Reports

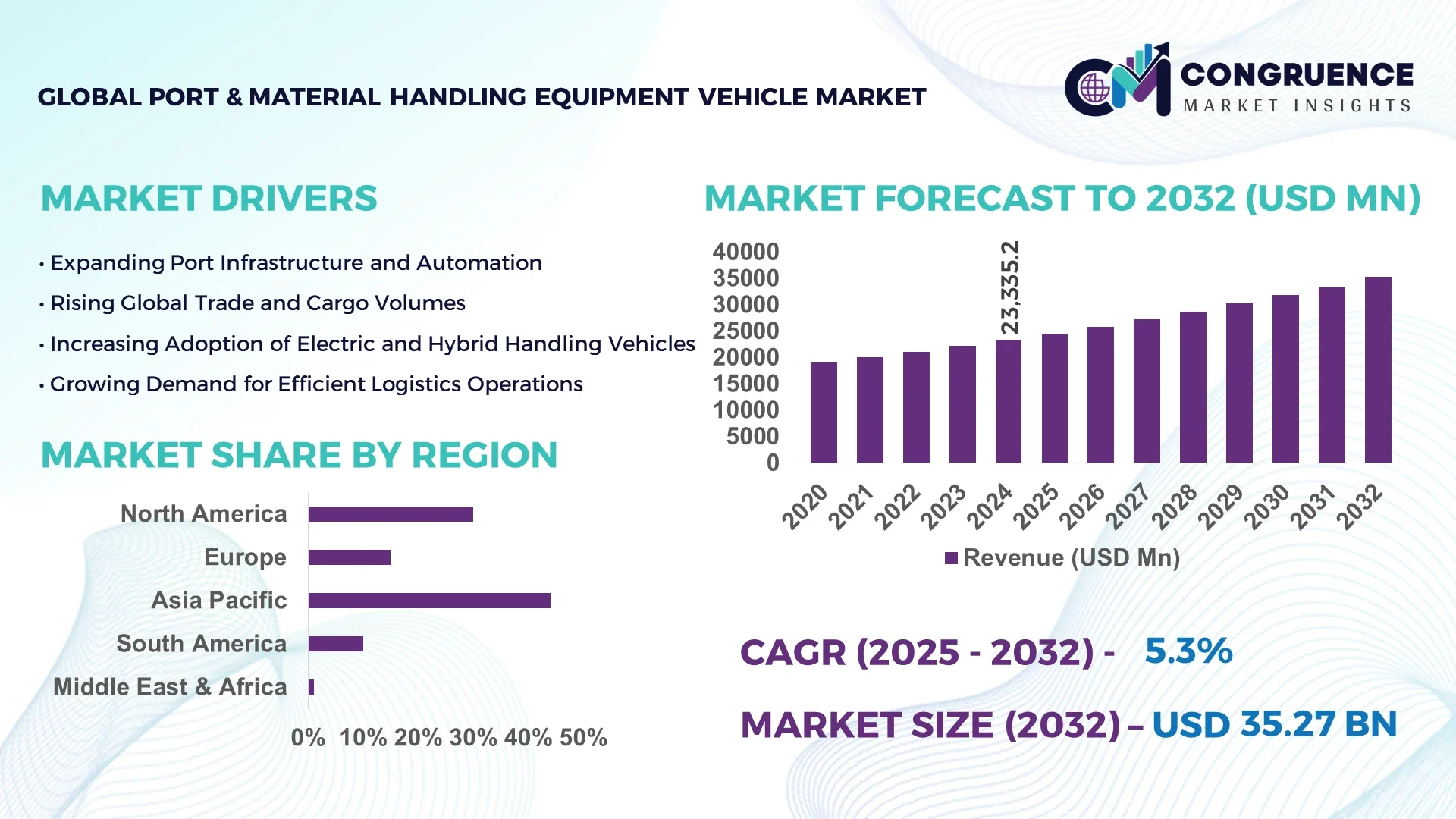

The Global Port & Material Handling Equipment Vehicle Market was valued at USD 23,335.21 Million in 2024 and is anticipated to reach a value of USD 35,272.71 Million by 2032 expanding at a CAGR of 5.3% between 2025 and 2032. This growth is primarily driven by rising automation in port operations and the increasing demand for fuel-efficient handling vehicles.

China leads the Port & Material Handling Equipment Vehicle Market with its vast production capacity exceeding 1.2 million handling units annually, backed by substantial investments in port modernization projects worth over USD 18 billion in 2023. The country has rapidly advanced in electric and hybrid handling vehicles, particularly for container terminals and bulk cargo operations. With over 65% adoption of automated stacking cranes in major coastal ports and continuous deployment of AI-driven fleet management systems, China demonstrates a strong push towards efficiency and sustainability. Growing integration of 5G-enabled monitoring in handling equipment further enhances its technological edge, ensuring global leadership in this sector.

Market Size & Growth: USD 23.33 Billion in 2024, projected at USD 35.27 Billion by 2032, expanding at 5.3% CAGR, driven by automation and digitalization of port operations.

Top Growth Drivers: 58% adoption of automated handling systems, 42% efficiency improvement via electrification, 37% cost optimization through fleet management.

Short-Term Forecast: By 2028, operational downtime expected to reduce by 29% due to predictive maintenance systems.

Emerging Technologies: Electric & hybrid port vehicles, AI-driven fleet optimization, and 5G-based equipment monitoring.

Regional Leaders: Asia-Pacific projected at USD 16.8 Billion by 2032 (dominated by China’s port automation), North America at USD 8.4 Billion (emphasis on sustainability), Europe at USD 7.2 Billion (focus on electrification).

Consumer/End-User Trends: High adoption by container terminals, bulk cargo operators, and logistics hubs emphasizing speed, automation, and fuel efficiency.

Pilot or Case Example: In 2024, Shanghai Port deployed autonomous container trucks reducing cargo handling time by 34%.

Competitive Landscape: Leading player holds ~21% share, followed by major competitors such as Konecranes, Hyster-Yale, Toyota Material Handling, and Cargotec.

Regulatory & ESG Impact: Stricter emission norms and government-backed incentives accelerating adoption of electric and low-emission vehicles.

Investment & Funding Patterns: Over USD 6.5 Billion invested globally in 2023 across port automation and vehicle modernization projects.

Innovation & Future Outlook: Increasing adoption of AI-integrated fleet management, robotics-based cargo handling, and electrification trends shaping long-term market expansion.

The Port & Material Handling Equipment Vehicle Market is witnessing rapid transformation across industries such as shipping, logistics, and manufacturing. Bulk and containerized cargo sectors account for a substantial share of demand, while innovations in autonomous handling systems and electrified vehicles are reshaping operational efficiency. Regulatory pushes toward decarbonization, coupled with economic growth in emerging markets, are influencing adoption trends. Regional consumption patterns highlight Asia-Pacific’s dominance, while Europe and North America focus on green technologies. Looking ahead, digital integration, predictive maintenance, and AI-powered automation will define the future trajectory of this market, creating a robust ecosystem for sustainable and high-performance port operations.

The Port & Material Handling Equipment Vehicle Market holds strategic relevance as a backbone of global trade logistics, enabling seamless cargo flow across container terminals, bulk carriers, and inland distribution hubs. Advancements in electrification, automation, and AI-driven fleet management systems are redefining operational benchmarks. For example, autonomous electric straddle carriers deliver 28% efficiency improvement compared to conventional diesel-powered carriers. Regionally, Asia-Pacific dominates in volume due to large-scale port operations, while Europe leads in adoption with 46% of enterprises deploying electric and hybrid handling vehicles.

By 2027, predictive AI-based maintenance systems are expected to cut unplanned downtime by 32%, significantly enhancing throughput efficiency in high-volume ports. Firms are committing to ESG improvements, such as achieving a 40% reduction in port vehicle emissions by 2030, aligned with international climate targets. In 2024, Rotterdam Port achieved a 25% reduction in fuel consumption through AI-enabled vehicle routing and automation initiatives, setting a global benchmark for sustainable operations.

Looking forward, the Port & Material Handling Equipment Vehicle Market is poised to serve as a pillar of resilience, compliance, and sustainable growth. Its pathway emphasizes automation, digitization, and environmentally conscious investments that will define long-term competitiveness and ensure sustainable, technology-driven port ecosystems.

Global containerized trade surpassed 850 million TEUs in 2023, creating heightened demand for efficient cargo handling equipment. This surge is driving adoption of advanced vehicles such as automated guided vehicles (AGVs), reach stackers, and electric straddle carriers. Ports are investing heavily in modernization projects, with China alone allocating over USD 18 billion in 2023 for handling equipment upgrades. Increased reliance on just-in-time delivery models further emphasizes the need for efficiency, making high-capacity handling vehicles essential for maintaining port throughput. These vehicles are integral in reducing turnaround times, enhancing productivity by up to 25%, and ensuring supply chain continuity in the face of rising trade volumes.

The Port & Material Handling Equipment Vehicle Market faces challenges due to the high upfront cost of advanced vehicles, especially those equipped with electric or hybrid technologies. Autonomous handling systems and electrified fleets often require significant infrastructure upgrades, including charging stations, grid integration, and digital monitoring networks. Smaller and mid-sized ports struggle to justify these investments, slowing market penetration in certain regions. For instance, retrofitting traditional diesel-powered fleets with electric alternatives can cost up to 40% more, creating financial strain. Additionally, operational disruptions during infrastructure transition further limit adoption. These restraints highlight the difficulty of balancing modernization with financial feasibility for many operators.

The global push toward smart ports is opening substantial opportunities for the Port & Material Handling Equipment Vehicle Market. Digital integration of IoT, AI, and 5G technologies enables predictive maintenance, fleet tracking, and real-time cargo monitoring. By 2026, smart port projects are expected to improve operational efficiency by 30%, driving the need for connected handling vehicles. Investments in smart logistics corridors across Asia-Pacific and Europe are also creating demand for interoperable, digitally enabled fleets. Moreover, rising government incentives for electrification and carbon-neutral port initiatives are fueling opportunities for advanced equipment deployment. This convergence of smart technologies and sustainability goals ensures robust long-term growth potential.

The Port & Material Handling Equipment Vehicle Market faces growing challenges from global and regional regulations mandating stricter emission reductions. Compliance with IMO decarbonization strategies and EU emission standards requires significant investment in electric and hybrid vehicles, which not all operators can afford. Transitioning away from diesel fleets also presents logistical difficulties, as infrastructure for alternative fuels and charging remains unevenly distributed. Additionally, regulatory complexity across different jurisdictions complicates procurement strategies and slows adoption. Meeting sustainability targets—such as achieving a 50% reduction in emissions by 2030—requires coordinated industry-wide efforts. These challenges underscore the need for accelerated innovation, cost-efficient solutions, and harmonized policy frameworks.

Automation and Electrification in Port Vehicles: Automation and electrification are accelerating across major ports, with over 47% of new equipment orders in 2024 being electric or hybrid models. Automated guided vehicles (AGVs) have reduced container handling time by 31% compared to manual operations, while electrified straddle carriers are cutting emissions by nearly 40% in large European ports.

Integration of Digital Twin Technology: Adoption of digital twin systems in port operations has grown by 52% in the past three years. These platforms allow real-time simulation of handling vehicles, improving asset utilization by 28% and reducing equipment downtime by 22%. Ports in Asia-Pacific are leading this trend, where high-volume hubs require predictive analytics to support millions of TEUs annually.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Port & Material Handling Equipment Vehicle Market. Around 55% of new port infrastructure projects in 2024 integrated prefabricated elements, achieving cost savings of 20% and construction time reduction of 35%. Demand for high-precision vehicles to transport prefabricated materials is rising, particularly in North America and Europe.

5G and AI-Enabled Fleet Optimization: Deployment of 5G-enabled fleet systems has increased by 44% since 2022, enabling real-time monitoring of handling vehicles. AI-based optimization has reduced unproductive vehicle movement by 26% and improved port throughput efficiency by 19%. By 2026, it is expected that 60% of major container terminals will rely on AI-driven routing and scheduling to maximize operational efficiency.

The Port & Material Handling Equipment Vehicle Market is segmented by type, application, and end-user, each offering unique insights into industry adoption patterns. By type, container handling equipment leads due to its critical role in global containerized trade, followed by automated vehicles and forklifts. By application, container terminals dominate, while bulk cargo handling and inland logistics present growing opportunities. End-users span shipping companies, logistics operators, and industrial hubs, with shipping and logistics accounting for the largest share. Each segment is shaped by automation, electrification, and regulatory compliance, creating opportunities for innovation and efficiency in global cargo operations.

Container handling equipment currently holds the largest share, accounting for 41% of total market adoption. Its dominance is supported by the surge in global containerized trade surpassing 850 million TEUs in 2023. Automated guided vehicles (AGVs) represent the fastest-growing type, projected at a 12% CAGR, driven by their ability to cut operational costs by up to 30% and improve port productivity. Forklifts and reach stackers collectively contribute 27% of the market, mainly supporting smaller-scale cargo and inland logistics operations. Other specialized vehicles, such as straddle carriers and yard trucks, together hold a 32% share, serving niche operations.

Container terminals dominate the Port & Material Handling Equipment Vehicle Market with a 48% share, driven by rising global trade volumes and port modernization programs. Bulk cargo handling follows with 28%, propelled by increased demand for coal, grain, and ore transportation. The fastest-growing application is inland logistics, expanding at a 10% CAGR, fueled by the rise in intermodal transport corridors and smart logistics hubs. Warehousing and industrial cargo handling collectively represent the remaining 24%, serving as vital extensions of port infrastructure.

Shipping companies are the leading end-users, accounting for 43% of adoption, as they require high-capacity vehicles for containerized and bulk cargo handling. Logistics service providers hold 29% of the market, supported by the rapid expansion of intermodal freight corridors and demand for efficiency in inland distribution networks. The fastest-growing end-user group is industrial hubs, projected to grow at 11% CAGR, as manufacturing and energy industries increasingly adopt automated port vehicles to streamline material handling. Other end-users, including government-managed port authorities and special economic zones, collectively contribute 28%.

Asia-Pacific accounted for the largest market share at 44% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

Europe followed with 28% market share in 2024, supported by strong regulatory frameworks and adoption of electric handling vehicles. North America contributed 19% share, with growing demand in logistics hubs and bulk cargo terminals. South America held 5% share, largely concentrated in Brazil’s ports, while the Middle East & Africa collectively accounted for 4% share, driven by infrastructure projects in UAE, Saudi Arabia, and South Africa. Asia-Pacific’s leadership is reinforced by over 65% adoption of automated stacking cranes in China, 42% port modernization investments in India, and Japan’s 25% integration rate of AI-powered handling systems. North America is projected to see a 33% increase in electrified fleet deployment by 2028, while Europe is expected to achieve a 40% reduction in emissions by 2030, reshaping the competitive landscape of the Port & Material Handling Equipment Vehicle Market.

North America accounted for 19% of the Port & Material Handling Equipment Vehicle Market in 2024, driven by large-scale container terminals and inland logistics networks. Key industries such as automotive, retail, and e-commerce are fueling adoption of automated guided vehicles and electrified forklifts. Regulatory frameworks such as the U.S. Clean Ports Initiative encourage deployment of low-emission vehicles, while digital transformation is visible in AI-powered routing systems used in California’s major ports. A notable local player, Hyster-Yale, has introduced hydrogen-powered forklifts, enhancing sustainability in industrial cargo handling. Consumer behavior in the region reflects higher adoption of automation among healthcare and finance-linked logistics operators, with nearly 36% of enterprises prioritizing ESG-compliant equipment.

Europe held 28% share of the Port & Material Handling Equipment Vehicle Market in 2024, led by Germany, the UK, and France. The European Union’s strict emission reduction directives are accelerating the adoption of electrified port vehicles, with over 45% of new orders being hybrid or electric. Germany has spearheaded modernization with extensive use of automated straddle carriers, while the UK has invested heavily in AI-driven vehicle management systems. Konecranes, a leading European player, has advanced automation in container handling across Scandinavian ports. Consumer adoption in Europe is shaped by regulatory pressures, with over 40% of enterprises demanding equipment that provides explainable, trackable emissions reductions, aligning with regional ESG targets.

Asia-Pacific accounted for 44% of the Port & Material Handling Equipment Vehicle Market in 2024, making it the largest regional market. China, India, and Japan dominate consumption, supported by extensive port infrastructure investments and manufacturing growth. China’s container ports handled more than 280 million TEUs in 2023, requiring large-scale deployment of automated guided vehicles and electric stackers. India has invested in digital corridors linking ports with industrial hubs, while Japan has pioneered AI-powered predictive maintenance systems across port handling fleets. A key local player, ZPMC, leads in large container handling equipment manufacturing, supplying globally. Consumer behavior in the region reflects strong adoption by e-commerce-driven logistics companies, with over 50% of new handling equipment in Asia-Pacific being automation-ready by 2024.

South America accounted for 5% of the Port & Material Handling Equipment Vehicle Market in 2024, with Brazil and Argentina being the largest contributors. Infrastructure expansion in Brazil’s Santos Port and Argentina’s Rosario terminals is driving demand for modern cargo handling vehicles. Government-backed trade policies and port modernization projects are incentivizing electrified fleets, though adoption remains slower compared to other regions. Local operators in Brazil are integrating semi-automated yard trucks to improve bulk commodity handling, particularly in agricultural exports. Consumer behavior in the region shows higher adoption among logistics companies tied to commodity exports, with approximately 28% of equipment purchases linked to energy and agriculture-related cargo handling.

The Middle East & Africa held 4% of the Port & Material Handling Equipment Vehicle Market in 2024, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Energy-driven trade flows and large construction projects are propelling the need for advanced port vehicles. Modernization trends include adoption of hybrid reach stackers in UAE ports and digital monitoring systems across South African terminals. Local companies in Saudi Arabia have begun deploying automated container movers to support large-scale infrastructure projects linked to Vision 2030. Consumer adoption is tied to energy and construction industries, with 32% of enterprises investing in equipment aligned with trade diversification and environmental compliance.

China – 31% market share: Dominance driven by massive port handling capacity, large-scale deployment of automated cranes, and heavy investment in electrification of cargo vehicles.

Germany – 14% market share: Leadership supported by strict EU regulations, high adoption of electric handling vehicles, and advanced port automation systems across major terminals.

The Port & Material Handling Equipment Vehicle market is characterized by a moderately consolidated structure, with the top 5 players collectively accounting for nearly 42% of the market share in 2024. The market hosts over 120 active global and regional competitors, with varying levels of specialization across container handling, cargo vehicles, and automated port machinery. Global leaders maintain their dominance through strategic mergers and acquisitions, including cross-border partnerships with logistics operators and shipping companies. Product innovation is a key differentiator, with over 30% of competitors investing in autonomous and electrified handling vehicles to meet emission standards and improve port efficiency.

The competitive landscape is increasingly shaped by digital transformation trends, including the integration of AI-driven fleet management, IoT-enabled tracking systems, and predictive maintenance technologies. Strategic initiatives such as joint ventures with port authorities and long-term service agreements with shipping giants are driving market positioning for leading players. Regional competitors, especially in Asia-Pacific, are gaining ground by offering cost-effective and customized solutions. The entry of technology-driven startups, particularly in the automation and electrification segment, has further intensified competition. Overall, while the market shows signs of consolidation, the presence of a large number of regional specialists ensures a competitive balance that fosters innovation and price competitiveness.

Konecranes

Hyster-Yale Group

Terex Corporation

Jungheinrich AG

Kalmar

SANY Group

Mitsubishi Logisnext Co., Ltd.

Technological advancements are reshaping the Port & Material Handling Equipment Vehicle market, with automation, electrification, and digital integration driving the next phase of growth. A significant trend is the deployment of autonomous guided vehicles (AGVs), which are increasingly used in container terminals to reduce human error and improve efficiency. By 2024, nearly 35% of new port handling equipment deliveries included autonomous features, reflecting rising investment in AI-driven solutions.

Electrification is another key driver, as ports transition toward sustainability goals. Electric forklifts, cranes, and reach stackers now account for over 28% of equipment purchases globally, with demand accelerated by stricter emission regulations. Hybrid solutions are also gaining momentum, particularly in regions where infrastructure for charging remains under development. Digitalization plays a central role, with IoT-enabled fleet management systems providing real-time tracking, predictive maintenance, and data-driven decision-making.

5G-enabled connectivity is enhancing operational efficiency by enabling low-latency communication across port ecosystems, supporting synchronized operations of cranes, vehicles, and yard equipment. Blockchain adoption in logistics is also improving traceability and security of cargo handling processes. In addition, AI-powered vision systems are being integrated into vehicles for improved navigation, object detection, and safety compliance. Collectively, these emerging technologies are transforming the operational efficiency, sustainability, and reliability of port handling systems, ensuring long-term competitiveness in global trade infrastructure.

In March 2023, Konecranes launched a new generation of hybrid reach stackers designed to cut fuel consumption by up to 40%. The innovation leverages a hybrid diesel-electric powertrain to improve sustainability and reduce operational costs across port operations. Source: www.konecranes.com

In October 2023, Hyster-Yale unveiled an advanced hydrogen fuel cell-powered terminal tractor for heavy-duty port applications. The vehicle supports extended runtime, quick refueling, and aligns with the industry’s decarbonization goals. Source: www.hyster-yale.com

In April 2024, Liebherr introduced a fully electric mobile harbor crane capable of handling up to 200 tons of cargo. The innovation represents a significant step in reducing CO₂ emissions while maintaining high lifting performance. Source: www.liebherr.com

In July 2024, Toyota Material Handling expanded its smart logistics solutions with AI-driven fleet management software integrated into automated forklifts. The system optimizes routes, reduces idle times, and enhances overall throughput efficiency. Source: www.toyota-industries.com

The Port & Material Handling Equipment Vehicle Market Report provides an extensive analysis of the industry’s structure, dynamics, and strategic opportunities across global and regional markets. It covers a wide range of vehicle categories, including forklifts, terminal tractors, automated guided vehicles, reach stackers, and container handling equipment. The report also examines their deployment in ports, logistics hubs, warehouses, and large-scale manufacturing facilities, where cargo handling efficiency is a key determinant of operational success.

The geographical scope spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with in-depth coverage of leading markets such as the United States, Germany, China, and Brazil. Regional insights address consumption patterns, regulatory frameworks, infrastructure investments, and government initiatives shaping adoption.

The report emphasizes technological developments, from electrification and automation to AI, IoT integration, and hydrogen-powered solutions. It highlights emerging demand in niche areas such as smart ports and green logistics, where sustainability is a major driver. Market segmentation also considers applications by industry verticals including shipping, automotive, construction, e-commerce, and energy.

By providing detailed numerical insights into market share distribution, adoption rates, and product penetration levels, the report equips decision-makers with a holistic understanding of current trends, competitive positioning, and long-term opportunities in the Port & Material Handling Equipment Vehicle market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 23335.21 Million |

|

Market Revenue in 2032 |

USD 35272.71 Million |

|

CAGR (2025 - 2032) |

5.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Toyota Material Handling, Konecranes, Cargotec Corporation, Hyster-Yale Group, Terex Corporation, Liebherr Group, Jungheinrich AG, Kalmar, SANY Group, Mitsubishi Logisnext Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |