Reports

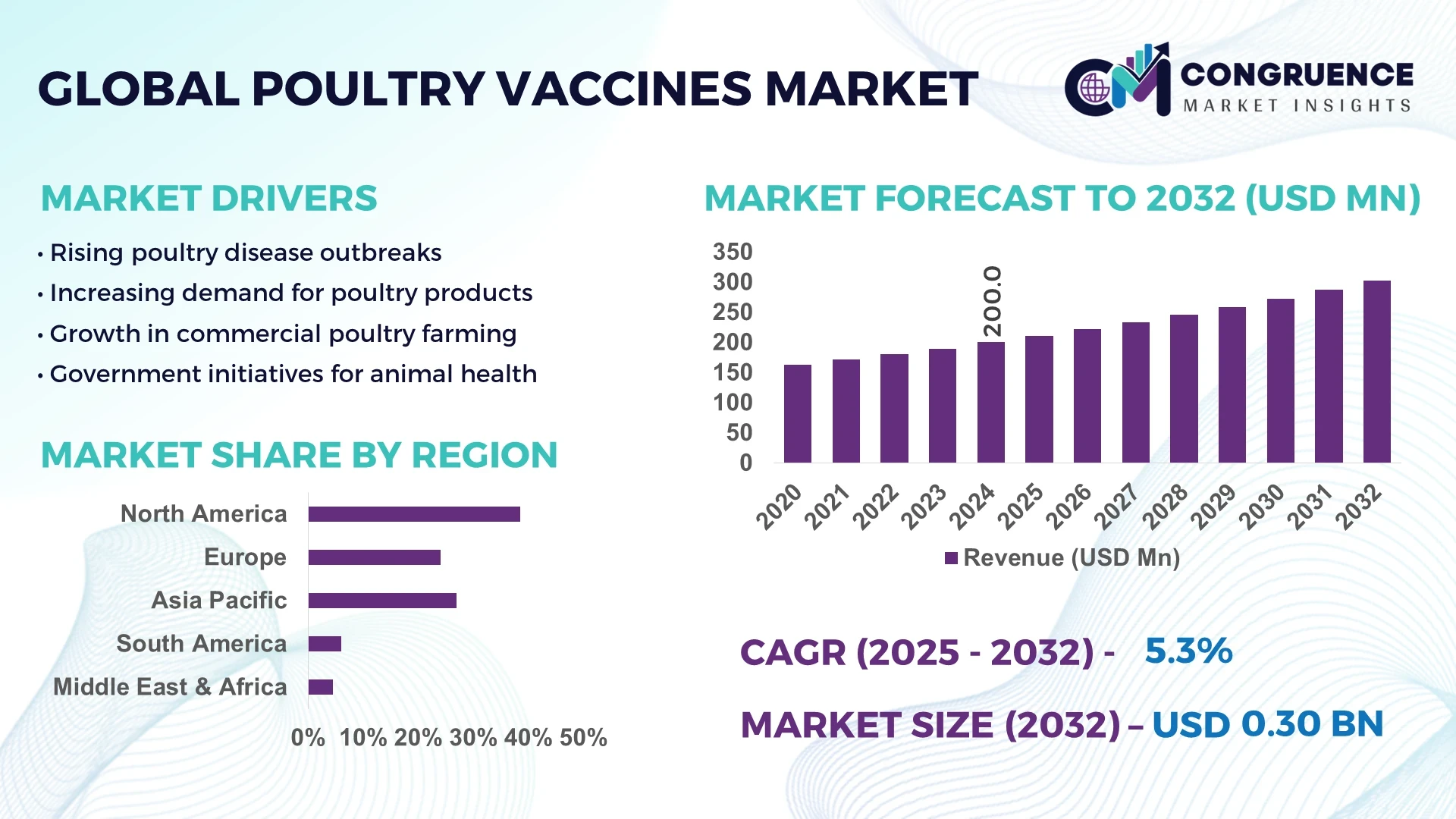

The Global Poultry Vaccines Market was valued at USD 200.0 Million in 2024 and is anticipated to reach a value of USD 302.5 Million by 2032 expanding at a CAGR of 5.31% between 2025 and 2032.

The United States is the dominant country in this marketplace: it maintains substantial production capacity with multiple commercial avian vaccine manufacturers operating large-scale fill-and-finish facilities, continuous investment in GMP-capable biologics infrastructure, widespread application across broiler and layer sectors, and active deployment of high-throughput manufacturing and digital quality-control technologies to support rapid batch release and traceability.

The Poultry Vaccines Market is shaped by diverse end-use sectors including commercial broiler and layer production, breeder operations, and backyard/regulated small-scale holdings. Key industry sectors such as large commercial integrators and veterinary service providers account for the majority of routine immunization programs, while emergency vaccination campaigns for avian influenza and Newcastle disease drive episodic spikes in procurement and deployment. Recent technological and product innovations impacting the market include recombinant and vectored vaccine platforms, virus-like particle and mRNA exploratory candidates, improved adjuvant formulations for extended immunity, and automated hatchery vaccine-delivery systems that improve dosing consistency. Regulatory and environmental drivers—such as stricter animal-health surveillance, biosecurity protocols, and policies aimed at reducing antibiotic use—are increasing institutional reliance on vaccination programs. Regional consumption patterns show mature, high-coverage vaccination programs in North America and parts of Europe, while rapid scaling of vaccination logistics is evident across Asia-Pacific due to expanding poultry production. Emerging trends include integration of digital traceability for cold-chain vaccines, targeted vaccination programs for high-risk zones, and growing use of modular contract-manufacturing to accelerate response to outbreak strains. The future outlook emphasizes portfolio diversification by vaccine manufacturers, closer alignment with diagnostic surveillance data, and continued investment in manufacturing flexibility to address strain drift and episodic disease pressure.

Artificial intelligence (AI) is reshaping multiple facets of the Poultry Vaccines Market by delivering measurable improvements in R&D workflows, production efficiency, vaccination accuracy, and field deployment logistics. In vaccine discovery and antigen design, machine-learning models are being applied to predict immunogenic epitopes and prioritize candidate sequences, reducing the number of experimental constructs required during preclinical development. Within manufacturing, AI-enabled process control systems analyze multivariate sensor data to stabilize fermentation and cell-culture parameters, improve batch-to-batch consistency, and shorten time-to-release for biologics produced for poultry use. On the operational side, computer-vision and object-detection models integrated into hatchery and on-farm vaccine-delivery equipment increase dosing precision and reduce operator variation; for example, advanced vision systems have achieved above-90% detection precision under commercial conditions, enabling automated targeting of individual chicks for more consistent immunization. Logistics and supply-chain optimization in the Poultry Vaccines Market also benefit from predictive analytics: AI models forecast demand spikes tied to disease surveillance signals and seasonal production cycles, enabling manufacturers and distributors to align cold-chain capacity and minimize stockouts during outbreak responses. Post-market surveillance is becoming more data-driven as well—AI tools ingest epidemiological feeds, lab confirmations, and flock-level health records to detect anomalous trends that may indicate vaccine escape or field efficacy issues, triggering targeted investigation and vaccine strain updates. Collectively, these AI applications are raising operational performance metrics across the Poultry Vaccines Market—improving dose delivery accuracy, increasing manufacturing process stability, and shortening development cycles—while enabling more responsive alignment of vaccine supply with dynamic disease risk in commercial poultry systems.

"In 2024, an AI-based poultry monitoring system using the YOLOv8 object-detection model reported a precision of 93.1% and a recall of 93.0% for automated chicken counting under commercial farm conditions, demonstrating reliable real-world performance for flock management and vaccination targeting."

The Poultry Vaccines Market Dynamics are driven by a combination of epidemiological pressures, production system scale, regulatory frameworks, and technological capability. Poultry Vaccines Market activity intensifies around endemic disease control programs (e.g., Newcastle disease, Marek’s disease) and reactive responses to transboundary threats such as highly pathogenic avian influenza. Vertical integration by large poultry integrators affects procurement patterns and vaccination program design, while contract-manufacturing organizations (CMOs) and specialized veterinary biologics firms shape supply options for niche vaccine formats. Advances in vaccine platforms (recombinant, vectored, subunit, and nucleic-acid modalities) and in-ovo or automated hatchery delivery systems are changing how immunization is executed at scale, altering logistics and cold-chain requirements. Regulatory inspections, batch release testing protocols, and national animal-health policies heavily influence time-to-market and the geographic availability of certain vaccine types. Surveillance intensity and diagnostic throughput determine how quickly vaccine strain updates or emergency stockpile releases are triggered, creating a close coupling between diagnostic networks and vaccine manufacturing rhythm. Finally, the Poultry Vaccines Market is seeing growing emphasis on vaccine quality attributes—stability, ease of administration, and compatibility with integrated health programs—shaping procurement decisions at commercial integrators and national veterinary services.

Intensive poultry production systems require vaccines that provide robust, reproducible protection with minimal handling stress and administration labor. This driver’s impact on the Poultry Vaccines Market is evidenced by growing adoption of in-ovo and automated hatchery delivery systems, expanded use of vectored and recombinant formulations that permit DIVA (differentiate infected from vaccinated animals) strategies, and investment in thermostable vaccine formulations that ease cold-chain constraints. Poultry integrators prioritize vaccines that lower mortality and improve uniformity of flock performance; as a result, manufacturers are directing R&D toward multi-valent products and novel adjuvants that extend duration of immunity. Procurement patterns in large commercial operations increasingly favor suppliers that can provide validated administration technologies and technical support, creating a market environment where vaccine efficacy characteristics and operational compatibility are as important as product availability.

A significant restraint for the Poultry Vaccines Market is the regulatory and compliance burden associated with vaccine registration and field authorization. Varying dossier requirements, differing environmental-release assessments for recombinant or novel platforms, and region-specific potency and batch-release testing protocols lengthen the timeline for market entry. For global manufacturers, harmonization gaps between veterinary regulatory authorities necessitate multiple localized studies and can require additional stability and safety data, increasing development costs and delaying commercial availability. These regulatory complexities also affect emergency use authorizations and stockpile deployment, where procedural lead times may limit the speed of response during sudden outbreaks.

There is a clear opportunity in developing thermostable vaccine formulations and delivery formats suited to low-infrastructure settings. Thermostable vaccines reduce reliance on continuous cold chains, lowering logistical barriers for vaccination campaigns in rural or resource-constrained regions. Innovations in micro-encapsulation, dry powder inhalable formats, and orally deliverable formulations offer potential to simplify administration while maintaining protective immunity. For manufacturers and public-private partnerships, scaling thermostable products represents an avenue to open new markets and support mass vaccination campaigns with reduced logistical overhead, improving coverage in regions where cold-chain limitations have historically constrained vaccine uptake.

A persistent challenge for the Poultry Vaccines Market is matching vaccine antigen composition rapidly to circulating field strains, particularly for highly variable viruses. Maintaining flexible manufacturing that can pivot to produce updated antigens requires modular production capacity, validated rapid-release assays, and coordination with surveillance networks. Investments in rapid analytical testing and flexible fill-and-finish lines are necessary to reduce lag between strain identification and vaccine deployment. Additionally, managing regulatory pathways for strain updates and ensuring sufficient raw-material and container supply during surge demand are operational challenges that complicate outbreak response and long-term preparedness.

Rise of Automated Hatchery Vaccination Systems: Automated hatchery vaccination—incorporating precision dispensers and imaging verification—has increased dosing consistency and reduced operator variability. In commercial hatchery trials, automated systems have demonstrated more uniform delivery across thousands of chicks per hour, enabling integrators to scale immunization throughput while maintaining biosecurity standards and reducing manual handling stress.

Shift toward Thermostable and Needle-Free Formulations: There is a measurable trend toward thermostable vaccine presentations and needle-free delivery (spray, aerosol, in-water, and oral formulations) that reduce cold-chain dependency and enable mass administration. Field deployments of thermostable formulations have shortened logistics lead times for rural campaigns, permitting broader geographic coverage without expanded refrigeration infrastructure.

Integration of Digital Traceability and Cold-Chain Monitoring: Vaccine distribution networks are increasingly adopting digital traceability tags and IoT-enabled cold-chain sensors; this trend provides real-time visibility on temperature excursions and vaccine lot movement, improving accountability and reducing wastage in national and commercial distribution systems.

Convergence of Diagnostics and Vaccine Strategy: A growing practice links high-throughput field diagnostics to dynamic vaccination strategies—surveillance data now inform targeted vaccination zones and strain selection more rapidly than in previous years. This convergence has increased the frequency of tactical vaccine deployments in response to localized outbreaks, improving disease control outcomes in densely populated poultry regions.

The Poultry Vaccines Market segmentation is organized across product types, application routes, and end-user categories to reflect technological and operational nuances. By type, segments include live attenuated vaccines, inactivated/killed vaccines, recombinant/vectored vaccines, subunit and protein-based vaccines, and emerging nucleic-acid candidates (e.g., mRNA, DNA). By application route, the market is divided into in-ovo, subcutaneous/intramuscular injection, spray/aerosol, drinking-water, and feed-based administration methods. End-users cover large commercial integrators, contract growers, smallholder/backyard producers, and governmental veterinary services conducting mass campaigns. Each segment influences procurement specifications: injection routes emphasize sterility and precision dosing equipment; in-ovo and automated hatchery methods prioritize compatibility with mechanized delivery platforms; spray and in-water formats focus on stability and dispersion properties; recombinant and vectored types require distinct cold-chain and biosecurity considerations. Analysts and decision-makers use segmentation to align manufacturing investments, choose appropriate distribution channels, and prioritize R&D toward formats that both meet operational constraints and support large-scale immunization programs.

The Poultry Vaccines Market by type covers live attenuated, inactivated/killed, recombinant/vectored, subunit/protein, and nucleic-acid (emerging) vaccines. Live attenuated vaccines remain a core product for many endemic diseases due to strong mucosal and cellular immunity profiles and ease of mass administration in some formats. Inactivated vaccines are widely used where safety and stability are prioritized, such as breeder vaccination programs and certain regulatory environments. Recombinant and vectored vaccines have gained prominence for their ability to express multiple antigens and enable DIVA strategies; these are increasingly selected for disease control programs requiring differentiation between infected and vaccinated birds. Subunit and protein vaccines provide targeted immune responses with favorable safety profiles, useful in specialized applications and breeder flocks. Emerging nucleic-acid platforms (mRNA, DNA) are under investigation and pilot testing for rapid strain updating and accelerated candidate design; these represent the fastest-growing type in R&D activity due to platform flexibility and shortened design cycles, driven by recent investments and interest in pandemic-scale responsiveness. Other niche types, such as plant-produced VLPs (virus-like particles) or inactivated oil-adjuvanted formulations, remain relevant for region-specific programs and legacy use cases.

Application routes in the Poultry Vaccines Market include in-ovo administration, injected (subcutaneous/intramuscular), spray/aerosol, drinking-water, and feed/sachet modalities. In-ovo is widely used for certain live vaccines in large commercial broiler operations as it allows early immunity and centralized application in hatcheries. Injection routes are the leading application where individual dosing precision and vaccine potency verification are required, particularly in breeder or high-value stock. Spray and aerosol applications serve large flocks through group administration, with proven utility in mass campaigns for respiratory pathogens. Drinking-water delivery is used for ease of administration in grow-out houses, though it requires attention to water quality and consumption behavior. Feed-based or oral sachet applications are niche but expanding for ease of administration in backyard and smallholder settings. The leading application is injection and hatchery-based delivery for breeder and integrated systems, driven by the need for controlled immunity in parent flocks. The fastest-growing application in field adoption is automated hatchery/in-ovo delivery, supported by hatchery automation investments and the drive for early, uniform immunity.

End-user segmentation in the Poultry Vaccines Market includes large commercial integrators, independent contract growers, smallholder/backyard producers, and national veterinary services. Large commercial integrators are the leading end-user group because they operate centralized hatcheries and large-scale production systems that require routine, high-volume vaccine procurement and support integrated vaccination programs. The fastest-growing end-user segment is national and regional veterinary services conducting coordinated mass-vaccination campaigns in response to transboundary disease threats; growth is driven by expanded surveillance capacity and public-sector funding for outbreak containment. Independent contract growers and smallholder producers represent additional demand streams, often favoring thermostable and low-handling formulations due to infrastructure constraints. Each end-user group imposes distinct product and service requirements—integrators emphasize compatibility with automated delivery and strict QA/QC; public veterinary services need scalable stocks and rapid deployment logistics; smallholders prioritize cost-effective, easy-administer formulations—informing manufacturer portfolio and distribution strategy.

North America accounted for the largest market share at 38.5% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

Regional patterns in the Poultry Vaccines Market reflect differences in production systems, regulatory frameworks, and disease pressure. North America’s leading position stems from vertically integrated poultry production, advanced veterinary services, and substantial commercial CMO capacity for vaccine fill-and-finish operations. Asia-Pacific’s rapid growth is driven by expansion of commercial broiler and layer production, scaled vaccination roll-outs, and increasing local production of veterinary biologics. Europe maintains a strong regulatory environment with centralized approvals for certain novel vaccines and significant investment in disease surveillance, while South America is expanding capacity linked to large agricultural feedstock availability and export-oriented poultry production. Middle East & Africa present growing demand driven by targeted national vaccination programs and infrastructure investments in biosecurity and cold-chain logistics.

North America held approximately 38.5% of the global Poultry Vaccines Market in 2024. Key industries driving demand include large commercial broiler and breeder integrators, veterinary service companies, and contract vaccine manufacturers. Regulatory updates and government support for emergency stockpiles and avian influenza preparedness have led to increased procurement and investments in rapid manufacturing capabilities. Technological advancements include automated hatchery vaccination systems, AI-enabled process controls for biomanufacturing, and digital traceability solutions for lot tracking and cold-chain monitoring. The region’s robust CMO network and certified biologics facilities support rapid scale-up for updated strain vaccines during outbreaks, while public-private initiatives have strengthened preparedness and rapid response mechanisms.

Europe accounted for roughly 24.0% of the Poultry Vaccines Market in 2024, with Germany, the UK, and France as the leading national markets. European regulatory bodies have emphasized harmonized vaccine approvals and surveillance programs, driving adoption of licensed novel vaccines and centralized marketing authorizations in certain cases. Sustainability initiatives are encouraging the move away from antibiotic reliance and promoting vaccines as a core disease-prevention tool. Adoption of emerging technologies—such as digital batch release, validated thermostable formats, and hatchery automation—is particularly strong in Germany, while France and the UK are notable for coordinated national vaccination campaigns and investment in R&D for next-generation platforms.

Asia-Pacific represented approximately 27.0% of the market by volume in 2024 and ranked as the fastest-growing region by volume. Top consuming countries include China, India, and Japan. Infrastructure trends show significant expansion of hatchery capacity and contract production sites, while manufacturing investments focus on localizing vaccine supply and reducing import dependence. Regional tech trends include adoption of automated hatchery and on-farm delivery systems, local development of recombinant vaccine platforms, and growing innovation hubs in China and India emphasizing scalable biologics production.

South America accounted for about 6.0% of the global Poultry Vaccines Market in 2024, with Brazil and Argentina as key contributors. The region benefits from abundant agricultural feedstock and expanding poultry processing capacity supporting export markets. Infrastructure investments include upgrades to cold-chain logistics and targeted national vaccination programs. Government incentives and trade policies that support agricultural exports have encouraged domestic vaccine procurement and limited regional fill-and-finish expansion.

Middle East & Africa held approximately 4.5% of the market in 2024, with notable activity in the UAE, Saudi Arabia, and South Africa. Regional demand trends reflect a mix of oil-sector diversification into food security, growing construction and industrial modernization, and targeted public vaccination programs for avian influenza control. Technological modernization includes pilot adoption of digital traceability and investments in cold-chain expansion, while trade partnerships are increasingly supporting access to international vaccine suppliers.

United States – 28.0% Market Share

The United States leads due to large-scale production capacity, comprehensive veterinary infrastructure, and significant investments in biologics manufacturing and automated vaccine delivery technologies.

China – 22.0% Market Share

China is a top contributor with extensive poultry integration, rapidly expanding hatchery and contract-manufacturing facilities, and increasing domestic R&D into recombinant and vectored vaccine platforms.

The competitive landscape in the Poultry Vaccines Market comprises a blend of established veterinary biologics firms, specialized regional manufacturers, and a growing number of biotechnology entrants focusing on novel platforms and rapid-response capabilities. There are dozens of active competitors globally, with market positions ranging from full-spectrum vaccine portfolios to niche suppliers of poultry-specific recombinant or thermostable formulations. Strategic initiatives across the sector include capacity expansions for fill-and-finish operations, strategic collaborations between diagnostics and vaccine developers to enable faster strain matching, licensing deals for regional commercialization, and targeted investments in modular manufacturing to improve surge capacity. Innovation trends shaping competition include development of DIVA-capable vaccines, advances in adjuvant science to extend immunity duration, and adoption of automated and in-ovo delivery systems that couple hardware and vaccine product offerings. Competitive differentiation increasingly depends on the ability to provide integrated solutions—vaccine product, validated delivery technology, and cold-chain/logistics support—alongside rapid technical support for outbreak response. New entrants with platform technologies (e.g., VLPs, mRNA/nucleic-acid pipelines) are intensifying competition in R&D, while incumbent firms leverage regulatory experience, manufacturing certifications, and global distribution networks to maintain commercial leadership.

MSD Animal Health (Merck Animal Health)

Zoetis

Elanco Animal Health

Ceva Santé Animale

BOEHRINGER INGELHEIM Animal Health

Phibro Animal Health Corporation

Hipra

Virbac

Vaxxinova International BV

Biovet Pvt. Ltd.

Technological developments play a central role in shaping product pipelines, manufacturing agility, and field administration for the Poultry Vaccines Market. Key platform technologies include live attenuated and inactivated production systems, recombinant/vectored constructs, virus-like particle (VLP) assemblies, and emerging nucleic-acid approaches (mRNA/DNA). Innovations in adjuvant science improve immunogenicity and dose sparing, while formulation science delivers thermostable presentations that ease logistics in low-infrastructure settings. Manufacturing technologies emphasize modular, single-use bioreactor systems that enable rapid scale-up and changeover, as well as flexible fill-and-finish lines designed for multiple vial sizes and closed-system aseptic handling. Downstream processing improvements—such as optimized chromatography and rapid potency assays—reduce release times and support faster deployment. Automated delivery technologies (in-ovo injectors, automated hatchery sprayers, and precision dosing robots) are reducing operator variability and increasing throughput. Digital and analytical technologies including AI-driven process control, computer vision for administration verification, and predictive supply-chain analytics are improving manufacturing yields and operational reliability. Finally, diagnostics and genomic surveillance technologies are tightly coupled to vaccine strategy, enabling faster antigen selection and targeted vaccination campaigns, which underscores the importance of integrated diagnostics-to-vaccine pathways in modern poultry health management.

• In May 2024, an EU-authorized vaccine for circulating avian influenza strains achieved centralized marketing approval for use in chickens, providing a standardized option for large-scale immunization campaigns and enabling coordinated national vaccination programs.

• In 2024, several hatcheries integrated automated vaccine-delivery systems into routine operations, increasing per-hour vaccination throughput and reducing manual handling time during peak chick processing periods.

• In 2024, a major animal health company secured conditional regulatory authorization for a novel avian influenza vaccine formulation intended for emergency stockpiles, enabling rapid release under defined outbreak conditions.

• In May 2023, a contract manufacturer expanded biologics fill-and-finish capacity for poultry vaccines, adding sterile vial lines and cold-chain storage that support faster batch turnaround and improved surge responsiveness.

The report provides comprehensive coverage of the Poultry Vaccines Market across product types, application routes, end-user segments, technologies, and regions to support strategic and operational decision-making. Geographical scope includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with region-level analyses of procurement patterns, manufacturing infrastructure, and regulatory considerations that influence market access. Product segmentation examines live attenuated, inactivated, recombinant/vectored, subunit/protein, and emerging nucleic-acid vaccine types, assessing production requirements, administration compatibility (in-ovo, injection, spray, drinking-water), and stability/performance attributes. End-user analysis covers commercial integrators, contract growers, smallholder producers, and governmental veterinary services, with insights into procurement cycles, cold-chain demands, and on-farm administration logistics. Technology focus spans manufacturing platforms (single-use bioreactors, modular fill-and-finish), formulation science (thermostability, adjuvants), automated delivery systems (in-ovo injectors, hatchery sprayers), and digital tools (AI process control, computer vision, and supply-chain analytics). Operational topics include feedstock and raw-material availability for vaccine production, cold-chain and logistics requirements, quality-assurance and batch-release testing, and emergency stockpile frameworks. The report also profiles competitive positioning—production capacity, strategic partnerships, and R&D roadmaps—and identifies niche opportunities such as thermostable formats, DIVA-capable vaccines, and rapid-update platform technologies that can support faster responses to evolving disease threats. The scope is designed to equip investors, product managers, procurement leads, and policy planners with actionable intelligence to prioritize investments, optimize supply chains, and align vaccine portfolios with evolving poultry health needs.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 200.0 Million |

| Market Revenue (2032) | USD 302.5 Million |

| CAGR (2025–2032) | 5.31% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | MSD Animal Health (Merck Animal Health), Zoetis, Elanco Animal Health, Ceva Santé Animale, BOEHRINGER INGELHEIM Animal Health, Phibro Animal Health Corporation, Hipra, Virbac, Vaxxinova International BV, Biovet Pvt. Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |