Reports

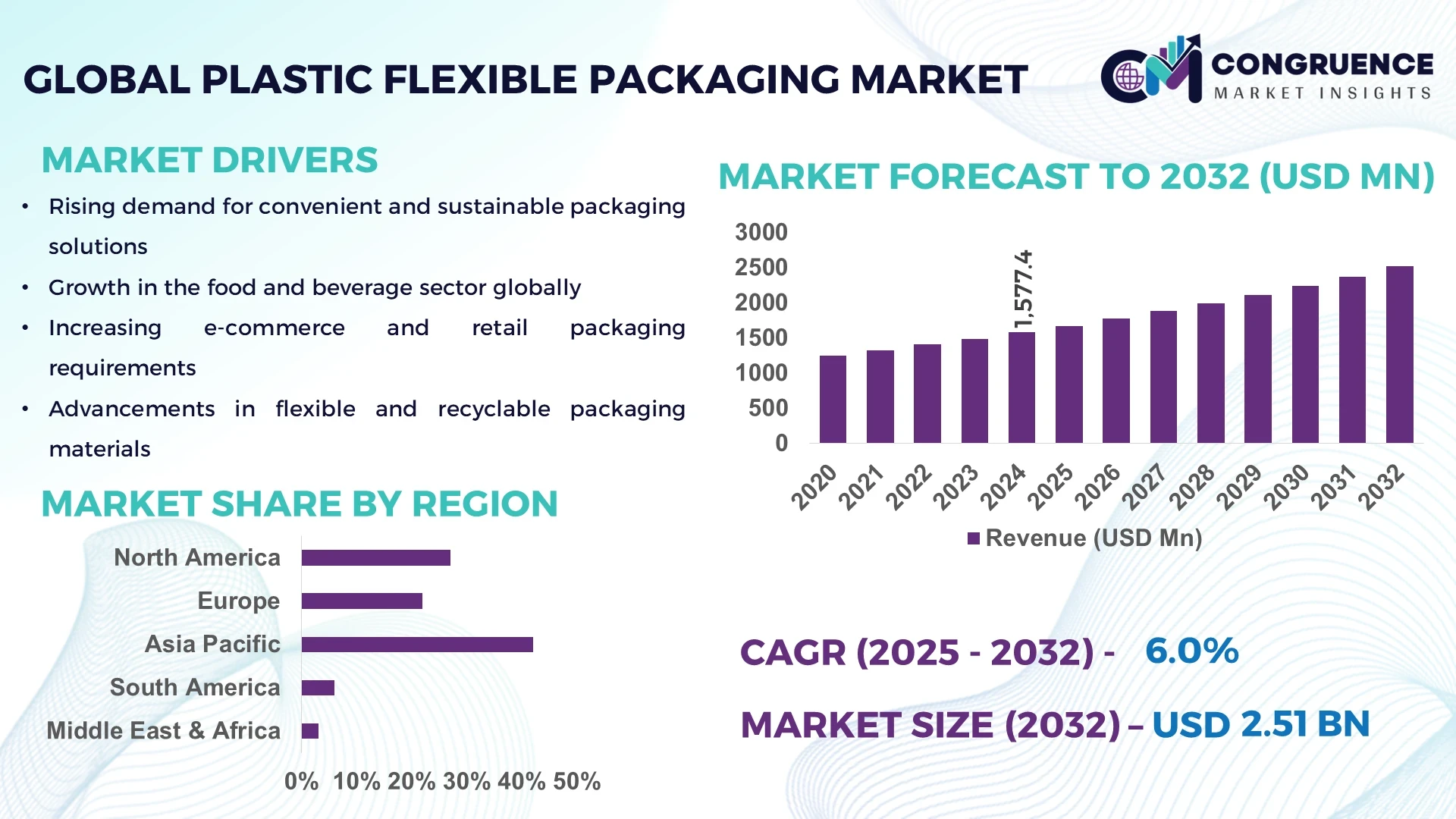

The Global Plastic Flexible Packaging Market was valued at USD 1,577.4 Million in 2024 and is anticipated to reach a value of USD 2,514.1 Million by 2032 expanding at a CAGR of 6.0% between 2025 and 2032.

China holds a leading position in the Plastic Flexible Packaging Market, with its advanced production infrastructure, extensive investment in automated manufacturing facilities, and significant application in fast-moving consumer goods and pharmaceutical sectors, supported by continuous adoption of eco-friendly technologies and digitalized supply chains.

The Plastic Flexible Packaging Market plays a pivotal role in industries including food and beverages, pharmaceuticals, personal care, and household products, with each sector contributing distinct applications that enhance product safety, extend shelf life, and improve transportation efficiency. Recent innovations include the integration of recyclable mono-material packaging and the adoption of bio-based plastics, aligning with stricter environmental regulations that encourage sustainable practices. Economic growth in emerging markets has accelerated regional consumption, particularly in Asia Pacific, while North America and Europe are witnessing increased adoption of high-barrier films for premium product categories. The market is further influenced by rising e-commerce activity, fueling demand for durable and lightweight packaging. Moving forward, the sector is expected to experience greater alignment with circular economy principles, enhanced digital printing for customization, and broader applications in medical and healthcare packaging, providing new avenues for technological advancements and investment.

Artificial Intelligence is increasingly transforming the Plastic Flexible Packaging Market by enhancing efficiency, reducing waste, and driving predictive capabilities in production and supply chain management. Manufacturers are utilizing AI-powered vision systems to identify defects in packaging films at speeds exceeding human capacity, thereby minimizing rejections and improving operational performance. Advanced machine learning algorithms are being deployed to forecast demand fluctuations across diverse end-use sectors, enabling companies to optimize production schedules and reduce excess inventory. AI-driven robotics in packaging lines are streamlining repetitive tasks, cutting changeover times, and ensuring consistent quality output, which is vital for industries with strict compliance requirements such as pharmaceuticals and food.

In addition, AI plays a critical role in material science within the Plastic Flexible Packaging Market. By analyzing massive datasets, AI tools are aiding in the formulation of new lightweight and sustainable polymers that retain essential barrier properties while reducing carbon footprint. Predictive maintenance powered by AI sensors has already demonstrated the ability to cut downtime in packaging plants by over 20%, leading to substantial cost savings and higher productivity. With growing emphasis on sustainability and efficiency, the integration of AI technologies is expected to redefine product innovation, distribution models, and consumer engagement strategies within the Plastic Flexible Packaging Market.

"In 2024, a leading European packaging manufacturer introduced an AI-enabled quality control system that reduced defect detection time for flexible plastic films by 35% while achieving an error identification accuracy rate above 98% during high-speed production runs."

The Plastic Flexible Packaging Market is shaped by a combination of technological innovation, regulatory pressures, and evolving consumer preferences. Demand is strongly influenced by the expansion of food and beverage distribution networks, where lightweight, durable, and protective packaging solutions are prioritized. At the same time, sustainability initiatives and strict environmental standards are accelerating the transition toward recyclable and bio-based materials. Innovation in smart packaging, digital printing, and barrier coatings is opening new possibilities across healthcare, personal care, and industrial applications. Additionally, regional growth patterns show that Asia Pacific leads in production, while Europe and North America are adopting advanced automation technologies to improve efficiency and reduce environmental impact.

The rapid expansion of online retail and food delivery services has significantly impacted the Plastic Flexible Packaging Market. Flexible plastics are being favored for their lightweight structure, durability, and ability to protect goods during transportation. E-commerce growth has increased the demand for pouches, courier bags, and resealable packaging, with packaging plants investing in automation to meet surging order volumes. In the food delivery sector, flexible packaging ensures freshness and minimizes leakage during transit. Rising consumer preference for convenience-oriented products is also encouraging innovations in portion-controlled packs and resealable options. This shift is driving consistent demand growth for plastic flexible solutions across developed and developing markets.

The Plastic Flexible Packaging Market faces restraints due to increasingly stringent global regulations on single-use plastics. Governments in regions such as Europe and North America have implemented policies restricting the use of non-recyclable packaging, requiring significant investment in research and compliance from manufacturers. These restrictions increase operational costs and slow product approvals, particularly for applications in food and beverages where barrier properties are critical. Additionally, the availability of cost-effective substitutes such as paper-based or compostable packaging materials adds competitive pressure. Manufacturers must balance regulatory compliance with maintaining product performance, creating a challenging environment for growth in certain market segments.

Sustainability presents a major opportunity in the Plastic Flexible Packaging Market, with increasing consumer and corporate commitment to reducing environmental impact. Investments in recyclable mono-material packaging and compostable bioplastics are gaining traction. Technological advancements in chemical recycling are enhancing the ability to reprocess plastic waste into high-quality raw materials suitable for food-grade applications. Brands are leveraging sustainable packaging as a differentiator in competitive markets, particularly in the food, beverage, and personal care sectors. The rising adoption of closed-loop recycling systems and circular economy initiatives across Europe and Asia Pacific further opens doors for long-term growth opportunities in this market.

One of the most pressing challenges in the Plastic Flexible Packaging Market is the high cost associated with adopting advanced manufacturing technologies. Equipment for AI-driven quality control, high-barrier film production, and sustainable polymer processing requires substantial capital investment, often limiting accessibility for small and medium enterprises. Additionally, the maintenance and training costs linked with advanced systems create operational hurdles. For large multinational firms, scaling these technologies across diverse production facilities adds further complexity. The necessity to meet evolving consumer preferences and regulatory demands while managing cost efficiency remains a difficult balancing act for industry participants.

Integration of Smart Packaging Technologies: The Plastic Flexible Packaging Market is experiencing a rise in the use of smart packaging solutions, such as embedded QR codes, RFID tags, and freshness indicators. These innovations allow enhanced product traceability, consumer engagement, and quality assurance, particularly in food and pharmaceuticals. Companies are increasingly adopting digital printing and connected packaging strategies to deliver personalized customer experiences and gather real-time consumption data.

Growth in High-Barrier Films for Premium Applications: The demand for high-barrier films is accelerating as industries such as pharmaceuticals, nutraceuticals, and premium food products require packaging that preserves product integrity and extends shelf life. These films offer superior protection against oxygen and moisture penetration, making them ideal for sensitive goods. Recent advancements in co-extrusion and nanotechnology are further enhancing barrier performance, driving adoption across both developed and emerging markets.

Advancements in Biodegradable and Compostable Plastics: Growing environmental awareness is spurring investment in biodegradable and compostable plastic packaging. Manufacturers are focusing on developing solutions that meet regulatory guidelines while maintaining strength, flexibility, and barrier functionality. Adoption is particularly strong in Europe, where strict waste management policies and consumer preference for eco-friendly packaging drive innovation and deployment of bio-based alternatives.

Digitalization and Automation in Production Processes: The Plastic Flexible Packaging Market is witnessing increasing digitalization of production lines, where AI-powered systems and robotics improve throughput, reduce material waste, and enable predictive maintenance. Smart factories integrating Industrial IoT solutions are achieving higher levels of efficiency and consistency. This digital transformation is not only lowering costs but also enabling manufacturers to respond rapidly to customization demands in fast-moving consumer goods and e-commerce packaging segments.

The Plastic Flexible Packaging Market is segmented by type, application, and end-user, each offering distinct insights into how the industry evolves to meet diverse demands. By type, categories such as pouches, bags, wraps, films, and sachets dominate, with innovations in barrier properties and recyclability shaping their adoption. Applications are wide-ranging, spanning food and beverages, pharmaceuticals, personal care, and industrial packaging, reflecting the market’s broad relevance to global supply chains. End-user insights reveal critical consumption patterns, with fast-moving consumer goods and healthcare remaining at the forefront, while e-commerce and retail contribute rapidly growing demand. This segmentation highlights the market’s adaptability, technological progress, and alignment with shifting consumer expectations across industries.

The Plastic Flexible Packaging Market comprises pouches, bags, wraps, films, sachets, and other specialized formats. Among these, pouches remain the leading type, driven by their versatility, lightweight structure, and suitability for food and beverage packaging. They provide strong sealing performance and convenient resealability, which enhances shelf life and consumer convenience. Films represent the fastest-growing segment, propelled by their widespread use in automated packaging lines, compatibility with digital printing, and ability to serve as high-barrier solutions for sensitive products such as pharmaceuticals and premium food items. Bags and wraps continue to play a vital role in transporting bulk and retail goods, especially in consumer and industrial markets where durability is critical. Sachets, while smaller in scale, are particularly relevant in personal care and sample distribution, catering to single-use and travel-friendly packaging. Each type addresses distinct needs, but the overarching trend emphasizes innovation in recyclable materials and advanced manufacturing technologies to reduce environmental impact and improve performance.

Applications of plastic flexible packaging cover food and beverages, pharmaceuticals, personal care and cosmetics, household products, and industrial uses. Food and beverages dominate the market, as flexible plastics ensure freshness, provide lightweight transportation benefits, and meet the rising demand for portion-controlled packaging. This sector leverages advancements in resealable pouches and high-barrier films to meet consumer expectations for convenience and product safety. Pharmaceutical packaging emerges as the fastest-growing application, supported by increasing global healthcare needs, stricter regulations for product protection, and the rise of unit-dose formats for medicines. Personal care and cosmetics rely on innovative designs and portability, driving growth in sachets and sample packs. Household products benefit from flexible plastic packaging due to ease of storage, spill prevention, and durability. Industrial applications, although more niche, utilize robust wraps and films for logistics and bulk handling. Overall, applications highlight the adaptability of flexible plastics across sectors, underscoring their essential role in modern supply chains.

End-users of the Plastic Flexible Packaging Market include fast-moving consumer goods (FMCG), healthcare, retail and e-commerce, and industrial sectors. FMCG remains the leading end-user, as global consumption of packaged foods, beverages, and household essentials drives consistent demand. The segment benefits from increasing urbanization and lifestyle changes that prioritize convenience. Healthcare stands out as the fastest-growing end-user, with rising requirements for tamper-proof, contamination-resistant, and high-barrier packaging for medicines and medical devices. Growth in this segment is also fueled by aging populations and expanded pharmaceutical distribution channels. Retail and e-commerce contribute significantly as packaging plays a crucial role in ensuring product protection and efficient delivery in growing online marketplaces. Industrial end-users, though smaller in scale, utilize flexible plastics for protective wrapping, storage, and bulk shipping, particularly in manufacturing and logistics. Together, these end-user insights demonstrate how flexible plastics serve both essential consumer needs and specialized industry requirements, reinforcing their integral role in diverse global markets.

Asia-Pacific accounted for the largest market share at 42% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

The Asia-Pacific region benefits from large-scale production facilities, high consumer demand, and investments in sustainable packaging, while North America is experiencing rapid growth due to technological advancements, strict regulatory compliance, and an expanding e-commerce ecosystem. Europe continues to evolve with strong sustainability mandates, while South America and the Middle East & Africa are emerging as promising regions fueled by infrastructure development, urbanization, and rising consumer markets.

North America represented 27% of the global Plastic Flexible Packaging Market share in 2024, supported by strong demand from the food and beverage, pharmaceutical, and personal care industries. The United States leads the region with advanced packaging infrastructure, while Canada is making strides in sustainable packaging solutions. Regulatory changes encouraging recyclability and reduced plastic waste have spurred investment in eco-friendly alternatives. Additionally, the adoption of digital transformation technologies, including AI-driven quality monitoring and smart printing, is enhancing packaging efficiency and customization. The region is also experiencing growth in e-commerce, further boosting demand for durable, lightweight, and protective flexible plastic packaging.

Europe accounted for 22% of the Plastic Flexible Packaging Market share in 2024, with Germany, the UK, and France as the primary contributors. The region is heavily influenced by regulatory bodies promoting circular economy practices, including strict guidelines on recyclability and waste reduction. European manufacturers are pioneering the development of biodegradable and compostable packaging materials, positioning the region at the forefront of sustainability. Adoption of emerging technologies such as high-barrier films and advanced co-extrusion processes is increasing across industries. Furthermore, digitalization in printing and labeling is supporting greater customization and consumer engagement, reinforcing Europe’s role as a hub for sustainable innovation.

Asia-Pacific held the largest volume share, accounting for 42% of the Plastic Flexible Packaging Market in 2024, driven by leading consumers such as China, India, and Japan. China dominates with its large-scale manufacturing base and advanced supply chain networks, while India is rapidly expanding capacity to meet demand in food, pharmaceuticals, and personal care sectors. Japan’s emphasis on high-quality packaging for electronics and consumer goods further strengthens the regional outlook. Investments in infrastructure and manufacturing technology, including smart factories and automation, are expanding rapidly. Asia-Pacific is also emerging as a global innovation hub, particularly in sustainable materials and digitalized production processes.

South America accounted for 6% of the Plastic Flexible Packaging Market share in 2024, with Brazil and Argentina being the key contributors. Brazil’s strong food processing industry and Argentina’s agricultural exports create steady demand for flexible packaging solutions. Infrastructure growth and expanding urban populations are boosting packaging consumption, particularly in ready-to-eat and household products. Government incentives for manufacturing investments and favorable trade policies are encouraging regional production. The adoption of lightweight, cost-efficient plastic packaging is increasing, especially in the retail and beverage sectors, where flexible formats offer superior shelf appeal and transport efficiency.

The Middle East & Africa region accounted for 3% of the Plastic Flexible Packaging Market share in 2024, with the UAE and South Africa emerging as notable growth centers. Packaging demand is being fueled by industries such as oil and gas, construction, and consumer goods, where flexible solutions offer cost efficiency and durability. Governments across the Gulf are promoting modernization in manufacturing, including the integration of automated and digital systems in packaging lines. Trade partnerships with Europe and Asia are also increasing product flow and investment in sustainable packaging solutions. Local regulations encouraging diversification beyond hydrocarbons are opening opportunities for broader adoption of innovative packaging technologies.

China – 28% Market Share

High production capacity and extensive manufacturing infrastructure make China the leading country in the Plastic Flexible Packaging Market.

United States – 19% Market Share

Strong end-user demand in pharmaceuticals, food, and e-commerce, combined with advanced packaging technologies, supports the United States’ position in the market.

The Plastic Flexible Packaging Market is highly competitive, with over 200 active players operating at global, regional, and local levels. Competition is shaped by product innovation, sustainability initiatives, and supply chain integration. Market leaders maintain strong positioning through diversified product portfolios and established customer bases in food, beverages, pharmaceuticals, and e-commerce. Mid-tier players focus on niche offerings such as biodegradable films, while emerging entrants are leveraging eco-friendly technologies to capture attention in environmentally conscious markets. Strategic initiatives remain a critical component of competition, with numerous mergers, acquisitions, and joint ventures aimed at expanding production capacity and geographic presence. Product launches in high-barrier films and compostable packaging solutions reflect the industry’s shift toward sustainable alternatives. Innovation trends such as digital printing, smart packaging, and advanced co-extrusion techniques are further intensifying rivalry. The competitive landscape is defined not only by price but also by differentiation in technology, sustainability performance, and customer-centric solutions, creating a dynamic environment where constant innovation is required to sustain market leadership.

Amcor plc

Sealed Air Corporation

Berry Global Inc.

Huhtamaki Oyj

Mondi Group

Sonoco Products Company

Constantia Flexibles

UFlex Ltd.

Coveris Holdings

Clondalkin Group

Technology continues to play a transformative role in the Plastic Flexible Packaging Market, reshaping product development, manufacturing processes, and end-user applications. One of the most significant advances is the integration of biodegradable and compostable polymers, which are increasingly being adopted to reduce environmental impact. Advanced barrier films, incorporating nanotechnology and multilayer co-extrusion, have gained traction by extending shelf life and enhancing protection for sensitive products such as pharmaceuticals and perishable foods.

Digital printing technology has emerged as a game-changer, enabling mass customization, shorter production runs, and faster time-to-market. This innovation is particularly beneficial for e-commerce packaging, where branding and personalization are key competitive differentiators. Automation and smart factory solutions are being widely implemented, optimizing operational efficiency, reducing wastage, and improving quality control. In addition, the rise of active and intelligent packaging—which includes QR codes, freshness indicators, and temperature-sensitive labels—is enhancing traceability and consumer engagement.

Sustainability-focused innovations are at the forefront, with companies investing heavily in recyclable mono-material packaging and bio-based resins. Data suggests that nearly 30% of new product developments in 2023–2024 incorporated some form of eco-friendly material innovation, highlighting the sector’s responsiveness to regulatory and consumer pressure. Emerging technologies such as blockchain-enabled supply chain transparency and AI-driven predictive maintenance in production are further influencing competitiveness. Collectively, these technological advancements are positioning the market for long-term evolution, balancing performance, cost-efficiency, and sustainability.

In March 2023, Amcor launched a high-barrier recyclable film designed for food packaging applications. The innovation delivers the same product protection as multi-material laminates but is fully recyclable, supporting industry-wide goals to improve material circularity.

In July 2023, Mondi introduced a recyclable flexible pouch for premium pet food packaging in Europe. The pouch combines durability with high-barrier protection while meeting growing consumer demand for environmentally responsible packaging.

In February 2024, Huhtamaki opened a new state-of-the-art manufacturing unit in Malaysia, focused on producing sustainable and lightweight plastic flexible packaging for food and personal care industries in the Asia-Pacific region.

In May 2024, Berry Global unveiled its new mono-material flexible packaging range for household products, featuring up to 70% post-consumer recycled content. The development highlights the industry’s transition toward circular packaging systems.

The scope of the Plastic Flexible Packaging Market Report encompasses a comprehensive analysis of industry trends, product innovations, and regional market dynamics across all major segments. The report covers market segmentation by type, including pouches, bags, wraps, films, and sachets, with detailed assessments of their applications across food and beverages, pharmaceuticals, personal care, household products, and industrial sectors. It also evaluates the role of end-users such as FMCG, healthcare, retail, and e-commerce, highlighting shifts in consumer demand and industry focus.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into both mature and emerging economies. Regional coverage includes country-level analysis of key markets such as the United States, China, India, Germany, Brazil, and the UAE, enabling decision-makers to understand growth drivers and regional opportunities.

From a technological perspective, the report investigates emerging innovations in recyclable materials, bio-based resins, nanotechnology-enhanced barrier films, and digital printing solutions. It also explores automation trends, smart packaging integration, and sustainability-focused product design, which are reshaping industry standards.

In addition to mainstream trends, the scope also considers niche segments, such as compostable packaging for organic food and high-performance packaging for pharmaceuticals and electronics. The analysis provides a holistic view of competitive dynamics, regulatory impacts, and supply chain shifts, ensuring stakeholders gain actionable insights into market opportunities, risks, and innovation pathways. This structured coverage ensures decision-makers have a clear roadmap for strategic planning, investment prioritization, and long-term market positioning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,577.4 Million |

| Market Revenue (2032) | USD 2,514.1 Million |

| CAGR (2025–2032) | 6.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Amcor plc, Sealed Air Corporation, Berry Global Inc., Huhtamaki Oyj, Mondi Group, Sonoco Products Company, Constantia Flexibles, UFlex Ltd., Coveris Holdings, Clondalkin Group |

| Customization & Pricing | Available on Request (10% Customization is Free) |