wafer fabrication capacity and strong EV supply chain integration, followed by Japan and South Korea with advanced R&D in wide-bandgap devices. India is emerging as a growth hotspot, driven by government incentives for local semiconductor manufacturing and expansion in renewable energy deployment. Regional demand is bolstered by massive infrastructure projects, rapid urbanization, and the digital economy’s growth. Innovation hubs across Taiwan and Singapore are also contributing with breakthroughs in chip miniaturization, packaging, and AI-enabled semiconductor design.

Infrastructure Expansion Creating Steady Semiconductor Demand

South America accounted for 6% of the Power Semiconductors Market in 2024, with Brazil and Argentina being the largest contributors. Brazil’s growing electric mobility programs and grid modernization projects are fueling demand for efficient semiconductor modules. Argentina is leveraging its renewable energy expansion, particularly wind and solar, to adopt advanced power conversion devices. Infrastructure development across transport and energy sectors is pushing governments to incentivize the adoption of high-performance semiconductors. Trade policies supporting local manufacturing and regional collaboration are further strengthening the foundation for gradual market expansion.

Energy Diversification and Industrial Modernization Fueling Growth

The Middle East & Africa accounted for 5% of the Power Semiconductors Market in 2024 but is set to experience the fastest expansion over the forecast period. The UAE and Saudi Arabia are leading in deploying wide-bandgap power devices for renewable integration and smart grid projects, while South Africa is driving adoption in industrial automation and mining operations. Demand is also rising from oil and gas projects requiring reliable, high-efficiency power modules. Regional regulations encouraging energy diversification, coupled with trade partnerships for semiconductor imports, are creating favorable conditions for growth. Digital modernization initiatives across construction and telecom sectors further accelerate adoption.

China: 29% market share | Dominates due to extensive manufacturing capacity, large-scale EV adoption, and advanced semiconductor R&D hubs.

United States: 18% market share | Strong leadership supported by innovation in wide-bandgap technologies and robust demand from aerospace, EV, and data center industries.

The Power Semiconductors Market is characterized by a highly competitive environment, with more than 35 globally active companies shaping industry growth through technology innovation, capacity expansion, and strategic partnerships. Leading firms are heavily investing in wide-bandgap technologies such as silicon carbide (SiC) and gallium nitride (GaN), with multiple new production facilities announced in 2024 to address rising demand from automotive and renewable energy sectors. Competition is intensified by regional players focusing on cost-competitive solutions, while global leaders differentiate through advanced packaging, digital integration, and AI-driven design tools. Mergers and acquisitions remain a recurring strategy, with several transactions in 2024 aimed at consolidating capabilities in wafer production and power module design. Product launches have also been frequent, particularly in the automotive and data center segments, with manufacturers introducing high-efficiency modules tailored for fast-charging and high-density power supplies. Innovation trends such as double-sided cooling, chip miniaturization, and predictive digital twins are further influencing competitive positioning. As a result, market leaders continue to emphasize R&D, scalability, and collaboration to strengthen their footprint in this evolving and technology-driven ecosystem.

Infineon Technologies AG

ON Semiconductor Corporation

Mitsubishi Electric Corporation

STMicroelectronics N.V.

Toshiba Electronic Devices & Storage Corporation

Texas Instruments Incorporated

Renesas Electronics Corporation

Fuji Electric Co., Ltd.

NXP Semiconductors N.V.

Rohm Semiconductor

The Power Semiconductors Market is undergoing significant transformation driven by technological innovation across materials, design, and manufacturing processes. Wide-bandgap semiconductors such as silicon carbide (SiC) and gallium nitride (GaN) are at the forefront, enabling higher power density, faster switching speeds, and improved thermal performance compared to conventional silicon devices. In 2024, global shipments of SiC MOSFETs grew by over 40%, particularly in electric vehicles, renewable energy inverters, and industrial automation systems. GaN devices are seeing rapid adoption in consumer electronics and fast-charging applications, where compact form factors and high efficiency are critical.

Advanced packaging technologies are also reshaping the market. Double-sided cooling modules, 3D stacking, and wafer-on-substrate designs are enhancing thermal management and system miniaturization, leading to greater performance reliability in high-voltage systems. The integration of embedded sensors into modules allows for real-time monitoring, predictive maintenance, and enhanced safety features in automotive and grid applications. Digital twin models and AI-driven design automation are further optimizing device development, reducing design cycles, and improving yield rates during manufacturing.

Meanwhile, ultra-high voltage IGBTs and hybrid modules combining SiC with traditional silicon are extending adoption across utility-scale energy storage and smart grids. Innovations in substrate manufacturing are lowering defect densities in SiC wafers, improving scalability for mass production. Collectively, these advancements position the Power Semiconductors Market as a central enabler of next-generation electrification, efficiency improvements, and sustainable energy transitions.

• In February 2023, Infineon Technologies expanded its CoolSiC portfolio with 750 V MOSFETs tailored for renewable energy and industrial applications, offering reduced switching losses and up to 99% efficiency in inverter systems.

• In July 2023, STMicroelectronics introduced new MasterGaN integrated power packages designed for fast-charging adapters, delivering higher power density and reducing overall system size for consumer electronics.

• In March 2024, ON Semiconductor opened a new 300 mm silicon carbide fabrication facility in the United States, increasing production capacity to support the growing demand in automotive electrification and energy infrastructure.

• In May 2024, Mitsubishi Electric unveiled an 8th-generation IGBT module optimized for rail traction systems, offering improved thermal cycling capability and reduced power losses, strengthening its role in heavy-duty transportation applications.

The Power Semiconductors Market Report provides a comprehensive analysis of industry dynamics, covering multiple dimensions including product types, applications, geographic regions, and technological advancements. Segmentation by type includes discrete devices such as diodes and transistors, power modules for high-voltage systems, and integrated circuits designed for efficient power management. Each category is analyzed with respect to performance, adoption trends, and emerging innovations such as SiC and GaN integration. The application scope encompasses automotive electrification, renewable energy systems, industrial automation, data centers, and consumer electronics. Automotive holds a leading position due to the widespread adoption of electric and hybrid vehicles, while renewable energy applications and fast-charging infrastructure represent the fastest-growing segments. Industrial motor drives, robotics, and aerospace systems also contribute significantly to demand.

From a regional perspective, the report examines established and emerging markets including Asia-Pacific, North America, Europe, South America, and Middle East & Africa. Asia-Pacific is the dominant region, with strong manufacturing hubs and rising end-user demand, while other regions are expanding through regulatory initiatives, energy transitions, and infrastructure modernization. Additionally, the report highlights technological trends shaping the industry such as wide-bandgap adoption, advanced packaging, AI-driven design, and embedded sensing solutions. It also explores emerging opportunities in niche areas such as smart grids, ultra-fast charging stations, and semiconductor-enabled renewable storage systems. This holistic scope equips business leaders and decision-makers with actionable insights into the current and future landscape of the Power Semiconductors Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 49487.57 Million |

|

Market Revenue in 2032 |

USD 67207.92 Million |

|

CAGR (2025 - 2032) |

3.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Infineon Technologies AG, ON Semiconductor Corporation, Mitsubishi Electric Corporation, STMicroelectronics N.V., Toshiba Electronic Devices & Storage Corporation, Texas Instruments Incorporated, Renesas Electronics Corporation, Fuji Electric Co., Ltd., NXP Semiconductors N.V., Rohm Semiconductor |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |